6-32

SOLUTIONS TO EXERCISES – SERIES B – CHAPTER 6

EXERCISE 6-1B

a. SOX refers to the Sarbanes-Oxley Act of 2002.

b. COSO stand for The Committee of Sponsoring Organizations of the

1. Control Environment. The integrity and ethical values of the

2. Risk Assessment. Management’s process of identifying

3. Control Activities. These are the activities usually thought of as

“the internal control.” They include such things as separation of

4. Information and Communication. The internal and external

5. Monitoring. Assessing the quality of a company’s internal

control over time and taking actions as necessary to ensure it

6-33

6-34

EXERCISE 6-2B

a. The two categories of internal controls are accounting controls and

administrative controls.

6-35

EXERCISE 6-3B

Some of the internal control features that should be included in the memo

to Stand Oden:

• Have as much separation of duties as possible. The manager should

6-36

EXERCISE 6-4B

a. The discrepancy was most likely caused by theft by Sally Knox, the

parts department manager. It is unlikely that sloppy recordkeeping

could account for this much of a difference. The manager could have

6-37

EXERCISE 6-5B

• Receipts should be promptly written for all cash received and the funds

deposited timely in a bank or other financial institution.

6-38

EXERCISE 6-6B

1. Quality of Employees

2. Bonded Employees

3. Authority and Responsibility

4. Physical Controls

5. Performance Evaluations

6-39

EXERCISE 6-7B

a. & c.

Hibbert Supplies

Statements Model

Assets

=

Liab.

+

S. Equity

Rev.

−

Exp.

=

Net Inc.

Cash Flow

Cash

+

Acct. Rec.

=

+

(a) (300)

+

300

=

NA

+

NA

NA

−

NA

=

NA

(300) OA

(c) 325

+

(300)

=

NA

+

25

25

−

NA

=

25

325 OA

b. Asset exchange.

c. See financial statements model above. The $25 fee is miscellaneous

income.

d. Asset Exchange is $300 and Asset Source is $25.

e.

Event

Account Titles

Debit

Credit

a.

Accounts Receivable

300

Cash

300

c.

Cash

325

Accounts Receivable

300

Miscellaneous Income

25

6-40

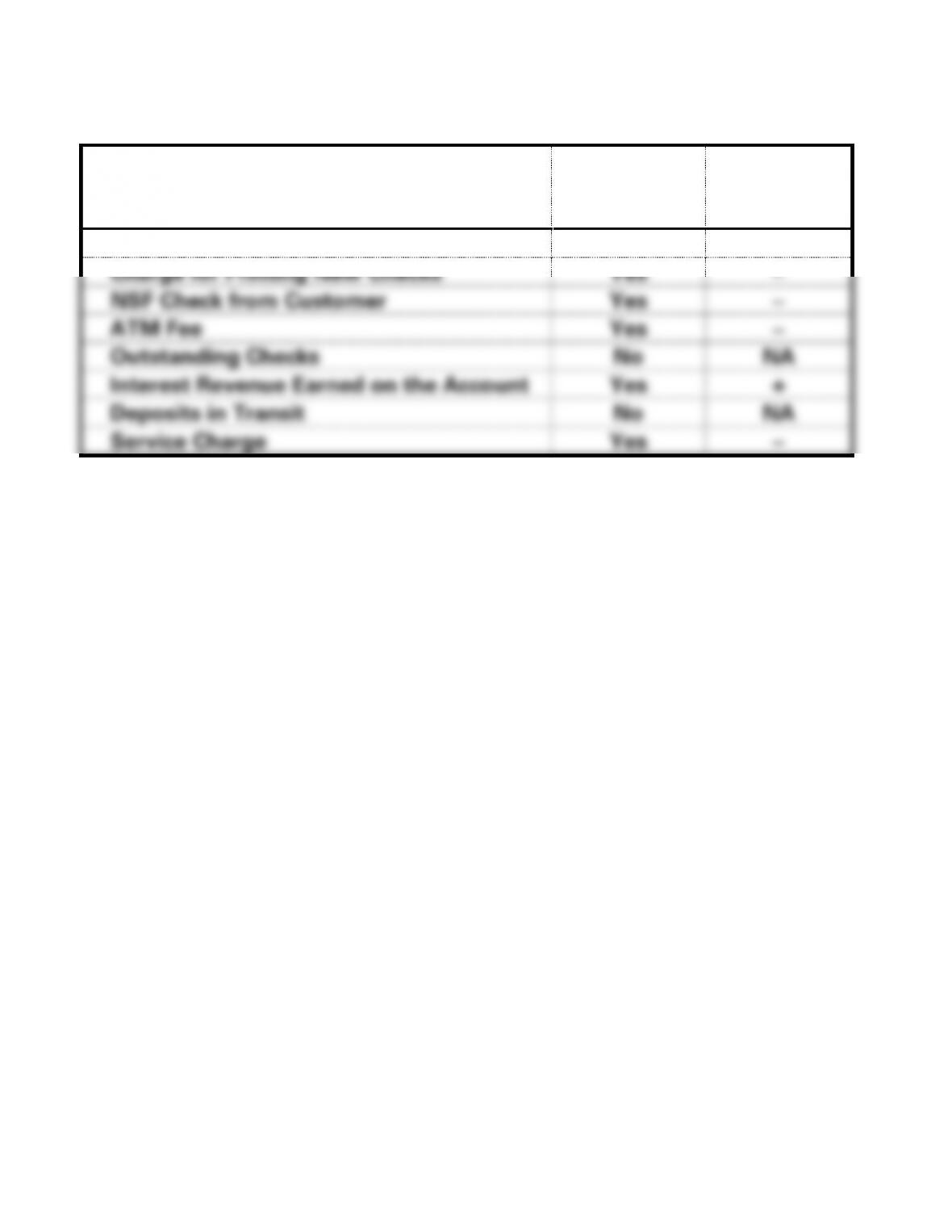

EXERCISE 6-8B

Reconciling Items

Book

Balance

Adjusted?

Added or

Subtracted?

Automatic Debit for Utility Bill

Yes

−

Charge for Printing New Checks

Yes

−

NSF Check from Customer

Yes

−

ATM Fee

Yes

−

Outstanding Checks

No

NA

Interest Revenue Earned on the Account

Yes

+

Deposits in Transit

No

NA

Service Charge

Yes

−

6-41

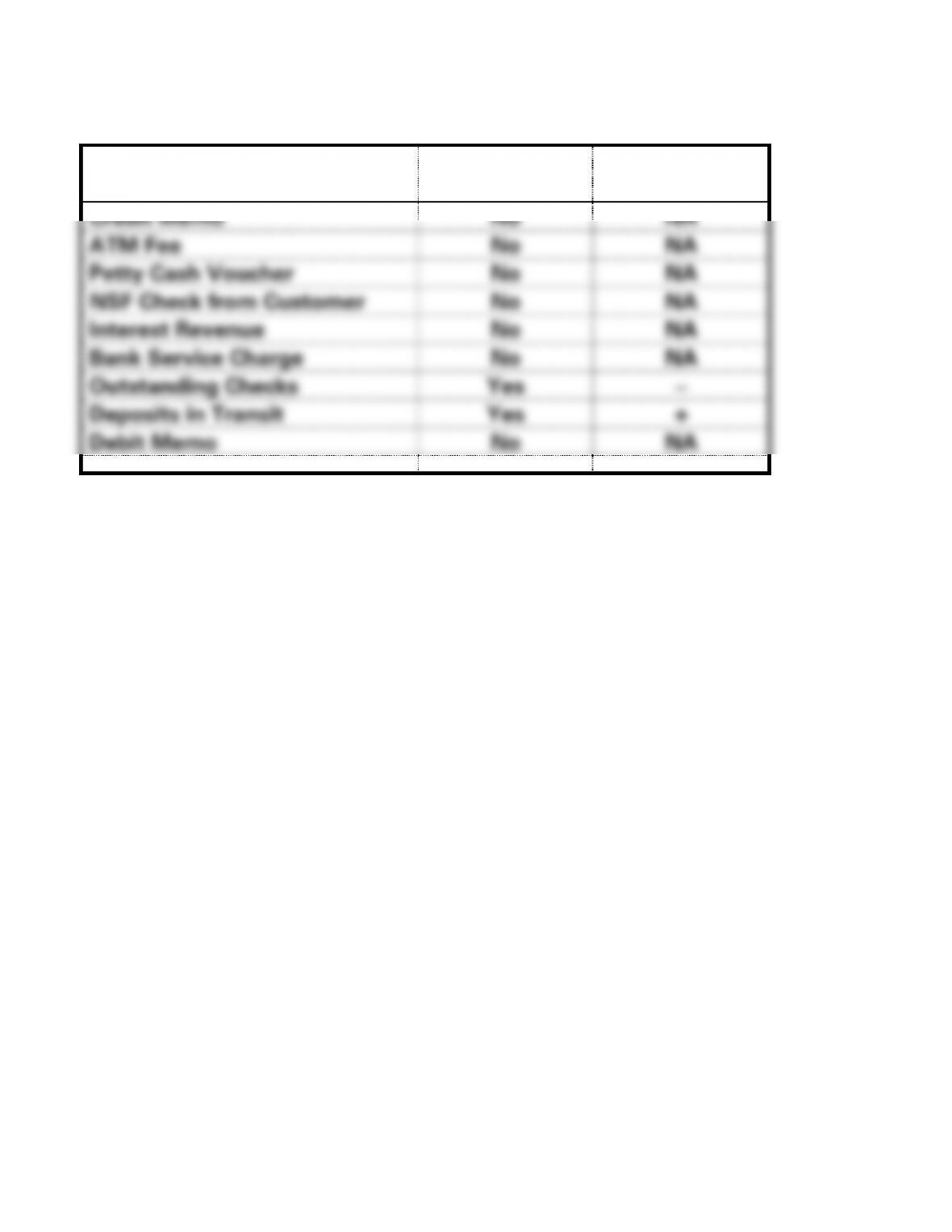

EXERCISE 6-9B

Reconciling Items

Bank Balance

Adjusted?

Added or

Subtracted?

Credit Memo

No

NA

ATM Fee

No

NA

Petty Cash Voucher

No

NA

NSF Check from Customer

No

NA

Interest Revenue

No

NA

Bank Service Charge

No

NA

Outstanding Checks

Yes

−

Deposits in Transit

Yes

+

Debit Memo

No

NA

6-42

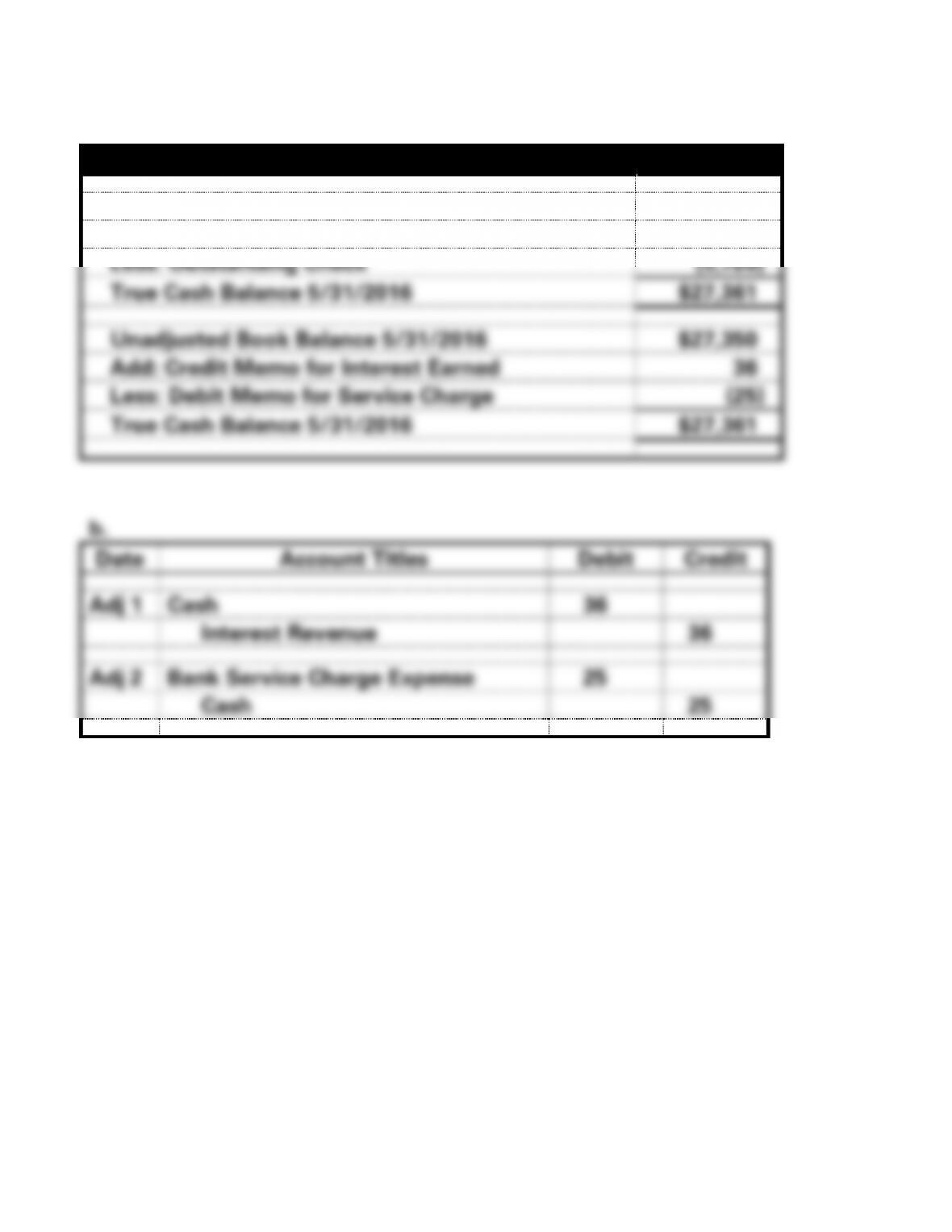

EXERCISE 6-10B

a.

Bank Reconciliation

Unadjusted Bank Balance 5/31/2016

$26,100

Add: Deposit in Transit

6,981

Less: Outstanding Check

(5,720)

True Cash Balance 5/31/2016

$27,361

Unadjusted Book Balance 5/31/2016

$27,350

Add: Credit Memo for Interest Earned

36

Less: Debit Memo for Service Charge

(25)

True Cash Balance 5/31/2016

$27,361

b.

Date

Account Titles

Debit

Credit

Adj 1

Cash

36

Interest Revenue

36

Adj 2

Bank Service Charge Expense

25

Cash

25

6-43

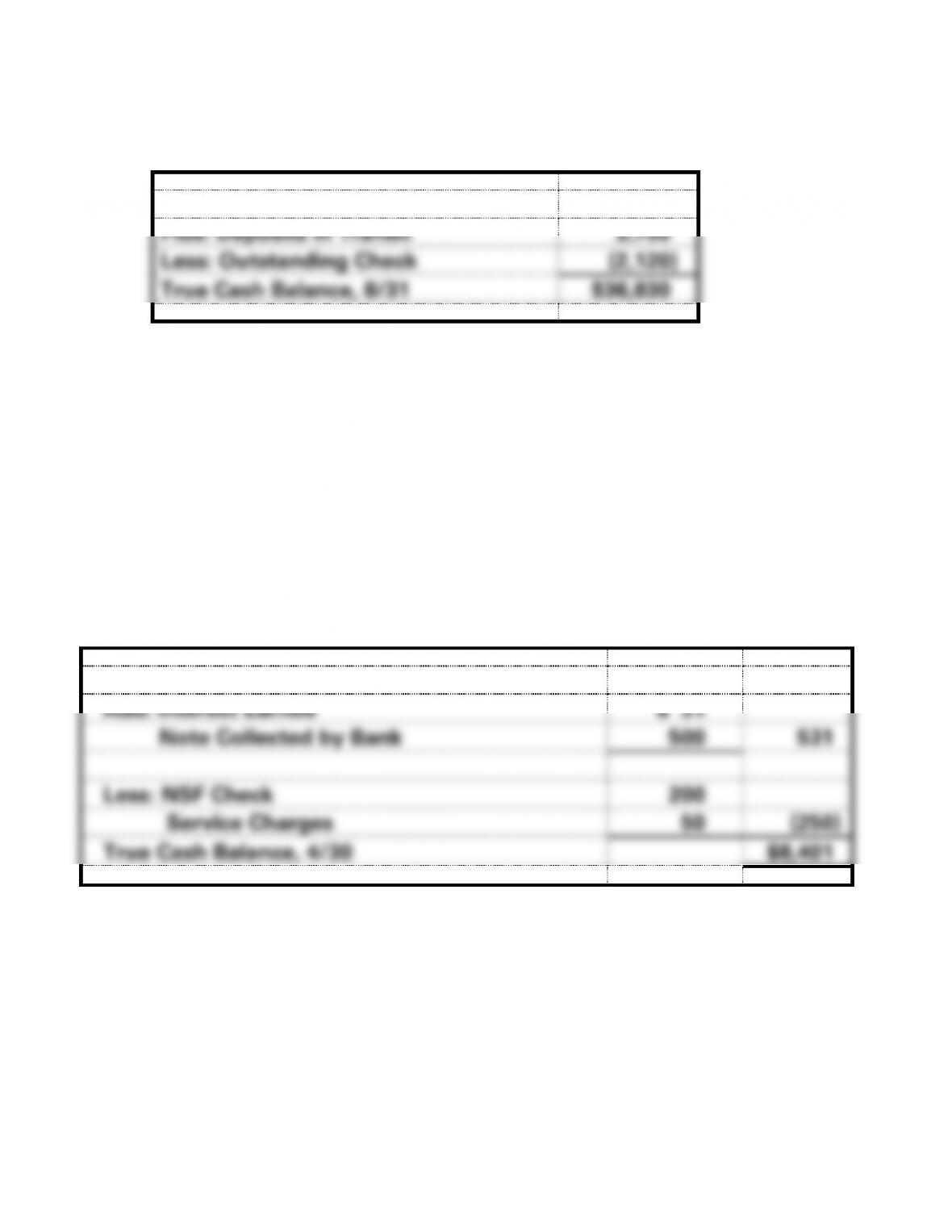

EXERCISE 6-11B

Unadjusted Bank Balance, 8/31

$35,200

Plus: Deposits in Transit

3,750

Less: Outstanding Check

(2,120)

True Cash Balance, 8/31

$36,830

EXERCISE 6-12B

Unadjusted Book Balance, 4/30

$8,120

Add: Interest Earned

$ 31

Note Collected by Bank

500

531

Less: NSF Check

200

Service Charges

50

(250)

True Cash Balance, 4/30

$8,401

EXERCISE 6-13B

6-45

EXERCISE 6-14B

a.

Payton, Inc.

Statements Model

Assets

=

S. Equity

Rev.

−

Exp.

=

Net Inc.

Statement

No.

Cash

+

Petty

Cash

=

Ret. Earn.

of

Cash Flows

1.

(150.00)

+

150.00

=

NA

NA

−

NA

=

NA

NA

2.

NA

+

NA

=

NA

NA

−

NA

=

NA

NA

3.

(141.80)*

+

NA

=

(141.80)

NA

−

141.80

=

(141.80)

(141.80) OA

*$150.00 − $8.20 = $141.80

b.

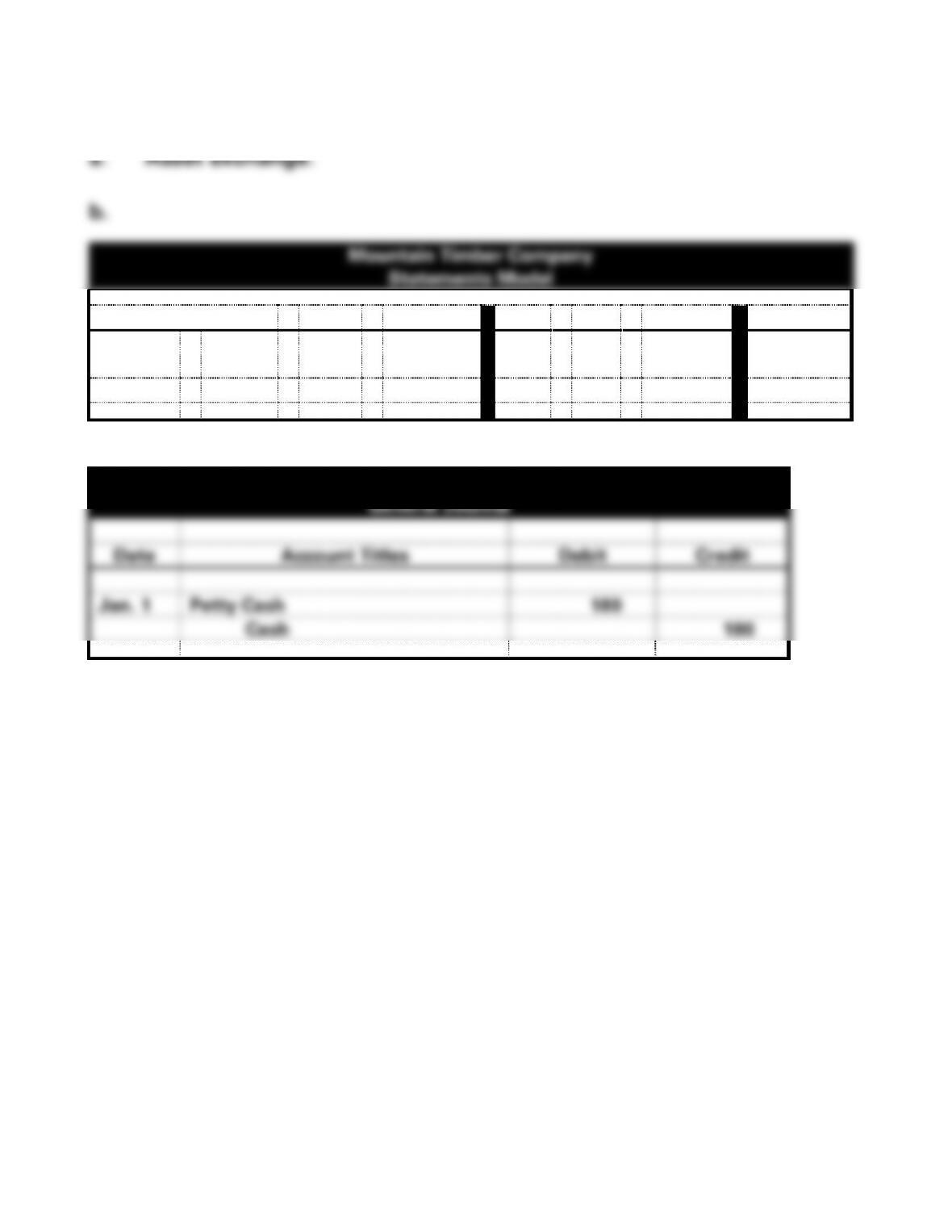

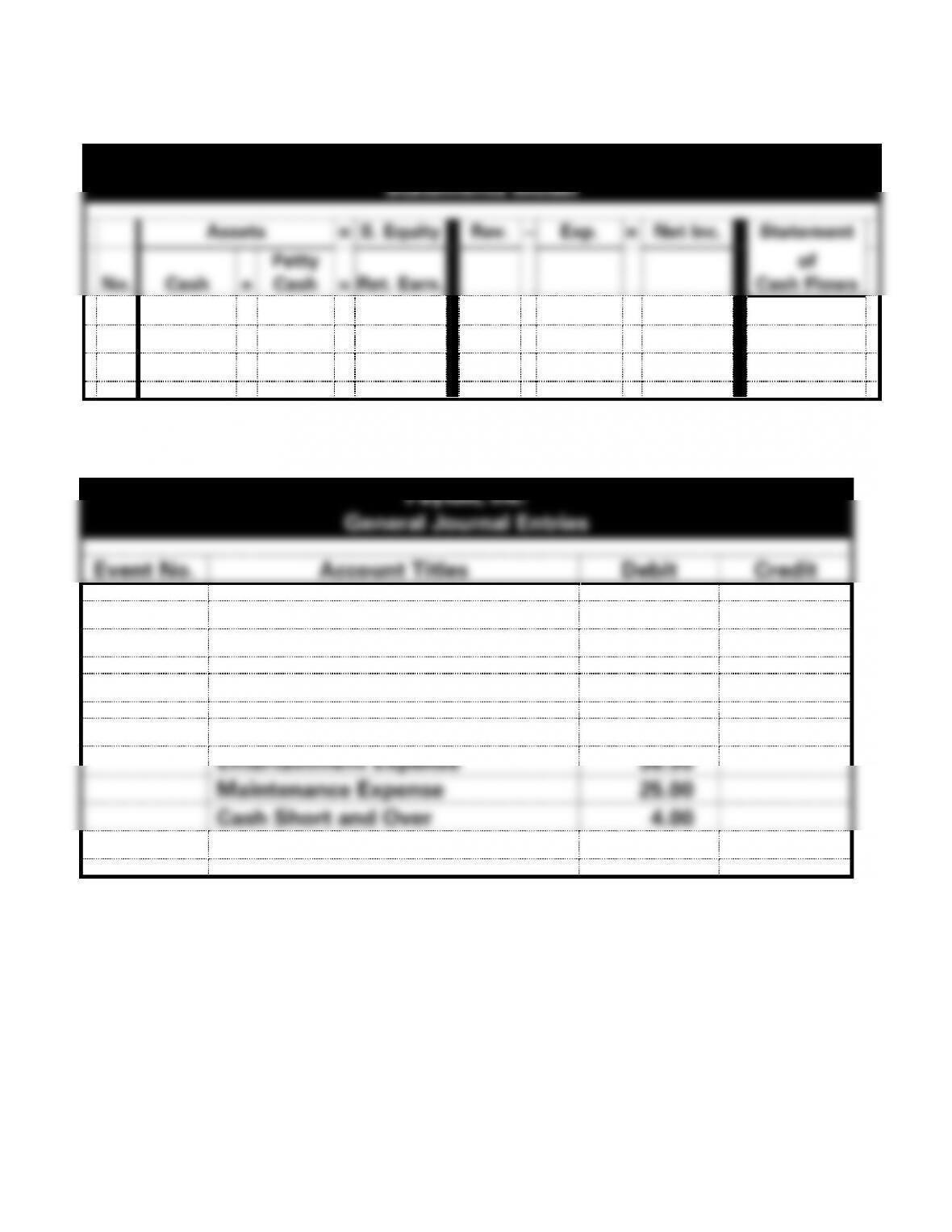

Payton, Inc.

General Journal Entries

Event No.

Account Titles

Debit

Credit

1.

Petty Cash

150.00

Cash

150.00

2.

No Entries

3.

Postage and Office Expense

76.30

Entertainment Expense

36.50

Maintenance Expense

25.00

Cash Short and Over

4.00

Cash

141.80

6-46

EXERCISE 6-15B

$171.40, the amount of the vouchers; cash short and over will be

6-47

EXERCISE 6-16B

The memo should contain some of the following information:

Something is considered material if knowing about the problem would

6-48

PROBLEM 6-17B

a. Separation of duties would have helped to prevent this type of act.

The authority function, check writing function, and check delivery

function should have been separated.

6-49

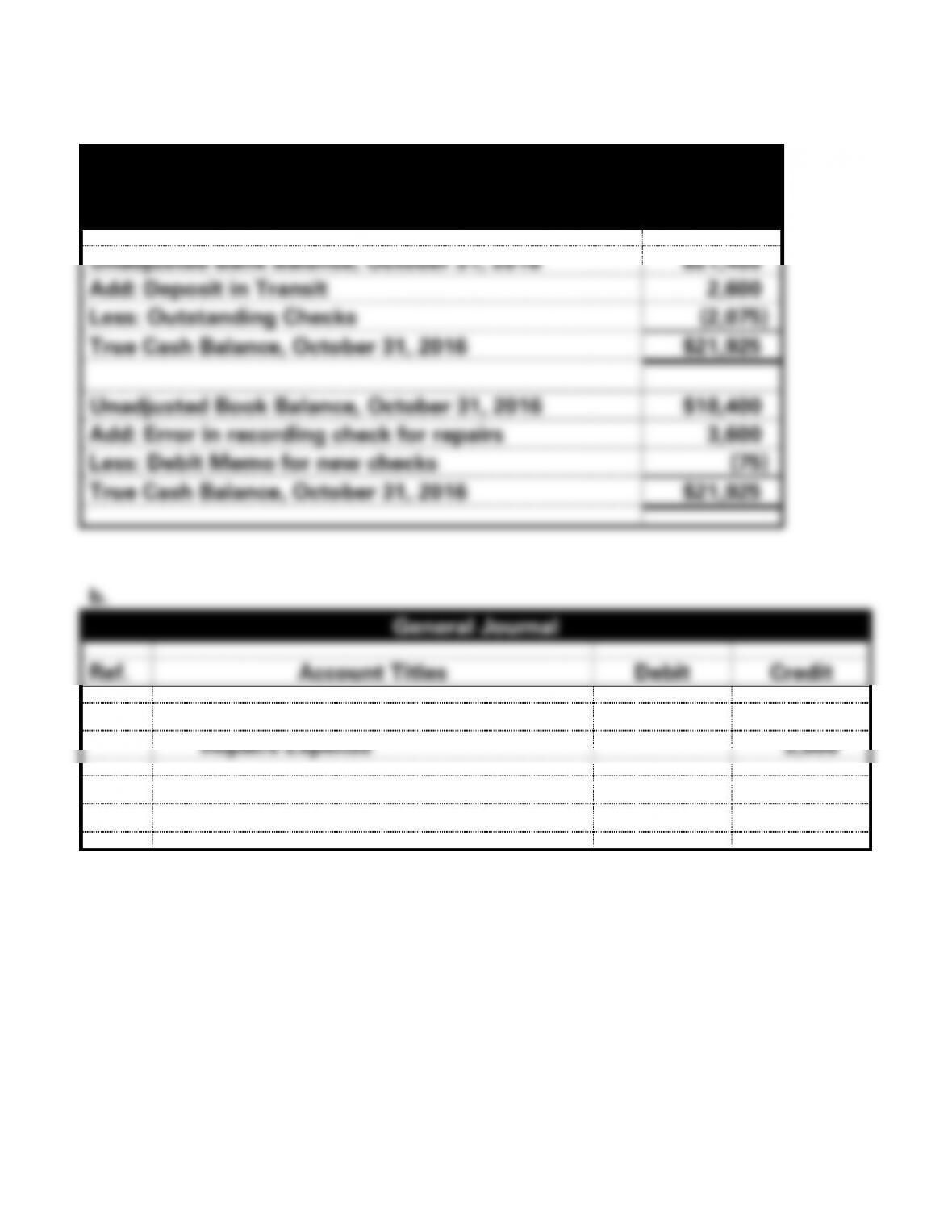

PROBLEM 6-18B

a.

Lewis Supply Co.

Bank Reconciliation

October 31, 2016

Unadjusted Bank Balance, October 31, 2016

$21,400

Add: Deposit in Transit

2,600

Less: Outstanding Checks

(2,075)

True Cash Balance, October 31, 2016

$21,925

Unadjusted Book Balance, October 31, 2016

$18,400

Add: Error in recording check for repairs

3,600

Less: Debit Memo for new checks

(75)

True Cash Balance, October 31, 2016

$21,925

b.

General Journal

Ref.

Account Titles

Debit

Credit

1.

Cash

3,600

Repairs Expense

3,600

2.

Office Supplies Expense

75

Cash

75

6-50

PROBLEM 6-19B

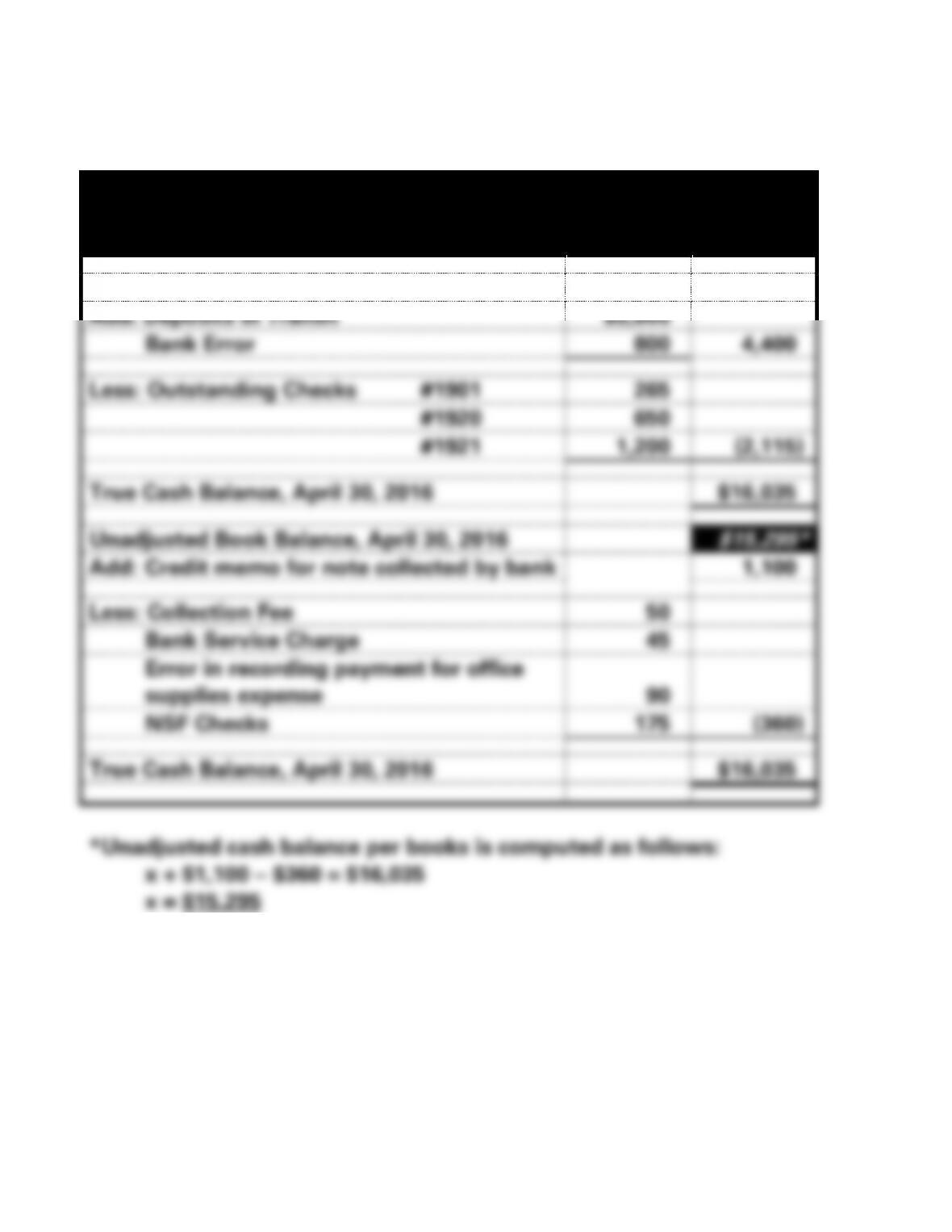

Woods Sports Inc.

Bank Reconciliation

April 30, 2016

Unadjusted Bank Balance, April 30, 2016

$13,750

Add: Deposits in Transit

$3,600

Bank Error

800

4,400

Less: Outstanding Checks #1901

265

#1920

650

#1921

1,200

(2,115)

True Cash Balance, April 30, 2016

$16,035

Unadjusted Book Balance, April 30, 2016

$15,295*

Add: Credit memo for note collected by bank

1,100

Less: Collection Fee

50

Bank Service Charge

45

Error in recording payment for office

supplies expense

90

NSF Checks

175

(360)

True Cash Balance, April 30, 2016

$16,035

*Unadjusted cash balance per books is computed as follows:

x + $1,100 − $360 = $16,035

x = $15,295

6-51

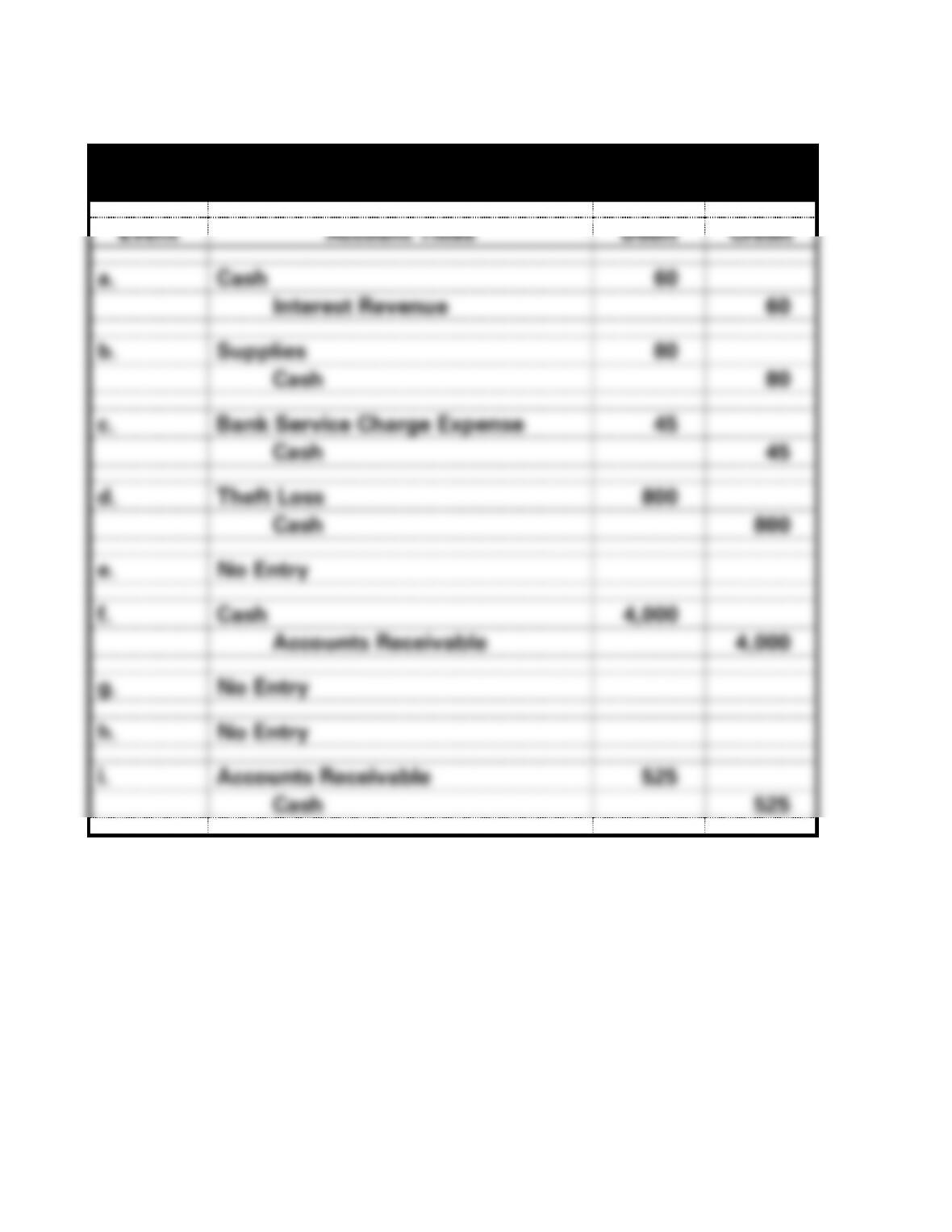

PROBLEM 6-20B

China Imports

General Journal

Event

Account Titles

Debit

Credit

a.

Cash

60

Interest Revenue

60

b.

Supplies

80

Cash

80

c.

Bank Service Charge Expense

45

Cash

45

d.

Theft Loss

800

Cash

800

e.

No Entry

f.

Cash

4,000

Accounts Receivable

4,000

g.

No Entry

h.

No Entry

i.

Accounts Receivable

525

Cash

525