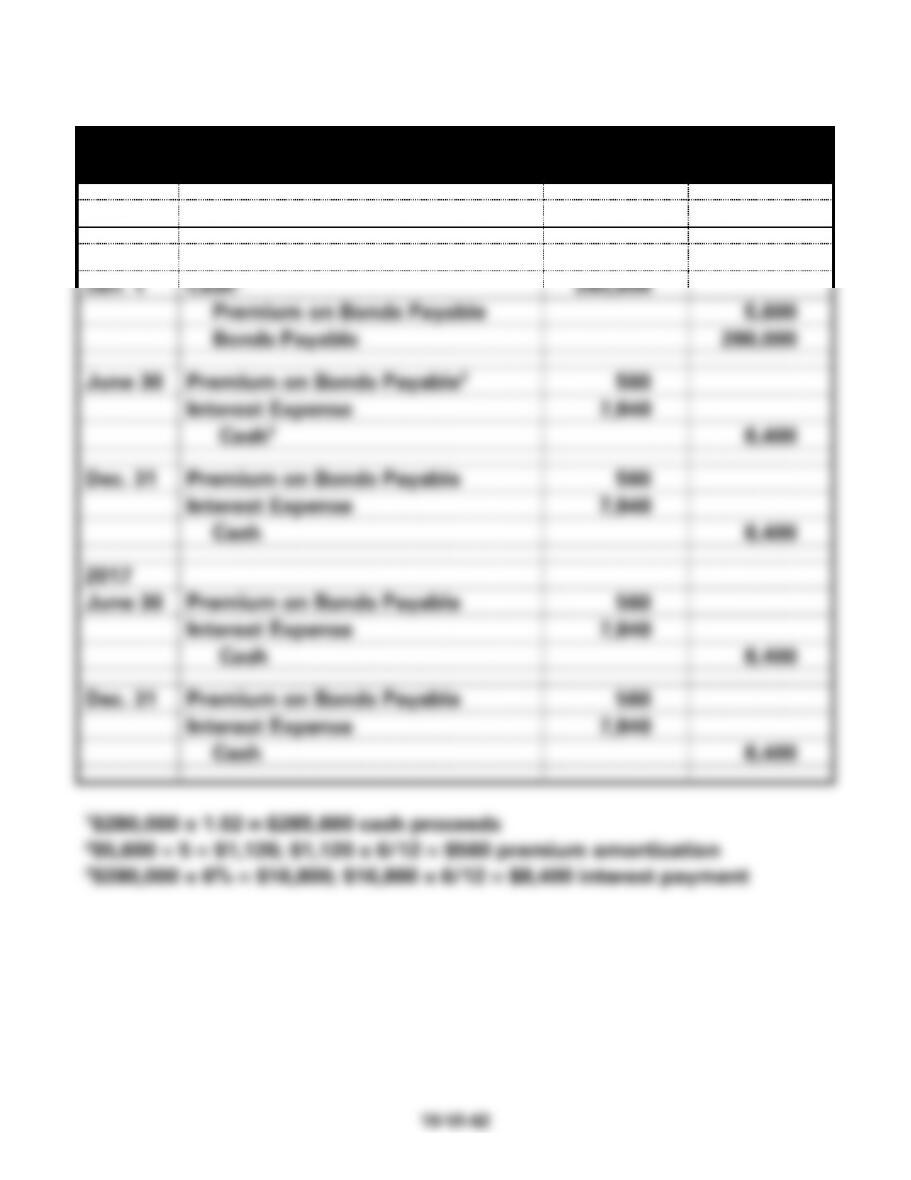

EXERCISE 10-18A

Sayers Company

General Journal

Date

Account Titles

Debit

Credit

2016

Jan. 1

Cash1

285,600

Premium on Bonds Payable

5,600

Bonds Payable

280,000

June 30

Premium on Bonds Payable2

560

Interest Expense

7,840

Cash3

8,400

Dec. 31

Premium on Bonds Payable

560

Interest Expense

7,840

Cash

8,400

2017

June 30

Premium on Bonds Payable

560

Interest Expense

7,840

Cash

8,400

Dec. 31

Premium on Bonds Payable

560

Interest Expense

7,840

Cash

8,400

EXERCISE 10-19A

a.

Face Value

−

Bond Price

=

Discount

$300,000

−

$278,932

=

$21,068

b.

Carrying Value

x

Effective Rate

=

Interest Expense

$278,932

x

.07

=

$19,525

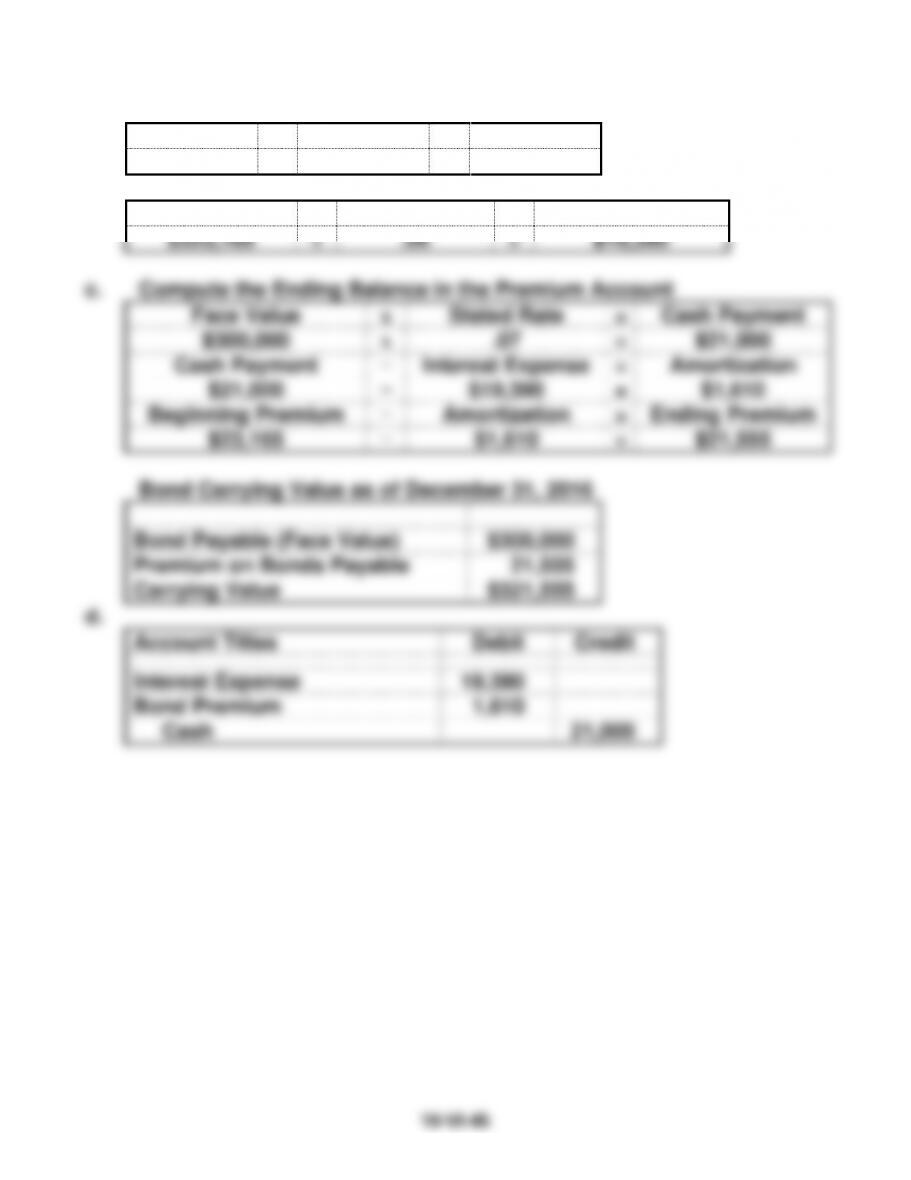

c. Compute the Ending Balance in the Discount Account

Face Value

x

Stated Rate

=

Cash Payment

$300,000

x

.06

=

$18,000

Interest Expense

−

Cash Payment

=

Amortization

$19,525

−

$18,000

=

$1,525

Beginning Discount

−

Amortization

=

Ending Discount

$21,068

−

$1,525

=

$19,543

Bond Carrying Value as of December 31, 2016

Bond Payable (Face Value)

$300,000

Discount on Bonds Payable

19,543

Carrying Value

$280,457

d.

Account Titles

Debit

Credit

Interest Expense

19,525

Bond Discount

1,525

Cash

18,000

EXERCISE 10-20A

a.

Date

Cash

Payment

Interest

Expense

Discount

Amortization

Carrying

Value

January 1, 2016

76,888

December 31, 2016

6,400

6,920

520

77,408

December 31, 2017

6,400

6,967

567

77,975

December 31, 2018

6,400

7,018

618

78,593

December 31, 2019

6,400

7,073

673

79,266

December 31, 2020

6,400

7,134*

734

80,000

Totals

32,000

35,112

3,112

Bond liability

$80,000

Less: Bond discount

734

Carrying value

$79,266

c. The income statement would show $7,073 of interest expense.

d. The statement of cash flows would show a $6,400 cash outflow for

interest in the operating activities section.

EXERCISE 10-21A

a.

Bond Price

−

Face Value

=

Premium

$323,165

−

$300,000

=

$23,165

b.

Carry Value

x

Effective Rate

=

Interest Expense

$323,165

x

.06

=

$19,390

c. Compute the Ending Balance in the Premium Account

Face Value

x

Stated Rate

=

Cash Payment

$300,000

x

.07

=

$21,000

Cash Payment

−

Interest Expense

=

Amortization

$21,000

−

$19,390

=

$1,610

Beginning Premium

−

Amortization

=

Ending Premium

$23,165

−

$1,610

=

$21,555

Bond Carrying Value as of December 31, 2016

Bond Payable (Face Value)

$300,000

Premium on Bonds Payable

21,555

Carrying Value

$321,555

d.

Account Titles

Debit

Credit

Interest Expense

19,390

Bond Premium

1,610

Cash

21,000

EXERCISE 10-22A

a.

Date

Cash

Payment

Interest

Expense

Premium

Amortization

Carrying

Value

January 1, 2016

156,150

December 31, 2016

12,000

10,931

1,069

155,081

December 31, 2017

12,000

10,856

1,144

153,937

December 31, 2018

12,000

10,776

1,224

152,713

December 31, 2019

12,000

10,690

1,310

151,403

December 31, 2020

12,000

10,597*

1,403

150,000

Totals

60,000

53,850

6,150

EXERCISE 10-23A

Since the stated rate of interest is higher than the effective interest rate

the bonds will sell at a premium. Because the effective interest rate

EXERCISE 10-24A

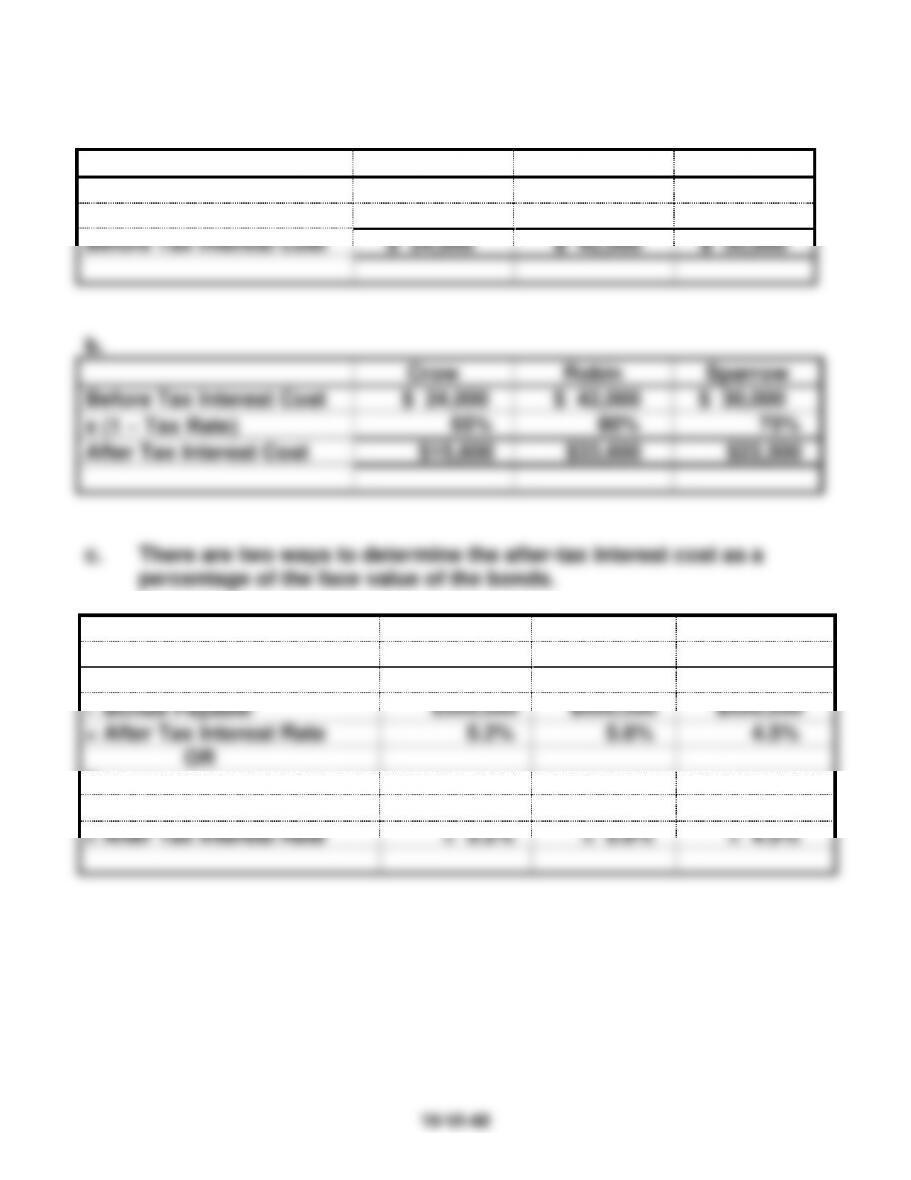

a.

Crow

Robin

Sparrow

Bonds Payable

$300,000

$600,000

$500,000

Interest Rate

8%

7%

6%

Before Tax Interest Cost

$ 24,000

$ 42,000

$ 30,000

b.

Crow

Robin

Sparrow

Before Tax Interest Cost

$ 24,000

$ 42,000

$ 30,000

x (1 − Tax Rate)

65%

80%

75%

After Tax Interest Cost

$15,600

$33,600

$22,500

1.

Crow

Robin

Sparrow

After Tax Interest Cost

$ 15,600

$ 33,600

$ 22,500

Bonds Payable

$300,000

$600,000

$500,000

= After Tax Interest Rate

5.2%

5.6%

4.5%

OR

2.

Interest Rate x (1 − Tax Rate)

.08 x ( 1−.35)

.07 x (1 − .2)

.06 x (1 − .25)

= After Tax Interest Rate

= 5.2%

= 5.6%

= 4.5%

EXERCISE 10-25A

a. Note to Instructor: Students may be able to solve this problem more

easily if they first prepare a table showing the balances in current

assets, total assets, current liabilities, and total liabilities for each

situation. Then, they can more easily compute the new ratios and

10–VI–50

SOLUTIONS TO PROBLEMS – SERIES A – CHAPTER 10

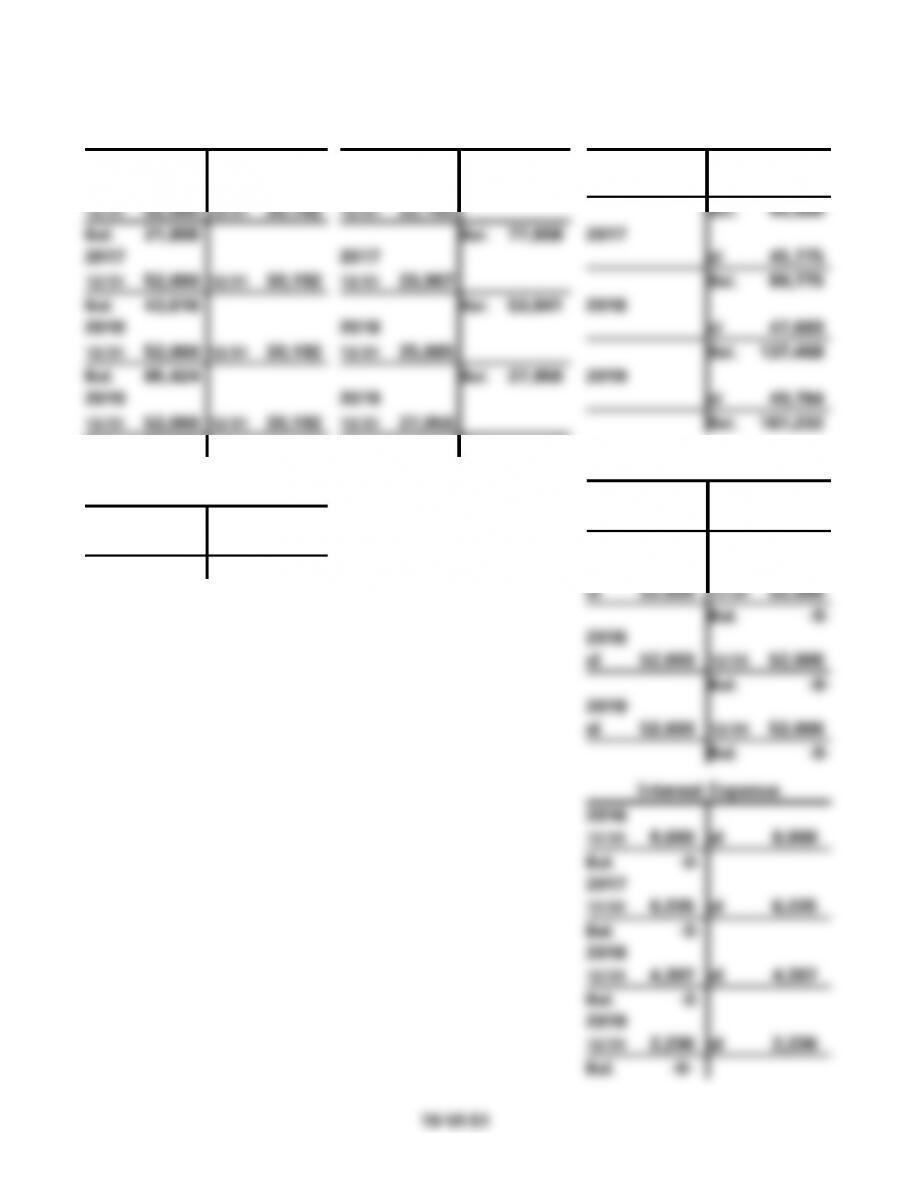

PROBLEM 10-26A

a.

Brown Co.

Amortization Schedule

$100,000, 4-Yr. Term Note, 8% Interest Rate

Year

Prin. Bal.

on Jan 1

Cash Pay.

Dec. 31

Applied to

Interest

Applied to

Principal

Prin. Bal.

End of Period

2016

$100,000

$30,192

$8,000

$22,192

$77,808

2017

77,808

30,192

6,225

23,967

53,841

2018

53,841

30,192

4,307

25,885

27,956

2019

27,956

30,192

2,236

27,956

-0-

PROBLEM 10-26A (cont.)

b. Provided for the use of the Instructor:

Cash

Notes Payable

Retained Earnings

2016

2016

2016

1/1 100,000

1/1 100,000

1/1 100,000

cl 44,000

12/31 52,000

12/31 30,192

12/31 22,192

Bal. 44,000

Bal. 21,808

Bal. 77,808

2017

2017

2017

cl 45,775

12/31 52,000

12/31 30,192

12/31 23,967

Bal. 89,775

Bal. 43,616

Bal. 53,841

2018

2018

2018

cl 47,693

12/31 52,000

12/31 30,192

12/31 25,885

Bal. 137,468

Bal. 65,424

Bal. 27,956

2019

2019

2019

cl 49,764

12/31 52,000

12/31 30,192

12/31 27,956

Bal. 187,232

Bal. 87,232

Bal. -0-

Rent Revenue

Land

2016

2016

cl 52,000

12/31 52,000

1/1 100,000

Bal. -0–

Bal. 100,000

2017

cl 52,000

12/31 52,000

Bal. -0–

2018

cl 52,000

12/31 52,000

Bal. -0–

2019

cl 52,000

12/31 52,000

Bal. -0–

Interest Expense

2016

12/31 8,000

cl 8,000

Bal. -0-

2017

12/31 6,225

cl 6,225

Bal. -0-

2018

12/31 4,307

cl 4,307

Bal. -0-

2019

12/31 2,236

cl 2,236

Bal. -0-

10–VI–51

PROBLEM 10-26A b. (cont.)

Brown Co.

Financial Statements

2016

2017

2018

2019

Income Statements for the Year Ended December 31

Rent Revenue

$52,000

$52,000

$52,000

$52,000

Interest Expense

(8,000)

(6,225)

(4,307)

(2,236)

Net Income

$44,000

$45,775

$47,693

$49,764

Balance Sheets as of December 31

Assets

Cash

$ 21,808

$ 43,616

$ 65,424

$ 87,232

Land

100,000

100,000

100,000

100,000

Total Assets

$121,808

$143,616

$165,424

$187,232

Liabilities

Notes Payable

$ 77,808

$53,841

$ 27,956

$ -0-

Stockholders’ Equity

Retained Earnings

44,000

89,775

137,468

187,232

Total Liab. and Stk. Equity

$121,808

$143,616

$165,424

$187,232

Statements of Cash Flows for the Year Ended December 31

Cash Flows From Oper. Act.:

Receipts from Rental

$52,000

$52,000

$52,000

$52,000

Paid for Interest

(8,000)

(6,225)

(4,307)

(2,236)

Net Cash Flow fm. Op. Act.:

44,000

45,775

47,693

49,764

Cash Flows From Inv. Act.:

Paid to Purchase Land

(100,000)

-0-

-0-

-0-

Cash Flows From Fin. Act.:

Proceeds from Loan

100,000

-0-

-0-

-0-

Repayment of Loan

(22,192)

(23,967)

(25,885)

(27,956)

Net Cash Flow from Fin. Act.

77,808

(23,967)

(25,885)

(27,956)

Net Change in Cash

21,808

21,808

21,808

21,808

Plus: Beginning Cash Balance

-0-

21,808

43,616

65,424

Ending Cash Balance

$ 21,808

$43,616

$65,424

$87,232

PROBLEM 10-26A (cont.)

c. Because the company is making both principal and interest payments

PROBLEM 10-27A

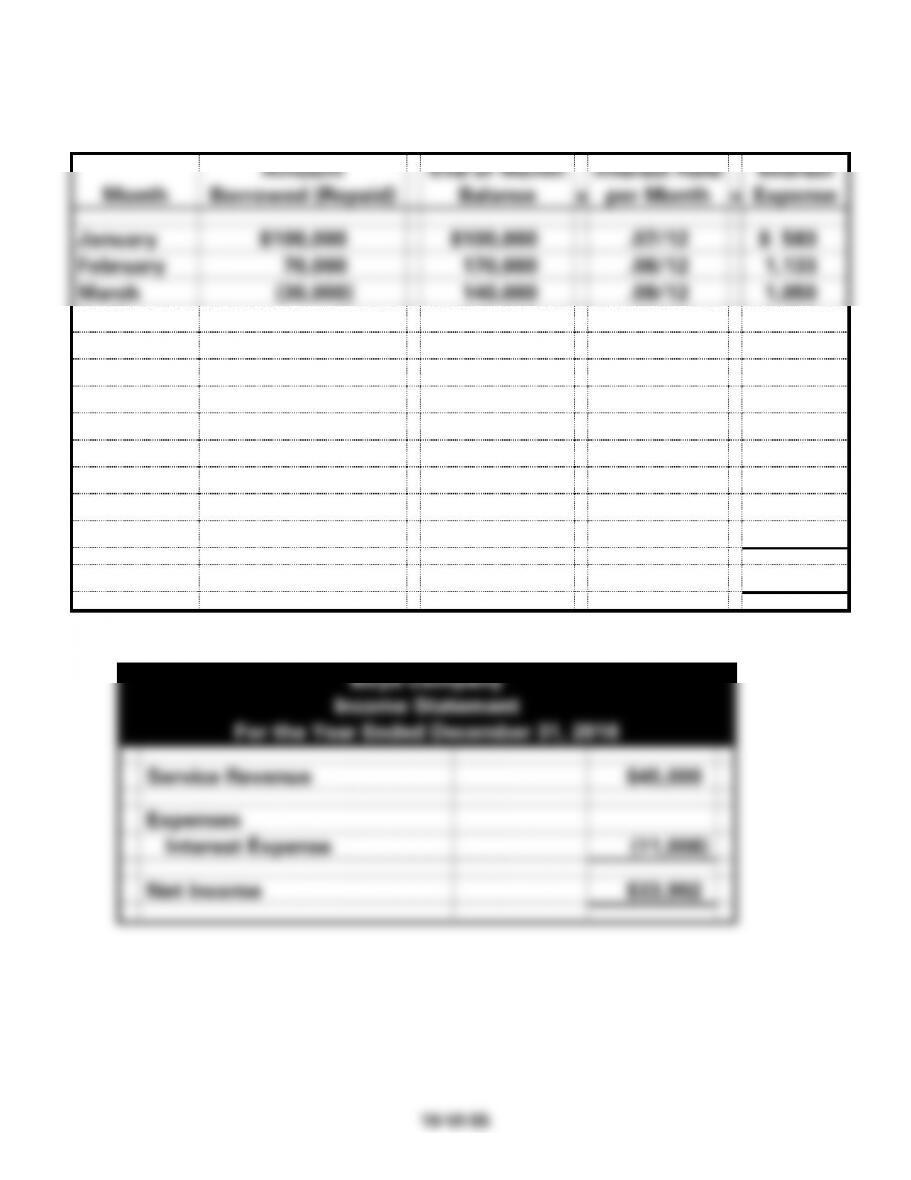

Computation of Interest Expense

Month

Amount

Borrowed (Repaid)

End of Month

Balance

x

Interest Rate

per Month

=

Interest

Expense

January

$100,000

$100,000

.07/12

$ 583

February

70,000

170,000

.08/12

1,133

March

(30,000)

140,000

.09/12

1,050

April

-0-

140,000

.09/12

1,050

May

-0-

140,000

.09/12

1,050

June

-0-

140,000

.09/12

1,050

July

-0-

140,000

.09/12

1,050

August

-0-

140,000

.09/12

1,050

September

-0-

140,000

.09/12

1,050

October

-0-

140,000

.09/12

1,050

November

(50,000)

90,000

.08/12

600

December

(40,000)

50,000

.07/12

292

Total

$11,008

a.

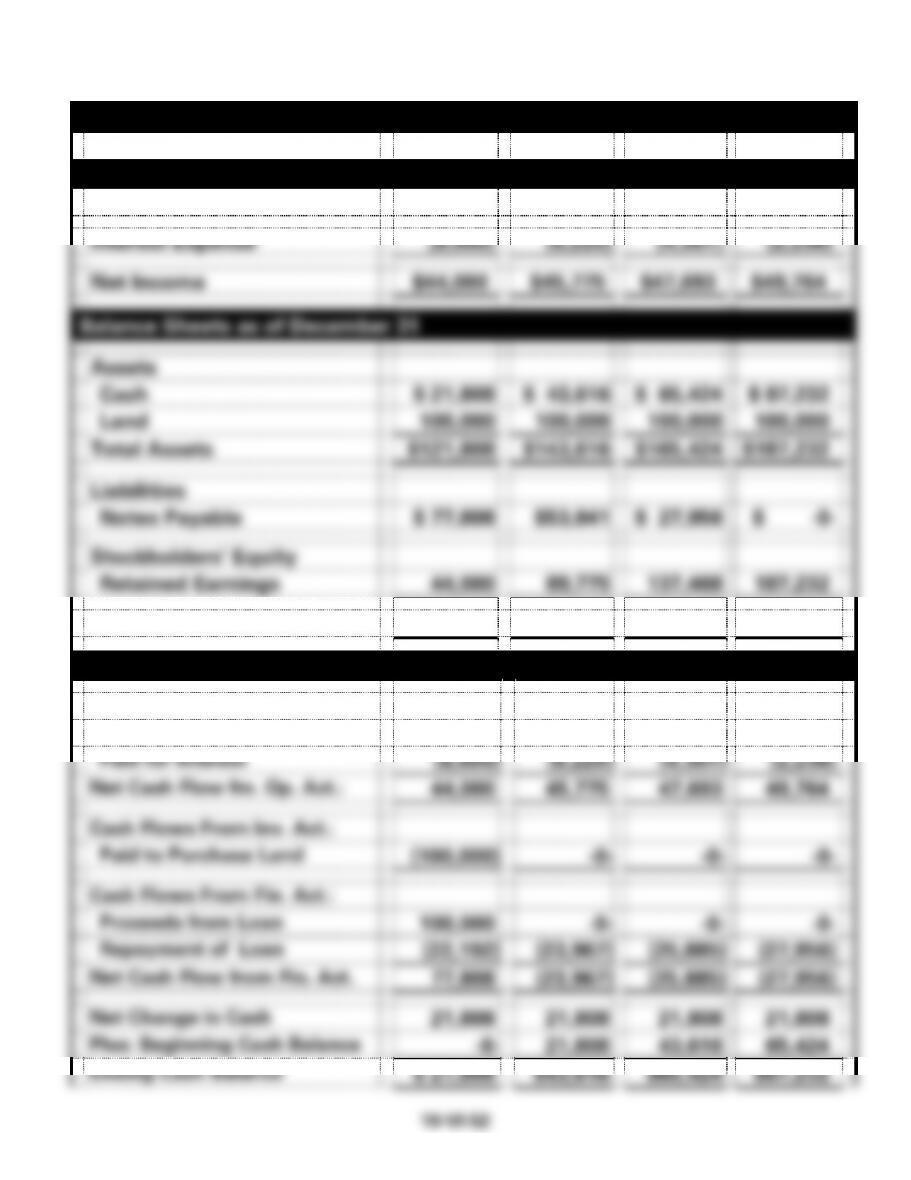

Boyd Company

Income Statement

For the Year Ended December 31, 2016

Service Revenue

$45,000

Expenses

Interest Expense

(11,008)

Net Income

$33,992

PROBLEM 10-27A a. (cont.)

Boyd Company

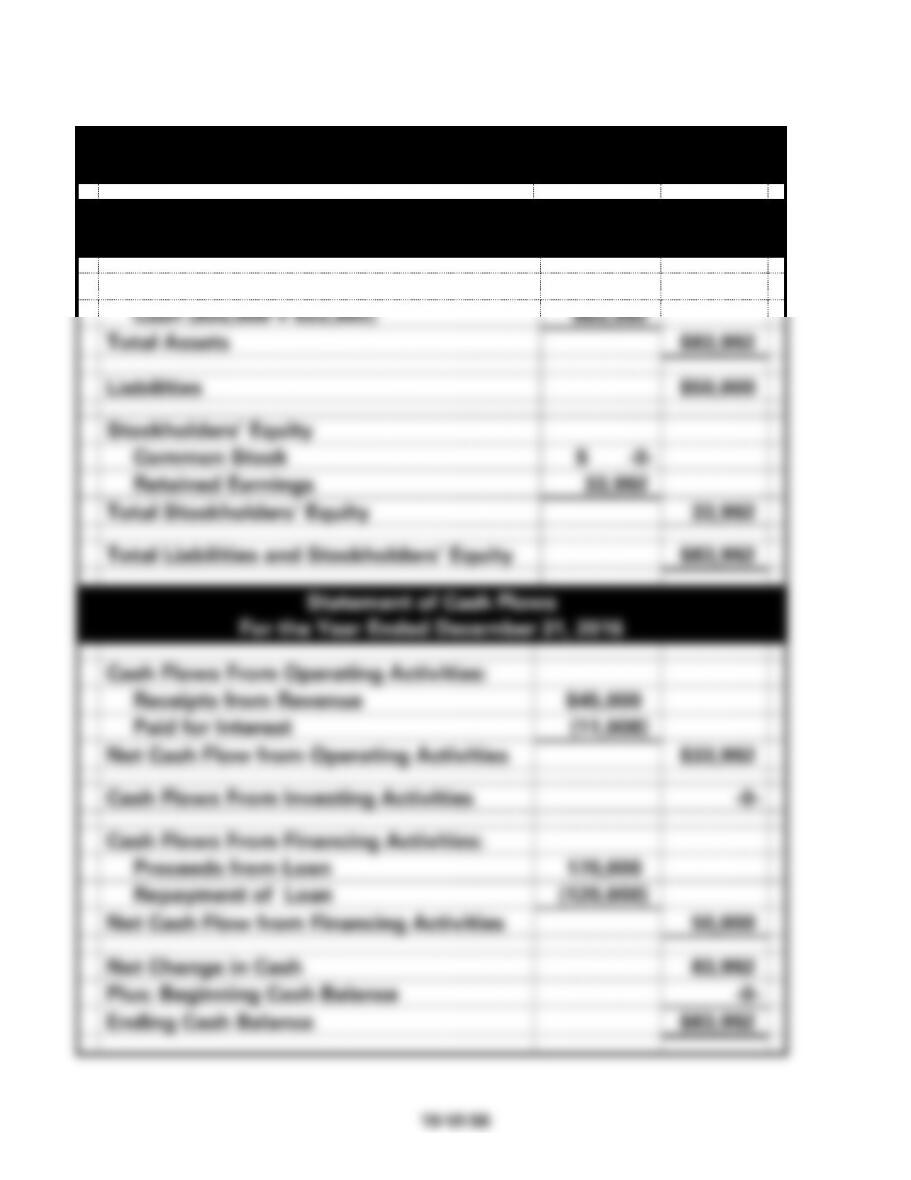

Financial Statements

Balance Sheet

As of December 31, 2016

Assets

Cash ($50,000 + $33,992)

$83,992

Total Assets

$83,992

Liabilities

$50,000

Stockholders’ Equity

Common Stock

$ -0-

Retained Earnings

33,992

Total Stockholders’ Equity

33,992

Total Liabilities and Stockholders’ Equity

$83,992

Statement of Cash Flows

For the Year Ended December 31, 2016

Cash Flows From Operating Activities:

Receipts from Revenue

$45,000

Paid for Interest

(11,008)

Net Cash Flow from Operating Activities

$33,992

Cash Flows From Investing Activities

-0-

Cash Flows From Financing Activities:

Proceeds from Loan

170,000

Repayment of Loan

(120,000)

Net Cash Flow from Financing Activities

50,000

Net Change in Cash

83,992

Plus: Beginning Cash Balance

-0-

Ending Cash Balance

$83,992

PROBLEM 10-27A (cont.)

b. Boyd used debt financing instead of equity financing. Boyd borrowed

PROBLEM 10-28A

a.

Effect of Transactions on Financial Statements

No.

Assets

=

Liab.

+

S. Equity

Rev./

Gain

−

Exp./

Loss

=

Net Inc.

Cash Flow

1.

600,000

=

600,000

+

NA

NA

−

NA

=

NA

600,000 FA

2.

(48,000)

=

NA

+

(48,000)

NA

−

48,000

=

(48,000)

(48,000) OA

3.

(624,000)

=

(600,000)

+

(24,000)

NA

−

24,000

=

(24,000)

(624,000) FA

b.

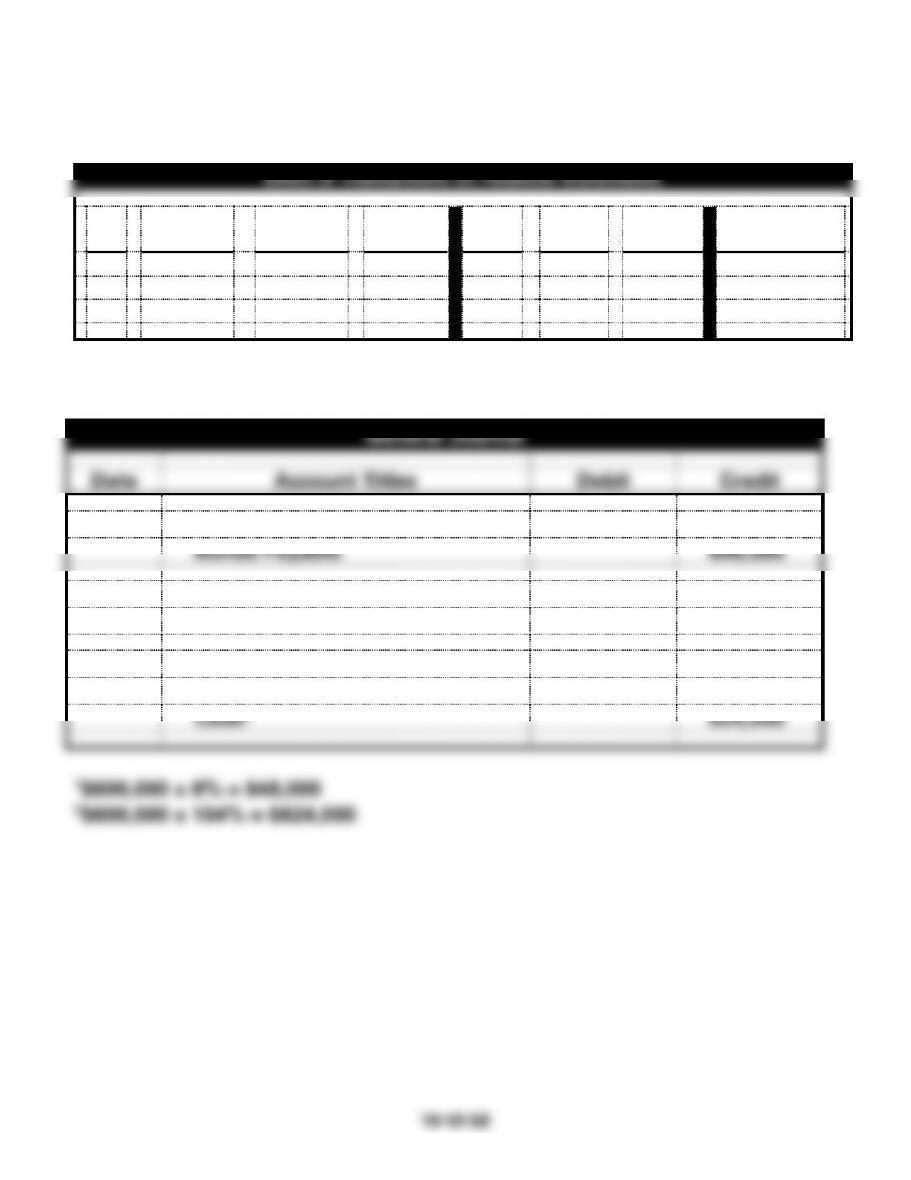

General Journal

Date

Account Titles

Debit

Credit

1.

Cash

600,000

Bonds Payable

600,000

2.

Interest Expense1

48,000

Cash

48,000

3.

Bonds Payable

600,000

Loss on Redemption of Bonds

24,000

Cash2

624,000

10–VI–58

10–VI–59

PROBLEM 10-29A

Pine Land Co.

2016

Event

No.

Type of

Event

Assets

=

Liabilities

+

Common

Stock

+

Retained

Earnings

Net

Income

Cash Flow

1.

AS

+

NA

+

NA

NA

+ FA

2.

AS

+

+

NA

NA

NA

+ FA

3.

AE

+−

NA

NA

NA

NA

− IA

4.

AS

+

NA

NA

+

+

+ OA

5a.

AU/CE

−

−

NA

−

−

− OA

6.

Closing

NA

NA

NA

NA

NA

NA

7.

Closing

NA

NA

NA

NA

NA

NA

8.

AS

+

NA

NA

+

+

+ OA

9a.

AU/CE

−

−

NA

−

−

− OA

10.

Closing

NA

NA

NA

NA

NA

NA

11.

Closing

NA

NA

NA

NA

NA

NA

12.

AS/AE

+

NA

NA

+

+

+ IA

13.

AU

−

−

NA

NA

NA

− FA

10–60

PROBLEM 10-30A

a. The bonds sold for less than the face amount; therefore, the bonds

were sold at a discount. This means that the stated rate of interest is

less than the market rate of interest. The amount of the discount acts

to equate the two interest rates. If the bonds had been sold at the face

10–61

PROBLEM 10-30A (cont.)

c.

2016

2017

Liabilities

Bonds Payable

$300,000

$300,000

Less: Discount on Bonds Payable

(5,400)1

(4,800)2

Carrying Value of Bonds Payable

$294,600

$295,200

2016

2017

d.

Interest Expense Reported on Income Statement:

$18,600

$18,600

2016

2017

e.

Interest Paid in Cash to Bondholders:

$18,000

$18,000