7–6

ANSWERS TO QUESTIONS – CHAPTER 7

1. Accounts receivable are the expected future receipts when a

company permits its customers to buy now and pay later. The

2. The net realizable value is the amount expected to be collected

3. Allowance for Doubtful Accounts is a contra asset account.

4. Estimating uncollectible accounts expense improves the accuracy

of financial statements by (1) reporting expected realizable value

5. When using the allowance method, uncollectible accounts

expense is matched with current revenues. A company does not

6. The most common format for reporting accounts receivable on

the balance sheet is gross receivables less the allowance for

7. The practice of reestablishing a previously written off account,

then recording its collection as a payment on account, reflects a

7–7

8. Factors for use in estimating uncollectible accounts include:

(1) the percentage of uncollectible accounts from years past.

9. Recognizing uncollectible accounts expense reduces net accounts

10. A write-off of an uncollectible account when the allowance

method is used has no effect on the accounting equation because

expense).

11. The recovery of an uncollectible account when the allowance

method is used does not affect the income statement. Only

12. The advantage of using the allowance method is that it improves

13. If the company is an established business, it will examine its

credit history; that is, the actual write-offs for the previous year as

14. The percent of receivables is a more accurate measure because it

7–8

currently been outstanding. Those receivables that have been

15. When using an aging schedule for estimating uncollectible

accounts, accounts receivable is divided into categories based on

16. The allowance method is a method of accounting for bad debts

where bad debts are estimated and expensed in the same period

17. The direct write-off method is not GAAP, but is allowed if the

18. A promissory note is a legal document that sets forth credit terms

19. a. Maker: The borrower or debtor.

b. Payee: The person to whom the note is made

payable.

c. Principal: The amount of money loaned by the payee

20. Interest is computed as:

7–9

Principal X annual interest rate X time outstanding

21. Accrued interest is interest that has been earned but not yet

7–10

22. The adjusting entry for accrued interest is generally only recorded

23. Big Corp. would report interest revenue of $360 for 2016

computed as follows:

24. When Big Corp. collects the $12,720, $12,000 will be reported as

25. It is generally beneficial to accept major credit cards because the

business then avoids the risk of bad debts as well as the cost of

26. The acceptance of major credit cards enables a business to avoid

the cost of uncollectible accounts and the clerical costs of

27. Accounts

Receivable = Sales

28. Average Days

7–11

This ratio tells the user how many days on average it takes a

29. No, accounting terminology is not standard even in English–

speaking countries. In the U.K. sales are called “turnover,”

30. The operating cycle is the length of time it takes to convert

7–12

EXERCISE 7-1A

Event

Assets

=

Liab.

+

Equity

Rev.

–

Exp.

=

Net Inc.

Cash Flows

1.

−

=

NA

+

−

NA

−

+

=

−

NA

2.

+/−

=

NA

+

NA

NA

−

NA

=

NA

NA

3.

+

=

NA

+

+

+

−

NA

=

+

NA

4.

+/−

=

NA

+

NA

NA

−

NA

=

NA

+ OA

7–13

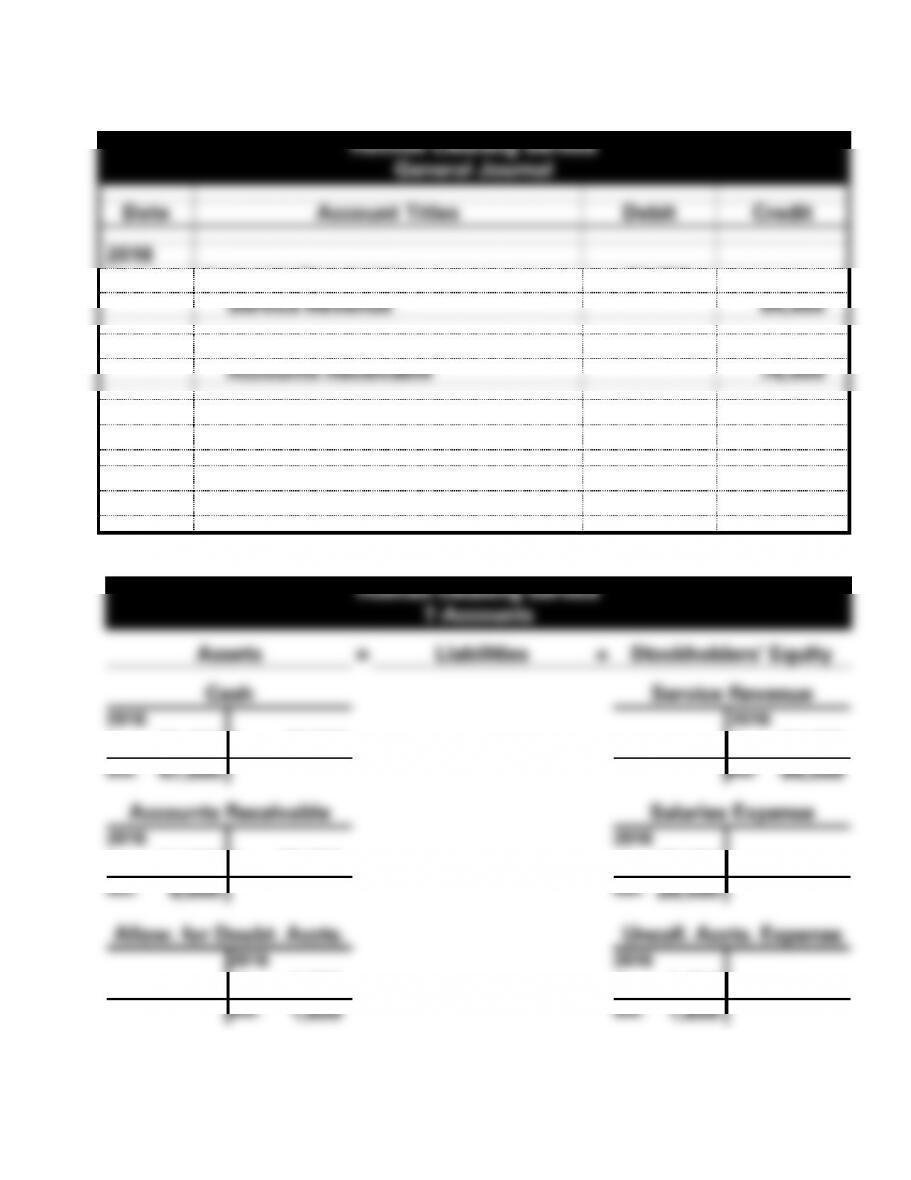

EXERCISE 7-2A a.

Holmes Cleaning Service

General Journal

Date

Account Titles

Debit

Credit

2016

1.

Accounts Receivable

84,000

Service Revenue

84,000

2.

Cash

76,000

Accounts Receivable

76,000

3.

Salaries Expense

28,500

Cash

28,500

4.

Uncollectible Accounts Expense

1,650

Allowance for Doubtful Accounts

1,650

b.

Holmes Cleaning Service

T-Accounts

Assets

=

Liabilities

+

Stockholders’ Equity

Cash

Service Revenue

2016

2016

2.

76,000

3.

28,500

1.

84,000

Bal.

47,500

Bal.

84,000

Accounts Receivable

Salaries Expense

2016

2016

1.

84,000

2.

76,000

3.

28,500

Bal.

8,000

Bal.

28,500

Allow. for Doubt. Accts.

Uncoll. Accts. Expense

2016

2016

4.

1,650

4.

1,650

Bal.

1,650

Bal.

1,650

EXERCISE 7-2A (cont.)

c.

Holmes Cleaning Service

Income Statement

For the Year Ended December 31, 2016

Service Revenue

$84,000

Operating Expenses

Salaries Expense

$28,500

Uncollectible Accounts Expense

1,650

Total Operating Expenses

(30,150)

Net Income

$53,850

Cash

$47,500

Accounts Receivable

Less: Allowance for Doubtful Accounts

Total Assets

$53,850

Liabilities

Retained Earnings

$53,850

Total Liabilities and Stockholders’ Equity

$53,850

7–15

EXERCISE 7-2A c. (cont.)

Holmes Cleaning Service

Statement of Cash Flows

For the Year Ended December 31, 2016

Cash Flows From Operating Activities:

Inflow from Customers

$76,000

Outflow for Expenses

(28,500)

Net Cash Flow from Operating Activities

$47,500

Cash Flows From Investing Activities

-0-

Cash Flows From Financing Activities

-0-

Net Change in Cash

47,500

Plus: Beginning Cash Balance

-0-

Ending Cash Balance

$47,500

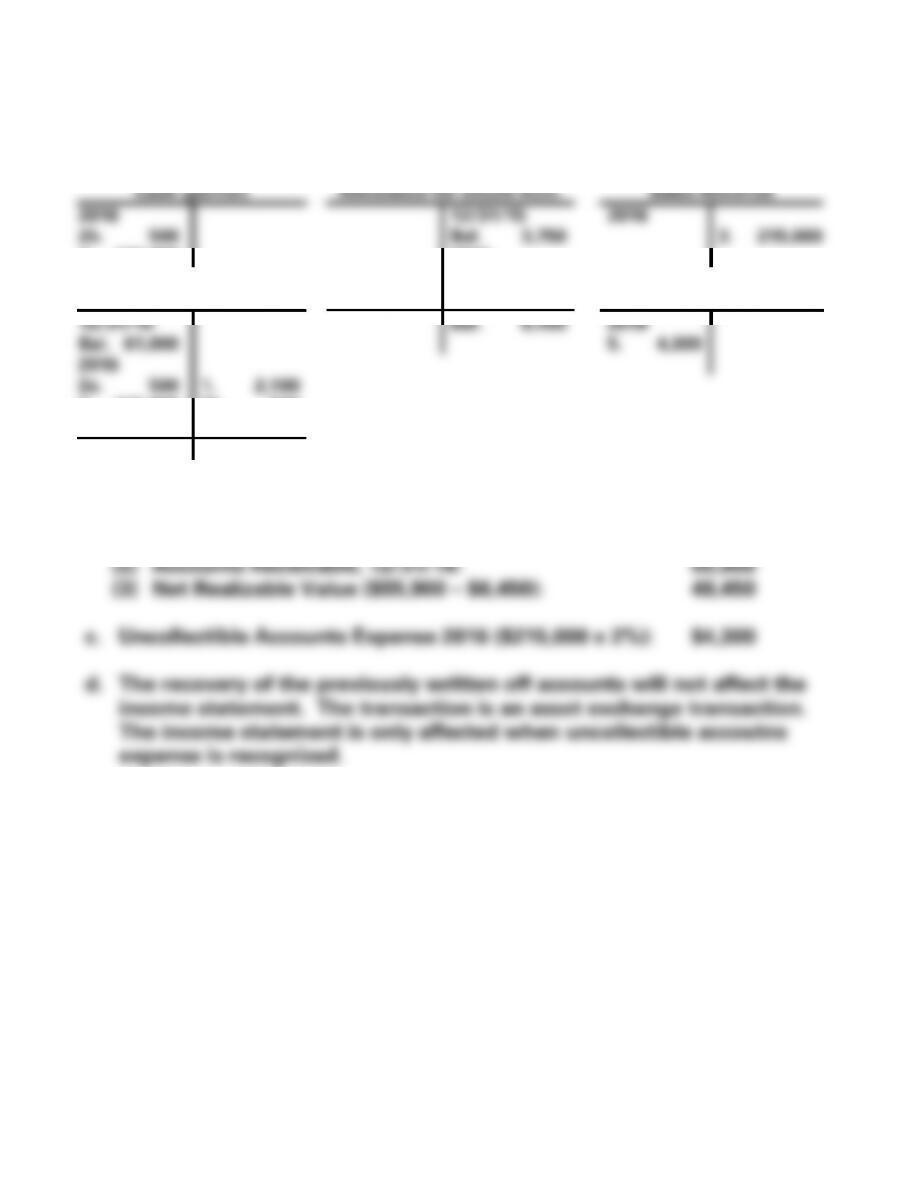

EXERCISE 7-3A

a. Analyze the Accounts Receivable account:

Accounts Receivable

Beginning Balance

$ 2,800

Plus: Revenue on Account

14,000

Less: Write-off

(150)

Less: Ending Balance

(3,600)

Collections of Accounts Rec.

$13,050

Beginning Balance

Less: Write-off

Less: Ending Balance

Uncollectible Accounts Expense

7–17

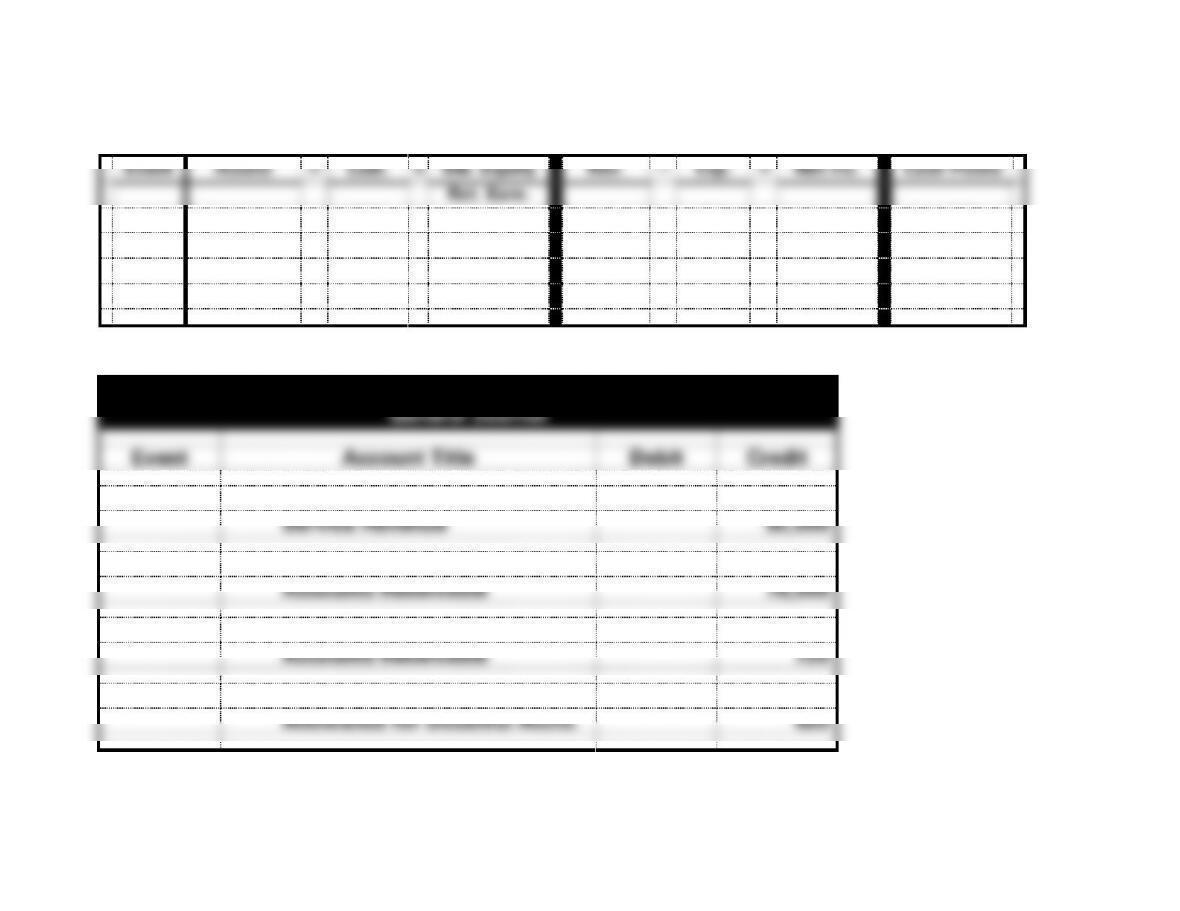

EXERCISE 7-4A

a. and c.

Rosie Dry Cleaning

T-Accounts

Assets

=

Liabilities

+

Stockholders’ Equity

Cash

Retained Earnings

2016

2016

2.

39,000

cl

450

cl

45,000

Bal.

39,000

Bal.

44,550

2017

3.

61,000

Service Revenue

Bal.

100,000

2016

cl

45,000

1.

45,000

Accounts Receivable

Bal.

-0-

2016

2017

1.

45,000

2.

39,000

2.

62,000

Bal.

6,000

Bal.

62,000

2017

2.

62,000

1.

300

Uncoll. Accts. Expense

3.

61,000

2016

Bal.

6,700

3.

450

cl

450

Bal.

-0-

Allow. For Doubt. Accts.

2017

2016

4.

620

3.

4501

Bal.

620

Bal.

450

2017

1.

300

4.

6202

Bal.

770

1$45,000 x 1% = $450

7–18

EXERCISE 7-4A (cont.)

(2) Net Cash Flow from Operating Activities: $39,000

(3) Balance of Accounts Receivable, 12/31/2016: $6,000

(4) Net Realizable Value of Accounts Receivable, 12/31/2016:

(2) Net Cash Flow from Operating Activities: $61,000

(3) Balance of Accounts Receivable, 12/31/2017: $6,700

(4) Net Realizable Value of Accounts Receivable, 12/31/2017:

7–19

EXERCISE 7-5A

a.

Event

Assets

=

Liab.

+

Stk. Equity

Rev.

–

Exp.

=

Net Inc.

Cash Flows

Ret. Earn.

1.

+

NA

+

+

NA

+

NA

2.

+/−

NA

NA

NA

NA

NA

+ OA

3.

+/−

NA

NA

NA

NA

NA

NA

4.

−

NA

−

NA

+

−

NA

b.

Grover, Inc.

General Journal

Event

Account Title

Debit

Credit

1.

Accounts Receivable

92,000

Service Revenue

92,000

2.

Cash

78,000

Accounts Receivable

78,000

3.

Allowance for Doubtful Accts.

720

Accounts Receivable

720

4.

Uncollectible Accounts Expense

920

Allowance for Doubtful Accts.

920

7–20

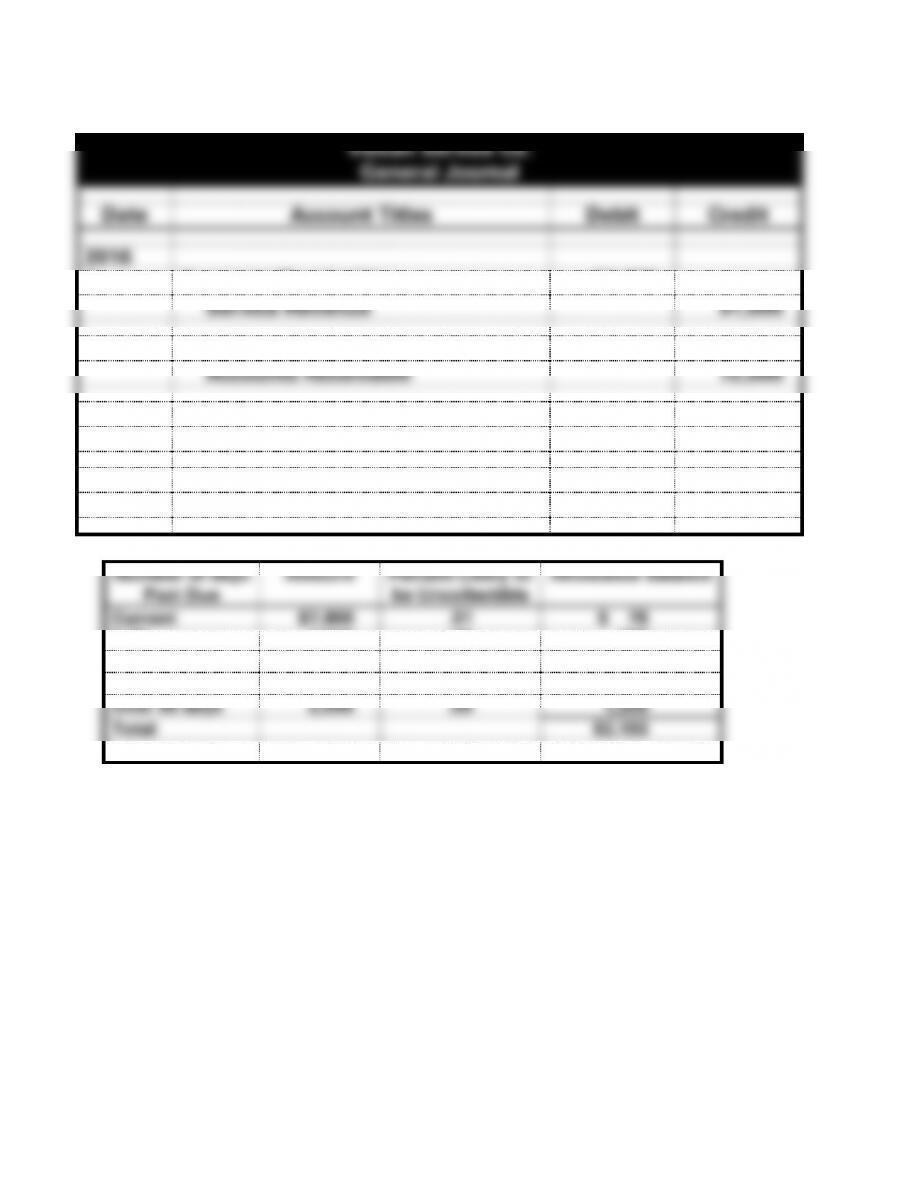

EXERCISE 7-6A

1. Uncollectible accounts written off: $2,100

3. Services on account: 215,000

4. Collections of accounts receivable: 218,000

5. Uncollectible Accounts Expense (215,000 x 2%): 4,300

Renue Spa

General Journal

Event

Account Title

Debit

Credit

2016

1.

Allowance for Doubtful Accounts

2,100

Accounts Receivable

2,100

2a.

Accounts Receivable

500

Allowance for Doubtful Accounts

500

2b.

Cash

500

Accounts Receivable

500

3.

Accounts Receivable

215,000

Service Revenue

215,000

4.

Cash

218,000

Accounts Receivable

218,000

5.

Uncollectible Accounts Expense

4,300

Allowance for Doubtful Accounts

4,300

7–21

EXERCISE 7-6A a. (cont.)

Selected T-Accounts:

Cash (partial)

Allowance for Doubt Acct.

Sales Revenue

2016

12/31/15

2016

2b. 500

Bal. 3,750

3. 215,000

4. 218,000

2016

1. 2,100

2a. 500

Accounts Receivable

5. 4,300

Uncoll. Accts. Expense

12/31/15

Bal. 6,450

2016

Bal. 61,000

5. 4,300

2016

2a. 500

1. 2,100

3. 215,000

2b. 500

4. 218,000

Bal. 55,900

b. (1) Allowance for Doubtful Accounts, 12/31/16: $ 6,450

7–22

EXERCISE 7-7A

a.

Vulcan Service Co.

General Journal

Date

Account Titles

Debit

Credit

2016

1.

Accounts Receivable

91,000

Service Revenue

91,000

2.

Cash

72,000

Accounts Receivable

72,000

3.

Salaries Expense

36,000

Cash

36,000

4.

Uncollectible Accounts Expense1

2,193

Allowance for Doubtful Accounts

2,193

1

Number of days

Past Due

Amount

Percent Likely to

be Uncollectible

Allowance Balance

Current

$7,800

.01

$ 78

0-30

4,500

.05

225

31–60

2,000

.10

200

61–90

2,200

.20

440

Over 90 days

2,500

.50

1,250

Total

$2,193

7–23

EXERCISE 7-7A a. (cont.)

Vulcan Service Co.

T-Accounts – 2016

Assets

=

Liabilities

+

Stockholders’ Equity

Cash

Service Revenue

2.

72,000

3.

36,000

1.

91,000

Bal.

36,000

Bal.

91,000

Accounts Receivable

Salaries Expense

1.

91,000

2.

72,000

3.

36,000

Bal.

19,000

Bal.

36,000

Allow. For Doubt. Accts.

Uncoll. Accts. Expense

4.

2,193

4.

2,193

Bal.

2,193

Bal.

2,193

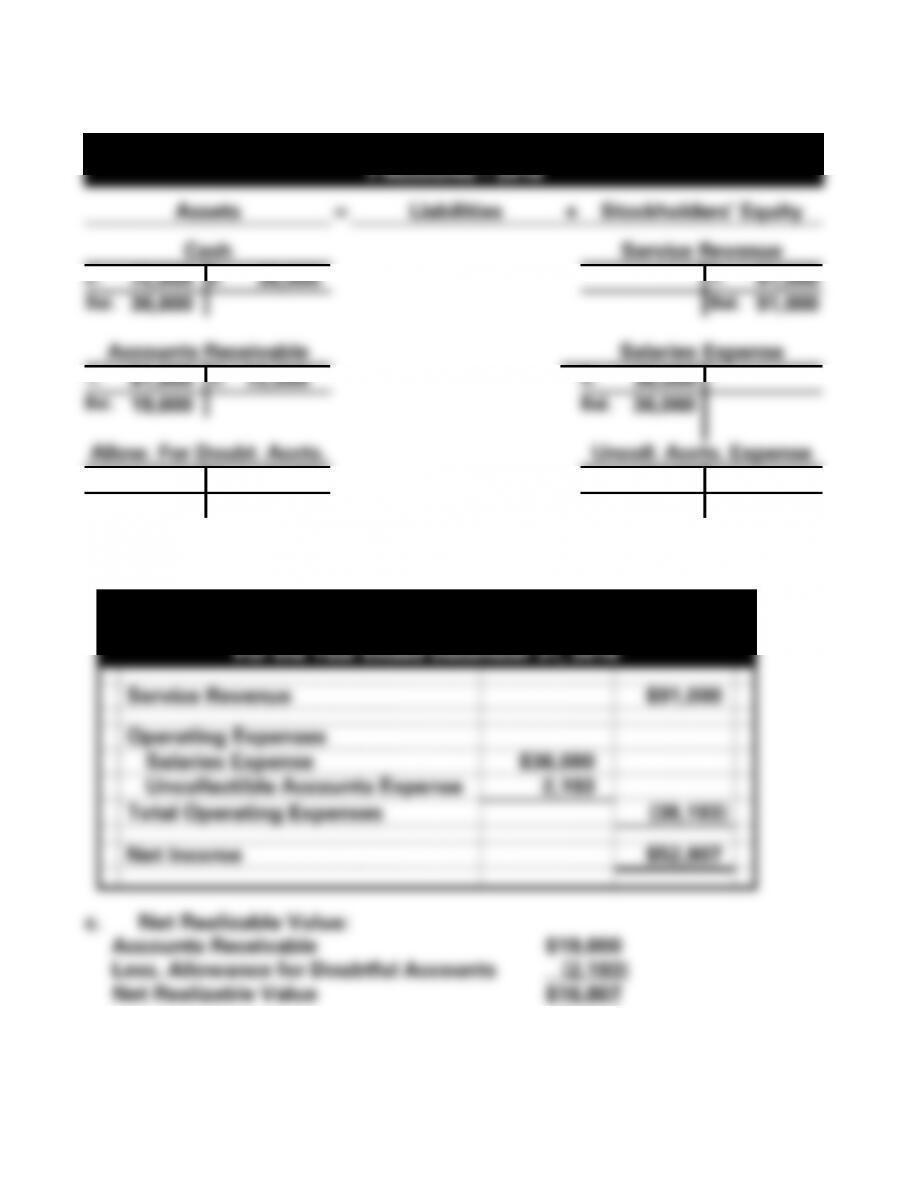

b.

Vulcan Service Co.

Income Statement

For the Year Ended December 31, 2016

Service Revenue

$91,000

Operating Expenses

Salaries Expense

$36,000

Uncollectible Accounts Expense

2,193

Total Operating Expenses

(38,193)

Net Income

$52,807

c. Net Realizable Value:

Accounts Receivable $19,000

Less, Allowance for Doubtful Accounts (2,193)

Net Realizable Value $16,807

7–24

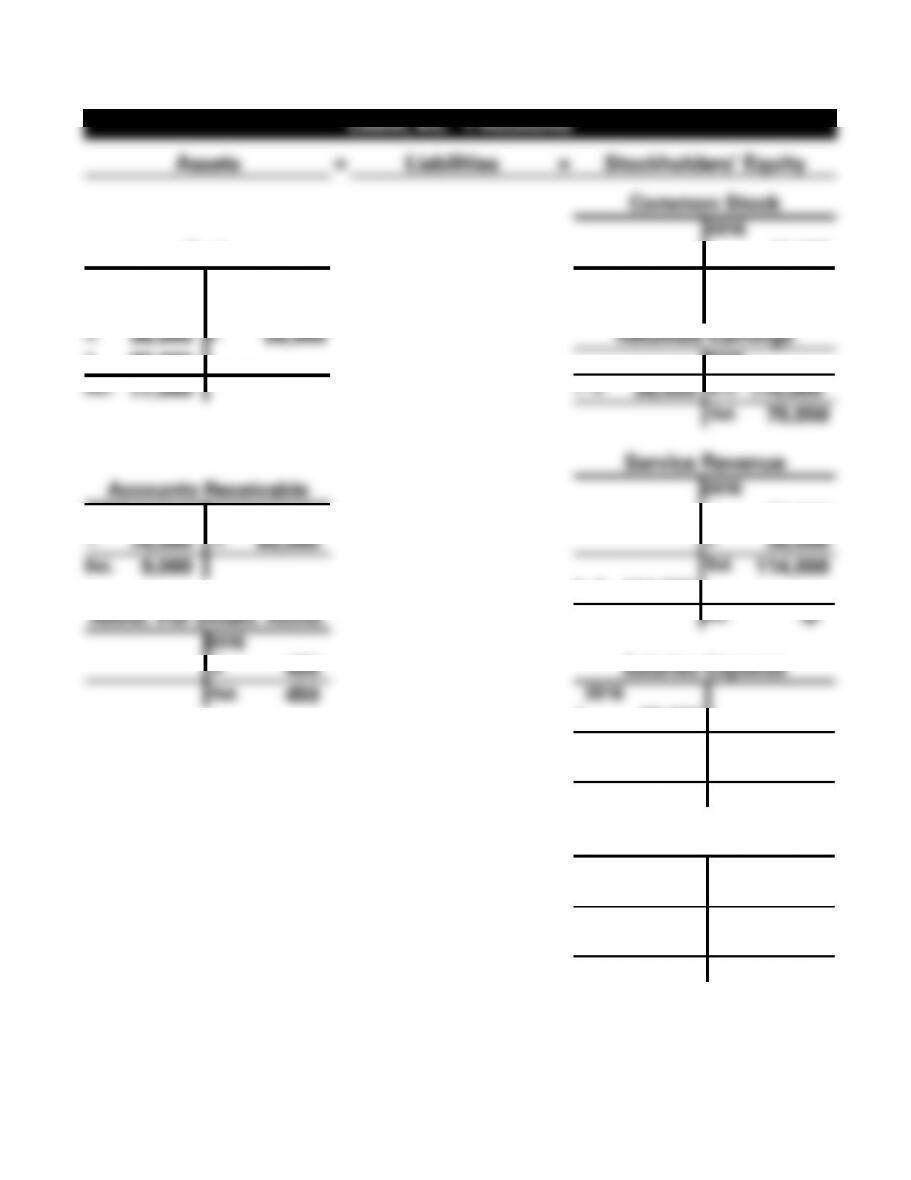

EXERCISE 7-8A

a.

Leach, Inc.

General Journal

Date

Account Titles

Debit

Credit

2016

1.

Cash

10,000

Common Stock

10,000

2.

Accounts Receivable

78,000

Service Revenue

78,000

3.

Cash

36,000

Service Revenue

36,000

4.

Cash

69,000

Accounts Receivable

69,000

5.

Salaries Expense

38,000

Cash

38,000

6.

Uncollectible Accounts Expense1

450

Allowance for Doubtful Accounts

450

7. cl

Service Revenue

114,000

Retained Earnings

114,000

8. cl

Retained Earnings

38,450

Uncollectible Accounts Exp.

450

Salaries Expense

38,000

7–25

EXERCISE 7-8A a. (cont.)

Leach, Inc. T-Accounts

Assets

=

Liabilities

+

Stockholders’ Equity

Common Stock

2016

Cash

1. 10,000

2016

Bal.

10,000

1. 10,000

3.

36,000

5.

38,000

Retained Earnings

4.

69,000

2016

Bal.

77,000

7. cl

38,450

6 cl.

114,000

Bal.

75,550

Service Revenue

Accounts Receivable

2016

2016

1.

78,000

1.

78,000

3.

69,000

2.

36,000

Bal.

9,000

Bal.

114,000

6. cl

114,000

Allow. For Doubt. Accts.

Bal.

-0-

2016

5.

450

Salaries Expense

Bal.

450

2016

4.

38,000

Bal.

38,000

7. cl

38,000

Bal.

-0-

Uncoll. Accts. Expense

2016

5.

450

Bal.

450

7. cl

450

Bal.

-0-