4-21

EXERCISE 4-1Aa. (cont.)

Sports Clothing

Statement of Cash Flows

For the Year Ended December 31, 2016

Cash Flows From Operating Activities:

Cash Inflow from Customers

50,000

Cash Outflow for Inventory

(50,000)

Cash Outflow for Expenses

(8,000)

Net Cash Flow from Operating Activities

($8,000)

Cash Flows From Investing Activities

-0-

Cash Flows From Financing Activities:

Cash Inflow from Loan

$90,000

Net Cash Flow from Financing Activities

90,000

Net Increase in Cash

82,000

Plus: Beginning Cash Balance

-0-

Ending Cash Balance

$82,000

EXERCISE 4-2A

a.

Dan Watson Merchandising

General Journal, 2016

Date

Account Titles

Debit

Credit

1.

Cash

30,000

Common Stock

30,000

2.

Merchandise Inventory

18,000

Cash

18,000

3a.

Cash

32,000

Sales Revenue

32,000

3b.

Cost of Goods Sold

15,000

Merchandise Inventory

15,000

4-23

EXERCISE 4-2A (cont.)

c.

Don Watson Merchandising

Income Statement

For the Year Ended December 31, 2016

Net Sales

$32,000

Cost of Goods Sold

(15,000)

Gross Margin

17,000

Operating Expenses

-0-

Net Income

$17,000

Cash Flows From Operating Activities:

Cash Inflow from Customers

$32,000

Cash Outflow for Inventory

(18,000)

Net Cash Flow from Operating Act.

$14,000

4-24

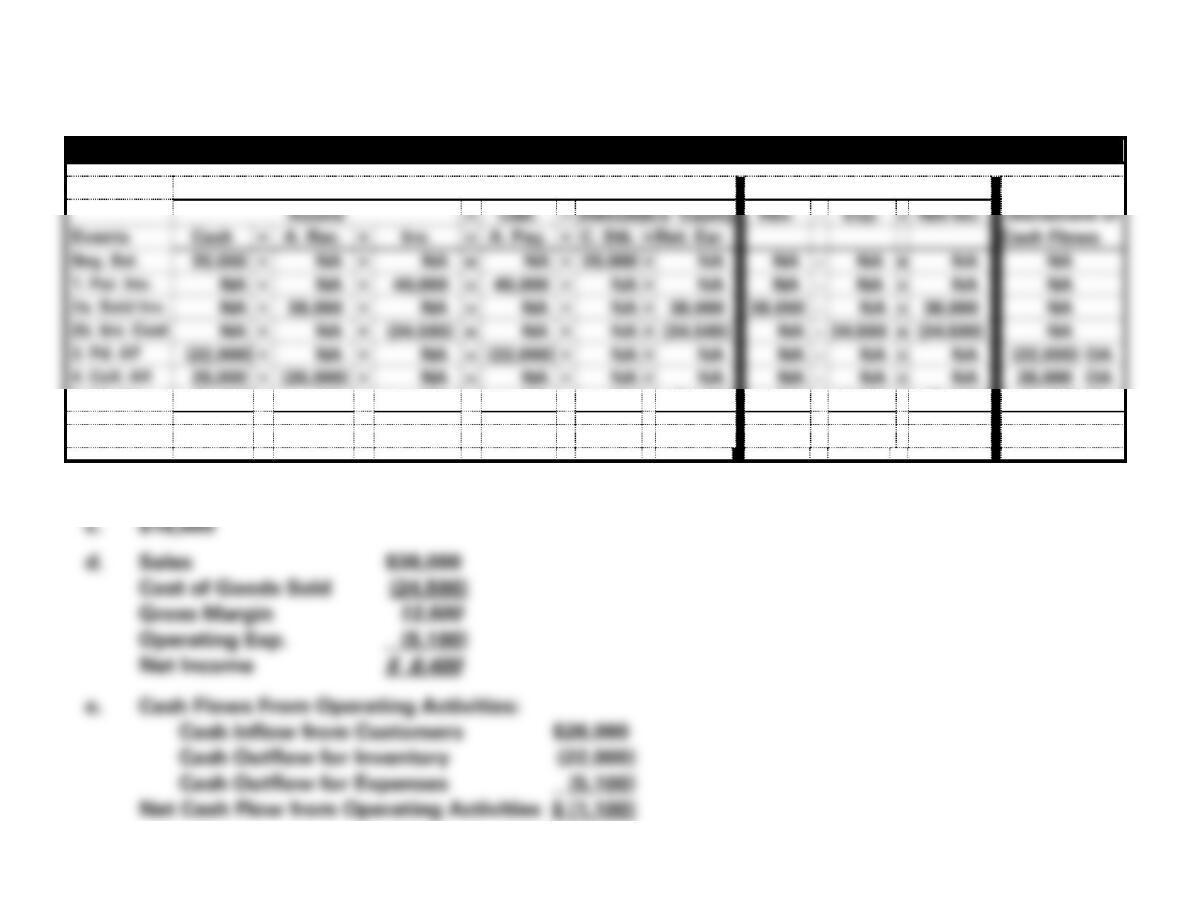

EXERCISE 4-3A

a. NC = Net Change in Cash

Hardy Merchandising Company Effect of Events on the Financial Statements

Balance Sheet

Income Statement

Assets

=

Liab.

+

Stkholders’ Equity

Rev.

−

Exp.

=

Net Inc.

Statement of

Events

Cash

+

A. Rec.

+

Inv.

=

A. Pay.

+

C. Stk.

+

Ret. Ear.

Cash Flows

Beg. Bal.

20,000

+

NA

+

NA

=

NA

+

20,000

+

NA

NA

−

NA

=

NA

NA

1. Pur. Inv.

NA

+

NA

+

40,000

=

40,000

+

NA

+

NA

NA

−

NA

=

NA

NA

2a. Sold Inv.

NA

+

38,000

+

NA

=

NA

+

NA

+

38,000

38,000

−

NA

=

38,000

NA

2b. Inv. Cost

NA

+

NA

+

(24,500)

=

NA

+

NA

+

(24,500)

NA

−

24,500

=

(24,500)

NA

3. Pd. AP

(22,000)

+

NA

+

NA

=

(22,000)

+

NA

+

NA

NA

−

NA

=

NA

(22,000) OA

4. Coll. AR

26,000

+

(26,000)

+

NA

=

NA

+

NA

+

NA

NA

−

NA

=

NA

26,000 OA

5. Pd. Exp.

(5,100)

+

NA

+

NA

=

NA

+

NA

+

(5,100)

NA

−

5,100

=

(5,100)

(5,100) OA

End. Bal.

18,900

+

12,000

+

15,500

=

18,000

+

20,000

+

8,400

38,000

−

29,600

=

8,400

(1,100) NC

b. $12,000

4-25

EXERCISE 4-3A (cont.)

f. Ending retained earnings and net income are the same in this problem

4-26

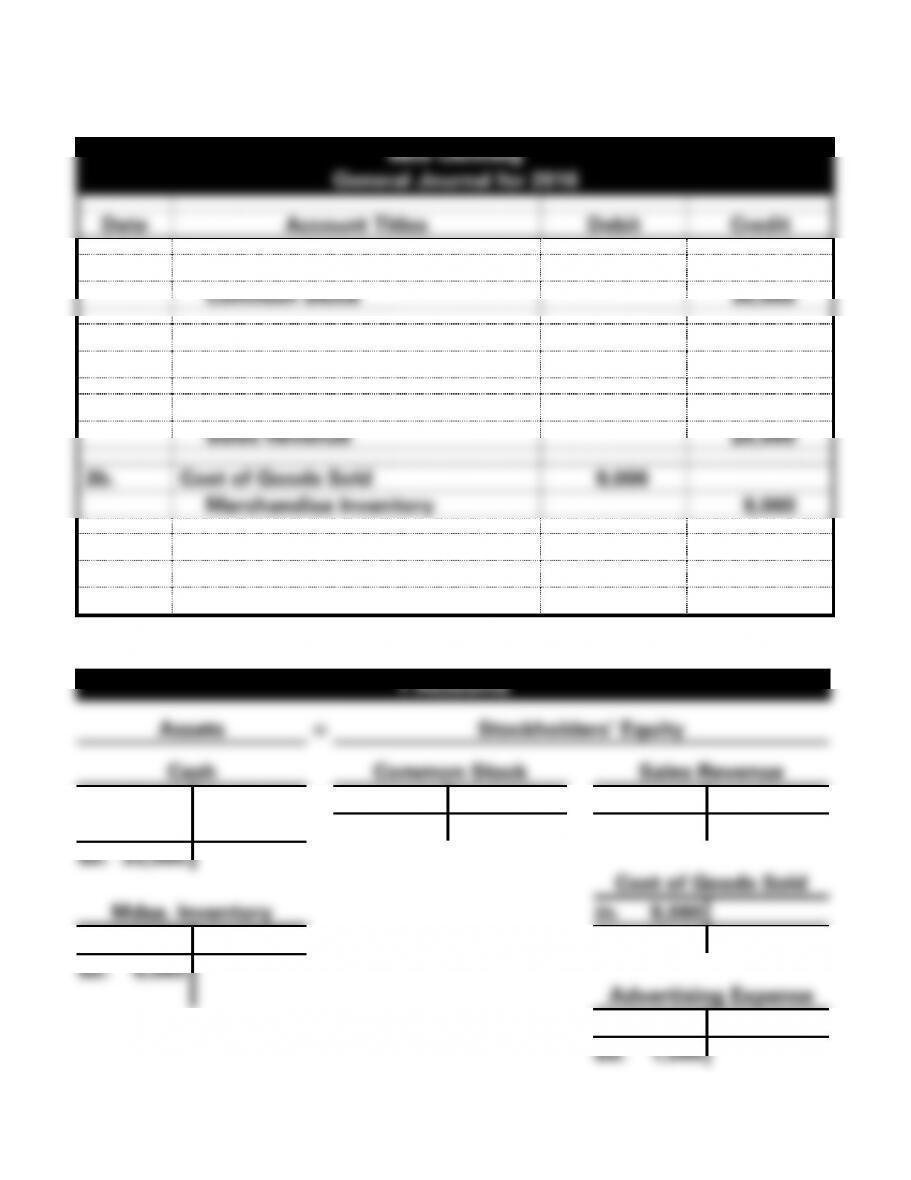

EXERCISE 4-4A

a.

Milo Clothing

General Journal for 2016

Date

Account Titles

Debit

Credit

1.

Cash

30,000

Common Stock

30,000

2.

Merchandise Inventory

15,000

Cash

15,000

3a.

Cash

20,000

Sales Revenue

20,000

3b.

Cost of Goods Sold

9,000

Merchandise Inventory

9,000

4.

Advertising Expense

1,500

Cash

1,500

b.

T-Accounts

Assets

=

Stockholders’ Equity

Cash

Common Stock

Sales Revenue

1. 30,000

2. 15,000

1. 30,000

3a. 20,000

3a. 20,000

4. 1,500

Bal. 30,000

Bal. 20,000

Bal. 33,500

Cost of Goods Sold

Mdse. Inventory

3b. 9,000

2. 15,000

3b. 9,000

Bal. 9,000

Bal. 6,000

Advertising Expense

4. 1,500

Bal. 1,500

4-27

EXERCISE 4-4A (cont.)

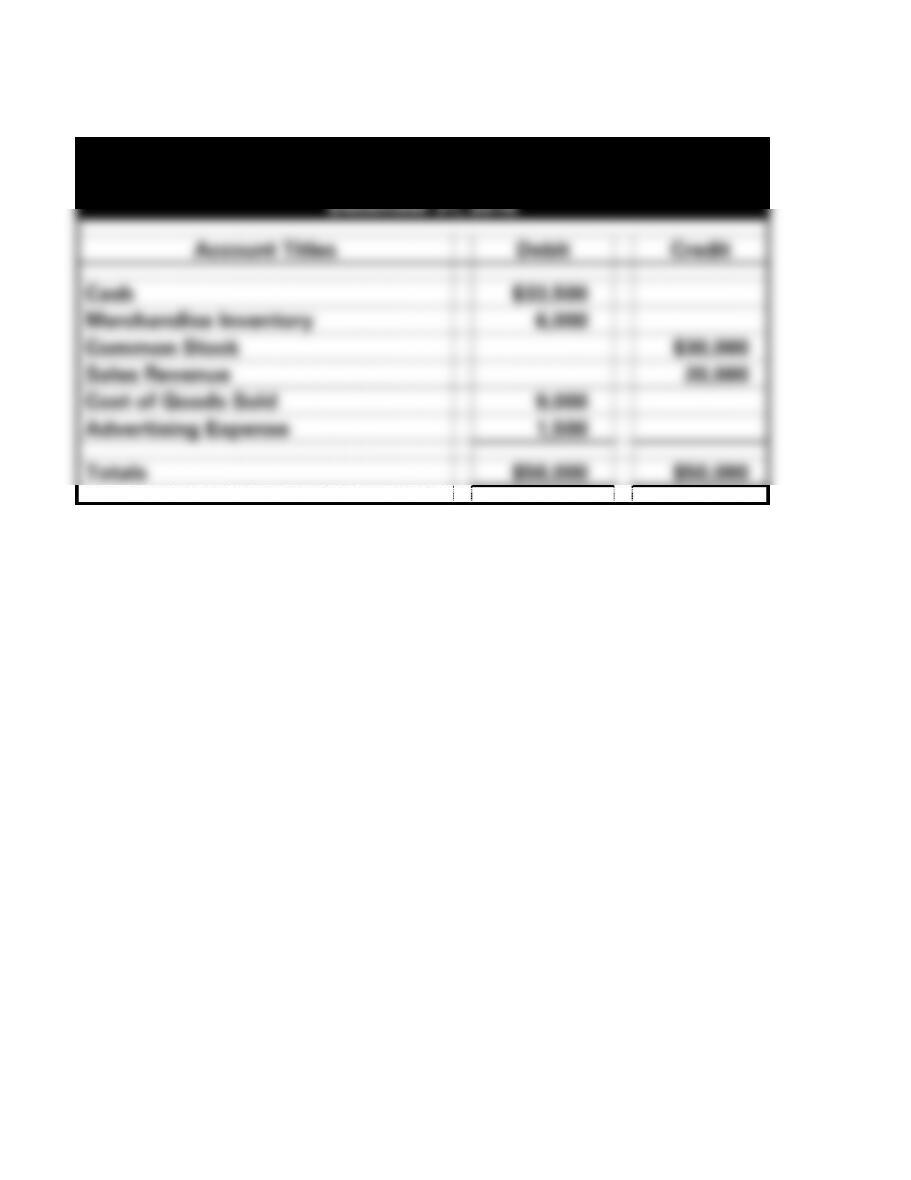

c.

Milo Clothing

Trial Balance

December 31, 2016

Account Titles

Debit

Credit

Cash

$33,500

Merchandise Inventory

6,000

Common Stock

$30,000

Sales Revenue

20,000

Cost of Goods Sold

9,000

Advertising Expense

1,500

Totals

$50,000

$50,000

4-28

EXERCISE 4-5A

a. FOB shipping point

4-29

EXERCISE 4-6A

a. & b.

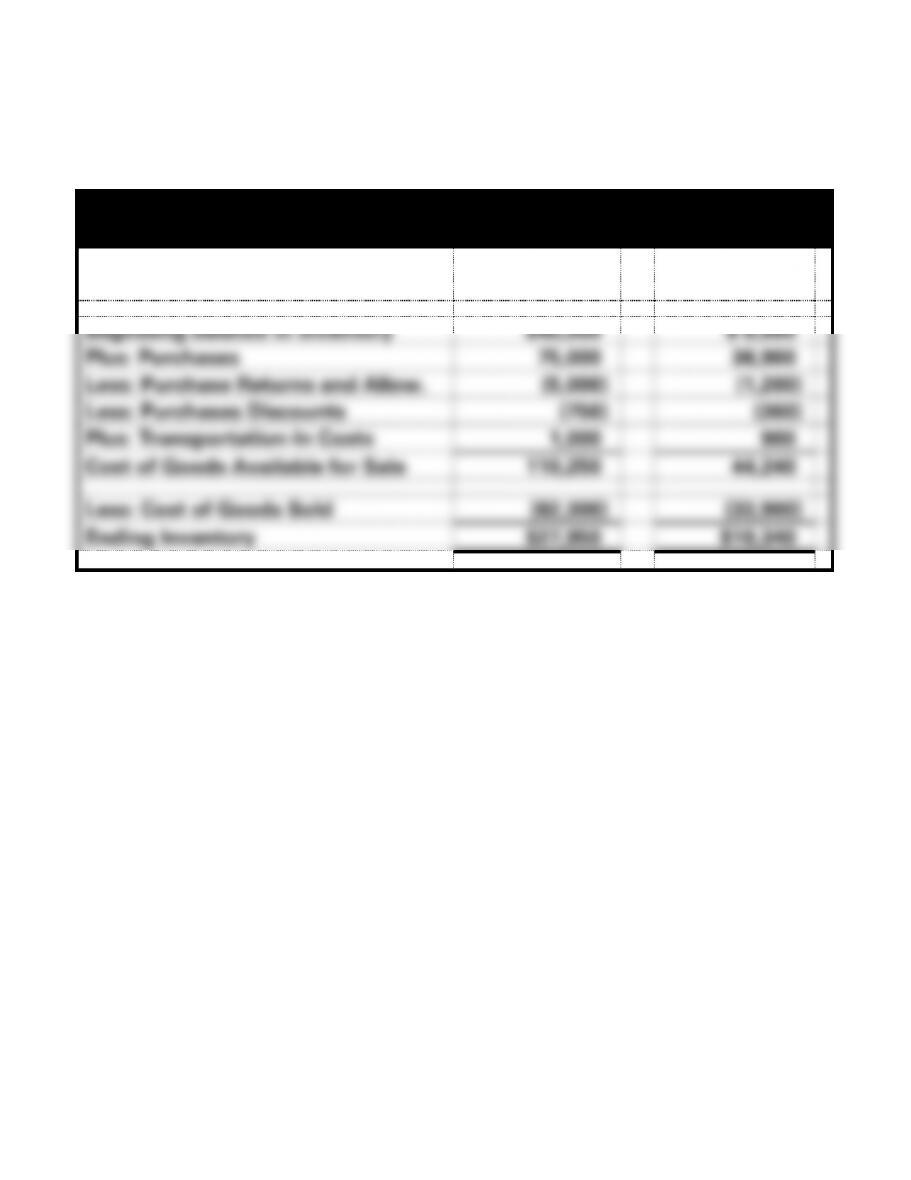

Computation of Ending Inventory

Jill’s Dress

Shop

Ken’s Bait

Shop

Beginning balance in inventory

$40,000

$ 8,000

Plus: Purchases

75,000

36,900

Less: Purchase Returns and Allow.

(5,000)

(1,200)

Less: Purchases Discounts

(750)

(360)

Plus: Transportation-In Costs

1,000

900

Cost of Goods Available for Sale

110,250

44,240

Less: Cost of Goods Sold

(82,300)

(33,900)

Ending Inventory

$27,950

$10,340

4-30

EXERCISE 4-7A

a.

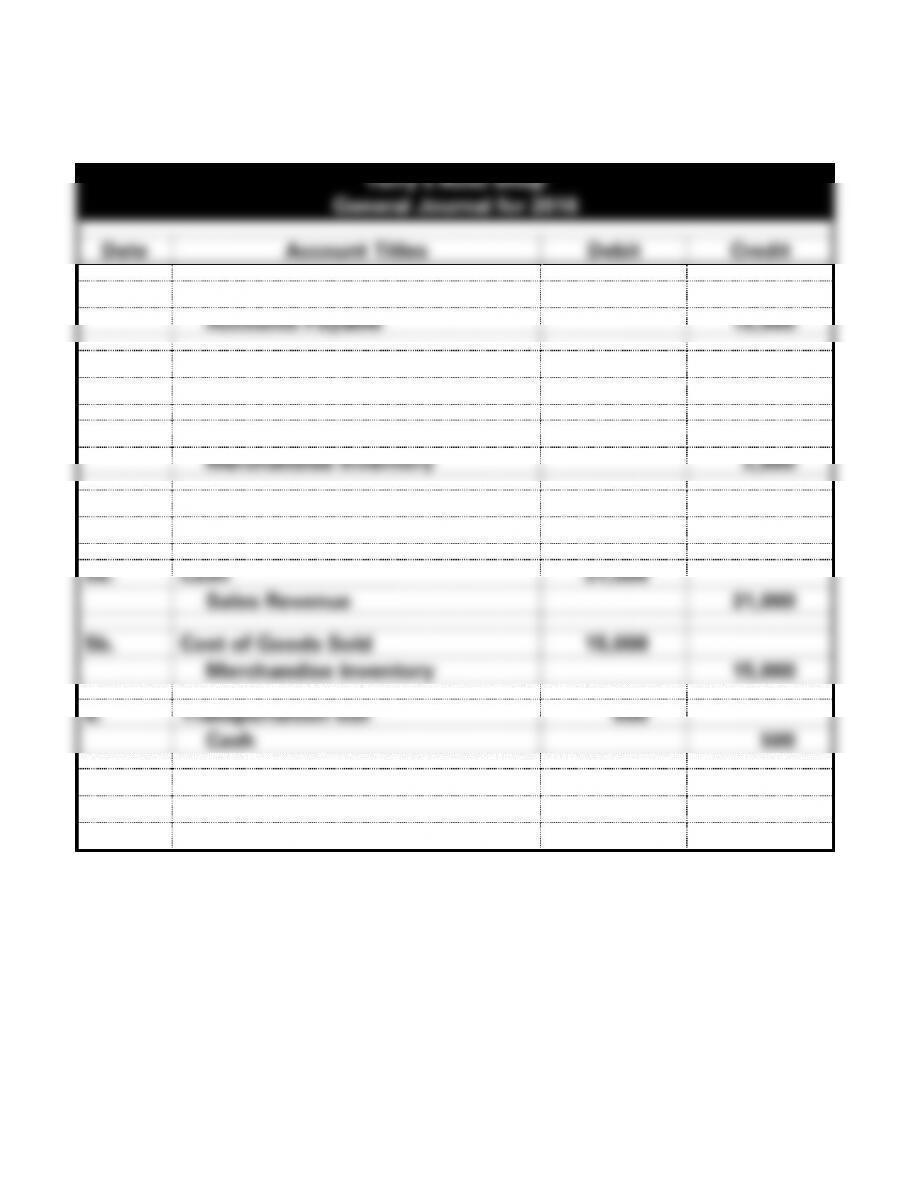

Terry’s Auto Shop

General Journal for 2016

Date

Account Titles

Debit

Credit

1.

Merchandise Inventory

15,000

Accounts Payable

15,000

2.

Merchandise Inventory

800

Cash

800

3.

Accounts Payable

2,600

Merchandise Inventory

2,600

4.

Accounts Payable

1,100

Merchandise Inventory

1,100

5a.

Cash

31,000

Sales Revenue

31,000

5b.

Cost of Goods Sold

15,000

Merchandise Inventory

15,000

6.

Transportation-out

500

Cash

500

7.

Accounts Payable

8,000

Cash

8,000

4-31

EXERCISE 4-7A (cont.)

b.

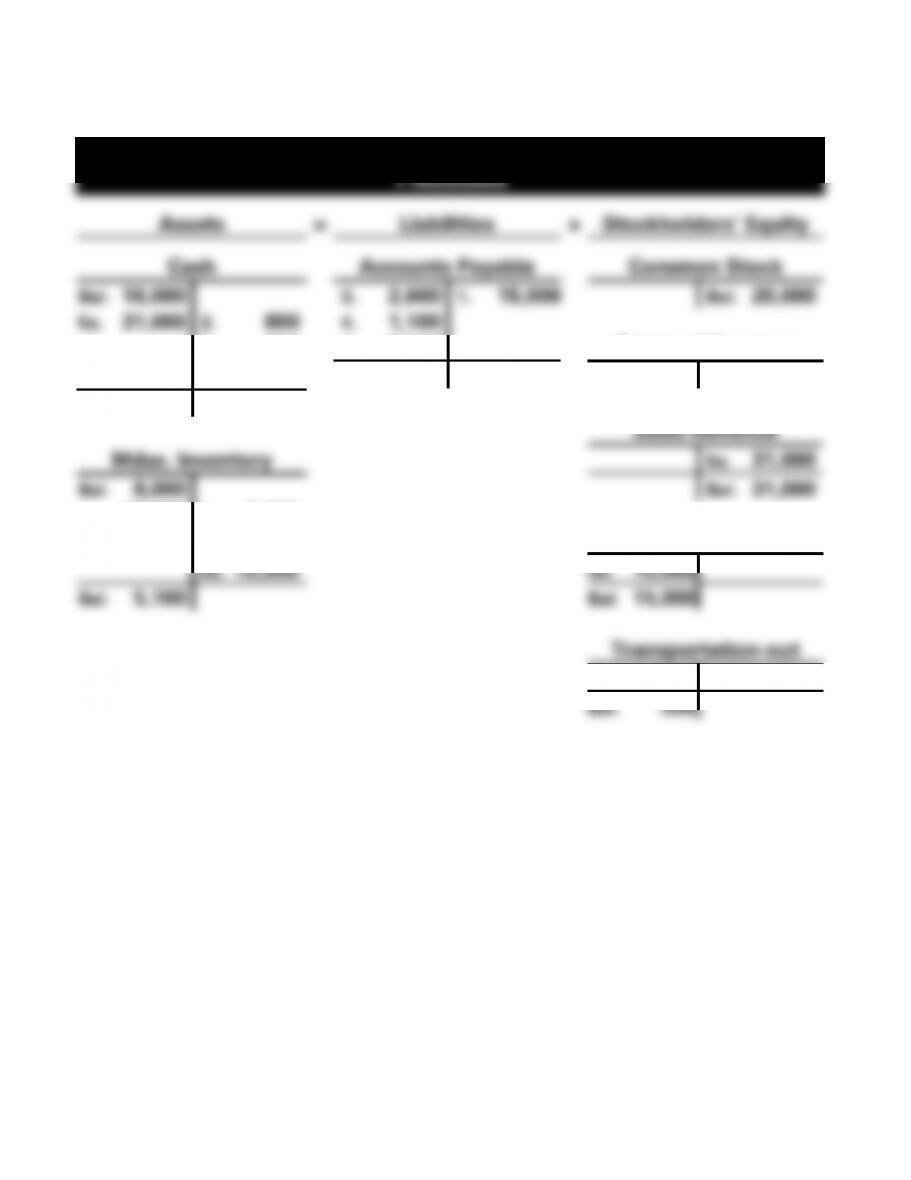

Terry’s Auto Shop

T-Accounts

Assets

=

Liabilities

+

Stockholders’ Equity

Cash

Accounts Payable

Common Stock

Bal. 16,000

3. 2,600

1. 15,000

Bal. 20,000

5a. 31,000

2. 800

4. 1,100

6. 500

7. 8,000

Retained Earnings

7. 8,000

Bal. 3,300

Bal. 4,000

Bal. 37,700

Sales Revenue

Mdse. Inventory

5a. 31,000

Bal. 8,000

Bal. 31,000

1. 15,000

3. 2,600

2. 800

4. 1,100

Cost of Goods Sold

5b. 15,000

5b. 15,000

Bal. 5,100

Bal. 15,000

Transportation-out

6. 500

Bal. 500

4-32

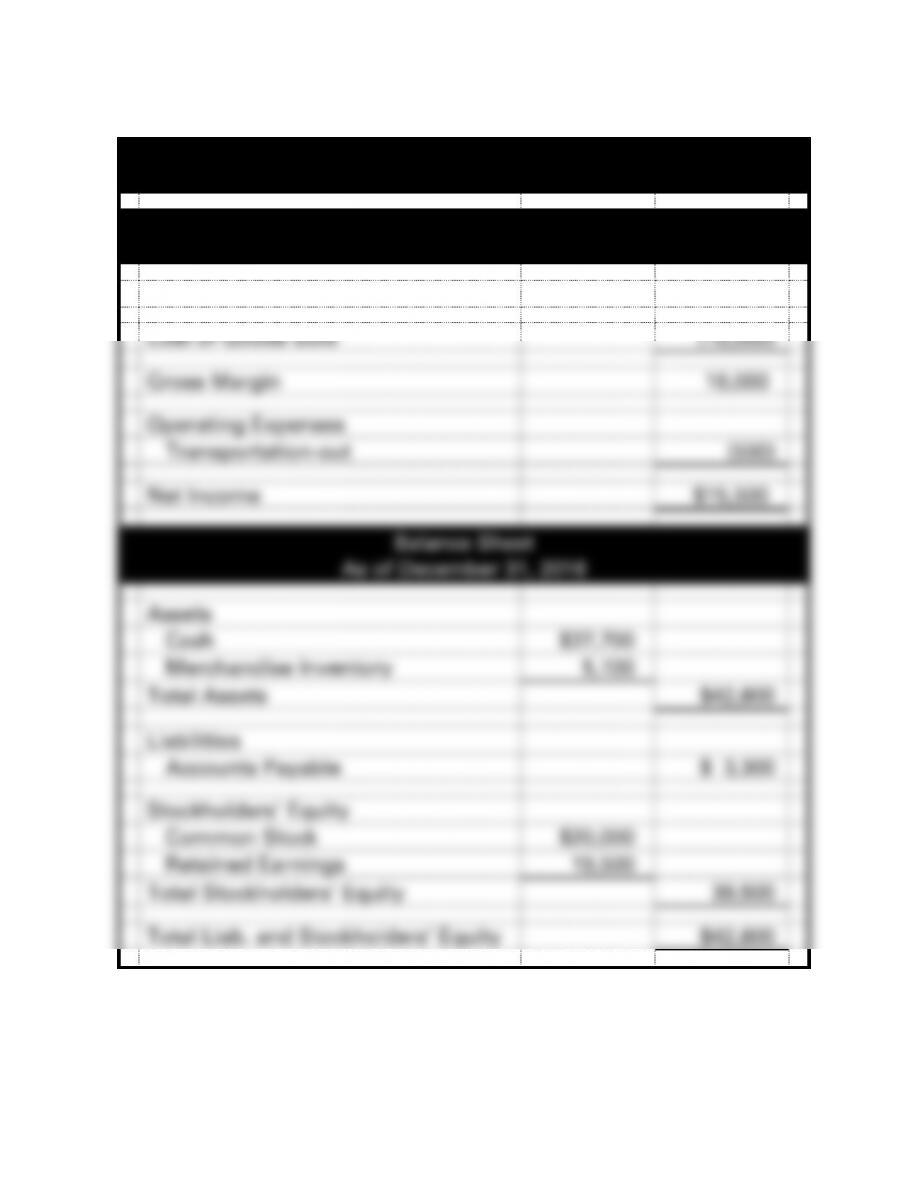

EXERCISE 4-7A (cont.)

c.

Terry’s Auto Shop

Financial Statements

Income Statement

For the Year Ended December 31, 2016

Net Sales

$31,000

Cost of Goods Sold

(15,000)

Gross Margin

16,000

Operating Expenses

Transportation-out

(500)

Net Income

$15,500

Balance Sheet

As of December 31, 2016

Assets

Cash

$37,700

Merchandise Inventory

5,100

Total Assets

$42,800

Liabilities

Accounts Payable

$ 3,300

Stockholders’ Equity

Common Stock

$20,000

Retained Earnings

19,500

Total Stockholders’ Equity

39,500

Total Liab. and Stockholders’ Equity

$42,800

4-33

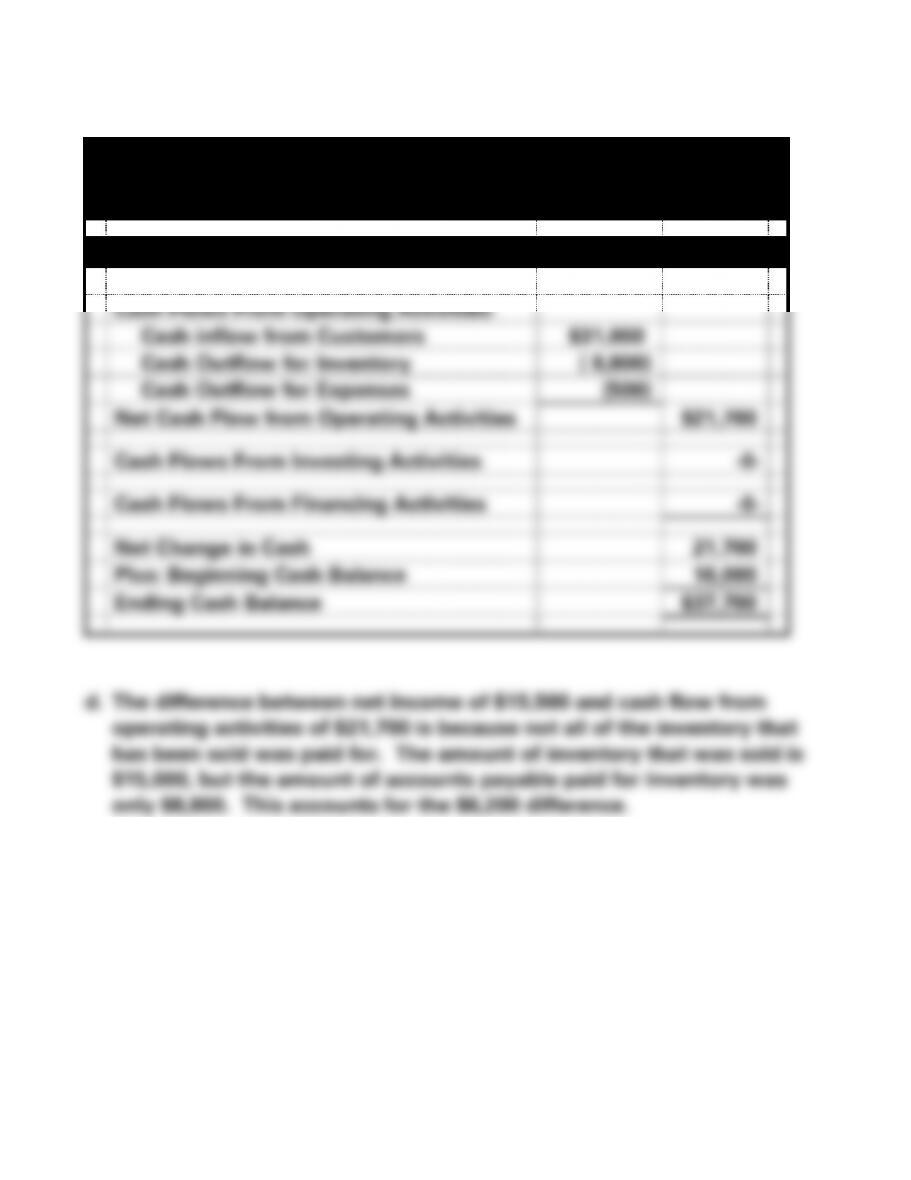

EXERCISE 4-7A c. (cont.)

Terry’s Auto Shop

Financial Statements

For the Year Ended December 31, 2016

Statement of Cash Flows

Cash Flows From Operating Activities:

Cash inflow from Customers

$31,000

Cash Outflow for Inventory

( 8,800)

Cash Outflow for Expenses

(500)

Net Cash Flow from Operating Activities

$21,700

Cash Flows From Investing Activities

-0-

Cash Flows From Financing Activities

-0-

Net Change in Cash

21,700

Plus: Beginning Cash Balance

16,000

Ending Cash Balance

$37,700

4-34

EXERCISE 4-8A

Transaction

Debited to Inventory

a. Transportation-out

No

b. Purchase discount

No

c. Transportation-in

Yes

d. Purchase computer

No

e. Purchase of inventory

Yes

f. Allowance for damaged inventory

No

4-35

EXERCISE 4-9A

a.

Transaction

Period Costs

Product Costs

Not

Applicable

1.

2.

3.

4.

5.

6.

7.

8.

9.

10.

4-36

EXERCISE 4-9A (cont.)

b. NC = Net Change in Cash

The Pet Store Horizontal Statements Model for 2016

Balance Sheet

Income Statement

Statement

of

Assets

=

Liab.

+

Stkholders’ Equity

Rev.

−

Exp.

=

Net Inc.

Cash Flows

Cash

+

A. Rec.

+

Inv.

=

A. Pay.

+

C. Stk.

+

Ret. Ear.

1. Stock

60,000

+

NA

+

NA

=

NA

+

60,000

+

NA

NA

−

NA

=

NA

60,000 FA

2. Pur Inv.

NA

+

NA

+

65,000

65,000

+

NA

+

NA

NA

−

NA

=

NA

NA

3. Freight

(900)

+

NA

+

900

=

NA

+

NA

+

NA

NA

−

NA

=

NA

(900) OA

4a. Sold Inv.

NA

+

71,000

+

NA

=

NA

+

NA

+

71,000

71,000

−

NA

=

71,000

NA

4b. Cost

NA

+

NA

+

(38,000)

=

NA

+

NA

+

(38,000)

NA

−

38,000

=

(38,000)

NA

5. Pd. Frt.

(620)

+

NA

+

NA

=

NA

+

NA

+

(620)

NA

−

620

=

(620)

(620) OA

6a. Ret. Sale

NA

+

(4,200)

+

NA

=

NA

+

NA

+

(4,200)

(4,200)

−

NA

=

(4,200)

NA

6b. Ret. Inv.

NA

+

NA

+

2,150

=

NA

+

NA

+

2,150

NA

−

(2,150)

=

2,150

NA

7. Coll. AR

58,300

+

(58,300)

+

NA

=

NA

+

NA

+

NA

NA

−

NA

=

NA

58,300 OA

8. Pd. AP

(59,200)

+

NA

+

NA

=

(59,200)

+

NA

+

NA

NA

−

NA

=

NA

(59,200) OA

9. Pd. Exp.

(2,600)

+

NA

+

NA

=

NA

+

NA

+

(2,600)

NA

−

2,600

=

(2,600)

(2,600) OA

10. Pd. Exp.

(3,100)

+

NA

+

NA

=

NA

+

NA

+

(3,100)

NA

−

3,100

=

(3,100)

(3,100) OA

End. Bal.

51,880

+

8,500

+

30,050

=

5,800

+

60,000

+

24,630

66,800

−

42,170

=

24,630

51,880 NC

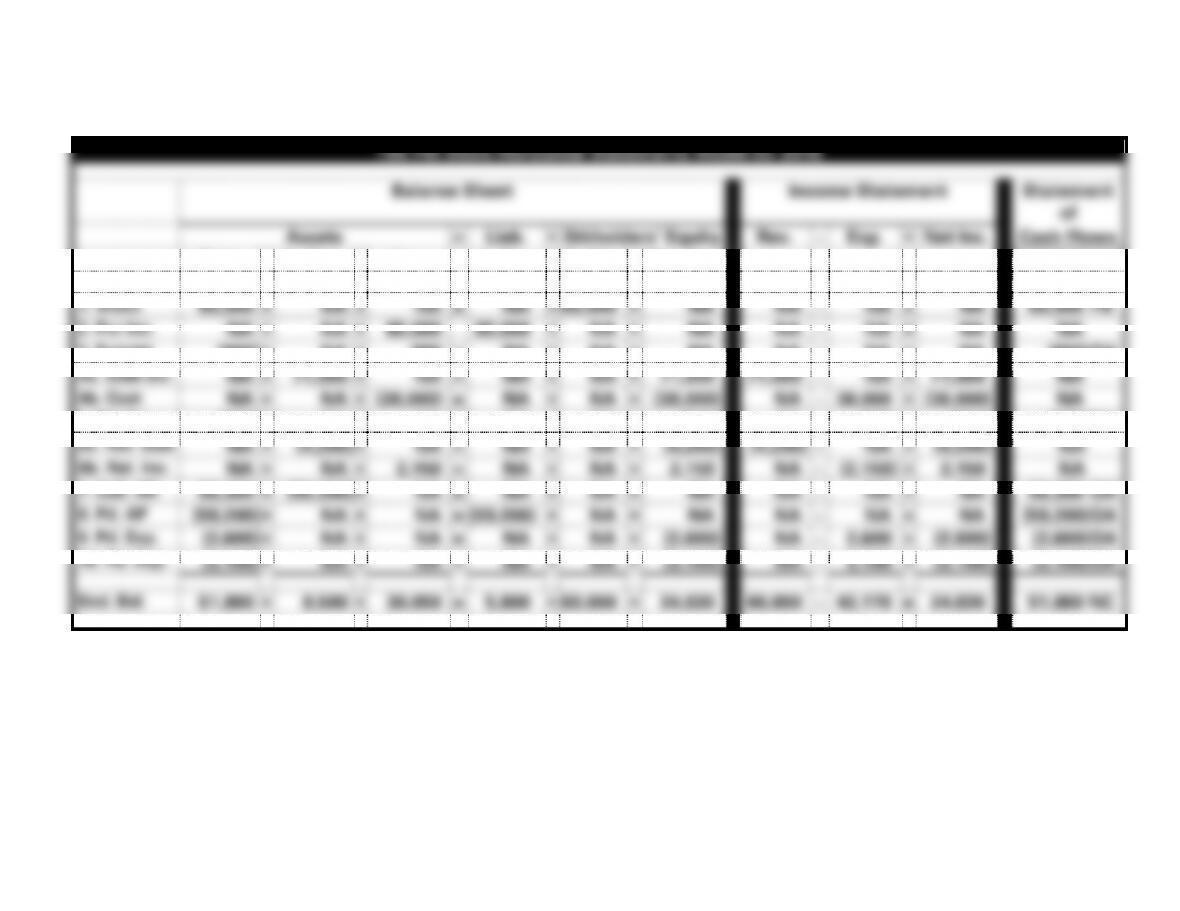

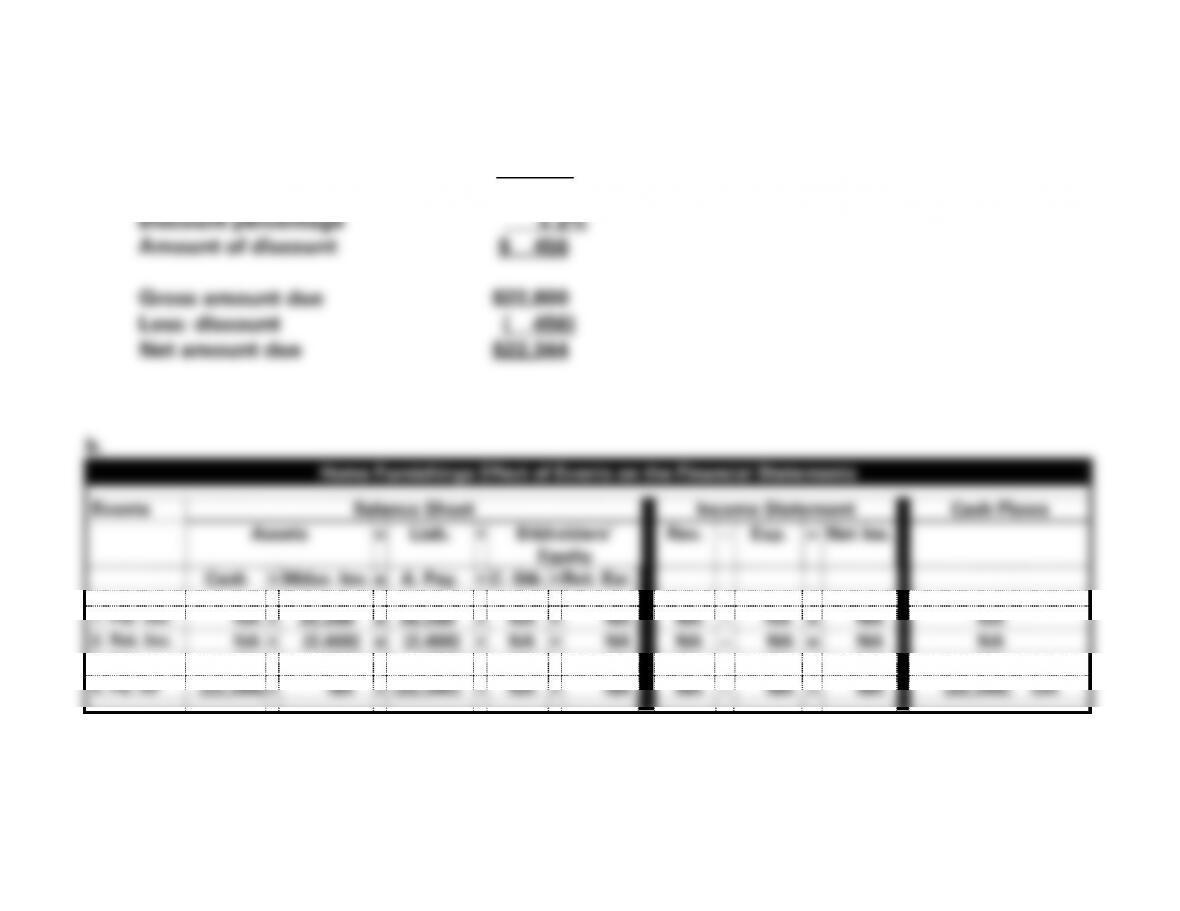

EXERCISE 4-10A

b. Purchase $25,200

Less: return (2,400)

Gross due (subject to discount) 22,800

4-38

EXERCISE 4-10A (cont.)

d. $22,800; they would not be eligible for the discount.

d.

Home Furnishings Effect of Events on the Financial Statements

Events

Balance Sheet

Income Statement

Cash Flows

Assets

=

Liab.

+

Stkholders’

Equity

Rev.

−

Exp.

=

Net Inc.

Cash

+

Mdse. Inv.

=

A. Pay.

+

C. Stk.

+

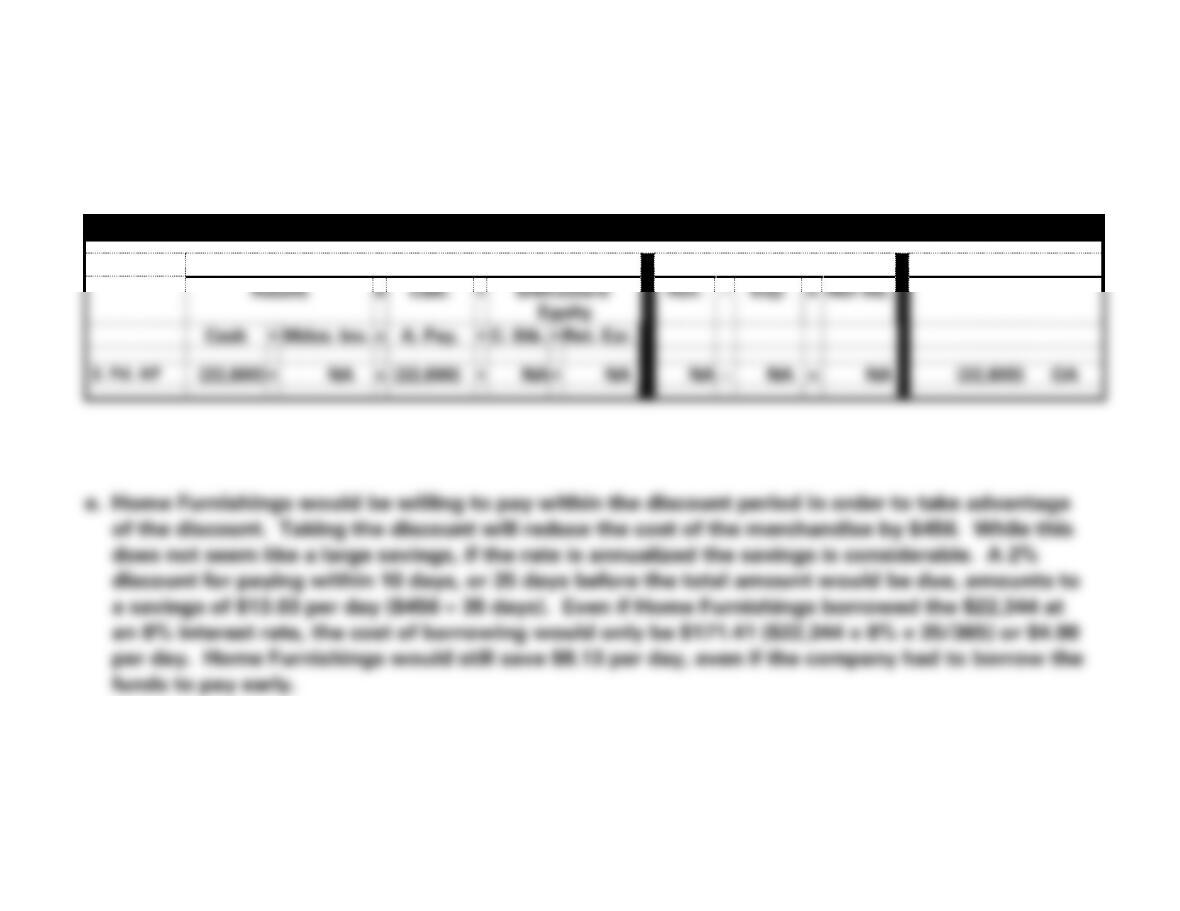

Ret. Ear.

3. Pd. AP

(22,800)

+

NA

=

(22,800)

+

NA

+

NA

NA

−

NA

=

NA

(22,800) OA

e. Home Furnishings would be willing to pay within the discount period in order to take advantage

of the discount. Taking the discount will reduce the cost of the merchandise by $456. While this

does not seem like a large savings, if the rate is annualized the savings is considerable. A 2%

discount for paying within 10 days, or 35 days before the total amount would be due, amounts to

a savings of $13.03 per day ($456 35 days). Even if Home Furnishings borrowed the $22,344 at

an 8% interest rate, the cost of borrowing would only be $171.41 ($22,344 x 8% x 35/365) or $4.90

per day. Home Furnishings would still save $8.13 per day, even if the company had to borrow the

funds to pay early.

4-39

EXERCISE 4-11A

Event

No.

Event

Type

Assets

=

Liab.

+

S.

Equity

Rev.

−

Exp.

=

Net Inc.

Cash Flows

1.

AE

+−

NA

NA

NA

NA

NA

− OA

2.

AS

+

+

NA

NA

NA

NA

NA

3.

AU

−

−

NA

NA

NA

NA

NA

4a.

AS

+

NA

+

+

NA

+

+ OA

4b.

AU

−

NA

−

NA

+

−

NA

5.

AU

−

−

NA

NA

NA

NA

− OA

6a.

AS

+

NA

+

+

NA

+

NA

6b.

AU

−

NA

−

NA

+

−

NA

7.

AU

−

NA

−

NA

+

−

− OA

8.

AE

+−

NA

NA

NA

NA

NA

− OA

9.

AE

+−

NA

NA

NA

NA

NA

+ OA

10.

AU

−

NA

−

NA

+

−

− OA

4-40

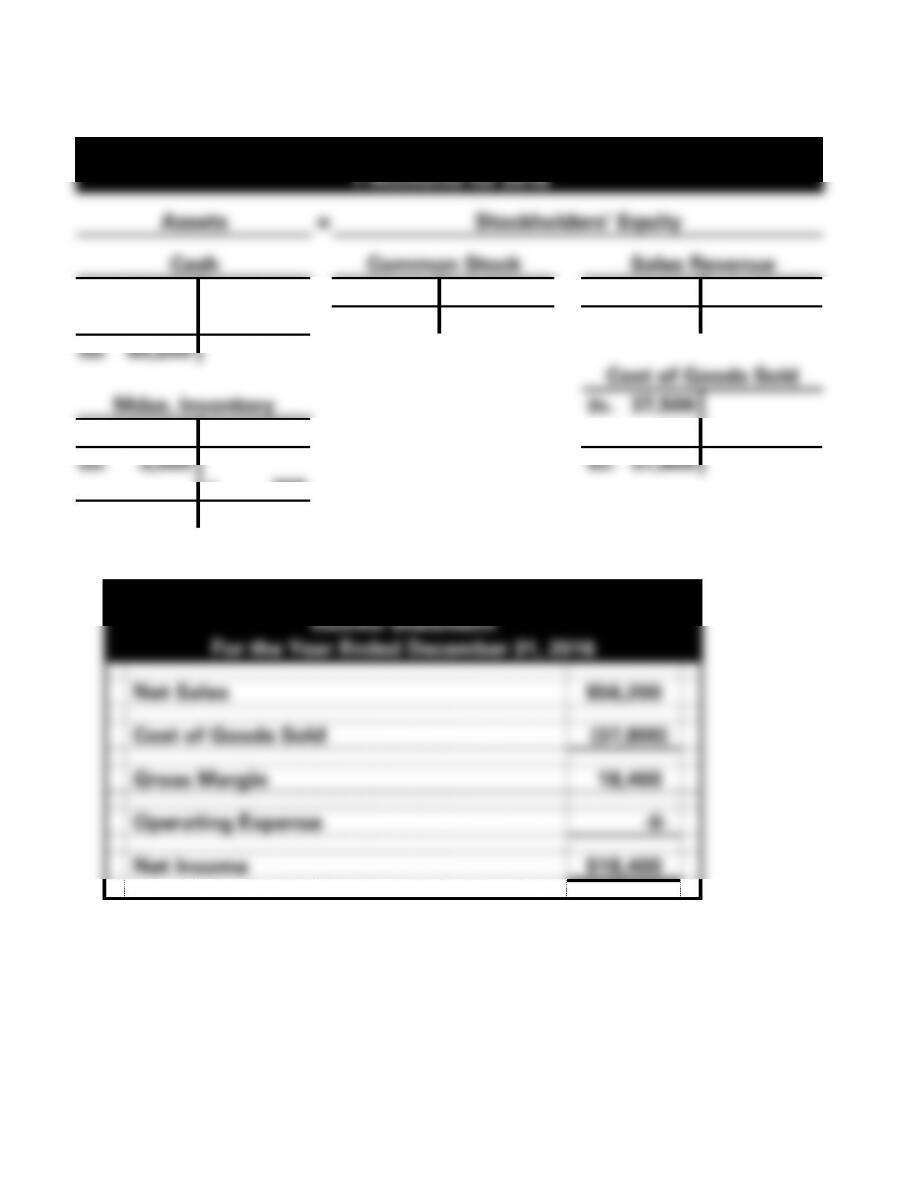

EXERCISE 4-12A

a.

Ho Designs

T-Accounts for 2016

Assets

=

Stockholders’ Equity

Cash

Common Stock

Sales Revenue

1. 70,000

2. 41,000

1. 70,000

3a. 56,200

3a. 56,200

Bal. 70,000

Bal. 56,200

Bal. 85,200

Cost of Goods Sold

Mdse. Inventory

3b. 37,500

2. 41,000

3b. 37,500

4. 300

Bal. 3,500

Bal. 37,800

4. 300

Bal. 3,200

b.

Ho Designs

Income Statement

For the Year Ended December 31, 2016

Net Sales

$56,200

Cost of Goods Sold

(37,800)

Gross Margin

18,400

Operating Expense

-0-

Net Income

$18,400