5-26

EXERCISE 5-6A (cont.)

c. Income tax paid using FIFO: $32,430

Income tax paid using LIFO: $31,710

d.

Parvin Company

Cash Flows from Operating Activities

FIFO

LIFO

Cash Flows From Operating Activities:

Cash Inflow from Customers

$243,000

$243,000

Cash Outflow for Inventory*

(92,800)

(92,800)

Cash Outflow for Operating Expense

(41,500)

(41,500)

Cash Outflow for Income Tax Expense

(32,430

(31,710)

Net Cash Flow from Operating Activities

$ 76,270

$ 76,990

*Computation of cash paid for inventory:

4/1 Purchase 2,000 units @ $35 = $70,000

10/1 Purchase 600 units @ 38 = 22,800

$92,800

e. The difference in cash flow from operating activities between FIFO

and LIFO is caused by the difference in income tax paid for the two

methods. Taxable income is greater by using FIFO; consequently

more income tax will be paid causing a greater cash outflow for tax

expense.

5-27

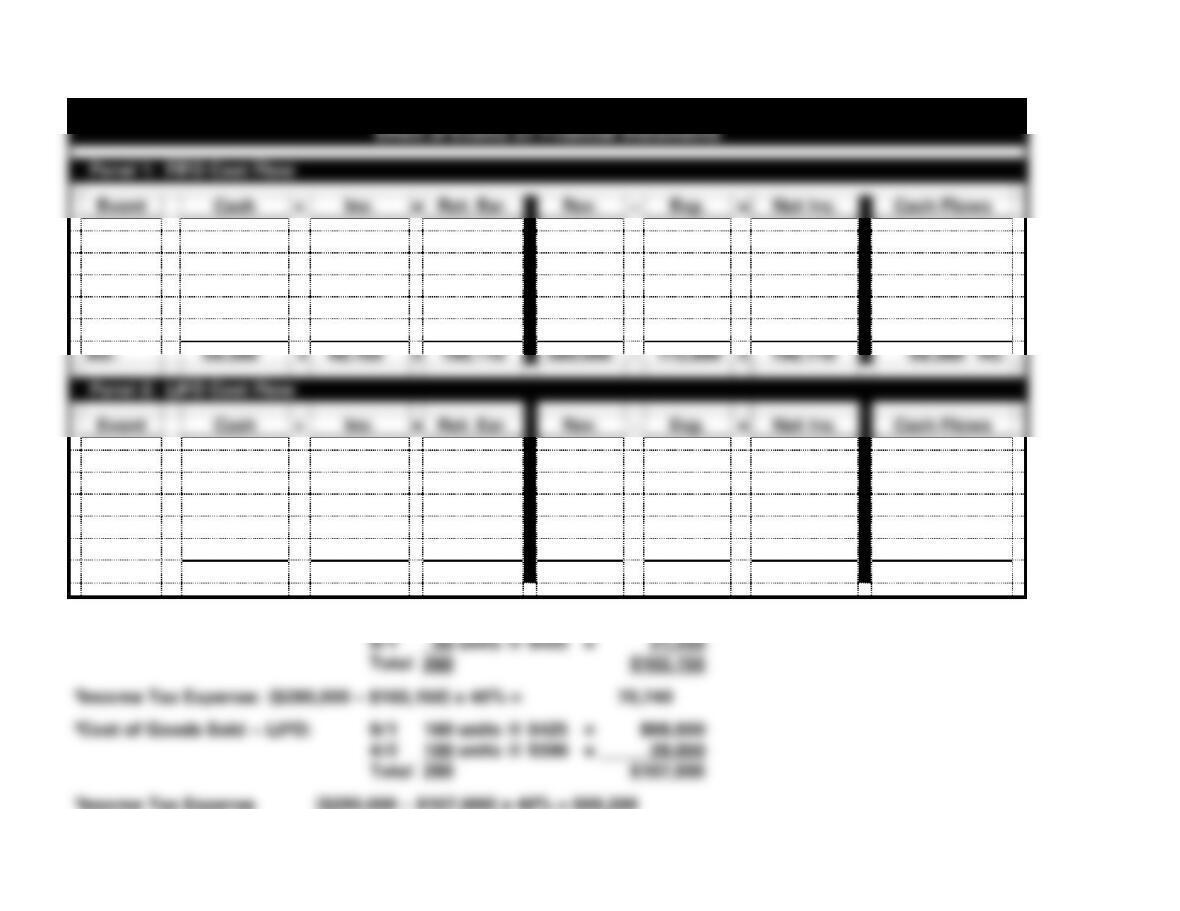

EXERCISE 5-7A a. NC = Net Change in Cash

The Brick Company

Effect of Events on Financial Statements

Panel 1: FIFO Cost Flow

Event

Cash

+

Inv.

=

Ret. Ear.

Rev.

−

Exp.

=

Net Inc.

Cash Flows

1. Sales

280,000

+

NA

=

280,000

280,000

−

NA

=

280,000

280,000 OA

2. 4/2

(81,900)

+

81,900

=

NA

NA

−

NA

=

NA

(81,900) OA

3. 9/1

(68,000)

+

68,000

=

NA

NA

−

NA

=

NA

(68,000) OA

4. CGS

NA

+

(103,150)1

=

(103,150)

NA

−

103,150

=

(103,150)

NA

5. Tax

(70,740)2

+

NA

=

(70,740)

NA

−

70,740

=

(70,740)

(70,740) OA

Bal.

59,360

+

46,750

=

106,110

280,000

−

173,890

=

106,110

59,360 NC

Panel 2: LIFO Cost Flow

Event

Cash

+

Inv.

=

Ret. Ear.

Rev.

−

Exp.

=

Net Inc.

Cash Flows

1. Sales

280,000

+

NA

=

280,000

280,000

−

NA

=

280,000

280,000 OA

2. 4/2

(81,900)

+

81,900

=

NA

NA

−

NA

=

NA

(81,900) OA

3. 9/1

(68,000)

+

68,000

=

NA

NA

−

NA

=

NA

(68,000) OA

4. CGS

NA

+

(107,000)3

=

(107,000)

NA

−

107,000

=

(107,000)

NA

5. Tax

(69,200)4

+

NA

=

(69,200)

NA

−

69,200

=

(69,200)

(69,200) OA

Bal.

60,900

+

42,900

=

103,800

280,000

−

176,200

=

103,800

60,900 NC

1Cost of Goods Sold — FIFO: 4/2 210 units @ $375 = $ 81,900

5-28

EXERCISE 5-7A (cont.)

b. Net Income assuming FIFO cost flow: $106,110 (see statements

model above).

e. FIFO

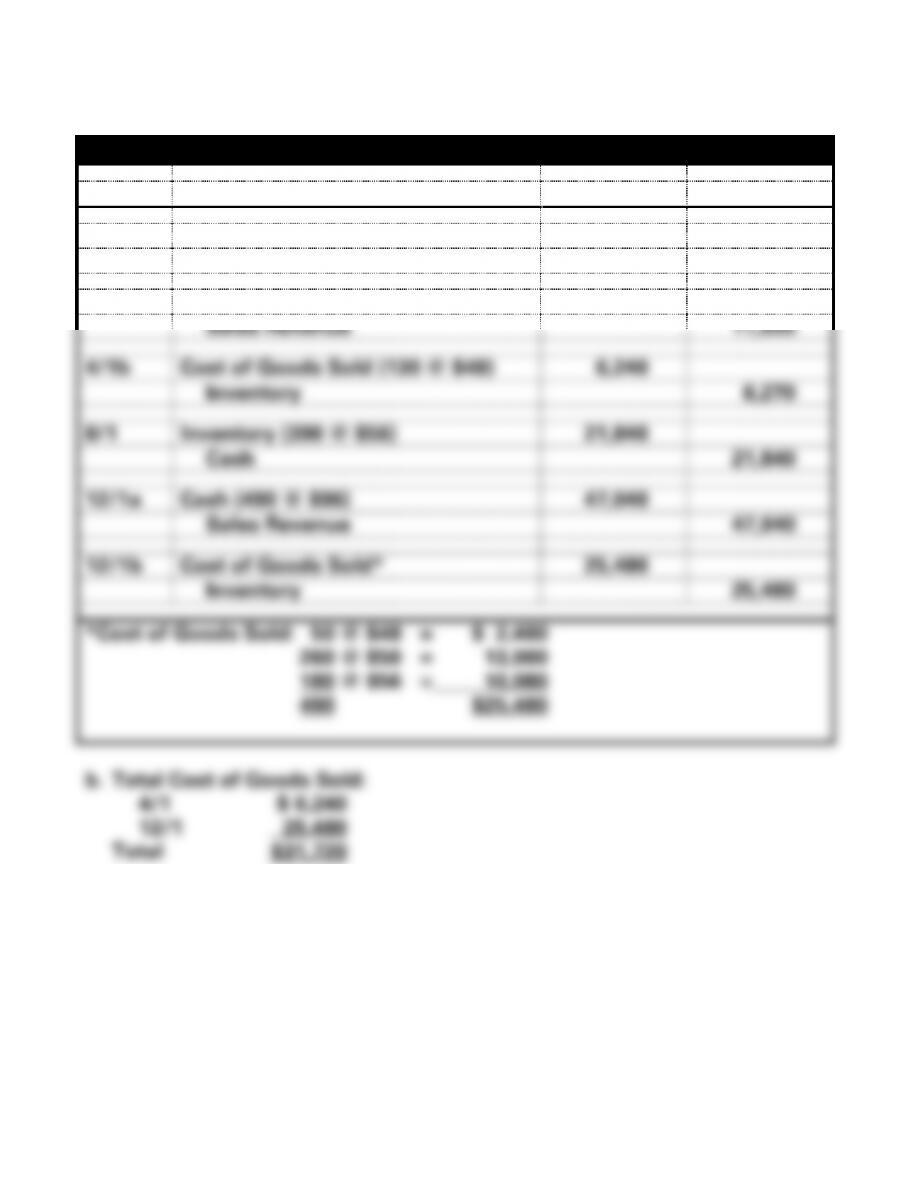

EXERCISE 5-8A

a.

Green Company – General Journal

Date

Account Titles

Debit

Credit

1/1/12

Inventory (260 @ $50)

13,000

Cash

13,000

4/1a

Cash (130 @ $85)

11,050

Sales Revenue

11,050

4/1b

Cost of Goods Sold (130 @ $48)

6,240

Inventory

6,270

8/1

Inventory (390 @ $56)

21,840

Cash

21,840

12/1a

Cash (490 @ $96)

47,040

Sales Revenue

47,040

12/1b

Cost of Goods Sold*

25,480

Inventory

25,480

*Cost of Goods Sold: 50 @ $48 = $ 2,400

260 @ $50 = 13,000

180 @ $56 = 10,080

490 $25,480

5-30

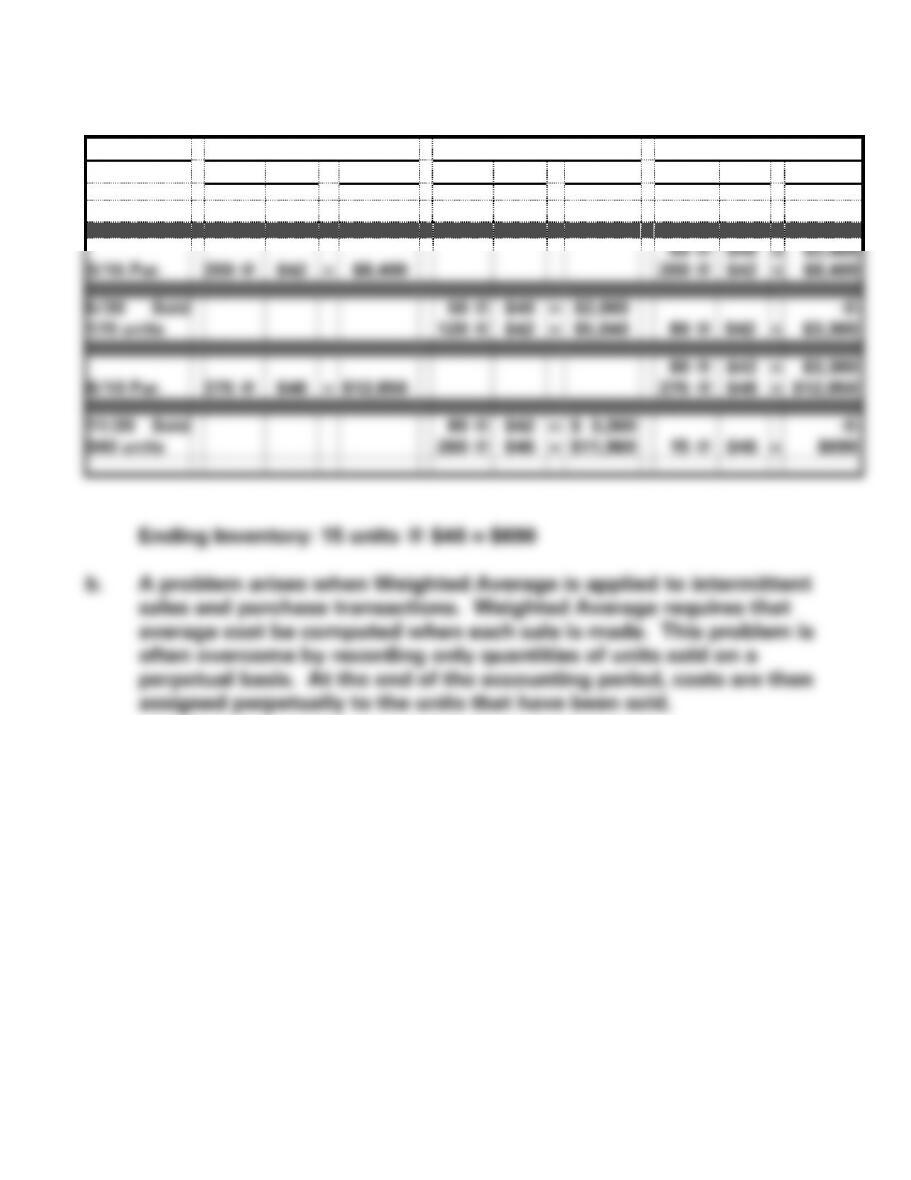

EXERCISE 5-9A

a. The Hat Store, Inc.

Date

Purchased

Sold

Inventory Balance

Units

Cost

Total

Units

Cost

Total

Units

Cost

Total

1/1 Beg. Inv.

50 @

$40

=

$2,000

3/15 Pur.

200 @

$42

=

$8,400

50 @

200 @

$40

$42

=

=

$2,000

$8,400

5/30 Sold

170 units

50 @

120 @

$40

$42

=

=

$2,000

$5,040

80 @

$42

=

-0-

$3,360

8/10 Pur.

275 @

$46

=

$12,650

80 @

275 @

$42

$46

=

=

$3,360

$12,650

11/20 Sold

340 units

80 @

260 @

$42

$46

=

=

$ 3,360

$11,960

15 @

$46

=

-0-

$690

Ending Inventory: 15 units @ $46 = $690

b. A problem arises when Weighted Average is applied to intermittent

sales and purchase transactions. Weighted Average requires that

average cost be computed when each sale is made. This problem is

often overcome by recording only quantities of units sold on a

perpetual basis. At the end of the accounting period, costs are then

assigned perpetually to the units that have been sold.

5-31

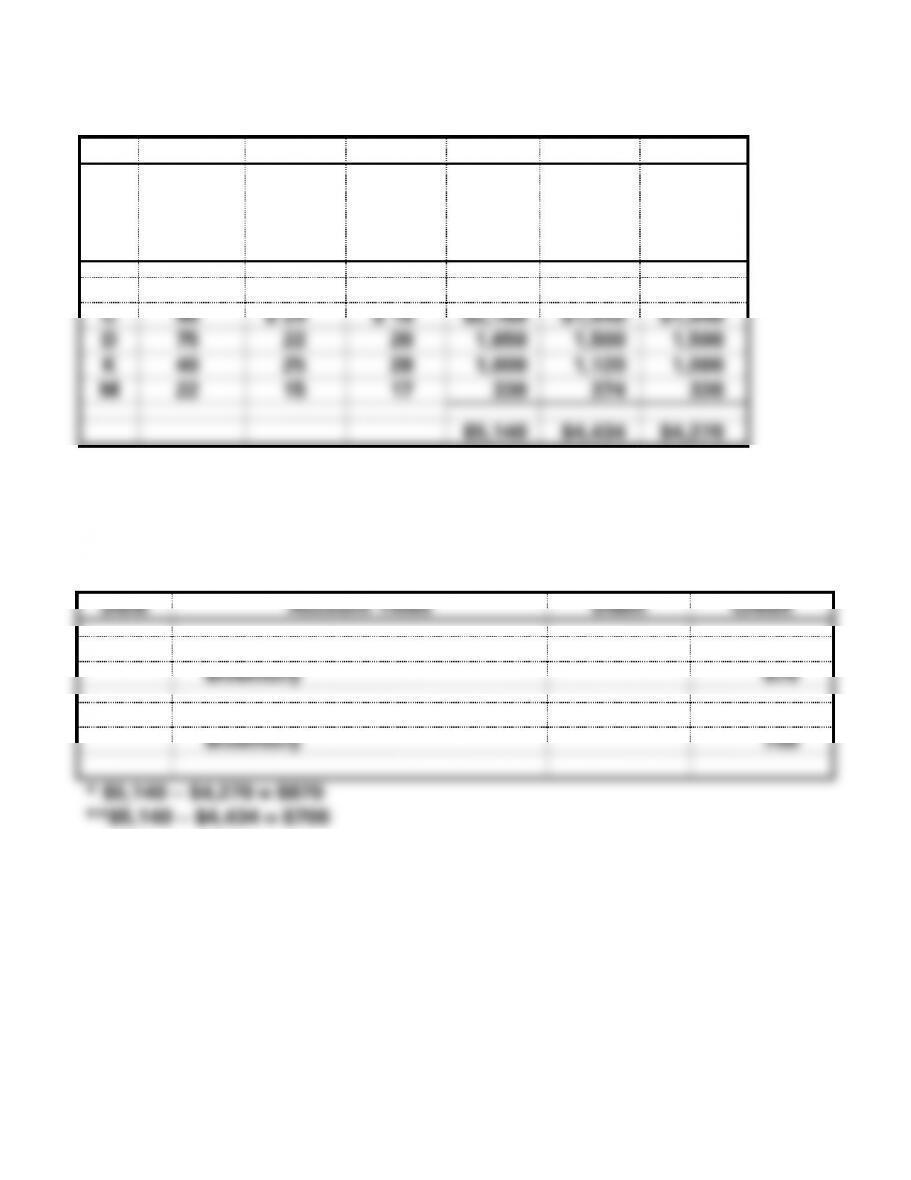

EXERCISE 5-10A

a.

Hagen Metal Works

a.

b.

c.

d.

e.

f.

g.

Item

Quantity

Cost Per

Unit

Mkt. Val.

per Unit

Total

Cost

Total

Market

Ind. Item

Lower

Cost/Mkt

.

(b x c)

(b x d)

e or f

C

90

$ 24

$ 16

$2,160

$1,440

$1,440

D

75

22

20

1,650

1,500

1,500

K

40

25

28

1,000

1,120

1,000

M

22

15

17

330

374

330

$5,140

$4,434

$4,270

1. Ending inventory using the individual item method: $4,270

2. Ending Inventory using the aggregate method: $4,434

b.

Date

Account Titles

Debit

Credit

1.

Cost of Goods Sold*

870

Inventory

870

2.

Cost of Goods Sold**

706

Inventory

706

5-32

EXERCISE 5-11A

a.

a.

b.

c.

d.

e.

f.

g.

Item

Quantity

Cost

Per

Unit

Mkt.

Value Per

Unit

Unit Lower

Cost/Mkt.

Total

Cost

Total

Lower

Cost/Mkt.

(b x c)

(b x e)

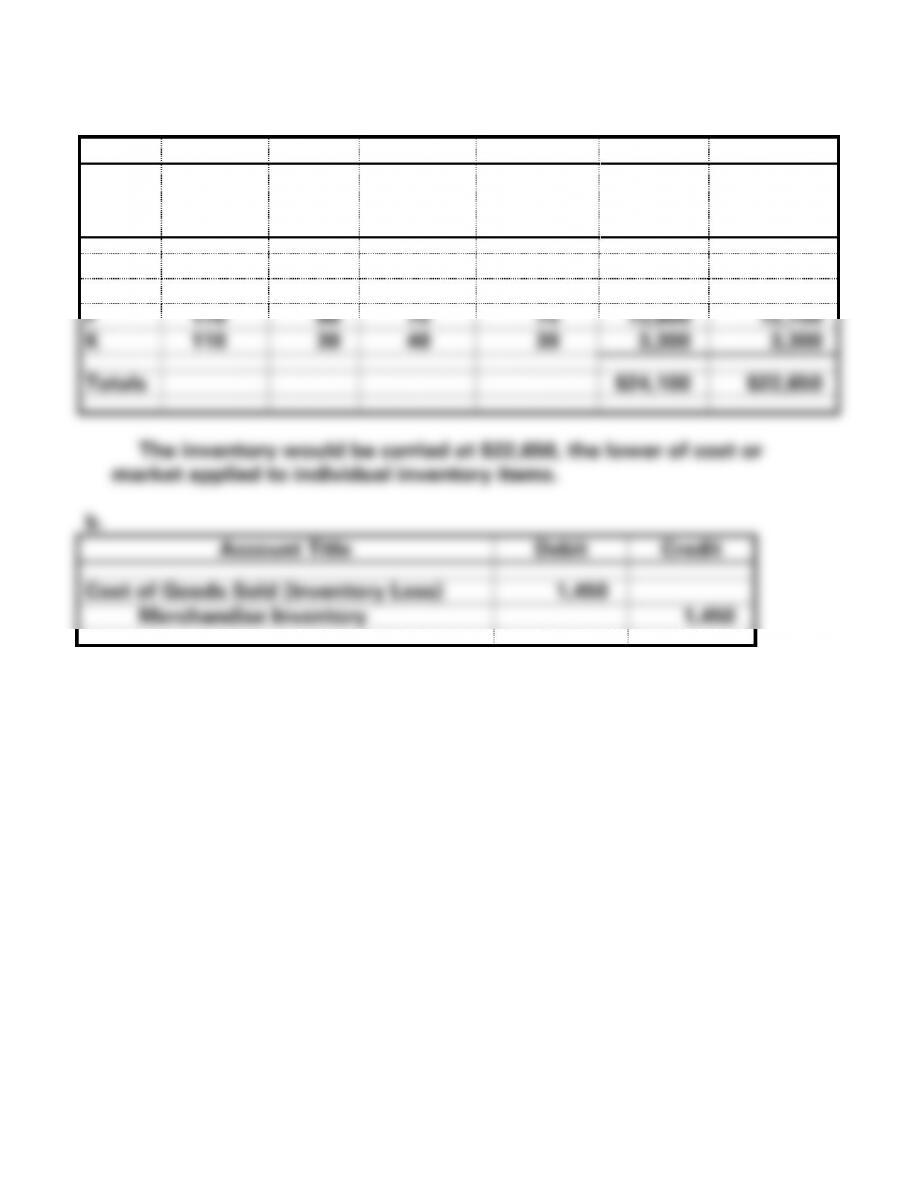

A

120

$60

$55

$55

$ 7,200

$ 6,600

F

170

80

75

75

13,600

12,750

K

110

30

40

30

3,300

3,300

Totals

$24,100

$22,650

The inventory would be carried at $22,650, the lower of cost or

market applied to individual inventory items.

b.

Account Title

Debit

Credit

Cost of Goods Sold (Inventory Loss)

1,450

Merchandise Inventory

1,450

5-33

EXERCISE 5-12A

Prentiss Sporting Goods

a. Gross Margin: Sales x Gross Margin %

$250,000 x 25% = $62,500

5-34

EXERCISE 5-13A

June 14 Inventory Account Balance

$280,000

Less: Cost of Unrecorded Sales

(42,000)

Correct Inventory Balance

238,000

Less: 5% Shrinkage

(11,900)

Less: Amount of Inventory in

Showroom

(58,000)

Inventory Damaged by Fire

$168,100

5-35

EXERCISE 5-14A

Stubbs Company

The uncounted inventory will only affect The Stubbs Company’s balance

5-36

EXERCISE 5-15A

Carver Co.

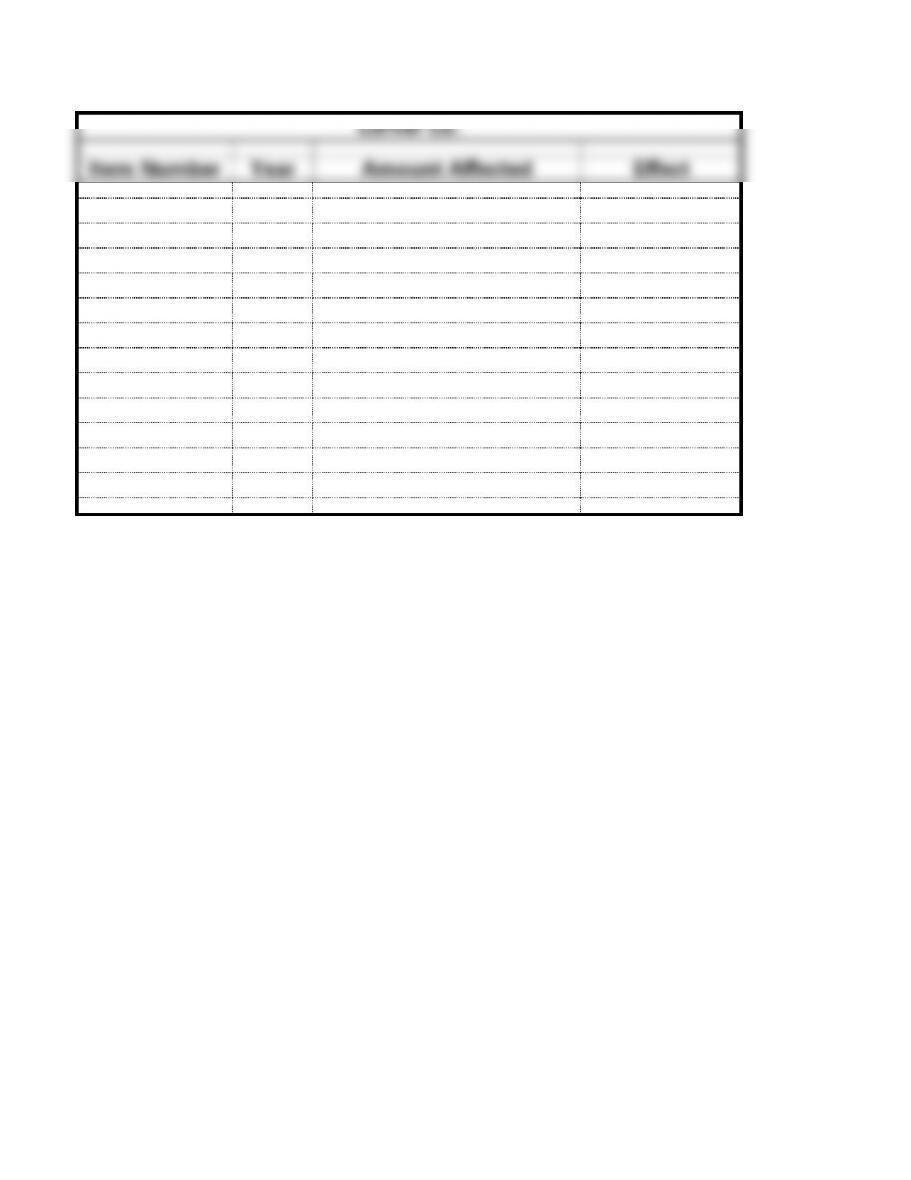

Item Number

Year

Amount Affected

Effect

1.

2016

Beginning Inventory

NA

2.

2016

Purchases

NA

3.

2016

Goods Available for Sale

NA

4.

2016

Cost of Goods Sold

Overstated

5.

2016

Gross Margin

Understated

6.

2016

Net Income

Understated

7.

2017

Beginning Inventory

Understated

8.

2017

Purchases

NA

9.

2017

Goods Available for Sale

Understated

10.

2017

Cost of Goods Sold

Understated

11.

2017

Gross Margin

Overstated

12.

2017

Net Income

Overstated

5-37

EXERCISE 5-16A

Most of Alcoa’s operations outside the United States are probably in

LIFO.

5-38

EXERCISE 5-17A

GAAP VS IFRS

a. GAAP allows the use of LIFO for reporting inventory and cost of

goods sold. This assumes that the newest goods purchased are the

SOLUTIONS TO PROBLEMS – SERIES A – CHAPTER 8

PROBLEM 5-18A

Wall’s China Shop

Inventory Purchases

Beginning Inventory

220

@

$150

=

$33,000

First Purchase

150

@

155

=

23,250

Second Purchase

160

@

160

=

25,600

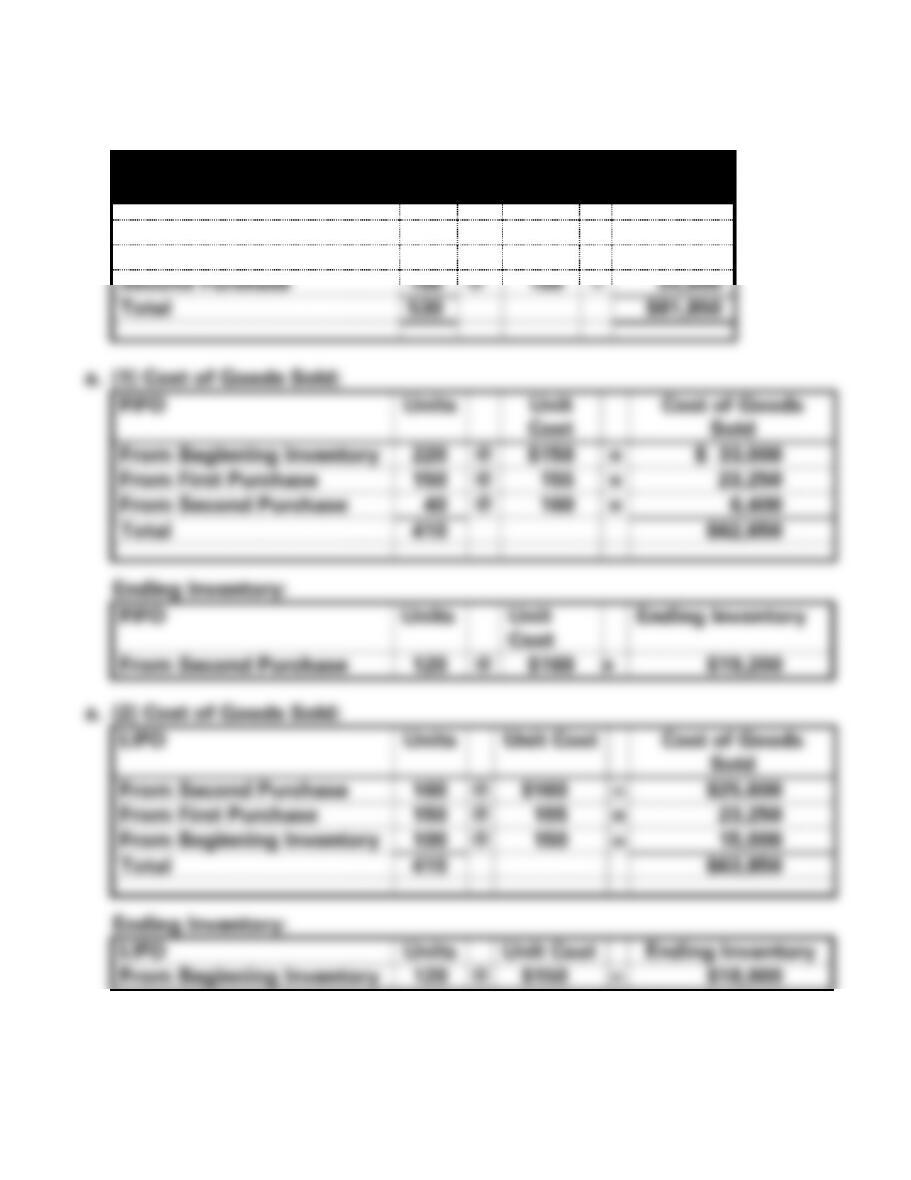

Total

530

$81,850

a. (1) Cost of Goods Sold:

FIFO

Units

Unit

Cost

Cost of Goods

Sold

From Beginning Inventory

220

@

$150

=

$ 33,000

From First Purchase

150

@

155

=

23,250

From Second Purchase

40

@

160

=

6,400

Total

410

$62,650

From Second Purchase

@

LIFO

Units

Unit Cost

Cost of Goods

Sold

From Second Purchase

160

From First Purchase

155

23,250

From Beginning Inventory

100

Total

410

$63,850

LIFO

Unit Cost

From Beginning Inventory

5-40

PROBLEM 5-18A a. (cont.)

a. (3)

Weighted Average

Total Cost

Total Units

=

Cost per Unit

$81,850

530

=

$154.433

Cost of Goods Sold:

410 units

@

$154.433

=

$63,318*

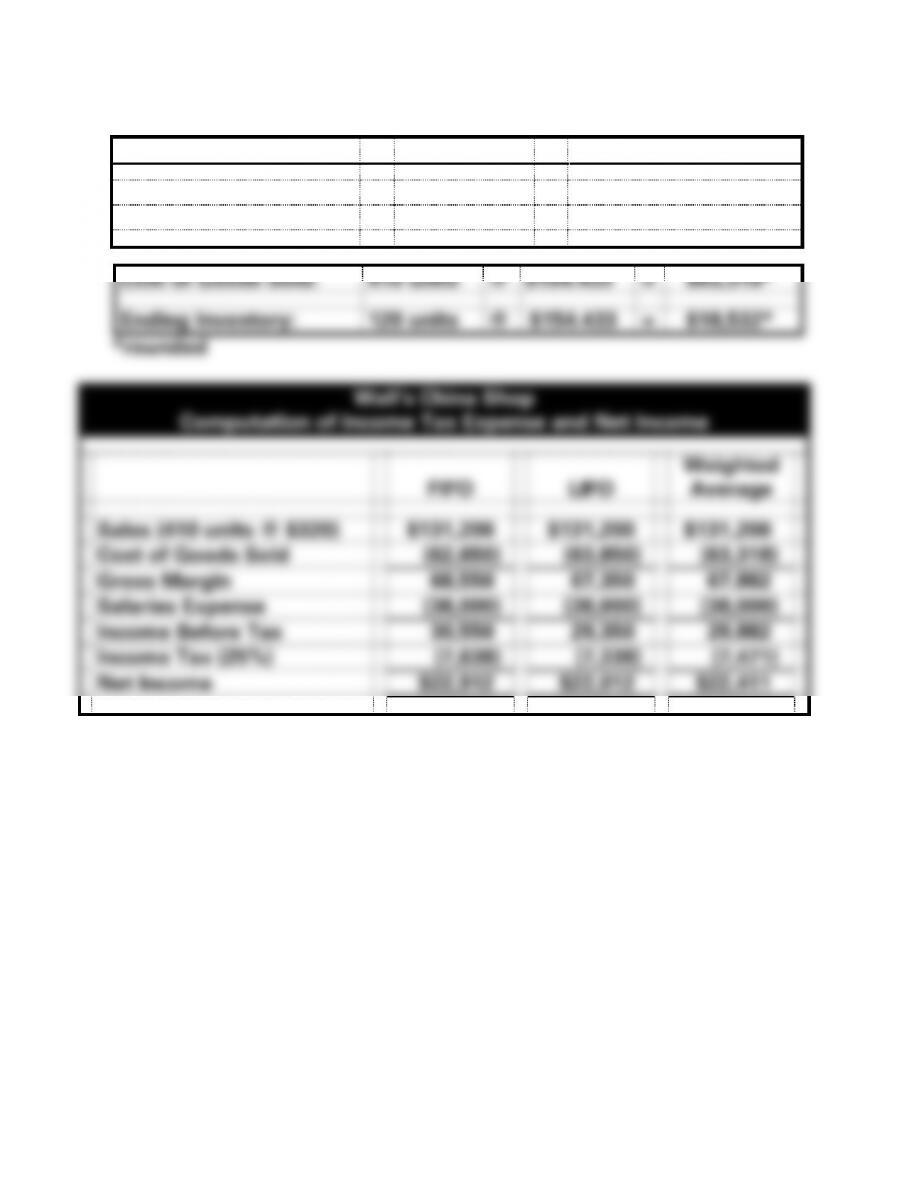

Ending Inventory:

120 units

@

$154.433

=

$18,532*

*rounded

Wall’s China Shop

Computation of Income Tax Expense and Net Income

FIFO

LIFO

Weighted

Average

Sales (410 units @ $320)

$131,200

$131,200

$131,200

Cost of Goods Sold

(62,650)

(63,850)

(63,318)

Gross Margin

68,550

67,350

67,882

Salaries Expense

(38,000)

(38,000)

(38,000)

Income Before Tax

30,550

29,350

29,882

Income Tax (25%)

(7,638)

(7,338)

(7,471)

Net Income

$22,912

$22,012

$22,411

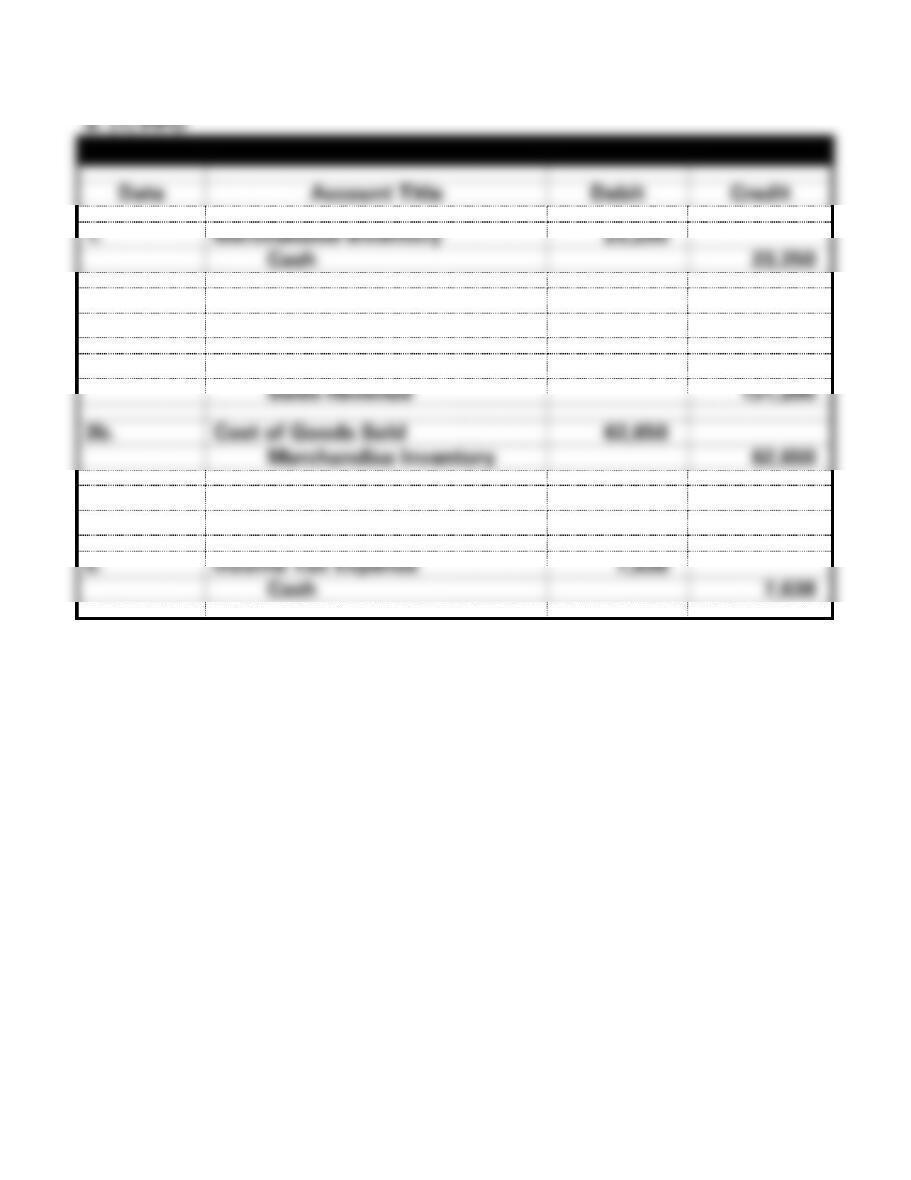

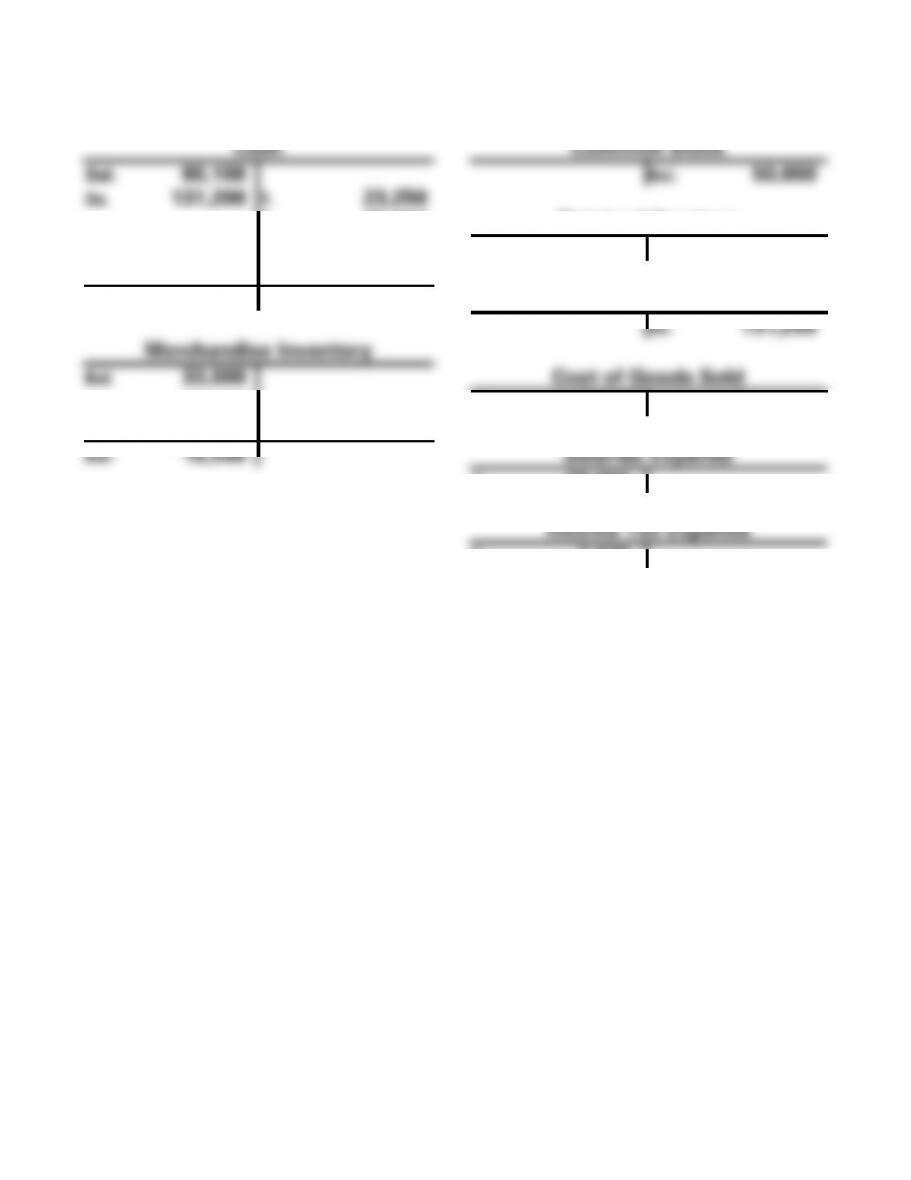

PROBLEM 5-18A (cont.)

5-42

PROBLEM 5-18A (cont.)

b. (1) FIFO

Cash

Common Stock

Bal. 80,100

Bal. 50,000

3a. 131,200

1. 23,250

2. 25,600

Retained Earnings

4. 38,000

Bal. 63,100

5. 7,638

Bal. 116,812

Sales Revenue

3a. 131,200

Merchandise Inventory

Bal. 33,000

Cost of Goods Sold

1. 23,250

3b. 62,650

2. 25,600

3b. 62,650

Bal. 19,200

Salaries Expense

4. 38,000

Income Tax Expense

5. 7,638

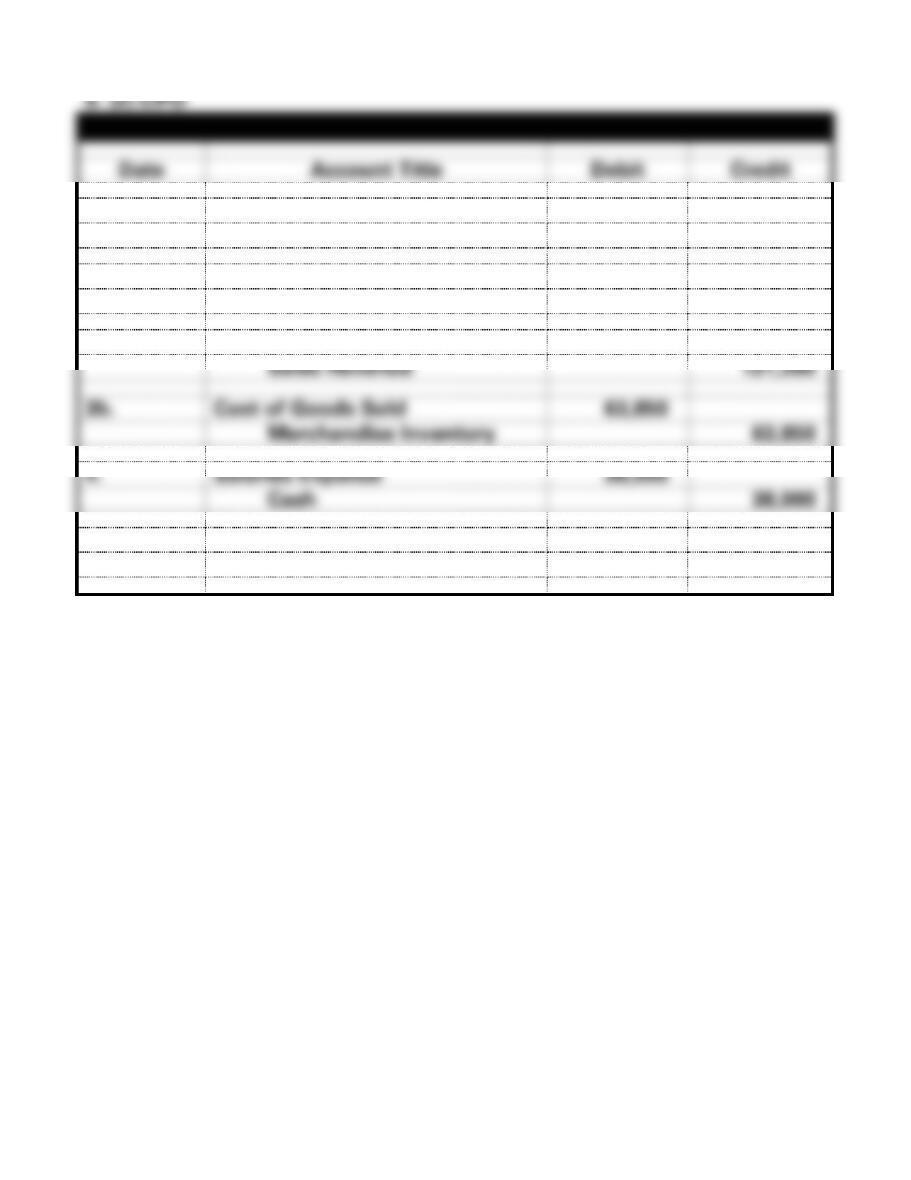

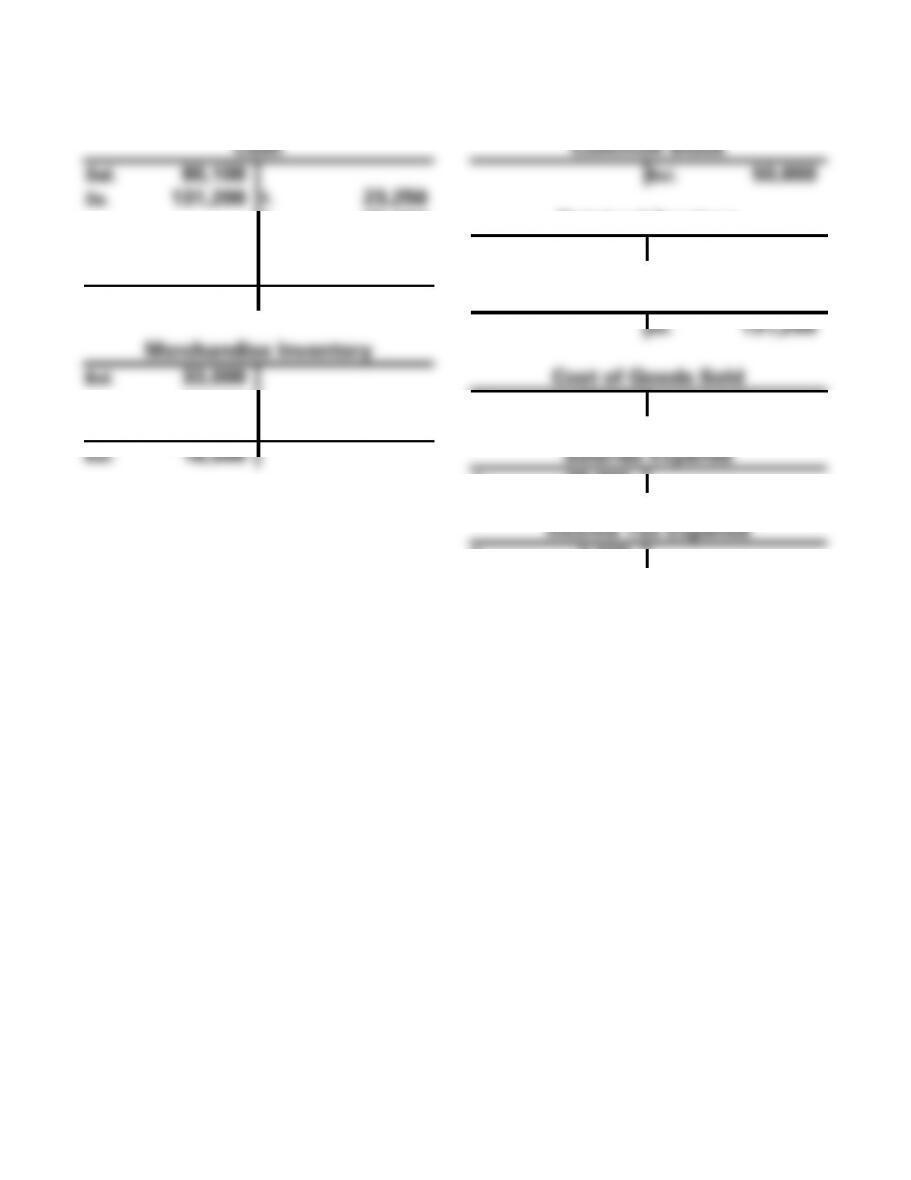

PROBLEM 5-18A (cont.)

5-44

PROBLEM 5-18A (cont.)

b. (2) LIFO

Cash

Common Stock

Bal. 80,100

Bal. 50,000

3a. 131,200

1. 23,250

2. 25,600

Retained Earnings

4. 38,000

Bal. 63,100

5. 7,338

Bal. 117,112

Sales Revenue

3a. 131,200

Merchandise Inventory

Bal. 33,000

Cost of Goods Sold

1. 23,250

3b. 63,850

2. 25,600

3b. 63,850

Bal. 18,000

Salaries Expense

4. 38,000

Income Tax Expense

5. 7,338

PROBLEM 5-18A (cont.)