1-21

1-22

EXERCISE 1-12A (cont.)

d.

Harris Company

Accounting Equation

Event

Assets

=

Liabilities

+

Stockholders’ Equity

Acquired assets

$7,800

$3,600

$4,200

Incurred loss

(4,900)

(700)

(4,200)

Balance

$2,900

$2,900

($ 0)

While creditors get first priority to receive assets in a business

liquidation, this does not mean they cannot lose all or a portion of the

assets they loan a business. In this case creditors are owed $3,600 but

the business has only $2,900 of assets. Since the creditors have first

priority, the entire $2,900 would be distributed to them. In this case

the creditors lose $700 ($3,600 original loan – $2,900 returned). Since

the investors own the business, they suffer the losses earned by the

business. The investors will lose the entire $4,200 they contributed to

the business.

1-23

1-24

EXERCISE 1-13A

Event

Classification

1.

Asset Source

2.

Asset Use

3.

Asset Use

4.

Asset Source

5.

Asset Exchange

6.

NA

7.

Asset Source

8.

Asset Use

9.

Asset Source

10.

Asset Exchange

11.

Asset Source

EXERCISE 1-14A

Steps:

1.

Common Stock Issued = Change in Common Stock

2.

Change in Stk. Equity = Change in Com. Stock + Change in Ret. Earn.

3.

Increase in Ret. Earn. = Net Income − Dividends

Alternate Solution:

From the Statement of Changes in Stockholders’ Equity we know (with

1-26

1-27

EXERCISE 1-15A

a.

Majka Company

Accounting Equation for 2016

Assets

=

Liabilities

+

Stockholders’ Equity

Common

Retained

Event

Cash

=

+

Stock

+

Earnings

1. Cash revenues

28,600

NA

NA

28,600

2. Paid expenses

(13,200)

NA

NA

(13,200)

3. Paid dividend

(1,500)

NA

NA

(1,500)

Ending Balance

13,900

=

-0-

+

-0-

+

13,900

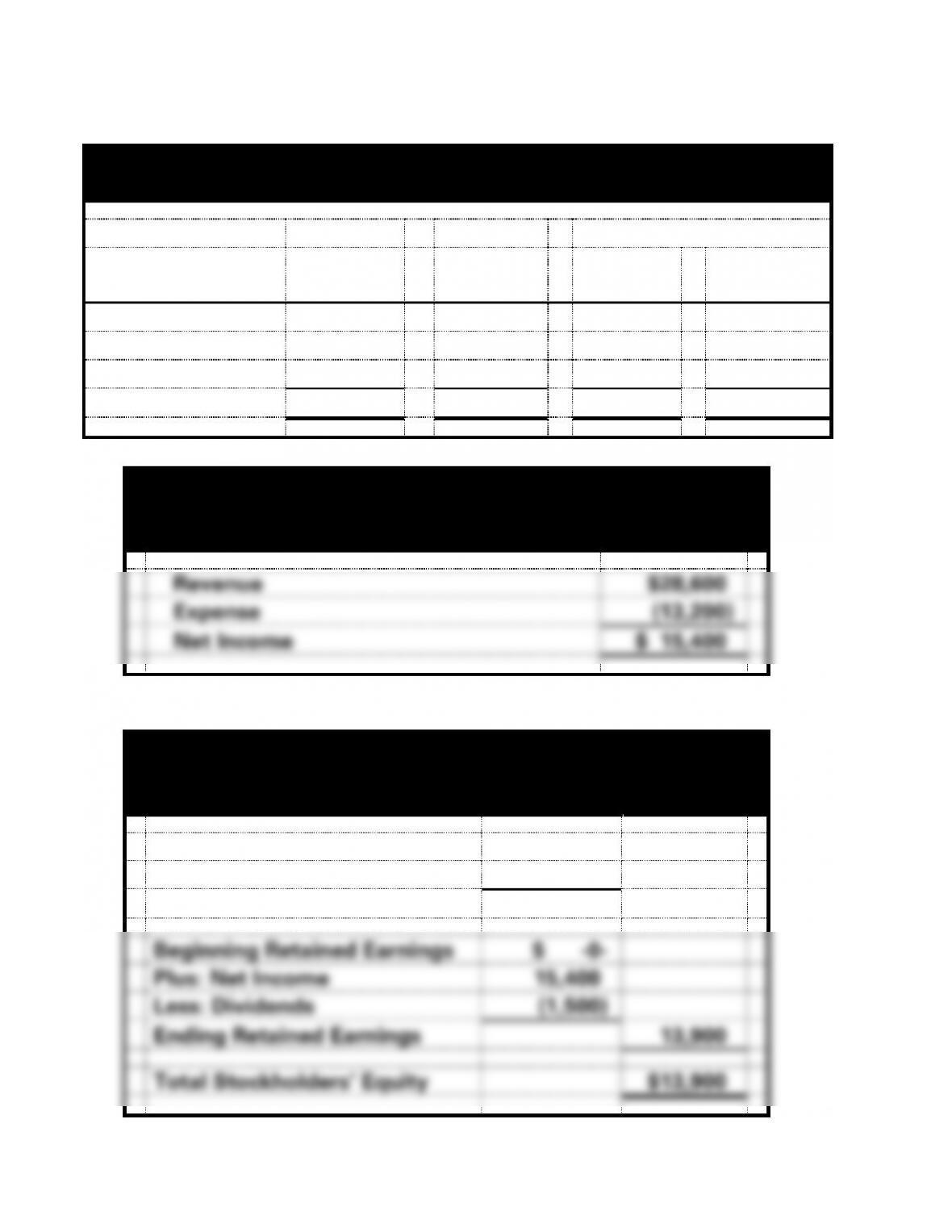

b.

Majka Company

Income Statement

For the Year Ended December 31, 2016

Revenue

$28,600

Expense

(13,200)

Net Income

$ 15,400

Majka Company

Statement of Changes in Stockholders’ Equity

For the Year Ended December 31, 2016

Beginning Common Stock

$ -0-

Plus: Common Stock Issued

0

Ending Common Stock

$ -0-

Beginning Retained Earnings

$ -0-

Plus: Net Income

15,400

Less: Dividends

(1,500)

Ending Retained Earnings

13,900

Total Stockholders’ Equity

$13,900

1-28

EXERCISE 1-15A (cont.)

Majka Company

Balance Sheet

As of December 31, 2016

Assets

Cash

$13,900

Liabilities

$ -0-

Stockholders’ Equity

Common Stock

$ -0-

Retained Earnings

13,900

Total Stockholders’ Equity

13,900

Total Liabilities and Stockholders’ Equity

$13,900

1-29

EXERCISE 1-16A

Note: The memo should contain a reference to the fact that the value of

prepared.

1-30

EXERCISE 1-17A

a.

Moore Company

Statement of Cash Flows

For the Year Ended December 31, 2016

Cash Flows From Operating Activities:

Net Cash Inflow from Operating Activities

$ 24,800

Cash Flows From Investing Activities:

Net Cash Outflow from Investing Activities

(16,000)

Cash Flows From Financing Activities:

Net Cash Outflow from Financing Activities

(6,800)

Net Increase in Cash

2,000

Plus: Beginning Cash Balance

45,800

Ending Cash Balance

$47,800

1-31

1-32

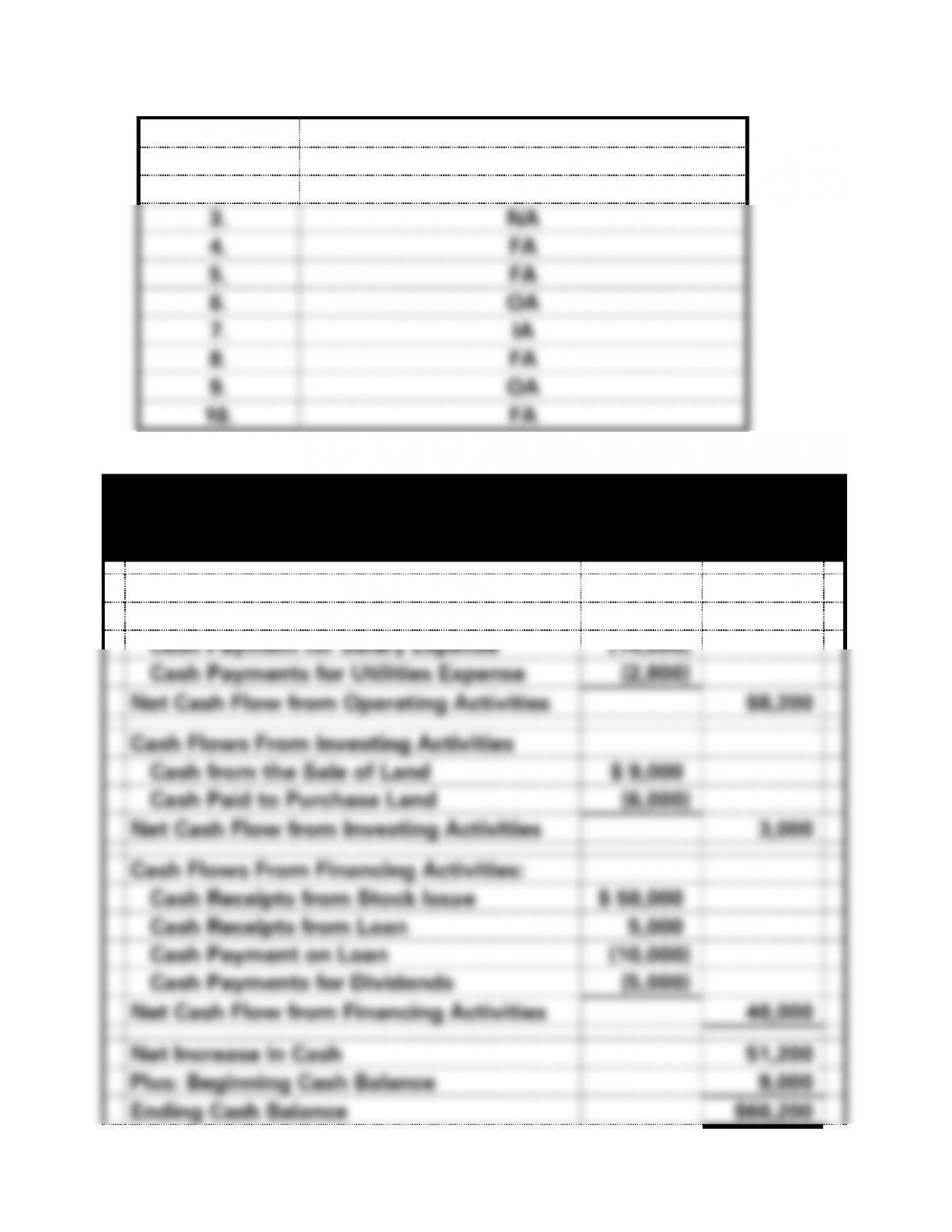

EXERCISE 1-18A a.

Event

Statement of Cash Flow Classification

1.

OA

2.

IA

3.

NA

4.

FA

5.

FA

6.

OA

7.

IA

8.

FA

9.

OA

10.

FA

b.

All Star Automotive Company

Statement of Cash Flows

For the Year Ended December 31, 2016

Cash Flows From Operating Activities:

Cash Receipts from Revenue

$ 25,000

Cash Payment for Salary Expense

(14,000)

Cash Payments for Utilities Expense

(2,800)

Net Cash Flow from Operating Activities

$8,200

Cash Flows From Investing Activities

Cash from the Sale of Land

$ 9,000

Cash Paid to Purchase Land

(6,000)

Net Cash Flow from Investing Activities

3,000

Cash Flows From Financing Activities:

Cash Receipts from Stock Issue

$ 50,000

Cash Receipts from Loan

5,000

Cash Payment on Loan

(10,000)

Cash Payments for Dividends

(5,000)

Net Cash Flow from Financing Activities

40,000

Net Increase in Cash

51,200

Plus: Beginning Cash Balance

9,000

Ending Cash Balance

$60,200

1-33

EXERCISE 1-19A

a.

Dakota Company

Accounting Equation for 2016

Assets

=

Liabilities

+

Stockholders’ Equity

Event

Cash

+

Land

=

Notes

Payable

+

Com.

Stock

+

Retained

Earnings

Acct.

Title/RE

Bal. 1/1/16

2,000

12,000

-0-

6,000

8,000

1. Issued stk.

30,000

NA

NA

30,000

NA

NA

2. Pur. Land

(12,000)

12,000

NA

NA

NA

NA

3. Loan

10,000

NA

10,000

NA

NA

NA

4. Provide Svc.

20,000

NA

NA

NA

20,000

Svc. Rev.

5. Paid Utilities

(1,000)

NA

NA

NA

(1,000)

Util. Exp.

6. Pd. Op. Exp.

(15,000)

NA

NA

NA

(15,000)

Op. Exp.

7. Paid Div.

(2,000)

NA

NA

NA

(2,000)

Dividends

8. Land Value

NA

NA

NA

NA

NA

Totals

32,000

+

24,000

=

10,000

+

36,000

+

10,000

b.

Dakota Company

Income Statement

For the Year Ended December 31, 2016

Service Revenue

$20,000

Utilities Expense

(1,000)

Operating Expense

(15,000)

Net Income

$ 4,000

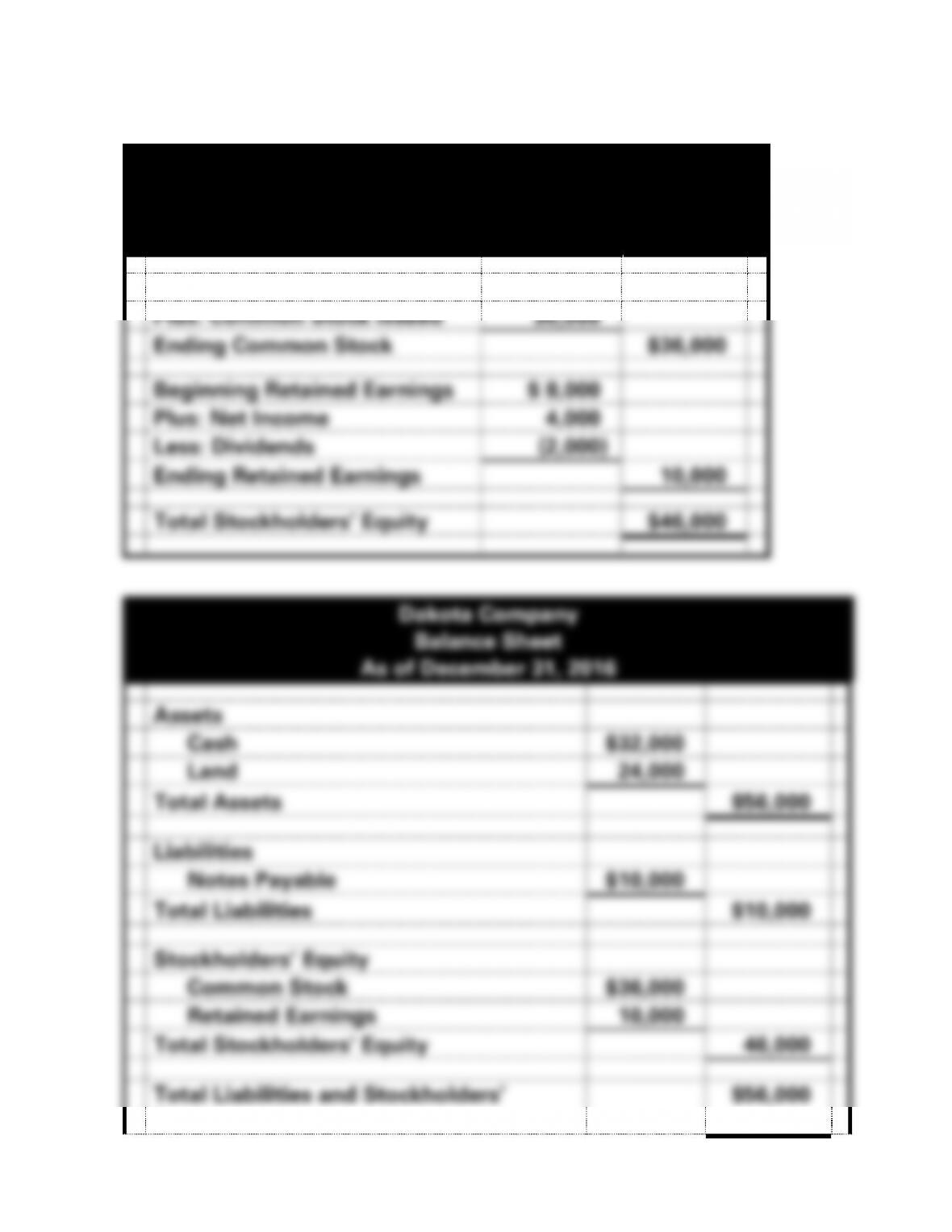

EXERCISE 1-19A b. (cont.)

Dakota Company

Statement of Changes in Stockholders’ Equity

For the Year Ended December 31, 2016

Beginning Common Stock

$ 6,000

Plus: Common Stock Issued

30,000

Ending Common Stock

$36,000

Beginning Retained Earnings

$ 8,000

Plus: Net Income

4,000

Less: Dividends

(2,000)

Ending Retained Earnings

10,000

Total Stockholders’ Equity

$46,000

Assets

Cash

Land

Total Assets

$56,000

Liabilities

Notes Payable

Total Liabilities

$10,000

Stockholders’ Equity

Common Stock

Retained Earnings

Total Stockholders’ Equity

46,000

1-35

1-36

EXERCISE 1-19A b. (cont.)

Dakota Company

Statement of Cash Flows

For the Year Ended December 31, 2016

Cash Flows From Operating Activities:

Cash Receipts from Customers

$20,000

Cash Payment for Utilities Expense

(1,000)

Cash Payments for Other Operating Exp.

(15,000)

Net Cash Flow from Operating Activities

$ 4,000

Cash Flows From Investing Activities:

Cash Paid to Purchase Land

$(12,000)

Net Cash Flow from Investing Activities

(12,000)

Cash Flows From Financing Activities:

Cash Receipts from Stock Issue

$30,000

Cash Receipts from Loan

10,000

Cash Payments for Dividends

(2,000)

Net Cash Flow from Financing Activities

38,000

Net Increase in Cash

30,000

Plus: Beginning Cash Balance

2,000

Ending Cash Balance

$32,000

1-37

EXERCISE 1-20A

a.

Riley Company: Asset Exchange

b.

Smally Company: Asset Exchange

c.

Riley Company: Investing Activity

d.

Smally Company: Investing Activity

EXERCISE 1-21A

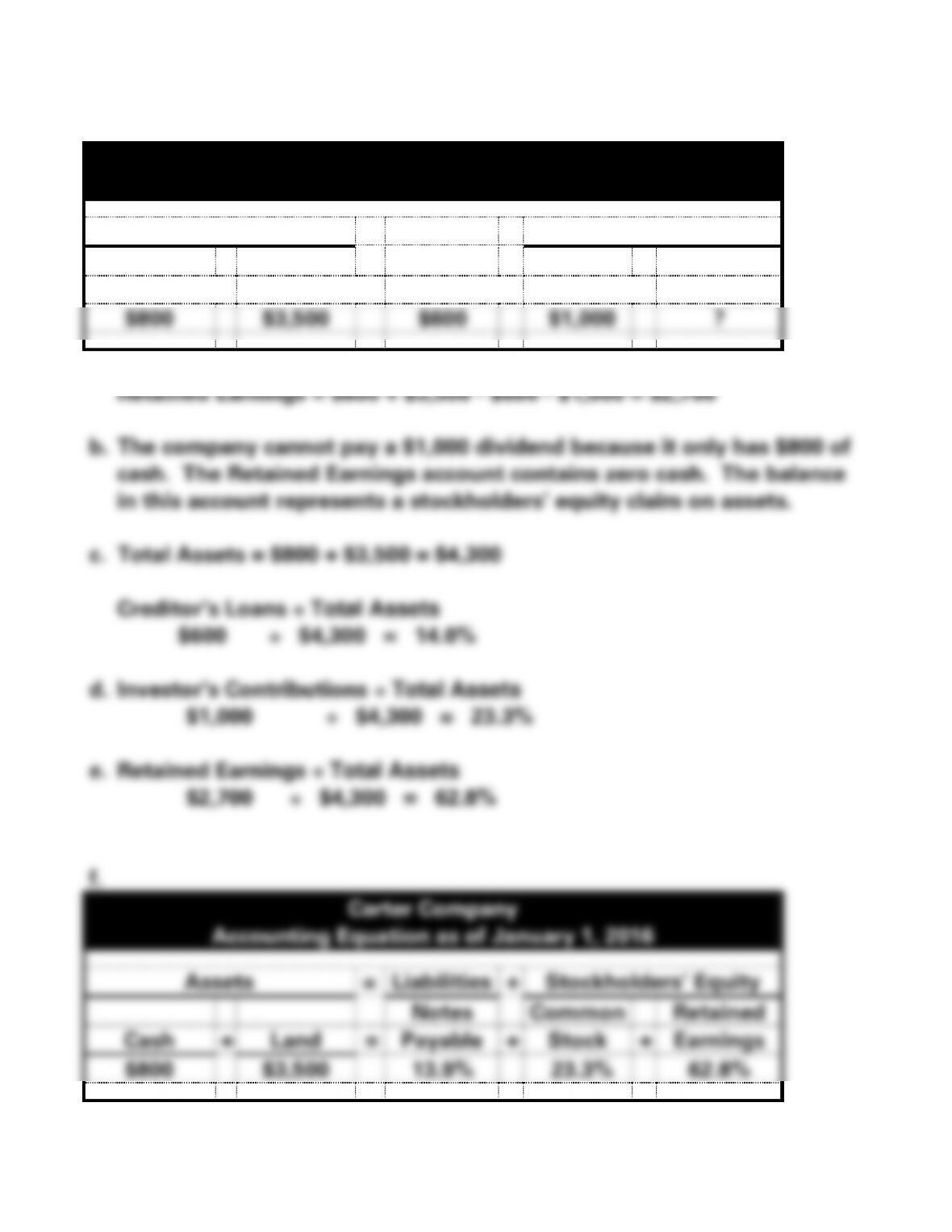

a.

Carter Company

Accounting Equation as of January 1, 2016

Assets

=

Liabilities

+

Stockholders’ Equity

Notes

Common

Retained

Cash

+

Land

=

Payable

+

Stock

+

Earnings

$800

$3,500

$600

$1,000

?

Accounting Equation as of January 1, 2016

Assets

=

Liabilities

+

Stockholders’ Equity

Notes

Common

Retained

Cash

+

Land

=

Payable

+

+

Earnings

1-39

EXERCISE 1-21A (cont.)

g.

Carter Company

Accounting Equation as of December 31, 2016

Assets

=

Liabilities

+

Stockholders’ Equity

Notes

Common

Retained

Cash

+

Land

=

Payable

+

Stock

+

Earnings

$800

$3,500

$1,600

$1,000

1,700

1,800

NA

NA

NA

1,800

Rev.

(1,200)

NA

NA

NA

(1,200)

Exp.

(500)

NA

NA

NA

(500)

Div

900

$3,500

$1,600

$1,000

$1,800

Carter Company

Income Statement

For the Year Ended December 31, 2016

Revenue

$1,800

Expenses

(1,200)

Net Income

$ 600