8-121

ATC 8-1

All dollar amounts are in millions.

a. Straight-line. See Note 12 of the annual report.

b. Note 14 of the annual report refers to “goodwill and intangible

assets.” Other than mentioning “goodwill” and “leasehold

8-122

ATC 8-2

Computation of depreciation expense:

Straight-line:

(Cost − Salvage Value) Useful life = Depreciation per year

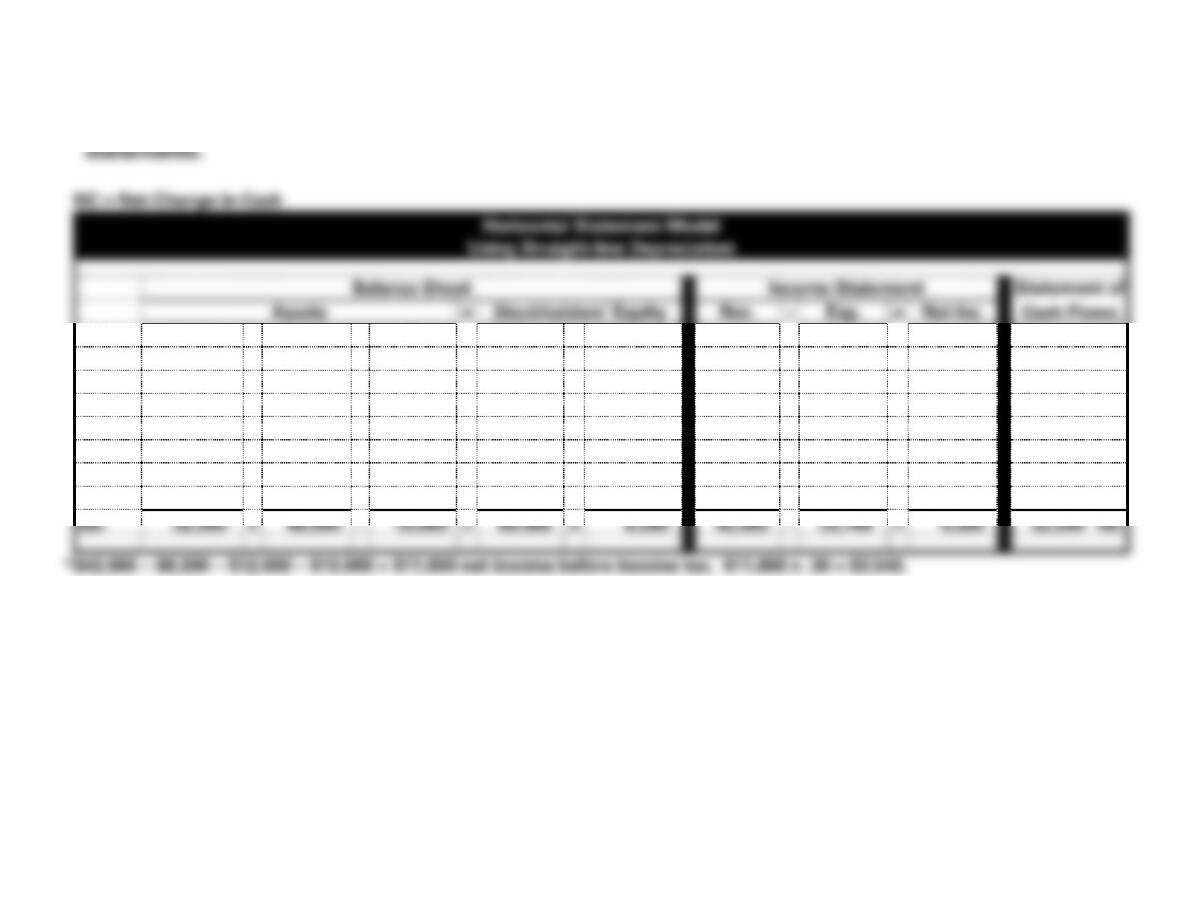

ATC 8-2 (cont.)

Note: It is useful to prepare a horizontal statements model before preparing the financial

8-124

ATC 8-2 (cont.)

NC = Net Change in Cash

Horizontal Statement Model

Using Double-Declining Balance Depreciation

Balance Sheet

Income Statement

Statement of

Assets

=

Stockholders’ Equity

Rev.

−

Exp.

=

Net Inc.

Cash Flows

Event

Cash

+

Equip.

−

A. Dep.

=

C. Stock

+

Ret. Ear.

−

=

1.

60,000

+

NA

−

NA

=

60,000

+

NA

NA

−

NA

=

NA

60,000 FA

2.

(46,000)

+

46,000

−

NA

=

NA

+

NA

NA

−

NA

=

NA

(46,000) IA

3.

42,000

+

NA

−

NA

=

NA

+

42,000

42,000

−

NA

=

42,000

42,000 OA

4.

(8,200)

+

NA

−

NA

=

NA

+

(8,200)

NA

−

8,200

=

(8,200)

(8,200) OA

5.

(12,000)

+

NA

−

NA

=

NA

+

(12,000)

NA

−

12,000

=

(12,000)

(12,000) OA

6.

NA

+

NA

−

23,000

=

NA

+

(23,000)

NA

−

23,000

=

(23,000)

NA

7.*

NA

+

NA

−

NA

=

NA

+

NA

NA

−

NA

=

NA

NA

Bal.

35,800

+

46,000

−

23,000

=

60,000

+

(1,200)

42,000

−

43,200

=

(1,200)

35,800 NC

8-125

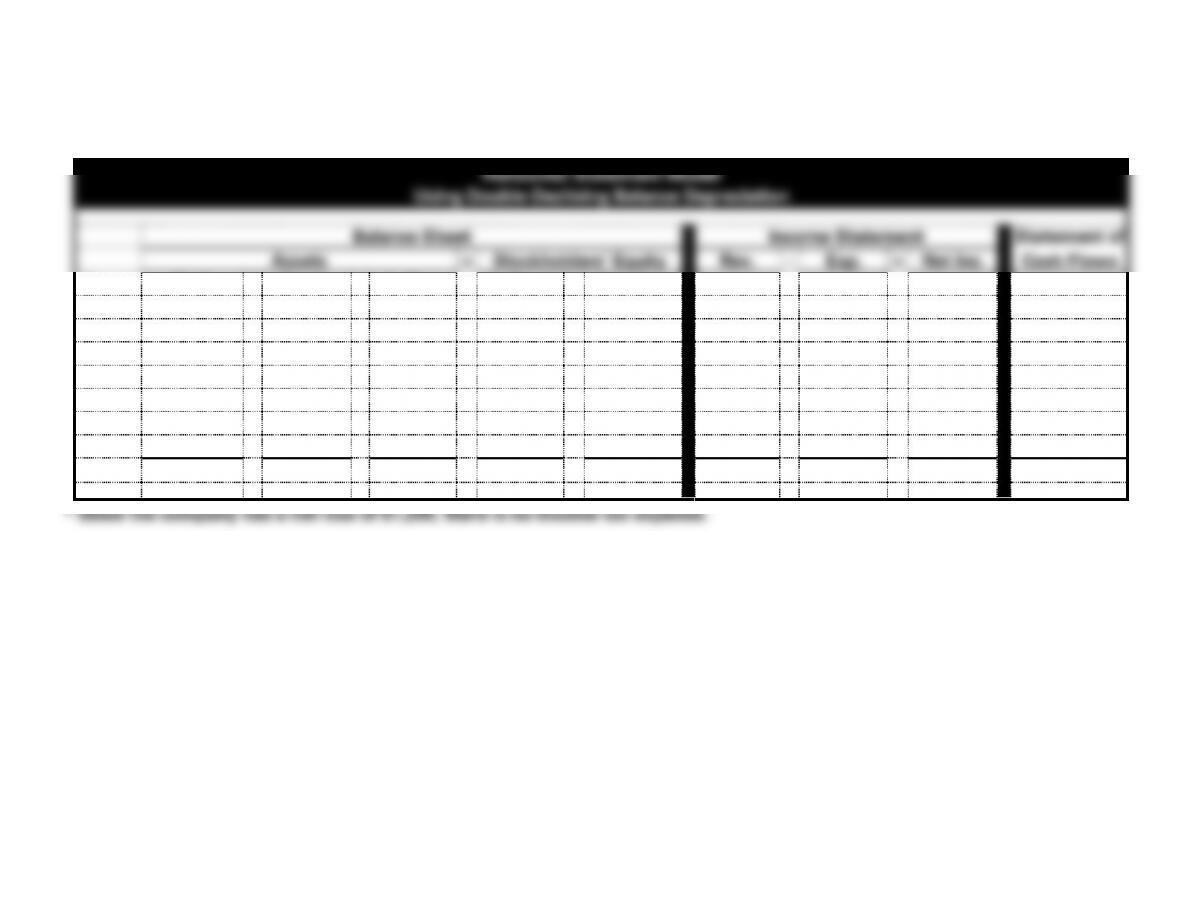

ATC 8-2 (cont.)

NC = Net Change in Cash

Horizontal Statement Model

Using MACRS Depreciation

Balance Sheet

Income Statement

Statement of

Assets

=

Stockholders’ Equity

Rev.

−

Exp.

=

Net Inc.

Cash Flows

Event

Cash

+

Equip.

−

A. Dep.

=

C. Stock

+

Ret. Ear.

−

=

1.

60,000

+

NA

−

NA

=

60,000

+

NA

NA

−

NA

=

NA

60,000 FA

2.

(46,000)

+

46,000

−

NA

=

NA

+

NA

NA

−

NA

=

NA

(46,000) IA

3.

42,000

+

NA

−

NA

=

NA

+

42,000

42,000

−

NA

=

42,000

42,000 OA

4.

(8,200)

+

NA

−

NA

=

NA

+

(8,200)

NA

−

8,200

=

(8,200)

(8,200) OA

5.

(12,000)

+

NA

−

NA

=

NA

+

(12,000)

NA

−

12,000

=

(12,000)

(12,000) OA

6.

NA

+

NA

−

9,200

=

NA

+

(9,200)

NA

−

9,200

=

(9,200)

NA

7.*

(3,780)

+

NA

−

NA

=

NA

+

(3,780)

NA

−

3,780

=

(3,780)

(3,780) OA

Bal.

32,020

+

46,000

−

9,200

=

60,000

+

8,820

42,000

−

33,180

=

8,820

32,020 NC

*$42,000 − $8,200 − $12,000 −$9,200 = $12,600 net income before tax. $12,600 x .30 = $3,780

8-64

ATC 8-2 (cont.)

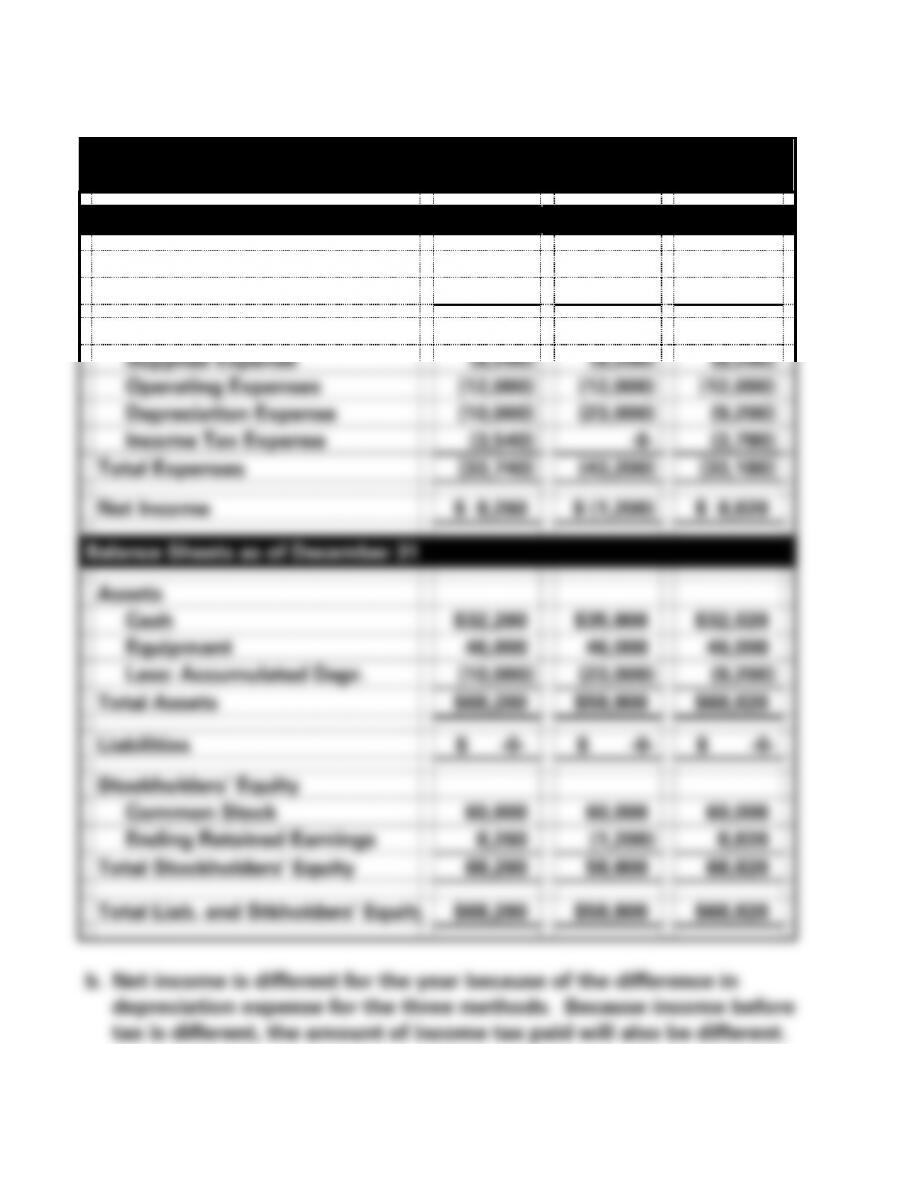

a.

Sweet’s Bakery

Financial Statement

Income Statements for the Year Ended December 31

SL

DDB

MACRS

Sales Revenue

$42,000

$42,000

$42,000

Expenses

Supplies Expense

(8,200)

(8,200)

(8,200)

Operating Expenses

(12,000)

(12,000)

(12,000)

Depreciation Expense

(10,000)

(23,000)

(9,200)

Income Tax Expense

(3,540)

-0-

(3,780)

Total Expenses

(33,740)

(43,200)

(33,180)

Net Income

$ 8,260

$ (1,200)

$ 8,820

Balance Sheets as of December 31

Assets

Cash

$32,260

$35,800

$32,020

Equipment

46,000

46,000

46,000

Less: Accumulated Depr.

(10,000)

(23,000)

(9,200)

Total Assets

$68,260

$58,800

$68,820

Liabilities

$ –0–

$ -0-

$ -0-

Stockholders’ Equity

Common Stock

60,000

60,000

60,000

Ending Retained Earnings

8,260

(1,200)

8,820

Total Stockholders’ Equity

68,260

58,800

68,820

Total Liab. and Stkholders’ Equity

$68,260

$58,800

$68,820

8-65

However over the life of the asset, the total amount of depreciation

8-66

ATC 8-3

The companies and the set of ratios to which each relates are as follows:

Molson Coors Brewing (MC) Company 2

Darden Restaurants Company 1

Deere & Company Company 4

Weight Watchers International (W-W) Company 3

Having identified Companies 1 and 3, this means that Molson must

be either Company 2 or 4. There are several significant differences

between the data for Companies 2 and 4, most notable are:

Current assets ÷ total assets

Average days to sell inventory

8-67

ATC 8-4

a. Depreciation expense as a percentage of sales:

Company 1: $44,326 ÷ $ 1,868,739 = 2.4%

Company 2: $ 1,104 ÷ $ 12,026 = 9.2%

b. Property, plant and equipment as a percentage of total assets:

8-68

ATC 8-5

a. Depreciation expense as a percentage of sales:

Chesapeake Energy: $2,903 ÷ $17,506 = 16.6%

Anadarko Petroleum: $3,927 ÷ $14,581 = 26.9%

b. Buildings, machinery, and equipment (depreciable assets) as a

percentage of total assets:

same.

8-69

ATC 8-6

This problem is used to test thinking and writing skills. Students should

realize that the equipment of the two companies had originally cost

methods.

8-70

ATC 8-7

a. As stated in the problem, operating expenses reduce the amount of

net income the company presents on the balance sheet. Mr.

Blowhard’s scheme takes the line costs, which should be operating

expenses, and classifies them as capital assets. This significantly

increases the amount of net income that the company will show.

8-71

ATC 8-8

The data for Microsoft is from its June 30, 2013 Form 10-K and the

data for Intel are from its December 25, 2013 Form 10-K. Dollars

amounts are in millions.

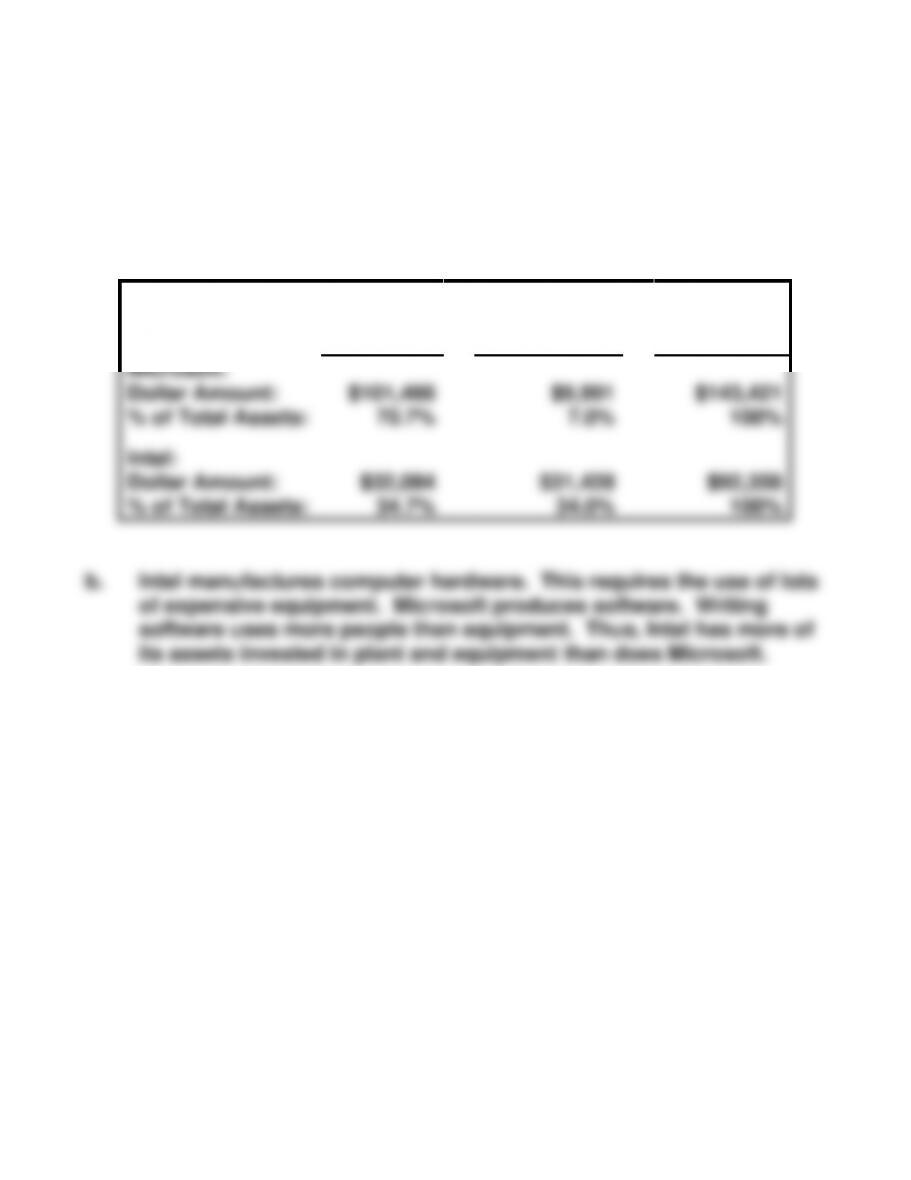

a.

Current

Assets

Property,

Plant and

Equipment

Total

Assets

Microsoft:

Dollar Amount:

$101,466

$9,991

$143,421

% of Total Assets:

70.7%

7.0%

100%

Intel:

Dollar Amount:

$32,084

$31,428

$92,358

% of Total Assets:

34.7%

34.0%

100%

b. Intel manufactures computer hardware. This requires the use of lots

of expensive equipment. Microsoft produces software. Writing

software uses more people than equipment. Thus, Intel has more of

its assets invested in plant and equipment than does Microsoft.

8-72

EXERCISE 8-1B

Note: There are many possibilities for answers to this question. The

answers given are only a few examples of long-term operational assets

that these companies may own. Also note that even though the

8-73

EXERCISE 8-2B

Event

Long-Term Operational Asset

a.

No

b.

Yes

c.

Yes

d.

No

e.

No

f.

Yes

g.

No

h.

Yes

i.

Yes (If the company is in a business that uses or sells timber)

j.

Yes (As long as it is not held for investment purposes)

k.

Yes

l.

Yes

8-74

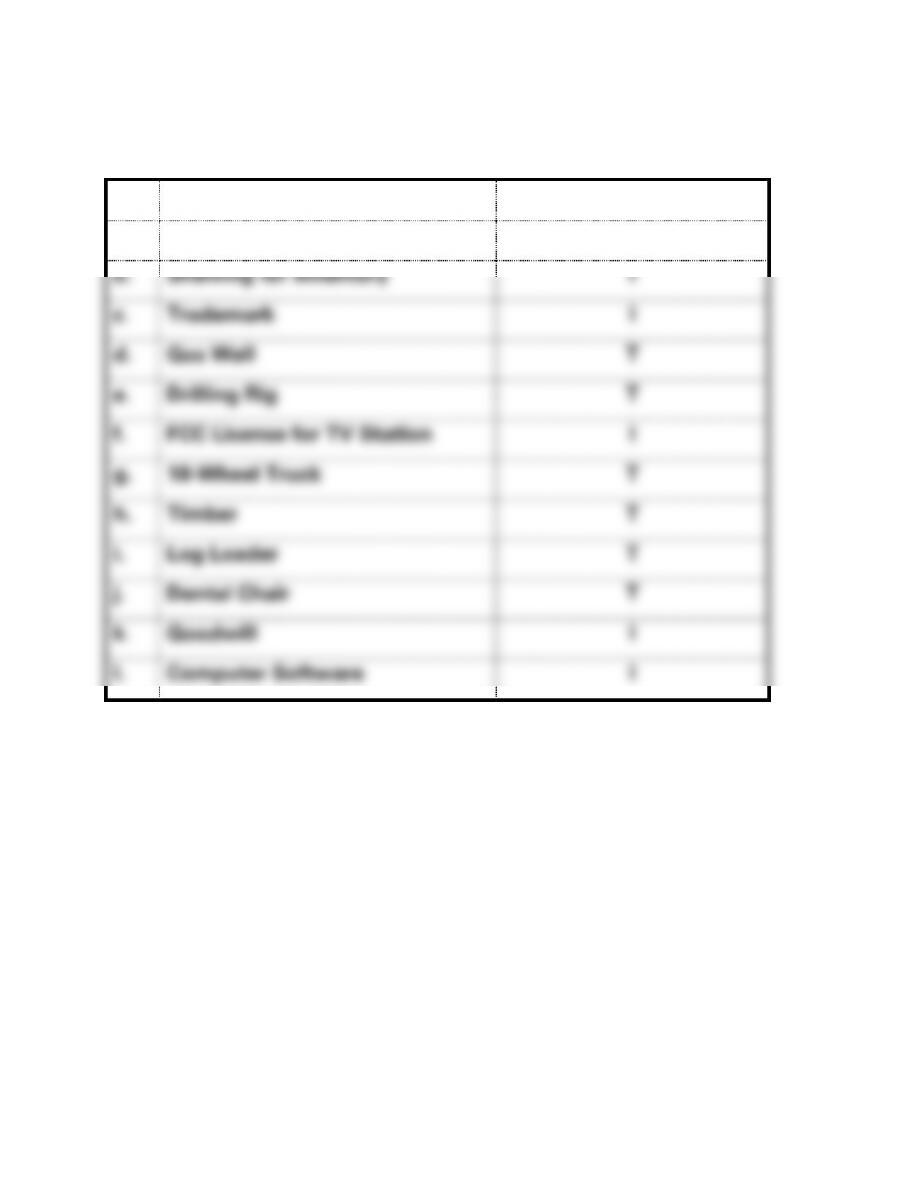

EXERCISE 8-3B

No.

Tangible (T), Intangible (I)

a.

Retail Store Building

T

b.

Shelving for Inventory

T

c.

Trademark

I

d.

Gas Well

T

e.

Drilling Rig

T

f.

FCC License for TV Station

I

g.

18-Wheel Truck

T

h.

Timber

T

i.

Log Loader

T

j.

Dental Chair

T

k.

Goodwill

I

l.

Computer Software

I

EXERCISE 8-4B

a.

Costs that are to be capitalized:

List Price $160,000

Less: Discount (8,000)*

EXERCISE 8-5B

a. Basket Purchase

b. % of* Purchase Allocated

Total Appraised Value App. Val. Price Cost

EXERCISE 8–6B

a.

Asset

Appraised Value

Percent of Appraised Value

Land

$200,000

25%

Building

480,000

60%

Equipment

120,000

15%

Total

$800,000

100%

Asset

% of App. Value

Purchase Price

Allocated Cost

Land

25%

x

$600,000

=

$150,000

Building

60%

x

600,000

=

360,000

Equipment

15%

x

600,000

=

90,000

Total

$600,000

Land

150,000

Building

360,000

Equipment

90,000

Cash

600,000

8-64

EXERCISE 8-7B

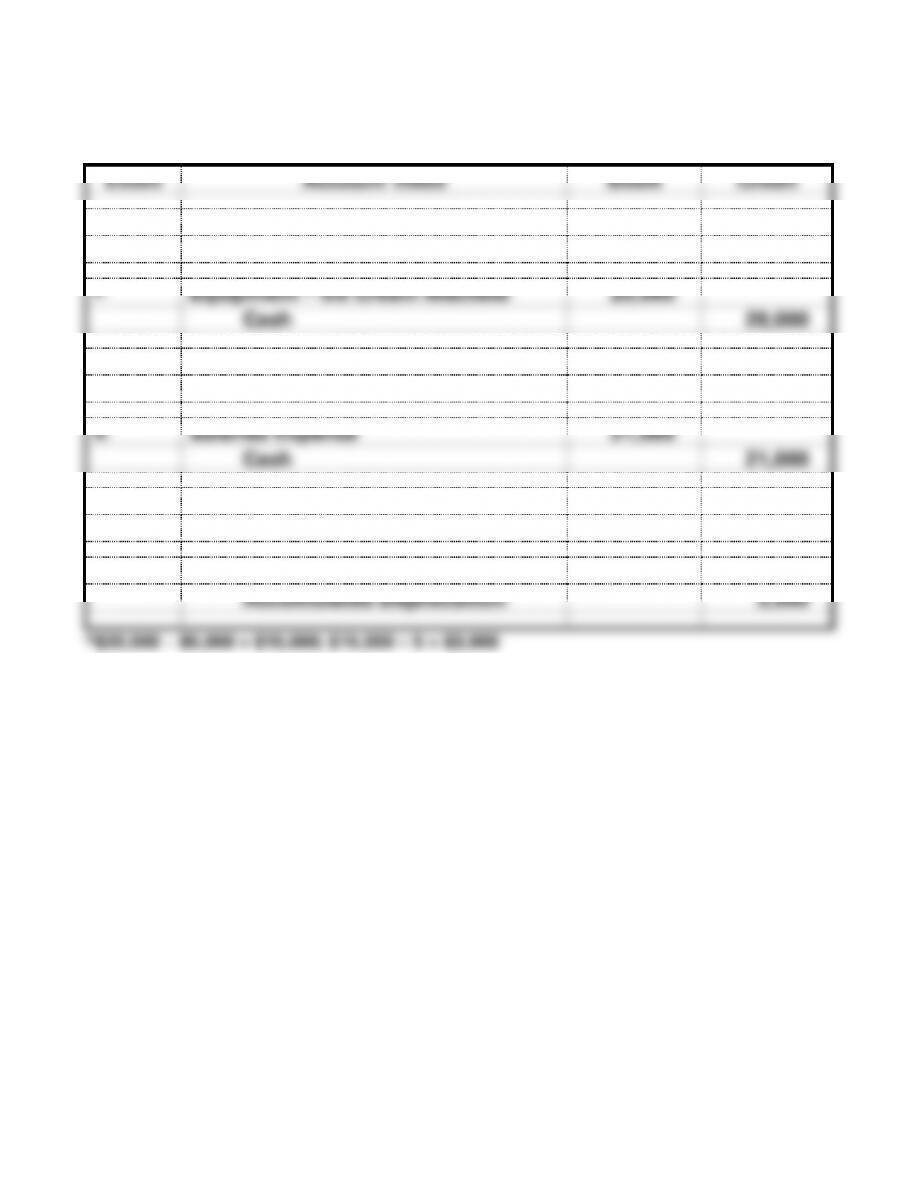

a.

Event

Account Titles

Debit

Credit

1.

Cash

20,000

Common Stock

20,000

2.

Equipment – Ice Cream Machine

20,000

Cash

20,000

3.

Cash

36,000

Sales Revenue

36,000

4.

Salaries Expense

21,000

Cash

21,000

5.

Operating Expenses

6,000

Cash

6,000

6.

Depreciation Expense*

3,000

Accumulated Depreciation

3,000