Chapter 12 Statement of Cash Flows

12-1

1. The statement of cash flows explains how a company obtained

future.

2. The three categories of cash inflows and outflows are

operating activities, investing activities, and financing

activities.

Operating activities include cash inflows and outflows that are

3. Noncash investing and financing activities are transactions

that do not require the receipt or payment of cash. For

example, a company may purchase an operating asset with a

Chapter 12 Statement of Cash Flows

12-2

4. Since the ending balance of accounts receivable exceeded the

beginning balance by $2,000, less cash was provided by

5. Since the ending balance of utilities payable exceeded the

beginning balance by $1,900, more utility cost was used than

6. Since the ending balance of unearned revenue was less than

the beginning balance by $1,100, less cash was received in

7. a. Payment of accounts payable – operating activity.

b. Payment of interest on bonds payable – operating activity.

8. Depreciation expense is an allocation of the cost of an asset

12-3

9. Cost of land $4,200

10. Cost of office equipment $7,500

Accumulated depreciation (7,200)

11. a. operating activities

b. investing activities, or operating activities if trading securities

c. investing activities

12. The difference in the cash flow statement when using the

direct or the indirect method is the presentation of the

operating activities section of the statement.

Chapter 12 Statement of Cash Flows

12-4

13. The direct method is more logical because the presentation

shows where cash came from and where it went, i.e., the

14. The primary advantage of using the indirect method is the fact

15. The primary advantage of using the direct method is that it is

more logical and presents the actual amount of cash inflows

16. a. Cash outflow of $46,000 as an investing activity.

b. Cash inflow of $8,700 as an investing activity. The gain on

17. Yes, it is possible for a company to have negative net cash

flow and net income in the same period. A company may use

12-5

EXERCISE 12-1A

1.

Not affected (Financing)

2.

Subtracted

3.

Subtracted

4.

Not affected (Investing)

5.

Added

6.

Not affected (Financing)

7.

Subtracted

8.

Added

9.

Added

10.

Not affected (Financing)

11.

Added

Chapter 12 Statement of Cash Flows

12-6

EXERCISE 12-2A

a.

Cash Flows From Operating Activities

Net Income

$31,600

Add: Decrease in accounts receivable (1)

1,600

Deduct: Decrease in accounts payable (2)

(1,500)

Net cash inflow from operating activities

$31,700

(1 ) Add decreases and subtract increases in current asset account balances, other than cash, to net

income.

(2) Add increases and subtract decreases in current liability account balances to net income.

b. The decrease in the balance in the Accounts Receivable account

suggests that the amount of cash collected from accounts

receivable was more than the amount of revenue recognized

12-7

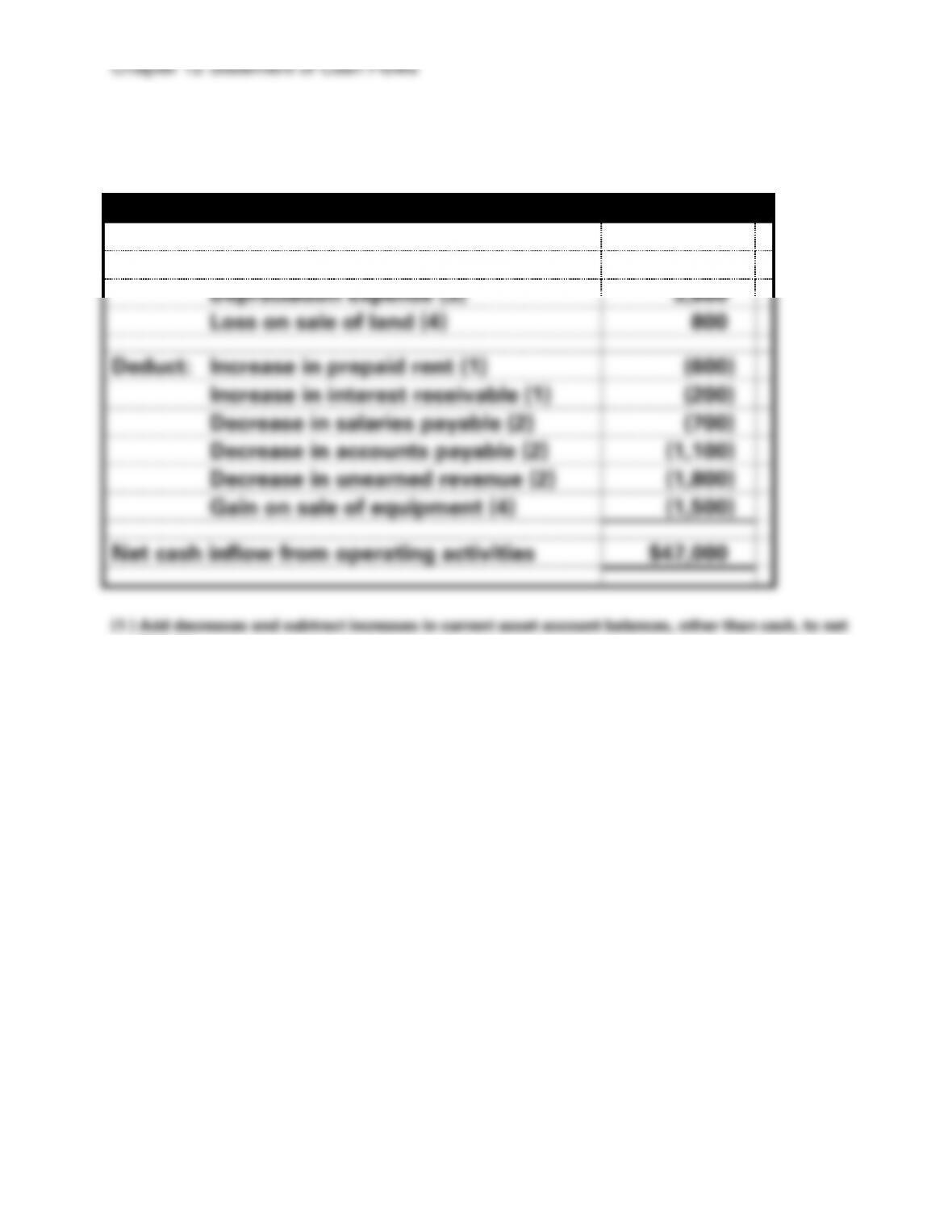

EXERCISE 12-3A

Cash Flows From Operating Activities

Net Income

$47,300

Add: Decrease in accounts receivable (1)

1,200

Depreciation expense (3)

3,600

Loss on sale of land (4)

800

Deduct: Increase in prepaid rent (1)

(600)

Increase in interest receivable (1)

(200)

Decrease in salaries payable (2)

(700)

Decrease in accounts payable (2)

(1,100)

Decrease in unearned revenue (2)

(1,800)

Gain on sale of equipment (4)

(1,500)

Net cash inflow from operating activities

$47,000

(1 ) Add decreases and subtract increases in current asset account balances, other than cash, to net

income.

(2) Add increases and subtract decreases in current liability account balances to net income.

(3) Add noncash expenses (e.g., depreciation) to net income.

(4) Add losses and subtract gains from the sale of noncurrent assets to net income.

Chapter 12 Statement of Cash Flows

12-8

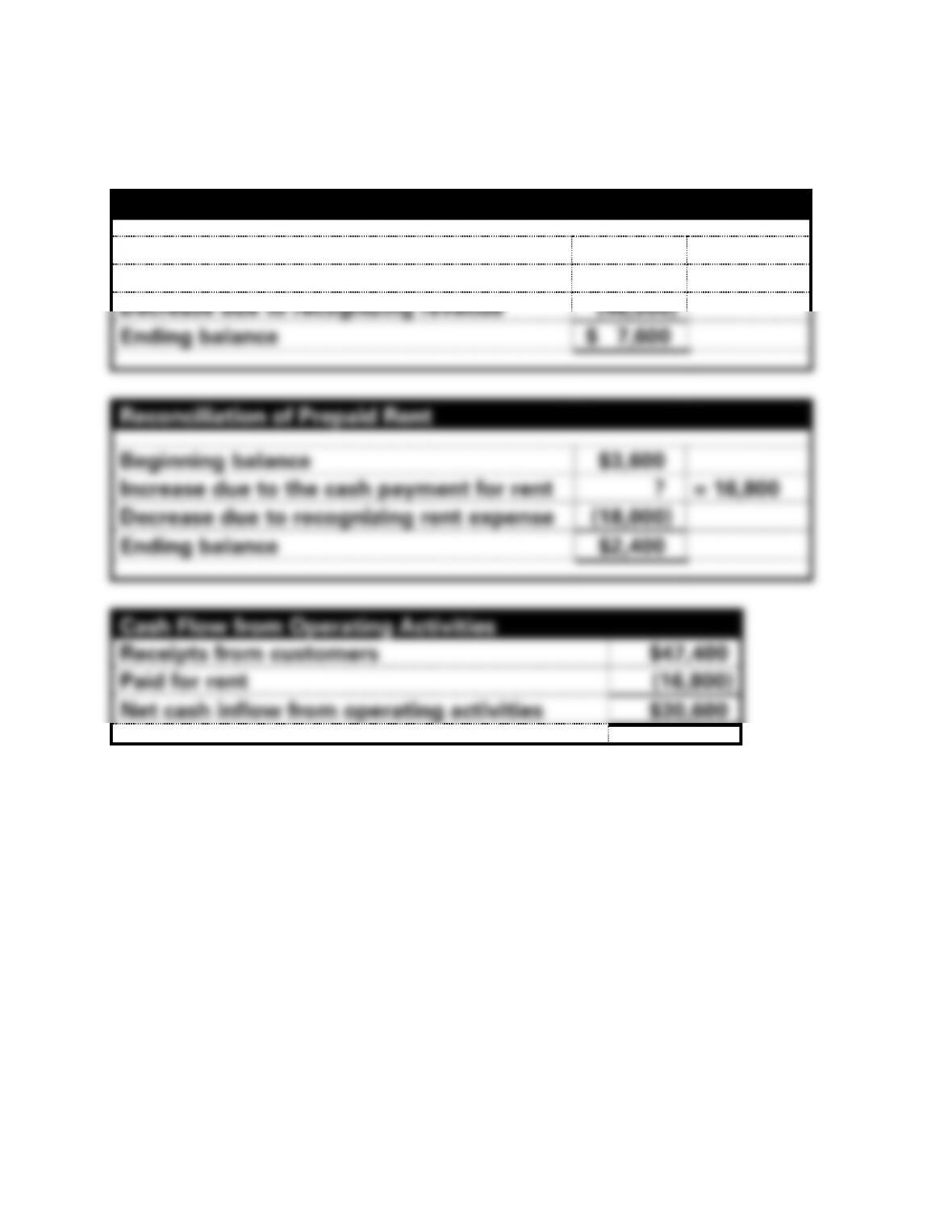

EXERCISE 12-4A

Reconciliation of Unearned Revenue

Beginning balance

$ 6,200

Increase due to collecting cash in advance

?

= 47,400

Decrease due to recognizing revenue

(46,000)

Ending balance

$ 7,600

Reconciliation of Prepaid Rent

Beginning balance

$3,600

Increase due to the cash payment for rent

?

= 16,800

Decrease due to recognizing rent expense

(18,000)

Ending balance

$2,400

Cash Flow from Operating Activities

Receipts from customers

$47,400

Paid for rent

(16,800)

Net cash inflow from operating activities

$30,600

12-9

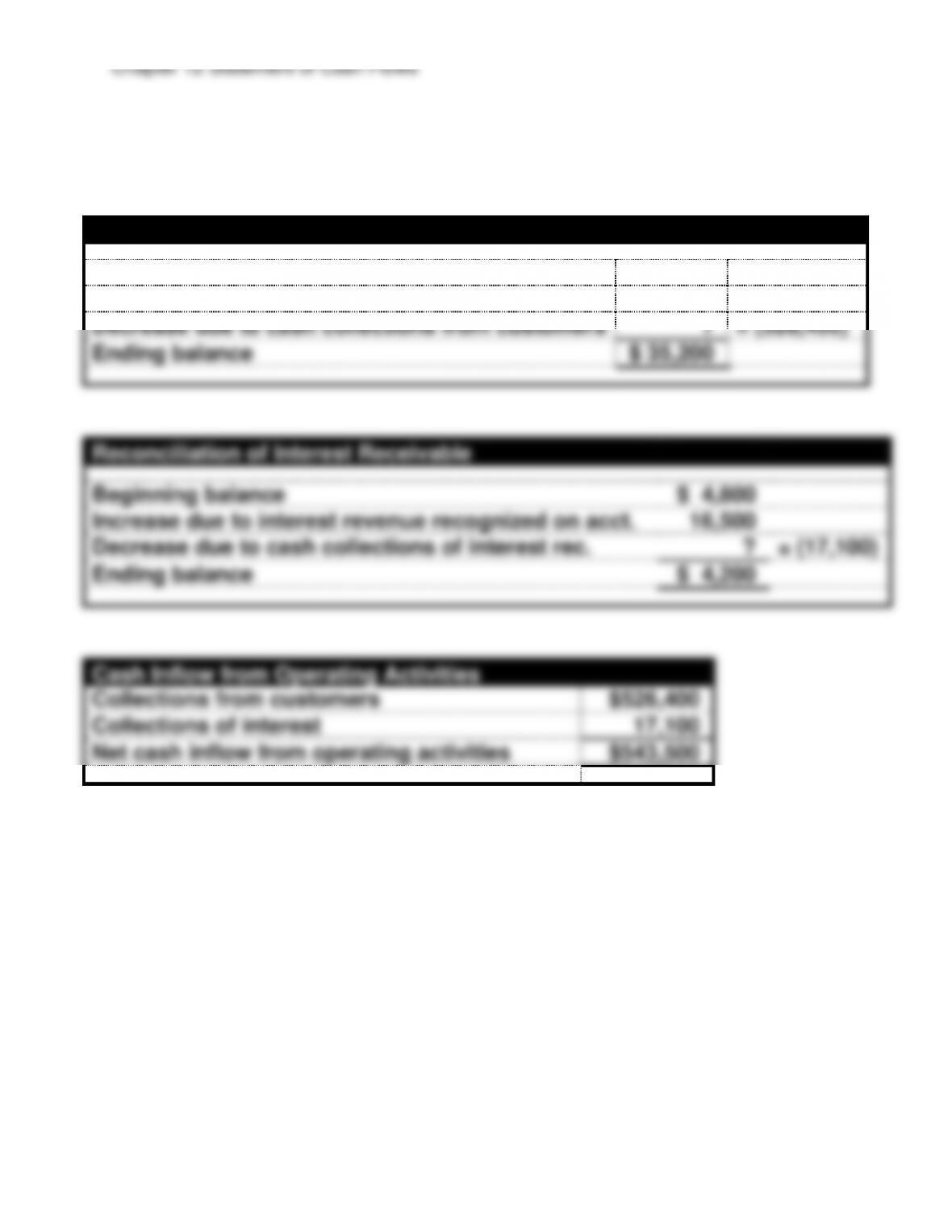

EXERCISE 12-5A

a.

Reconciliation of Accounts Receivable

Beginning balance

$ 31,600

Increase due to revenue recognized on account

530,000

Decrease due to cash collections from customers

?

= (526,400)

Ending balance

$ 35,200

Reconciliation of Interest Receivable

Beginning balance

$ 4,800

Increase due to interest revenue recognized on acct.

16,500

Decrease due to cash collections of interest rec.

?

= (17,100)

Ending balance

$ 4,200

Cash Inflow from Operating Activities

Collections from customers

$526,400

Collections of interest

17,100

Net cash inflow from operating activities

$543,500

Chapter 12 Statement of Cash Flows

EXERCISE 12-5A (cont.)

b.

Reconciliation of Other Operating Expenses Payable

Beginning balance

$ 18,500

Increase due to expenses recognized on account

175,000

Decrease due to payment to vendors

?

= (172,500)

Ending balance

$ 21,000

Reconciliation of Salaries Payable

Beginning balance

$ 7,200

Increase due to salaries expense recognized

214,000

Decrease due to cash paid for salaries

?

= (214,700)

Ending balance

$ 6,500

Cash paid for other operating expenses

Cash paid for salaries

Net cash outflow from operating activities

12–11

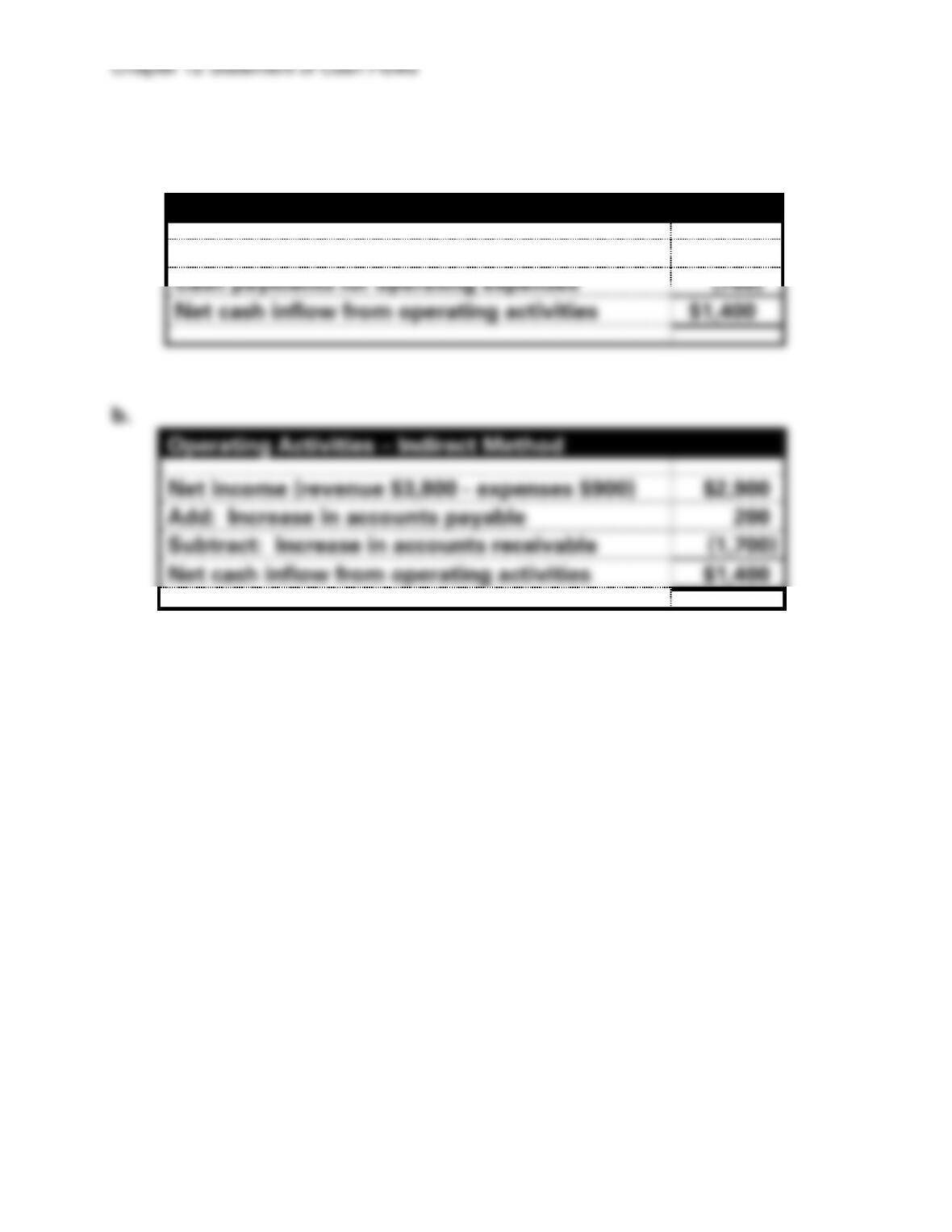

EXERCISE 12-6A

a.

Operating Activities – Direct Method

Cash receipts from customers

$2,100

Cash payments for operating expenses

(700)

Net cash inflow from operating activities

$1,400

Operating Activities – Indirect Method

Net income (revenue $3,800 – expenses $900)

$2,900

Add: Increase in accounts payable

200

Subtract: Increase in accounts receivable

(1,700)

Net cash inflow from operating activities

$1,400

Chapter 12 Statement of Cash Flows

12–12

EXERCISE 12-7A

a. Direct Method

Reconciliation of Accounts Receivable

Beginning balance

$ 62,000

Increase due to revenue recognized on account

268,000

Decrease due to cash collections from

customers

?

= (273,000)

Ending balance

$ 57,000

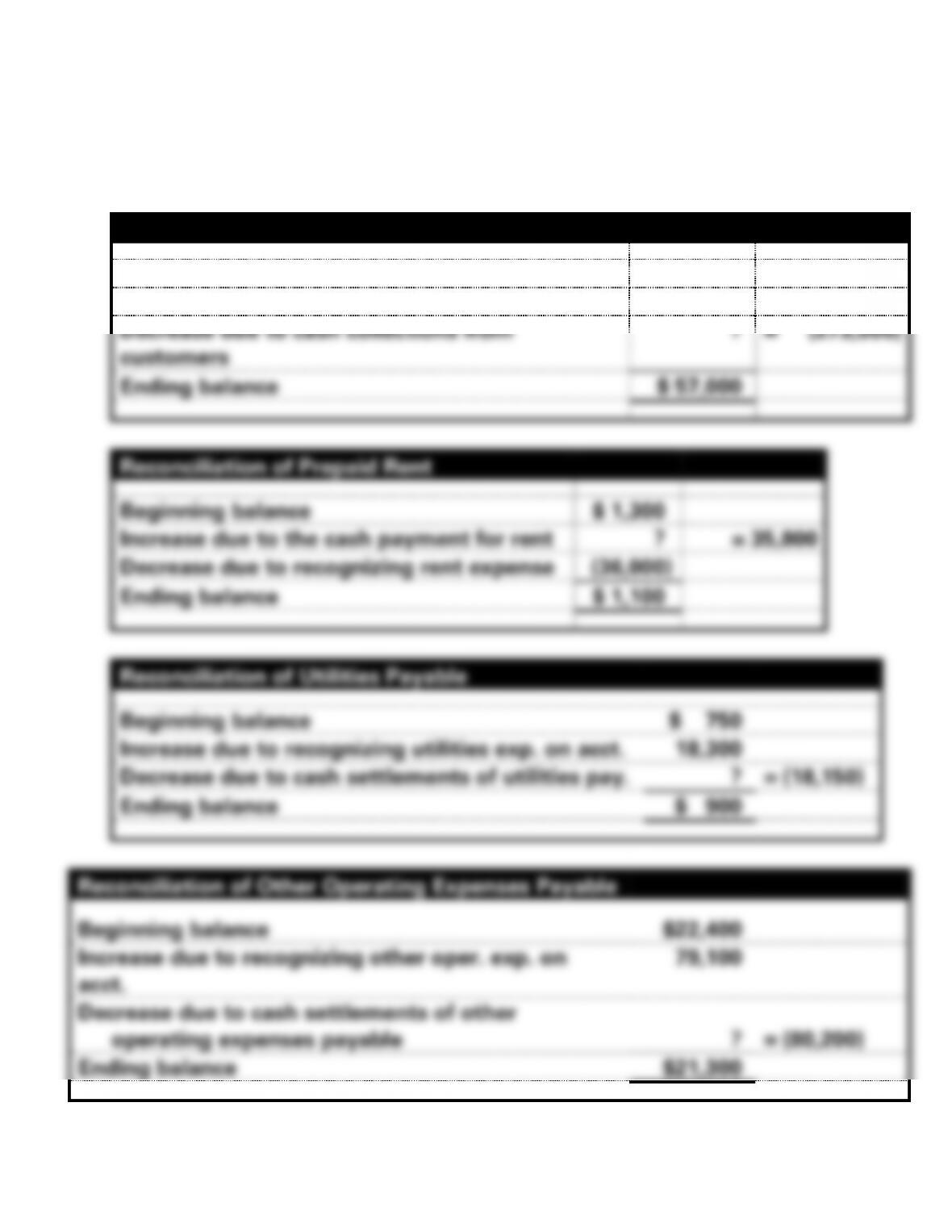

Reconciliation of Prepaid Rent

Beginning balance

$ 1,300

Increase due to the cash payment for rent

?

= 35,800

Decrease due to recognizing rent expense

(36,000)

Ending balance

$ 1,100

Reconciliation of Utilities Payable

Beginning balance

$ 750

Increase due to recognizing utilities exp. on acct.

18,300

Decrease due to cash settlements of utilities pay.

?

= (18,150)

Ending balance

$ 900

Reconciliation of Other Operating Expenses Payable

Beginning balance

$22,400

Increase due to recognizing other oper. exp. on

acct.

79,100

Decrease due to cash settlements of other

operating expenses payable

?

= (80,200)

Ending balance

$21,300

12–13

EXERCISE 12-7A a. (cont.)

Cash Flow From Operating Activities

Receipts from customers

$273,000

Paid for rent

(35,800)

Paid for utilities

(18,150)

Paid for other operating expenses

(80,200)

Net cash inflow from operating activities

$138,850

b. Indirect Method:

Begin by determining the amount of change in the balances in the

current accounts other than cash and current liability accounts.

2017

2016

Change

Accounts receivable

$57,000

$62,000

$(5,000)

Prepaid rent

1,100

1,300

(200)

Utilities payable

900

750

150

Other operating expenses payable

21,300

22,400

(1,100)

Cash Flow From Operating Activities

Net income:

$134,600

Add: Decrease in prepaid rent (1)

200

Decrease in accounts receivable (1)

5,000

Increase in utilities payable (2)

150

Deduct: Decrease in other oper. expense payable

(2)

1,100

Net cash inflow from operating activities

$138,850

income.

(2) Add increases and subtract decreases in current liability account balances to net income.

Chapter 12 Statement of Cash Flows

12–14

Proceeds from sale of land

Paid for purchase of land

Net cash inflow from investing activities

EXERCISE 12-8A

a.

Reconciliation of Land Account

Beginning balance

$325,000

Increase due to purchasing land

?

= 66,500

Decrease due to selling land

(106,500)

Ending balance

$285,000

Chapter 12 Statement of Cash Flows

12–16

EXERCISE 12-9A

a.

Reconciliation of Delivery Equipment Account

Beginning balance

$72,350

Increase due to purchasing delivery equip.

22,100

Decrease due to selling delivery equip.

?

= (25,050)

Ending balance

$69,400

In order to balance the account, delivery equipment with an original

cost of $25,050 must have been sold.

b.

Since a gain was recognized, the equipment must have been sold for

an amount of cash that was more than the book value of the

equipment. Specifically, the cash collected from the sale of the

equipment was $8,050 [($25,050 original cost – $22,000 accumulated

depreciation) = $3,050 book value; $3,050 + $5,000 gain on sale =

$8,050].

12–17

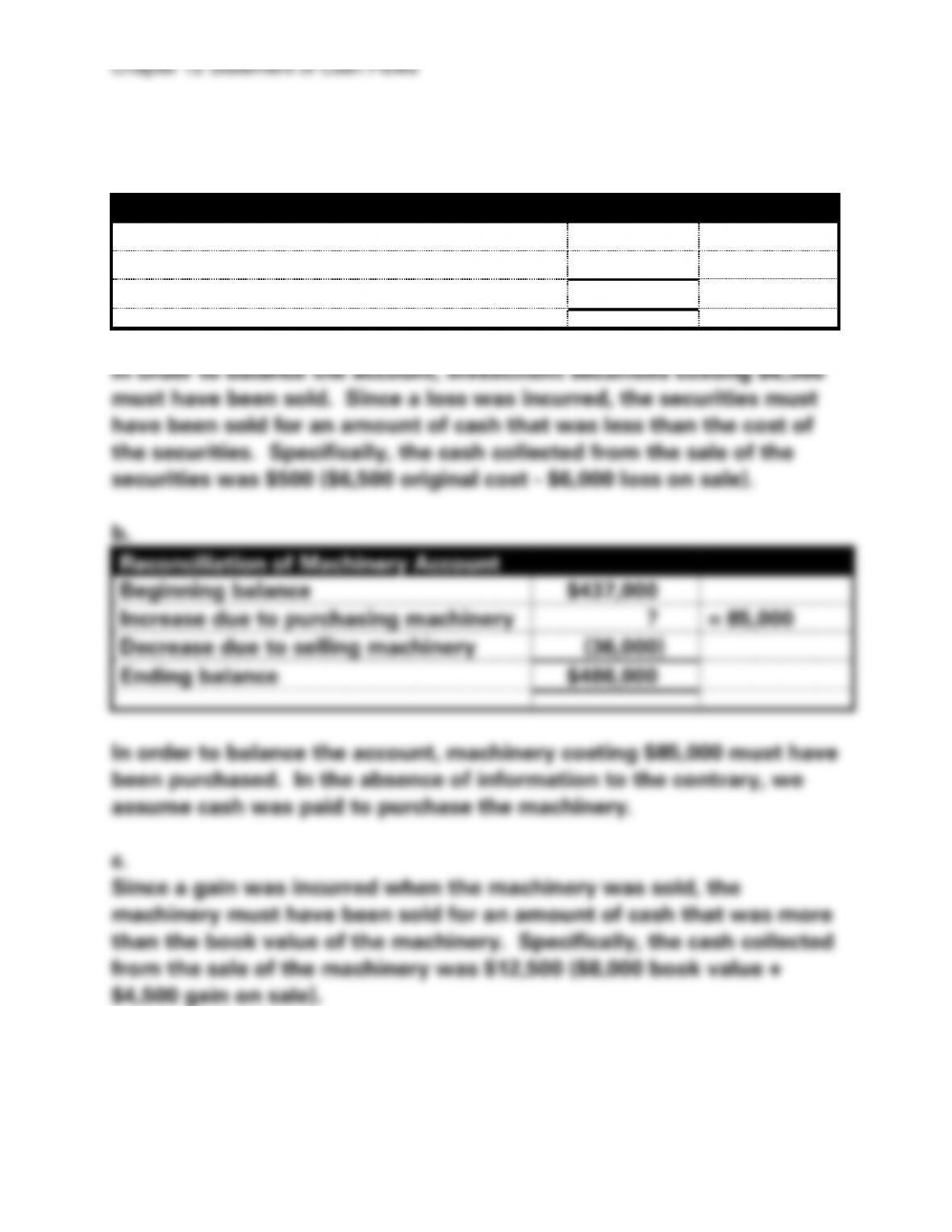

EXERCISE 12–10A

a.

Reconciliation of Investment securities Account

Beginning balance

$116,500

Decrease due to selling investment sec.

?

= (6,500)

Ending balance

$110,000

Reconciliation of Machinery Account

Beginning balance

$437,000

Increase due to purchasing machinery

?

= 85,000

Decrease due to selling machinery

(36,000)

Ending balance

$486,000

Chapter 12 Statement of Cash Flows

12–18

12–19

EXERCISE 12–10A (cont.)

d.

Reconciliation of Land Account

Beginning balance

$100,000

Increase due to purchasing land

?

= 60,000

Ending balance

$160,000

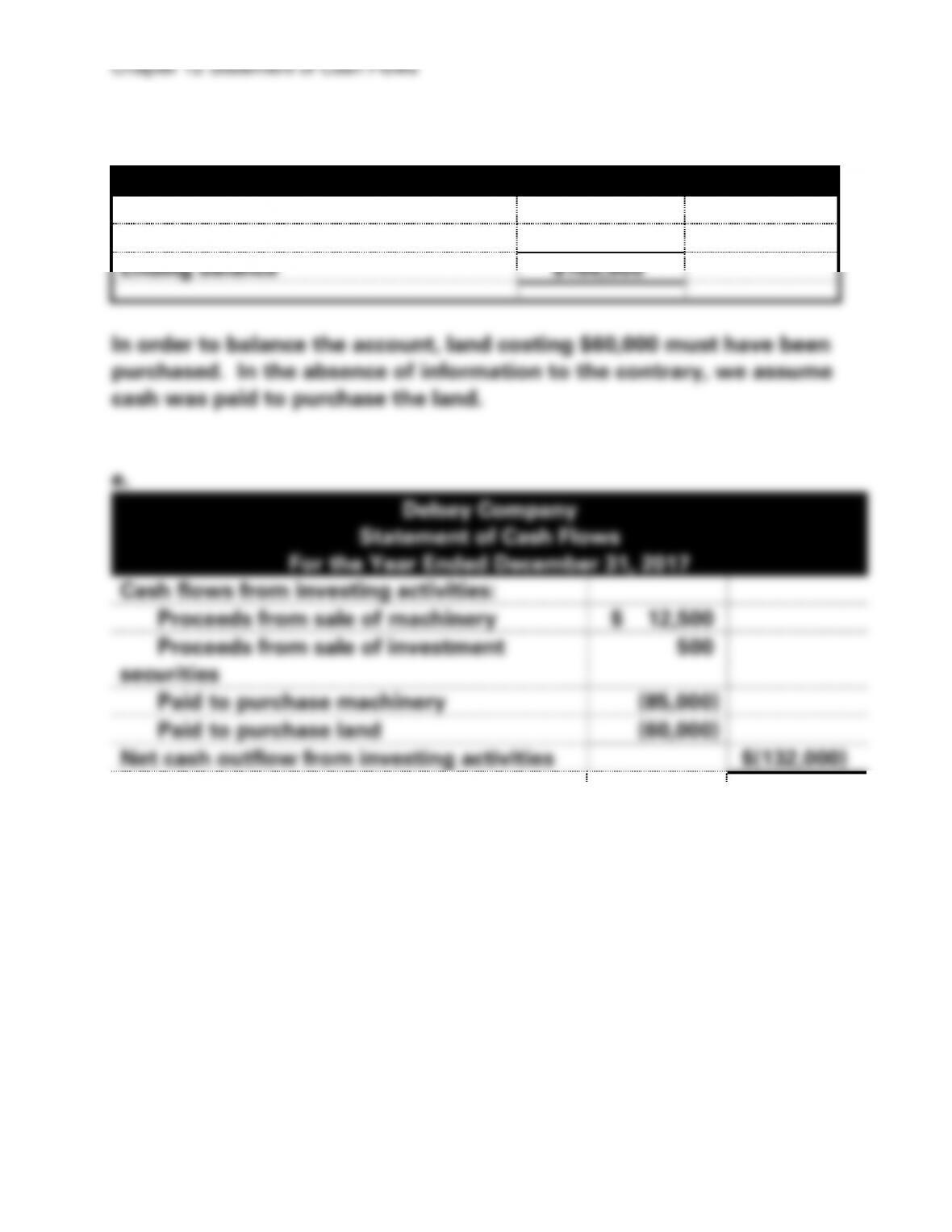

In order to balance the account, land costing $60,000 must have been

purchased. In the absence of information to the contrary, we assume

cash was paid to purchase the land.

e.

Delsey Company

Statement of Cash Flows

For the Year Ended December 31, 2017

Cash flows from investing activities:

Proceeds from sale of machinery

$ 12,500

Proceeds from sale of investment

securities

500

Paid to purchase machinery

(85,000)

Paid to purchase land

(60,000)

Net cash outflow from investing activities

$(132,000)

Chapter 12 Statement of Cash Flows

12–20

EXERCISE 12–11A

a.

Reconciliation of Bonds Payable Account

Beginning balance

$450,000

Increase due to issuing bonds payable

200,000

Decrease due to repayment of bonds

payable

?

= (250,000)

Ending balance

$400,000

Cash Flows from Financing Activities

Proceeds from issue of bonds payable

$200,000

Repayment of bonds payable

(250,000)

Net cash outflow from financing activities

$( 50,000)