1-95

EXERCISE 1-21B (cont.)

g.

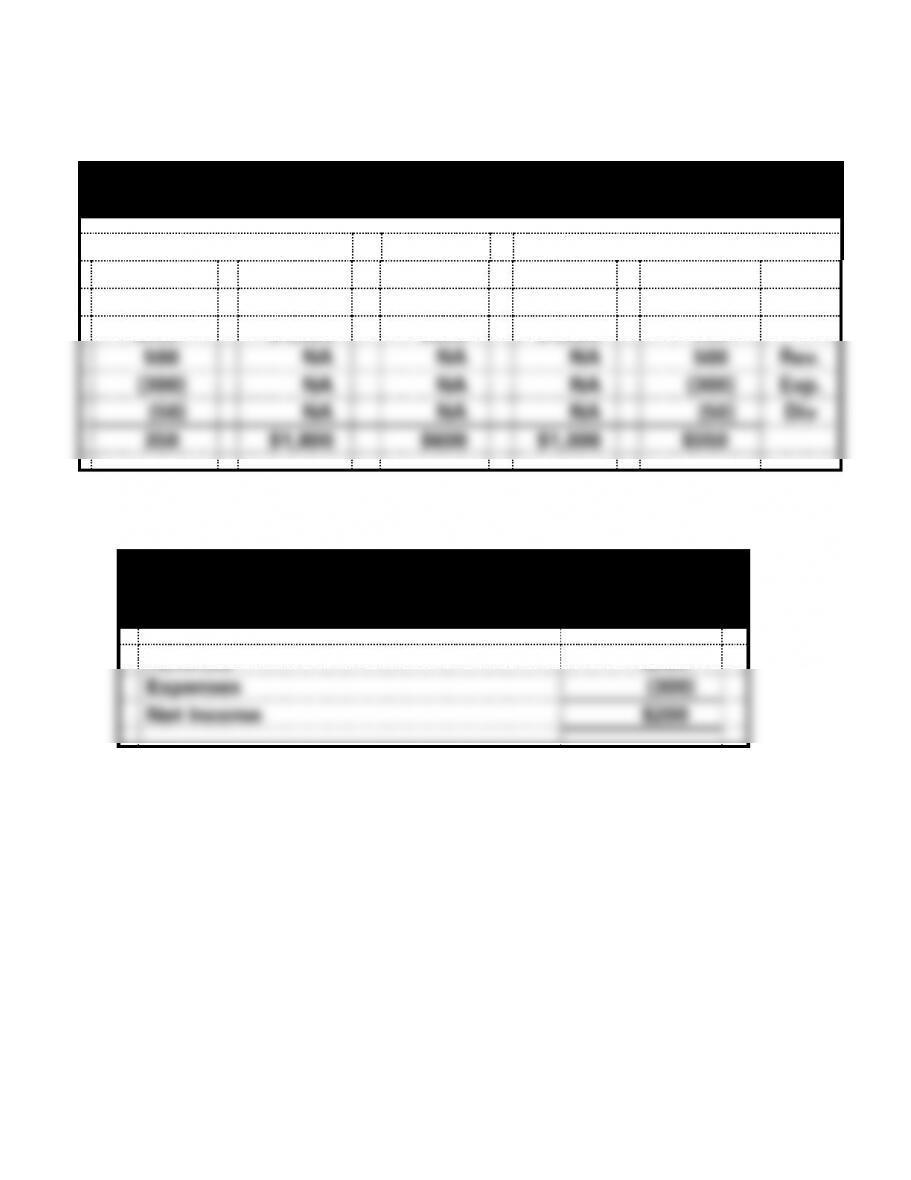

Zeke Company

Accounting Equation as of December 31, 2016

Assets

=

Liabilities

+

Stockholders’ Equity

Notes

Common

Retained

Cash

+

Land

=

Payable

+

Stock

+

Earnings

$200

$1,800

$600

$1,000

400

500

NA

NA

NA

500

Rev.

(300)

NA

NA

NA

(300)

Exp.

(50)

NA

NA

NA

(50)

Div

350

$1,800

$600

$1,000

$550

Zeke Company

Income Statement

For the Year Ended December 31, 2016

Revenue

$500

Expenses

(300)

Net Income

$200

1-96

EXERCISE 1-21B g. (cont,)

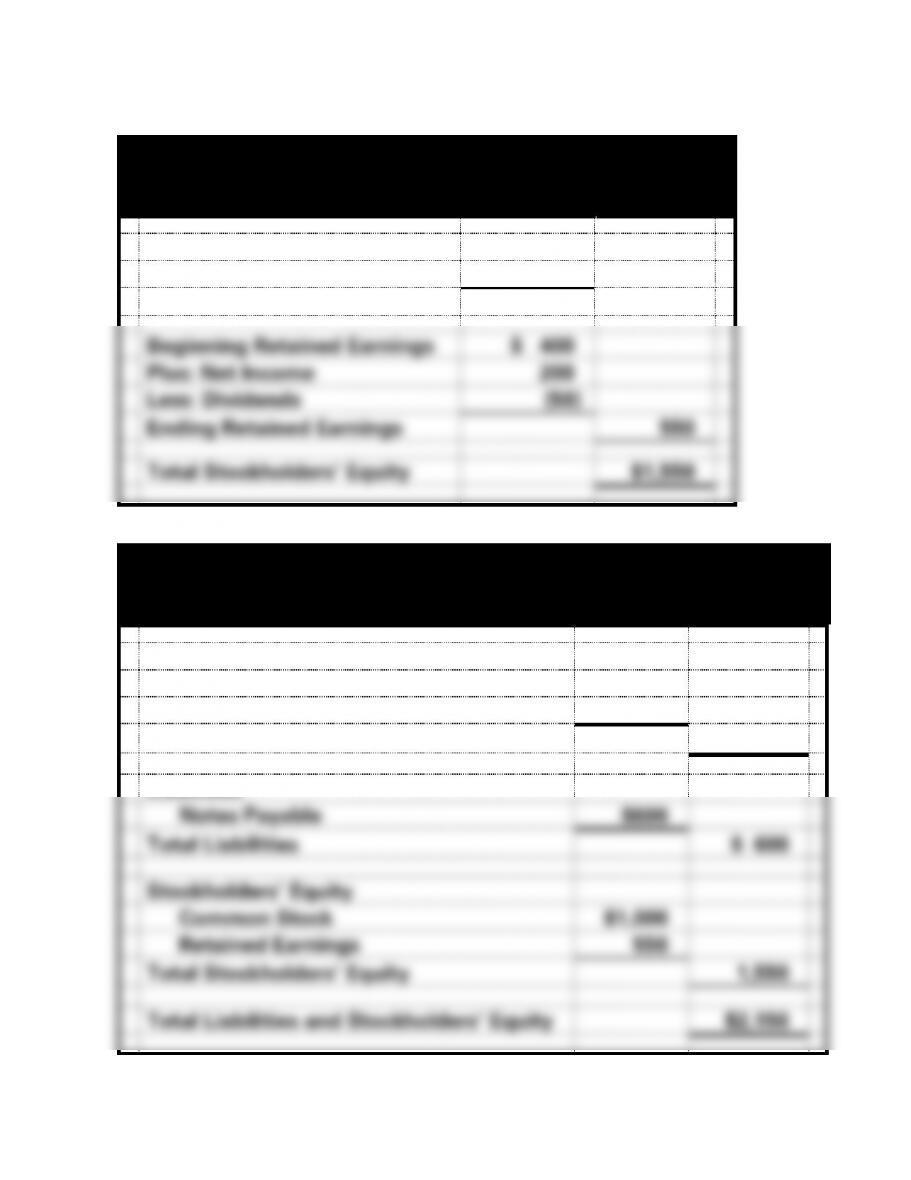

Zeke Company

Statement of Changes in Stockholders’ Equity

For the Year Ended December 31, 2016

Beginning Common Stock

$1,000

Plus: Common Stock Issued

-0-

Ending Common Stock

$1,000

Beginning Retained Earnings

$ 400

Plus: Net Income

200

Less: Dividends

(50)

Ending Retained Earnings

550

Total Stockholders’ Equity

$1,550

Zeke Company

Balance Sheet

As of December 31, 2016

Assets

Cash

$ 350

Land

1,800

Total Assets

$2,150

Liabilities

Notes Payable

$600

Total Liabilities

$ 600

Stockholders’ Equity

Common Stock

$1,000

Retained Earnings

550

Total Stockholders’ Equity

1,550

Total Liabilities and Stockholders’ Equity

$2,150

1-97

EXERCISE 1-21B g.(cont.)

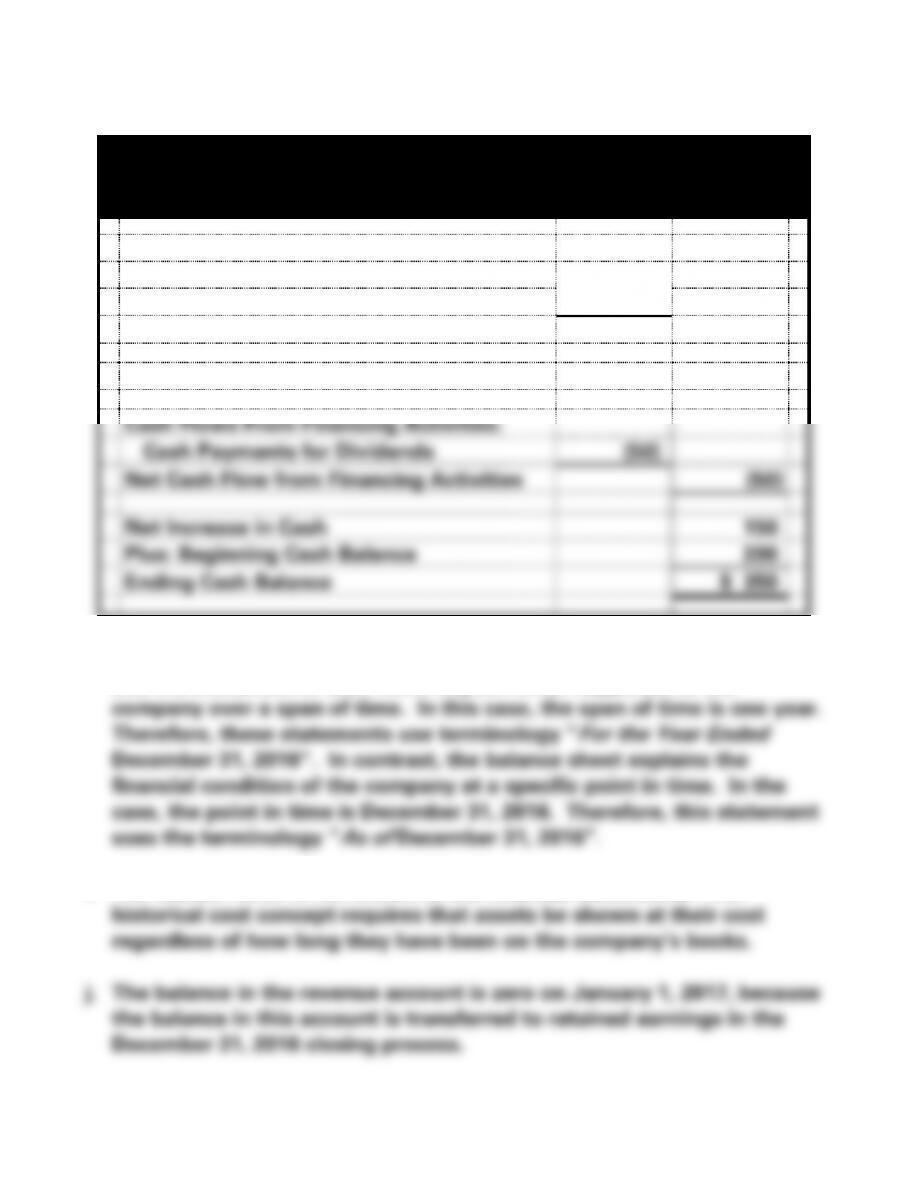

Zeke Company

Statement of Cash Flows

For the Year Ended December 31, 2016

Cash Flows From Operating Activities:

Cash Receipts from Customers

$500

Cash Payments for Expenses

(300)

Net Cash Flow from Operating Activities

$ 200

Cash Flows From Investing Activities:

0

Cash Flows From Financing Activities:

Cash Payments for Dividends

(50)

Net Cash Flow from Financing Activities

(50)

Net Increase in Cash

150

Plus: Beginning Cash Balance

200

Ending Cash Balance

$ 350

h. The income statement, statement of changes in stockholders’ equity

and the statement of cash flows explain what happened to the

i. The market value is not shown in the financial statements. The

EXERCISE 1-22B

a. Since the amount in the Notes Payable account increased from zero

to $3,000, Shundra, Inc. must have received a cash inflow of $3,000

from the issue of the note payable. Similarly, since the balance in

the common stock account increased from $2,500 to $8,000,

1-99

EXERCISE 1-22B c. (cont.)

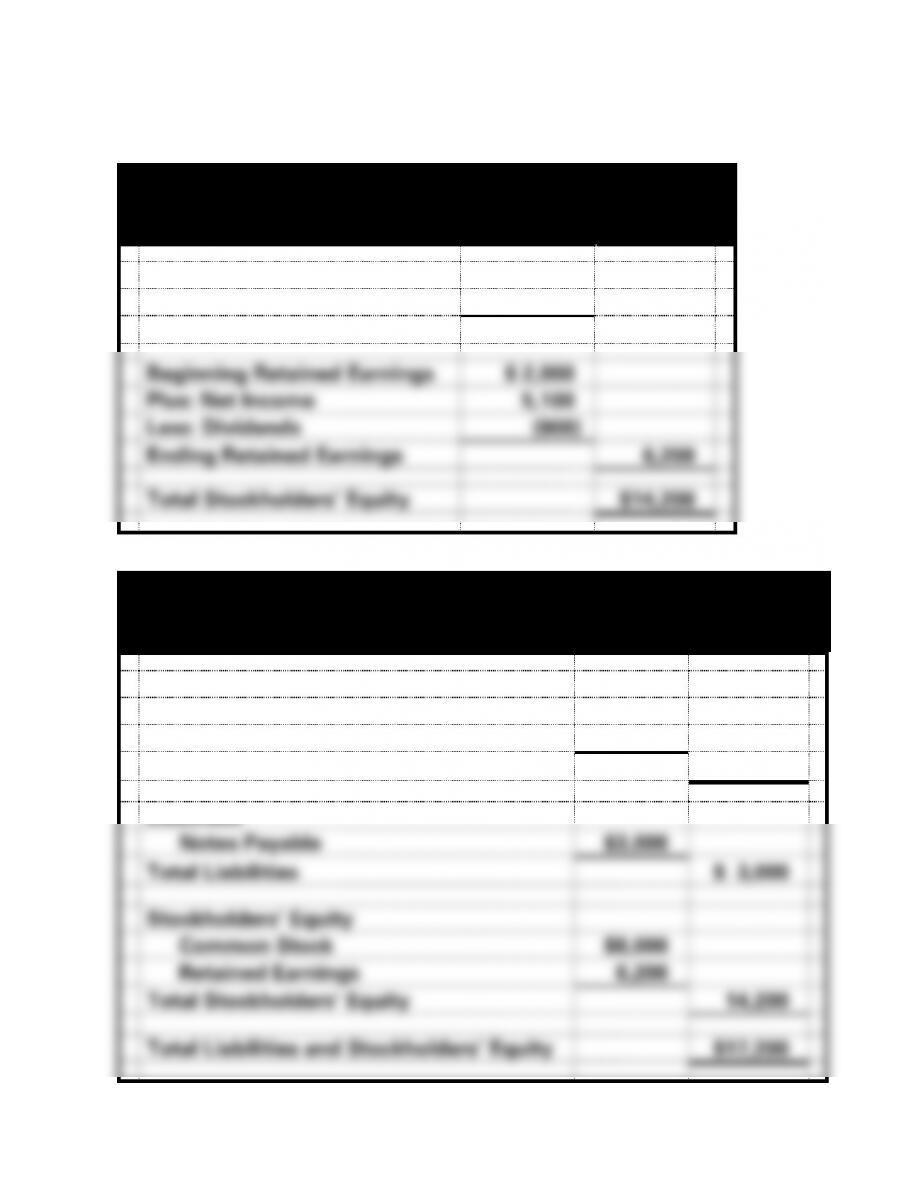

Shundra, Inc.

Statement of Changes in Stockholders’ Equity

For the Year Ended December 31, 2016

Beginning Common Stock

$ 2,500

Plus: Common Stock Issued

5,500

Ending Common Stock

$8,000

Beginning Retained Earnings

$ 2,000

Plus: Net Income

5,100

Less: Dividends

(900)

Ending Retained Earnings

6,200

Total Stockholders’ Equity

$14,200

Shundra, Inc.

Balance Sheet

As of December 31, 2016

Assets

Cash

$ 4,200

Land

13,000

Total Assets

$17,200

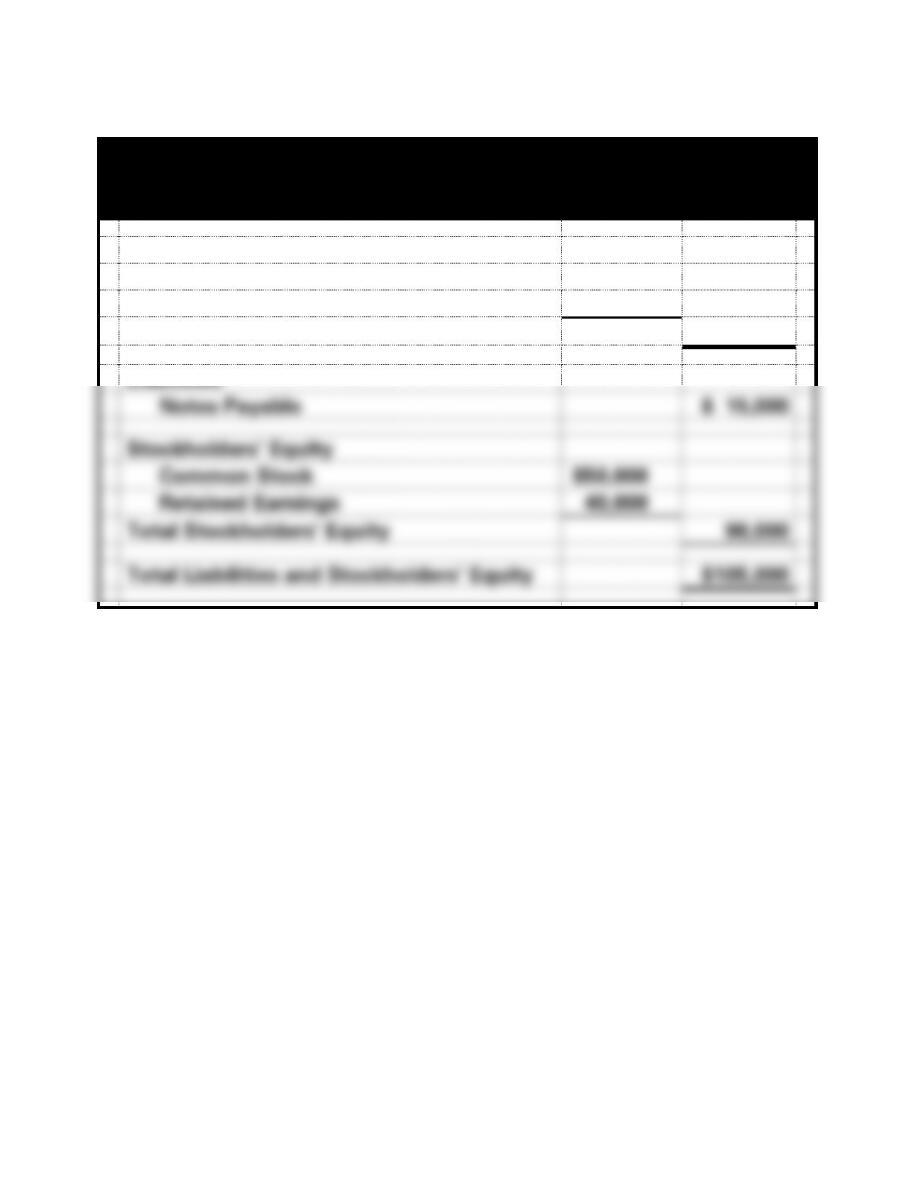

Liabilities

Notes Payable

$3,000

Total Liabilities

$ 3,000

Stockholders’ Equity

Common Stock

$8,000

Retained Earnings

6,200

Total Stockholders’ Equity

14,200

Total Liabilities and Stockholders’ Equity

$17,200

1-100

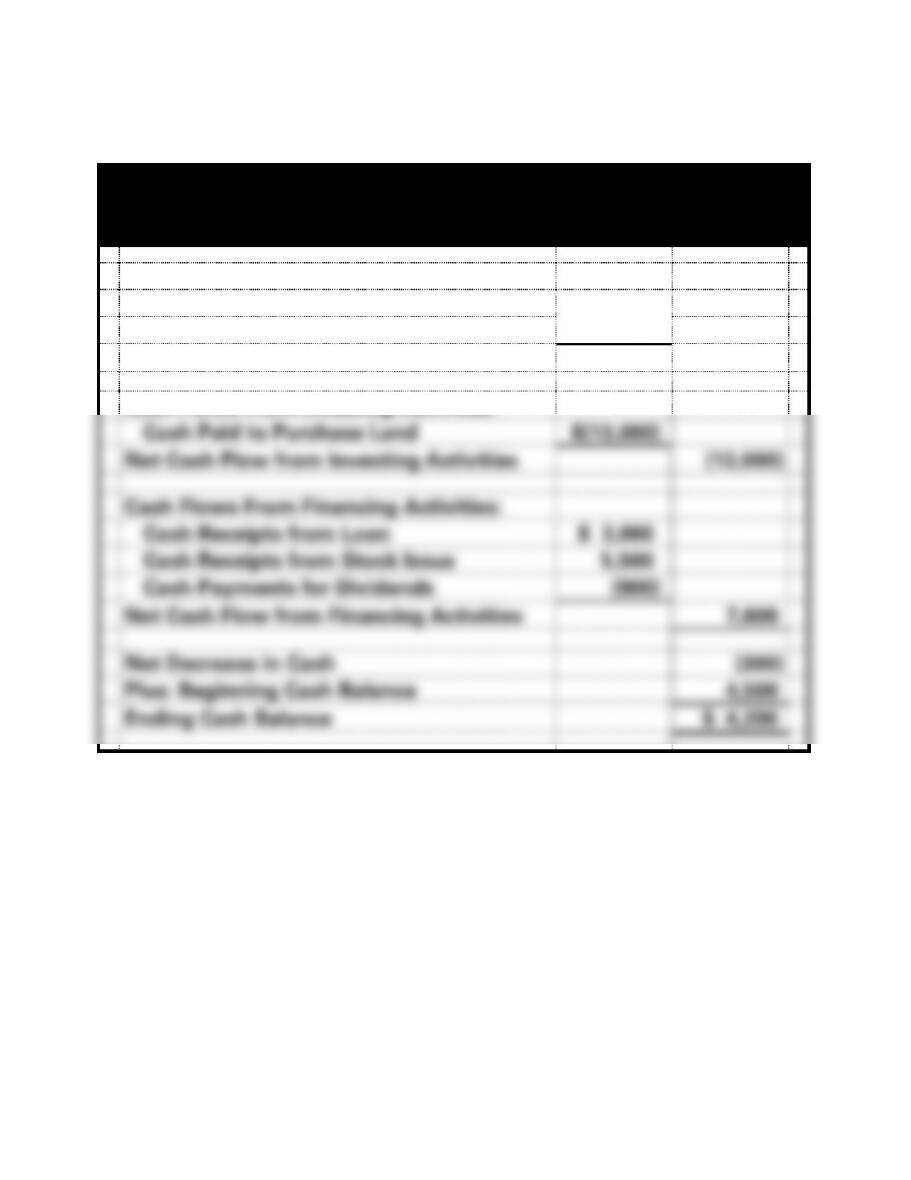

EXERCISE 1-22B c. (cont.)

Shundra, Inc.

Statement of Cash Flows

For the Year Ended December 31, 2016

Cash Flows From Operating Activities:

Cash Receipts from Customers

$ 9,900

Cash Payments for Expenses

(4,800)

Net Cash Flow from Operating Activities

$ 5,100

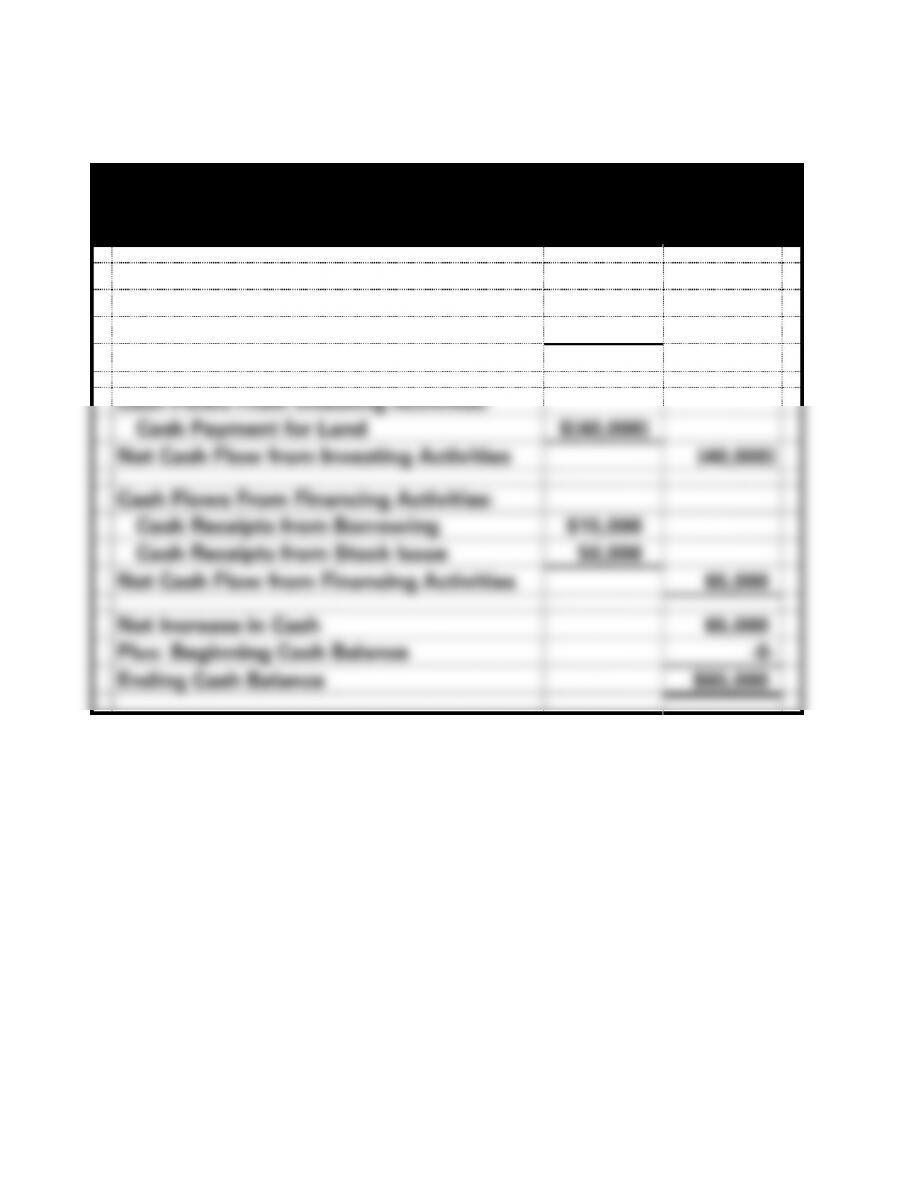

Cash Flows From Investing Activities:

Cash Paid to Purchase Land

$(13,000)

Net Cash Flow from Investing Activities

(13,000)

Cash Flows From Financing Activities:

Cash Receipts from Loan

$ 3,000

Cash Receipts from Stock Issue

5,500

Cash Payments for Dividends

(900)

Net Cash Flow from Financing Activities

7,600

Net Decrease in Cash

(300)

Plus: Beginning Cash Balance

4,500

Ending Cash Balance

$ 4,200

1-101

EXERCISE 1-23B

a.

Big Horn Company

Accounting Equation as of December 31, 2016

Assets

=

Liabilities

+

Common Stock

+

Retained Earnings

$100,000

$30,000

$50,000

?

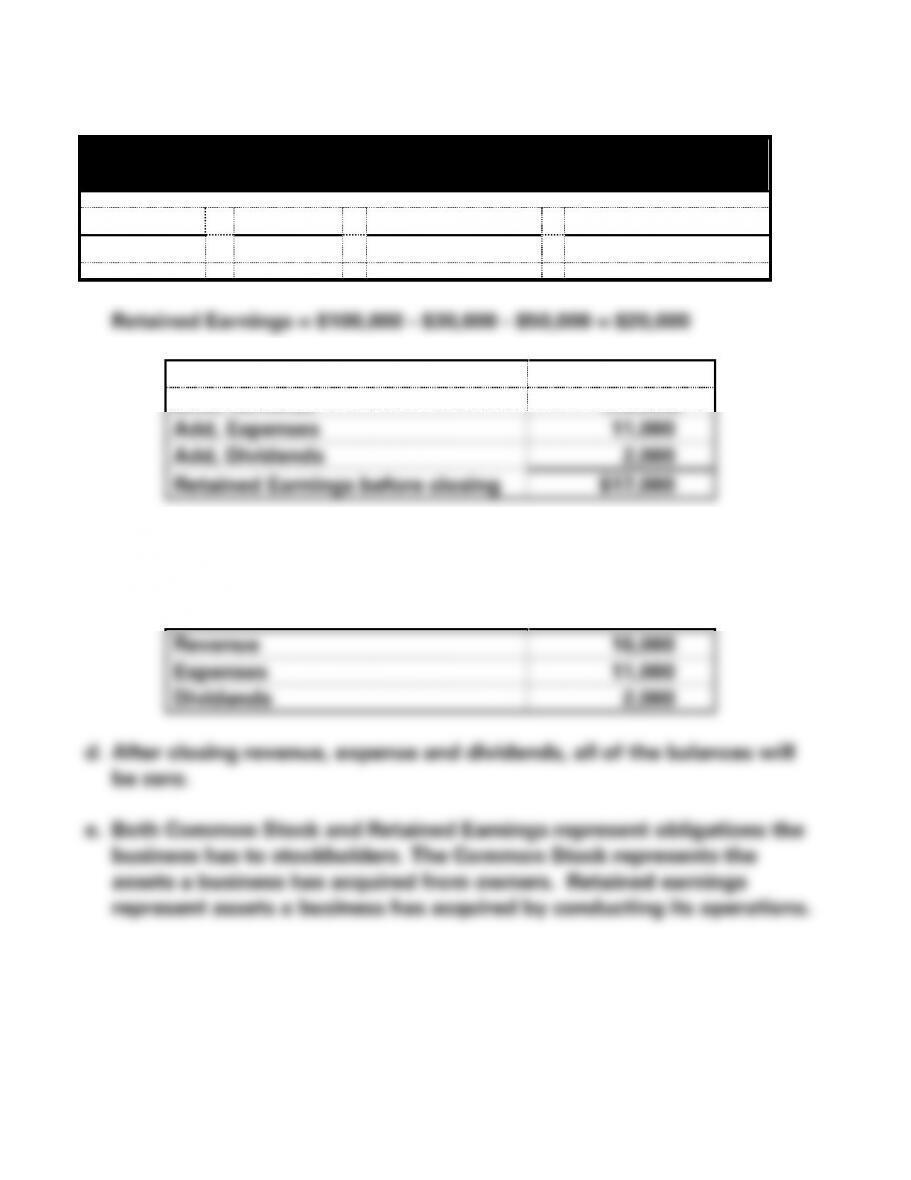

Retained Earnings after closing:

$20,000

Less, Revenue

(16,000)

Add, Expenses

11,000

Add, Dividends

2,000

Retained Earnings before closing

$17,000

b. Retained Earnings after closing is $20,000 (see the equation above).

c. The balances in revenue, expense and dividends before closing are:

Revenue

16,000

Expenses

11,000

Dividends

2,000

d. After closing revenue, expense and dividends, all of the balances will

be zero.

e. Both Common Stock and Retained Earnings represent obligations the

business has to stockholders. The Common Stock represents the

assets a business has acquired from owners. Retained earnings

represent assets a business has acquired by conducting its operations.

1-102

EXERCISE 1-23B (cont.)

f. The owners are no better off immediately after they contributed capital

to the business. While equity increased $40,000, the amount invested

1-103

EXERCISE 1-24B

a.

Year

Cash

Revenues

Cash

Expenses

Net

Income

Retained

Earnings

2016

$40,000

$21,000

19,000

19,000

2017

50,000

32,000

18,000

37,000

2018

70,000

48,000

22,000

59,000

Year

Cash

Revenues

Cash

Expenses

Net

Income

Retained

Earnings

2016

$40,000

$21,000

19,000

19,000

2017

50,000

32,000

18,000

31,000*

2018

70,000

48,000

22,000

53,000**

1-104

EXERCISE 1-25B

a. The balance in the Retained Earnings account as of January 31, 2016

is zero.

Explanation: The revenue is recorded in the Revenue account and is not transferred into

retained until the year-end closing process is accomplished.

is $56,600 ($4,600 + $52,000). The December 31, 2016 before closing

balance in the Expense account is $45,000 ($3,000 + $42,000).

Explanation: The revenue and expense amounts accumulate in the Revenue and

Expense accounts throughout the year.

e. The January 1, 2017 balance in the Retained Earnings account is

1-105

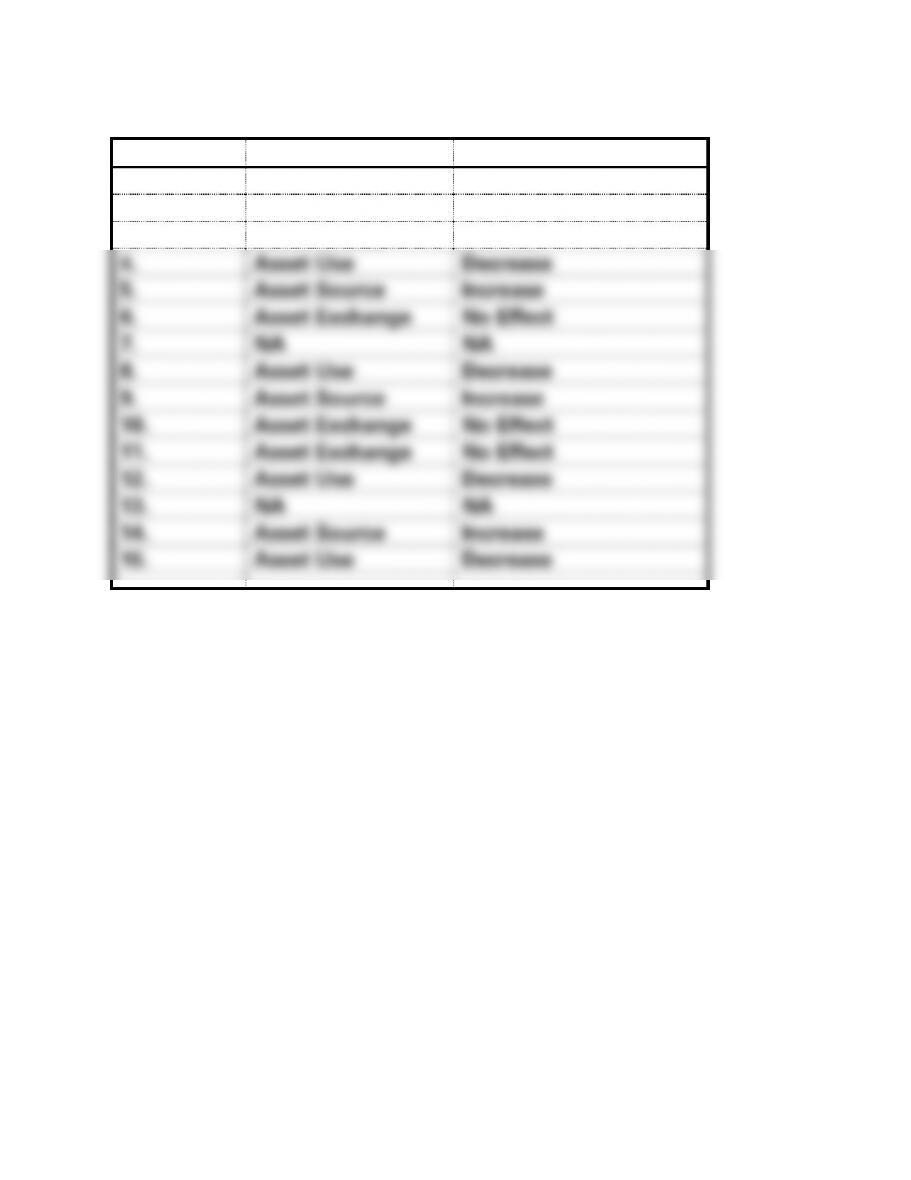

EXERCISE 1-26B

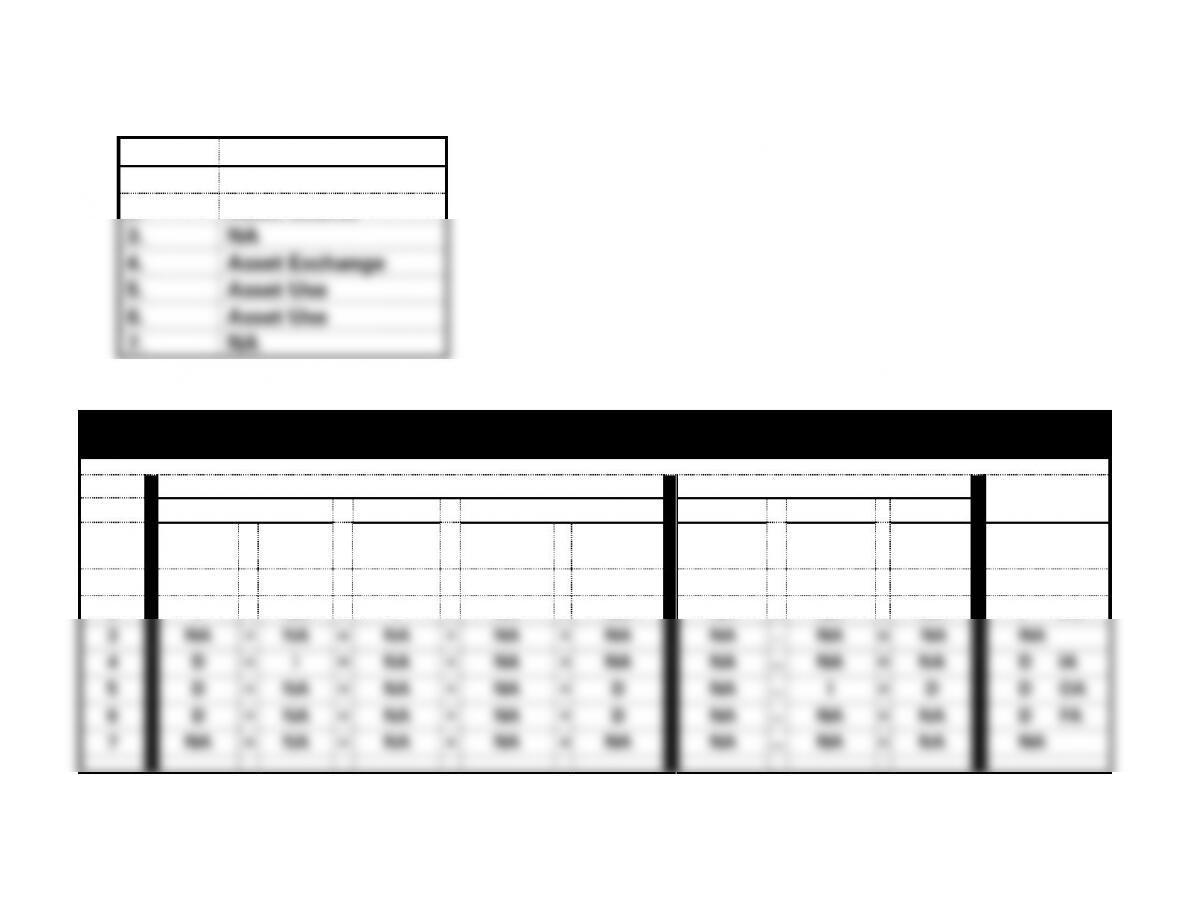

a.

Event

1.

Asset Source

2.

Asset Source

3.

NA

4.

Asset Exchange

5.

Asset Use

6.

Asset Use

7.

NA

b.

Pet Partners

Horizontal Statements Model for 2016

Balance Sheet

Income Statement

Statement of

Assets

=

Liab.

+

Stockholders’ Equity

Revenue

−

Expense

=

Net Inc.

Cash Flows

Event

No.

Cash

+

Land

=

Notes

Payable

+

Common

Stock

+

Retained

Earnings

1

I

+

NA

=

NA

+

I

+

NA

NA

−

NA

=

NA

I FA

2

I

+

NA

=

I

+

NA

+

NA

NA

−

NA

=

NA

I FA

3

NA

+

NA

=

NA

+

NA

+

NA

NA

−

NA

=

NA

NA

4

D

+

I

=

NA

+

NA

+

NA

NA

−

NA

=

NA

D IA

5

D

+

NA

=

NA

+

NA

+

D

NA

−

I

=

D

D OA

6

D

+

NA

=

NA

+

NA

+

D

NA

−

NA

=

NA

D FA

7

NA

+

NA

=

NA

+

NA

+

NA

NA

−

NA

=

NA

NA

1-106

EXERCISE 1-27B

c. The assets would be worth the same, but would be shown at

1-107

SOLUTIONS TO PROBLEMS – SERIES B – CHAPTER 1

PROBLEM 1-28B

a. GAAP Generally Accepted Accounting Principles

b. Revenue may be recognized in either of the years depending on the

entity’s determination of the point in time for revenue recognition.

c. Management accounting reporting is not bound by GAAP. GAAP is

required for external reporting. It helps insure consistent reporting

1-108

PROBLEM 1-29B

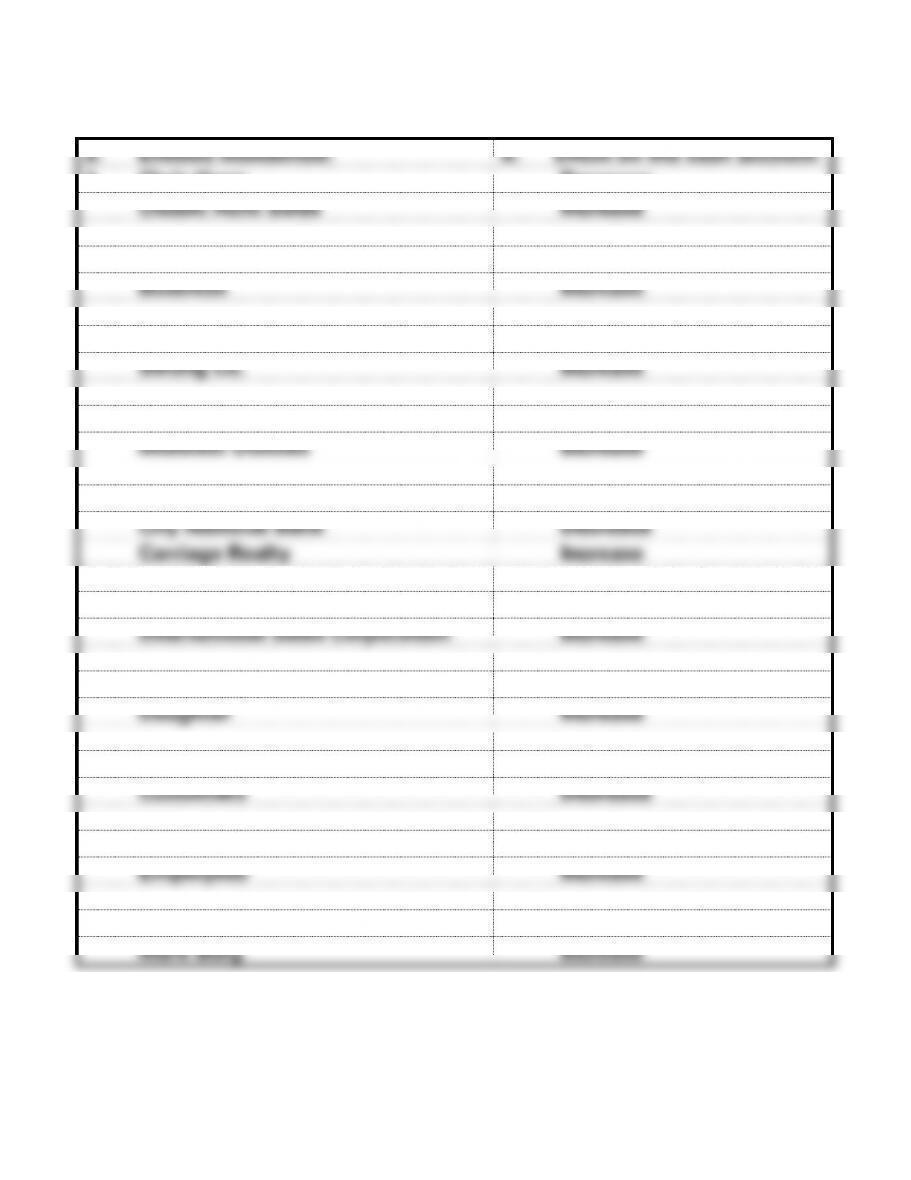

a. Entities mentioned:

b. Effect on the cash account:

1. Chris Hann

Decrease

Classic Auto Sales

Increase

2. Sal Pearl

Decrease

Business

Increase

3. First State Bank

Decrease

Strong Co.

Increase

4. Cindy’s Restaurant

Decrease

Midwest Utilities

Increase

5. Sun Corp.

Increase/Decrease

City National Bank

Decrease

Carriage Realty

Increase

6. Sue Wang

Decrease

International Sales Corporation

Increase

7. Chris Gordon

Decrease

Daughter

Increase

8. Motor Service Co.

Increase

Customers

Decrease

9. Poy Imports

Decrease

Employees

Increase

10. Borg, Inc.

Decrease

Mark Borg

Increase

1-109

PROBLEM 1-30B

Event No.

Type of Event

Effect on Total Assets

1.

Asset Use

Decrease

2.

Asset Use

Decrease

3.

Asset Source

Increase

4.

Asset Use

Decrease

5.

Asset Source

Increase

6.

Asset Exchange

No Effect

7.

NA

NA

8.

Asset Use

Decrease

9.

Asset Source

Increase

10.

Asset Exchange

No Effect

11.

Asset Exchange

No Effect

12.

Asset Use

Decrease

13.

NA

NA

14.

Asset Source

Increase

15.

Asset Use

Decrease

1-110

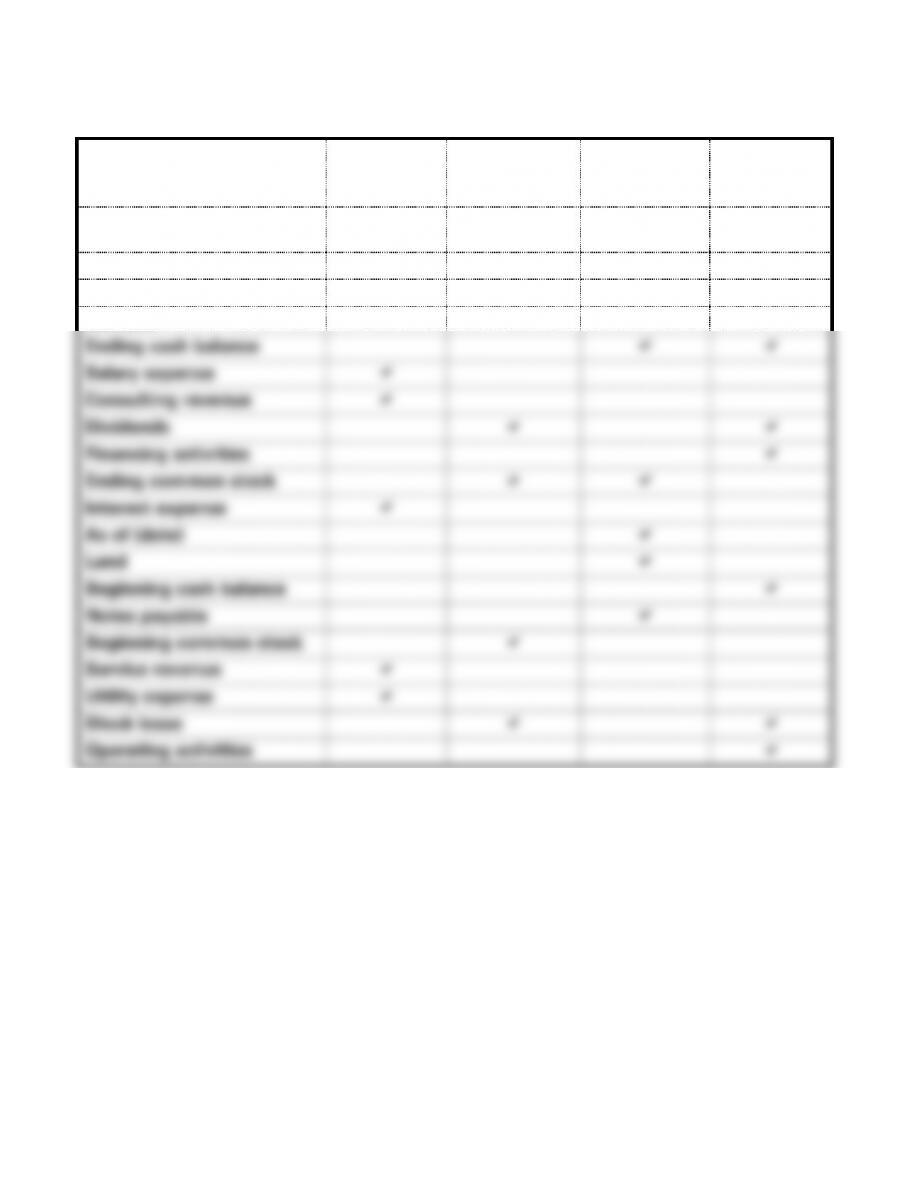

PROBLEM 1-31B

Item

Income

Statement

Statement of

Changes in

Stk. Equity

Balance

Sheet

Statement

of Cash

Flows

For the Period Ended

(Date)

Net income

Investing activities

Net loss

Ending cash balance

Salary expense

Consulting revenue

Dividends

Financing activities

Ending common stock

Interest expense

As of (date)

Land

Beginning cash balance

Notes payable

Beginning common stock

Service revenue

Utility expense

Stock issue

Operating activities

1-111

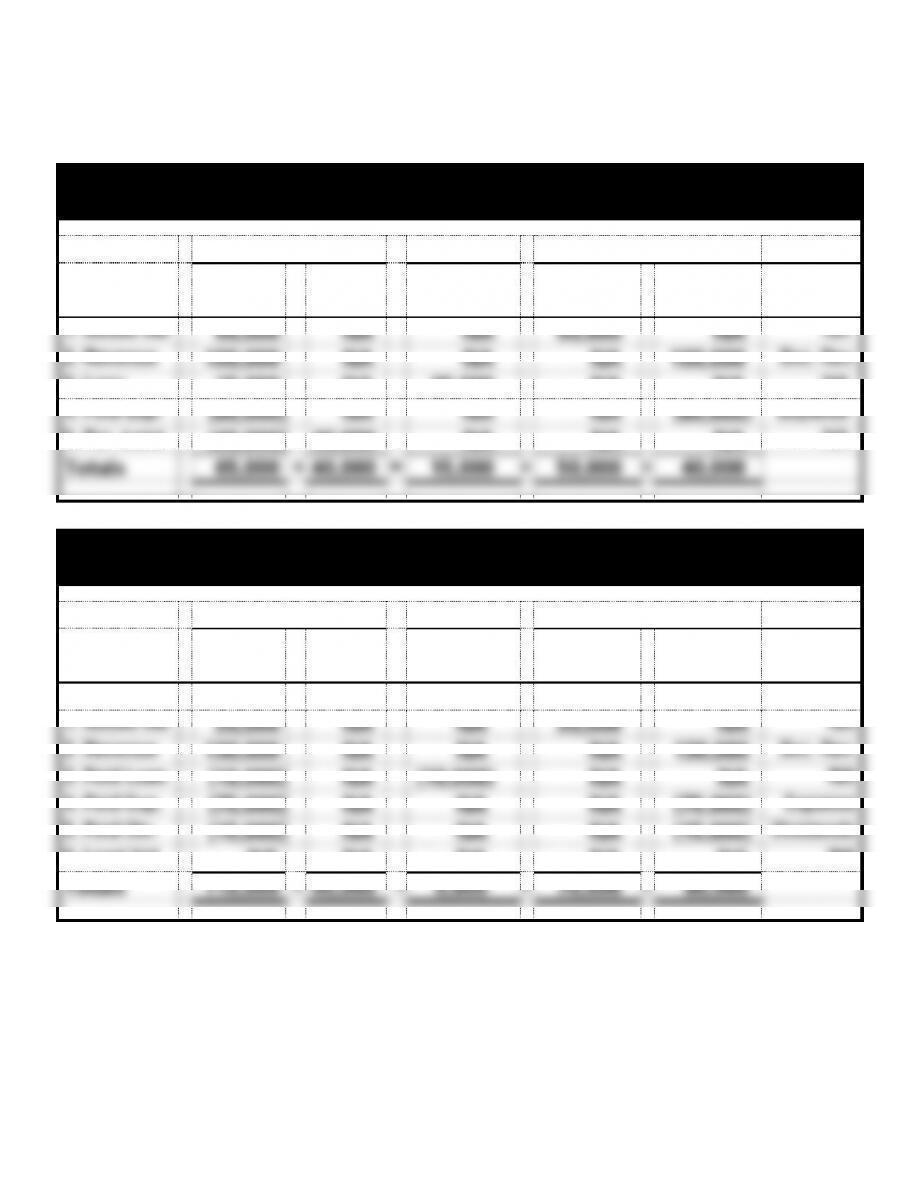

PROBLEM 1-32B

a.

Marco’s Consulting

Accounting Equation for 2016

Assets

=

Liabilities

+

Stockholders’ Equity

Event

Cash

+

Land

=

Notes

Payable

+

Common

Stock

+

Retained

Earnings

Acct.

Title/RE

1. Issued stk

50,000

NA

NA

50,000

NA

NA

2. Revenue

100,000

NA

NA

NA

100,000

Svc. Rev.

3. Loan

15,000

NA

15,000

NA

NA

NA

4. Paid Exp.

(60,000)

NA

NA

NA

(60,000)

Expense

5. Pur. Land

(40,000)

40,000

NA

NA

NA

NA

Totals

65,000

+

40,000

=

15,000

+

50,000

+

40,000

Marco’s Consulting

Accounting Equation for 2017

Assets

=

Liabilities

+

Stockholders’ Equity

Event

Cash

+

Land

=

Notes

Payable

+

Common

Stock

+

Retained

Earnings

Acct.

Title/RE

Beg. Bal.

65,000

40,000

15,000

50,000

40,000

1. Issued stk

20,000

NA

NA

20,000

NA

NA

2. Revenue

130,000

NA

NA

NA

130,000

Svc. Rev.

3. Paid Loan

(10,000)

NA

(10,000)

NA

NA

NA

4. Paid Exp.

(75,000)

NA

NA

NA

(75,000)

Expense

5. Paid Div.

(15,000)

NA

NA

NA

(15,000)

Dividends

6. Land Val.

NA

NA

NA

NA

NA

NA

Totals

115,000

+

40,000

=

5,000

+

70,000

+

80,000

1-112

PROBLEM 1-32B (cont.)

b.

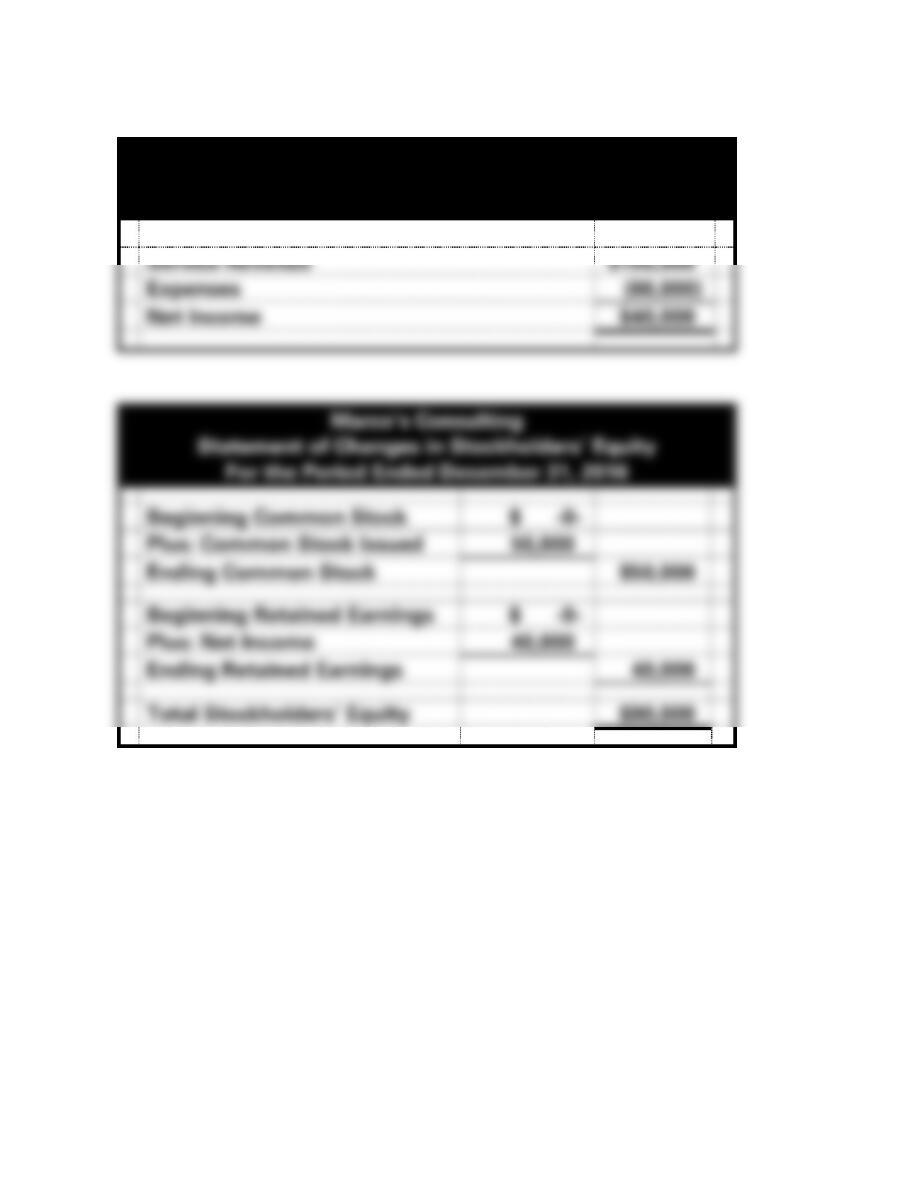

Marco’s Consulting

Income Statement

For the Period Ended December 31, 2016

Service Revenue

$100,000

Expenses

(60,000)

Net Income

$40,000

Marco’s Consulting

Statement of Changes in Stockholders’ Equity

For the Period Ended December 31, 2016

Beginning Common Stock

$ -0-

Plus: Common Stock Issued

50,000

Ending Common Stock

$50,000

Beginning Retained Earnings

$ -0-

Plus: Net Income

40,000

Ending Retained Earnings

40,000

Total Stockholders’ Equity

$90,000

1-113

PROBLEM 1-32B b. (cont.)

Marco’s Consulting

Balance Sheet

As of December 31, 2016

Assets

Cash

$65,000

Land

40,000

Total Assets

$105,000

Liabilities

Notes Payable

$ 15,000

Stockholders’ Equity

Common Stock

$50,000

Retained Earnings

40,000

Total Stockholders’ Equity

90,000

Total Liabilities and Stockholders’ Equity

$105,000

1-114

PROBLEM 1-32B b. (cont.)

Marco’s Consulting

Statement of Cash Flows

For the Year Ended December 31, 2016

Cash Flows From Operating Activities:

Cash Receipts from Customers

$100,000

Cash Payments for Expenses

(60,000)

Net Cash Flow from Operating Activities

$40,000

Cash Flows From Investing Activities:

Cash Payment for Land

$(40,000)

Net Cash Flow from Investing Activities

(40,000)

Cash Flows From Financing Activities:

Cash Receipts from Borrowing

$15,000

Cash Receipts from Stock Issue

50,000

Net Cash Flow from Financing Activities

65,000

Net Increase in Cash

65,000

Plus: Beginning Cash Balance

-0-

Ending Cash Balance

$65,000