11–57

Solutions to Analyze, Think, Communicate – Chapter 11

ATC 11-1

All dollar amounts are in millions.

a. The par value of Targets’ common stock is $.0833 (8.33 cents),

according to its balance sheet.

b. The company had 632,930,740 shares issued and outstanding.

11–58

ATC 11-2

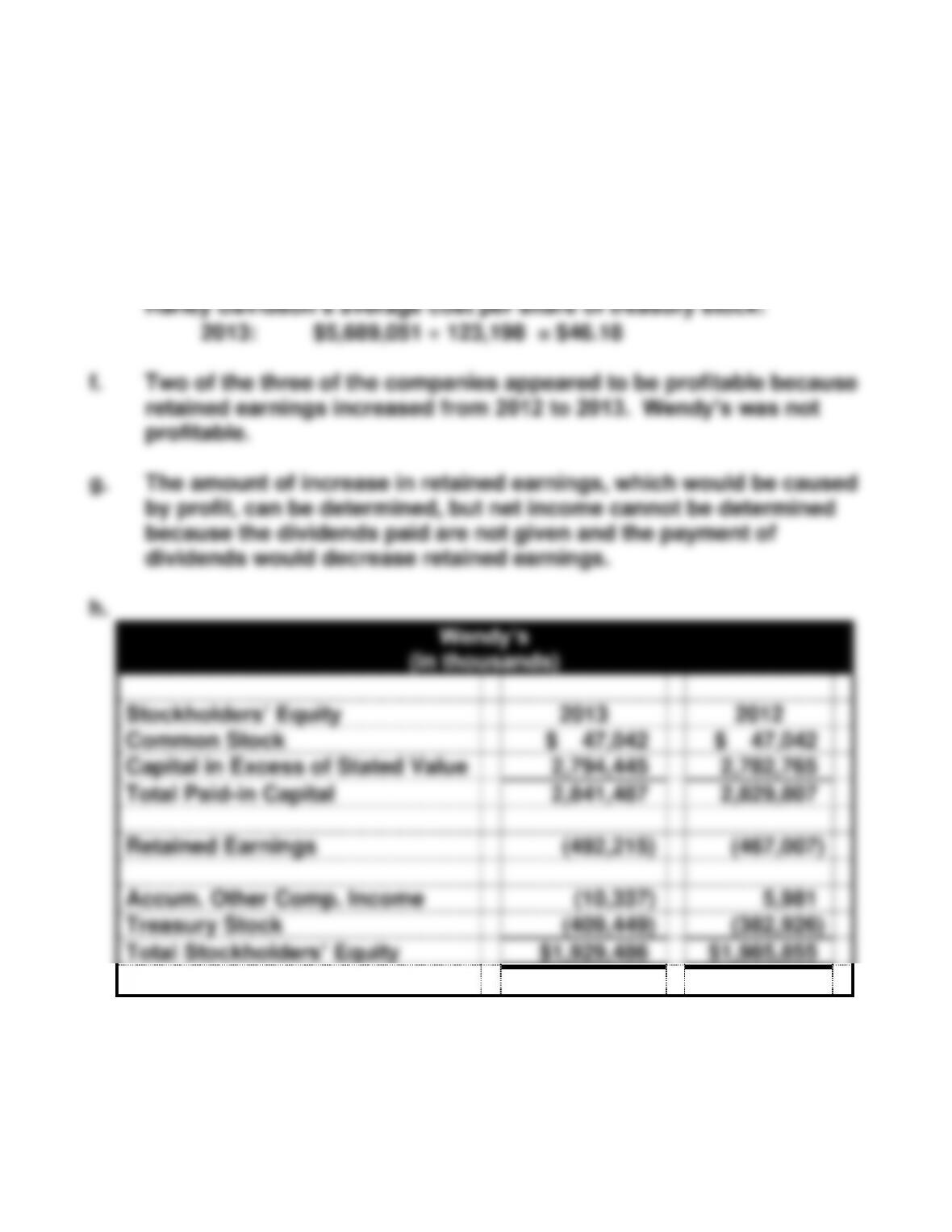

Except for per-share amounts, Wendy’s and Harley Davidson’s amounts

are in thousands, and Coca-cola amounts are in millions.

b. Wendy’s stated value per share:

$47,042 470,424 = $.10 per share

Coca-Cola par value per share:

ATC 11-2 (cont.)

e. Wendy’s average cost per share of treasury stock:

2013: $409,449 77,637 = $5.27

Coca-Cola’s average cost per share of treasury stock:

2013: $39,091 2,638 = $14.82

ATC 11-2 h. (cont.)

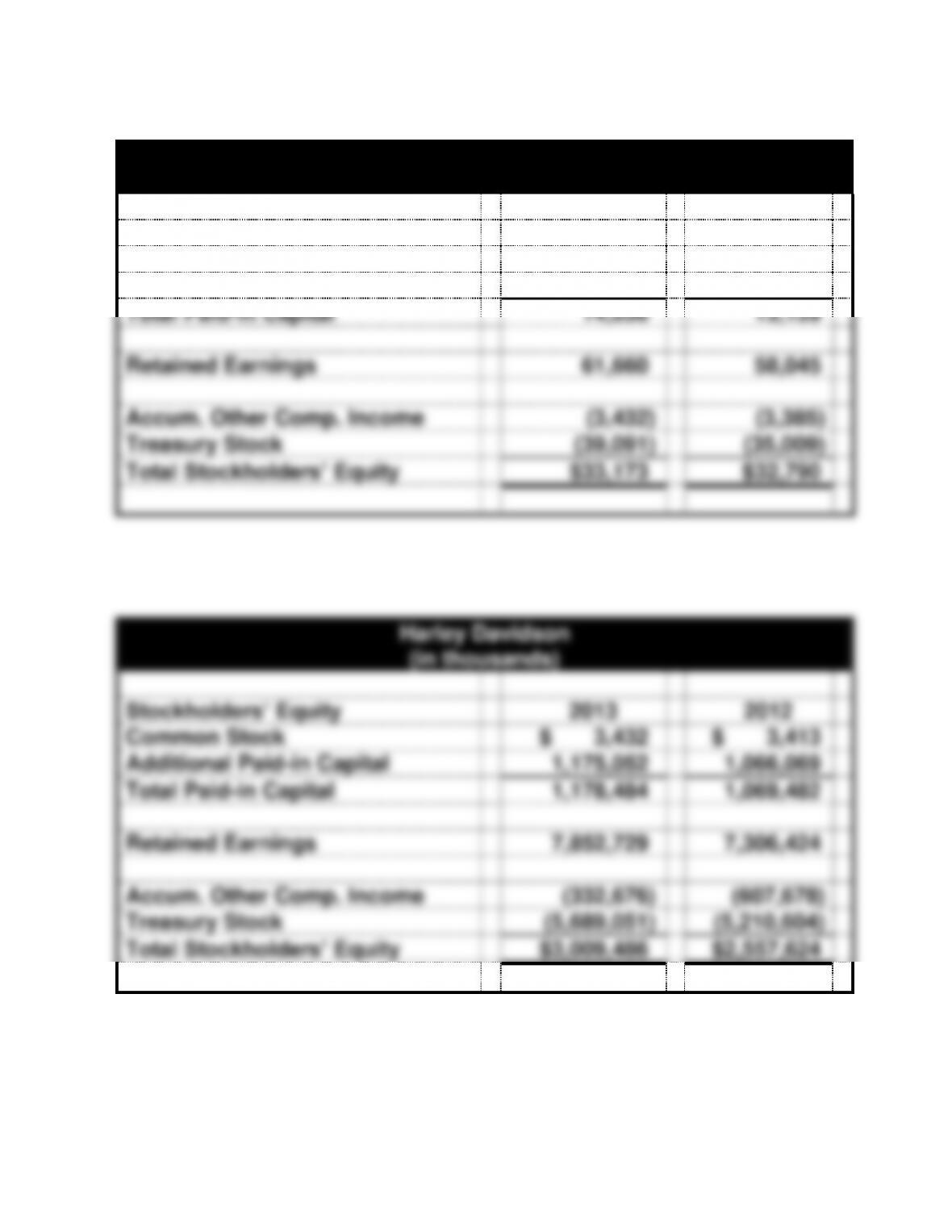

Cola-Cola

(in millions)

Stockholders’ Equity

2013

2012

Common Stock

$ 1,760

$ 1,760

Capital Surplus

12,276

11,379

Total Paid-in Capital

14,036

13,139

Retained Earnings

61,660

58,045

Accum. Other Comp. Income

(3,432)

(3,385)

Treasury Stock

(39,091)

(35,009)

Total Stockholders’ Equity

$33,173

$32,790

Stockholders’ Equity

2012

Common Stock

$ 3,432

$ 3,413

Additional Paid-in Capital

1,175,052

1,066,069

Total Paid-in Capital

1,178,484

1,069,482

Retained Earnings

7,852,729

7,306,424

Accum. Other Comp. Income

(332,676)

(607,678)

Treasury Stock

(5,689,051)

(5,210,604)

Total Stockholders’ Equity

$3,009,486

$2,557,624

11–61

ATC 11-3

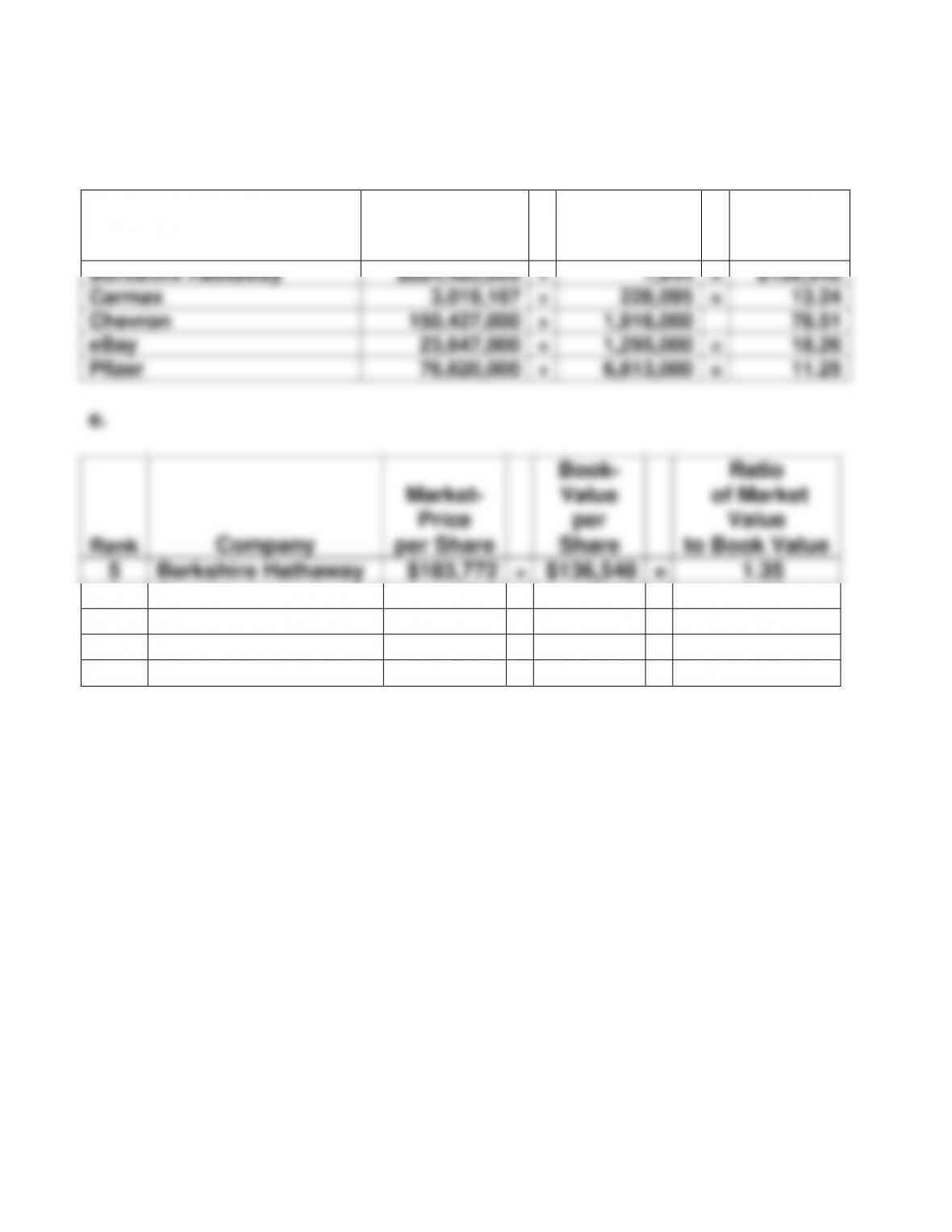

a.

Company

Net Earnings

Shares

Outstanding

EPS

Berkshire Hathaway

19,476,000

÷

1,644

=

11,847

Carmax

434,284

÷

228,095

=

1.90

Chevron

21,423,000

÷

1,916,000

=

11.18

eBay

2,856,000

÷

1,295,000

=

2.21

Pfizer

22,003,000

÷

6,813,000

=

3.23

b. and c.

Rank

Company

Market-

Price

per Share

EPS

P/E

Ratio

3

Berkshire Hathaway

$183,772

÷

11,847

=

15.5

2

Carmax

48.6

÷

1.90

=

25.6

4

Chevron

115.08

÷

11.18

=

10.3

1

eBay

59.06

2.21

=

26.7

5

Pfizer

32.43

÷

3.23

=

10.0

11–62

ATC 11-3 – (continued)

d.

Company

Stockholders’

Equity

Shares

Outstanding

Book–

Value per

Share

Berkshire Hathaway

$224,485,000

÷

1,644

=

$136,548

Carmax

3,019,167

÷

228,095

=

13.24

Chevron

150,427,000

÷

1,916,000

78.51

eBay

23,647,000

÷

1,295,000

=

18.26

Pfizer

76,620,000

÷

6,813,000

=

11.25

e.

Rank

Company

Market-

Price

per Share

Book-

Value

per

Share

Ratio

of Market

Value

to Book Value

5

Berkshire Hathaway

$183,772

÷

$136,548

=

1.35

1

Carmax

48.6

÷

13.24

=

3.67

4

Chevron

115.08

÷

78.51

=

1.47

2

eBay

59.06

÷

18.26

=

3.23

3

Pfizer

32.43

÷

11.25

=

2.88

11–63

ATC 11-4

Note: The stock price for the date two months after the end of the

company’s fiscal year was used because this about the time

the company’s audited financial statements and annual report

would be released to the public.

11–64

ATC 11-5

Note: The stock price for the date two months after the end of the

companies’ fiscal year was used because this was close to the

time the companies’ audited financial statements and annual

report would be released to the public.

11–65

ATC 11-6

Note to Instructor: The factors given below are only selected factors and

not meant to be all inclusive.

MEMO

TO: Jim and Scott

FROM: Sam Student

The advantages and disadvantages of the partnership and the corporate

11–66

Based on above information, I would recommend that the business be

11–67

ATC 11-7

a.

1. Converting to an accelerated method of depreciation would increase

expense on the income statement thereby decreasing net income

2. Increasing the receivables expected to be uncollectible would

increase the amount of bad debt expense on the income statement

3. Increasing the percentage of estimated warranty claims would

increase warranty expense in the current period. This action would

reduce net income and stockholders’ equity (i.e., retained earnings)

on the balance sheet. Other balance sheet accounts affected would

11–68

ATC 11-7 (cont.)

c. The managers of a company are hired to make decisions that are in

the best interest of the stockholders (the owners of the company).

They should make decisions that increase the value of stockholders’

equity, not decisions that increase their own personal worth.

11–69

ATC 11-8

This solution is based on the company’s From10-K for the fiscal year

ended September 29, 2013, and dollar amounts and total shares

outstanding are in millions.

1. The fair values of its assets, such as land, are higher than the

2. The “market” believes the company has goodwill that is not

3. The “market” believes the company has potential future

earnings power that is not reflected on its balance sheet under

11–70

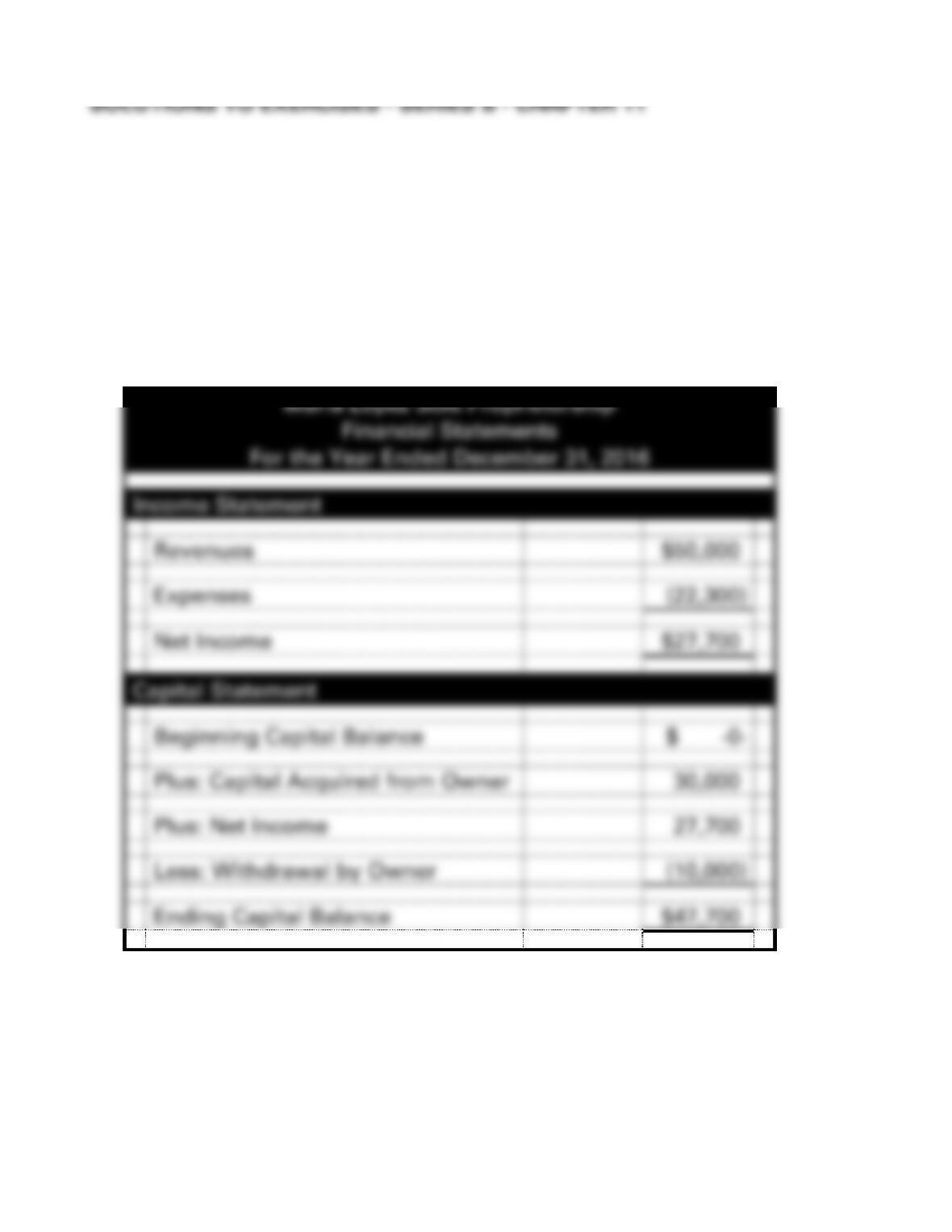

EXERCISE 11-1B

Transactions

Cash Acquired from Owner

$30,000

Revenues

50,000

Expenses

22,300

Withdrawals

10,000

Maria Lopez Sole Proprietorship

Financial Statements

For the Year Ended December 31, 2016

Income Statement

Revenues

$50,000

Expenses

(22,300)

Net Income

$27,700

Capital Statement

Beginning Capital Balance

$ -0-

Plus: Capital Acquired from Owner

30,000

Plus: Net Income

27,700

Less: Withdrawal by Owner

(10,000)

Ending Capital Balance

$47,700

11–71

EXERCISE 11-1B (cont.)

Maria Lopez Sole Proprietorship

Financial Statements

Balance Sheet

As of December 31, 2016

Assets

Cash

$47,700

Total Assets

$47,700

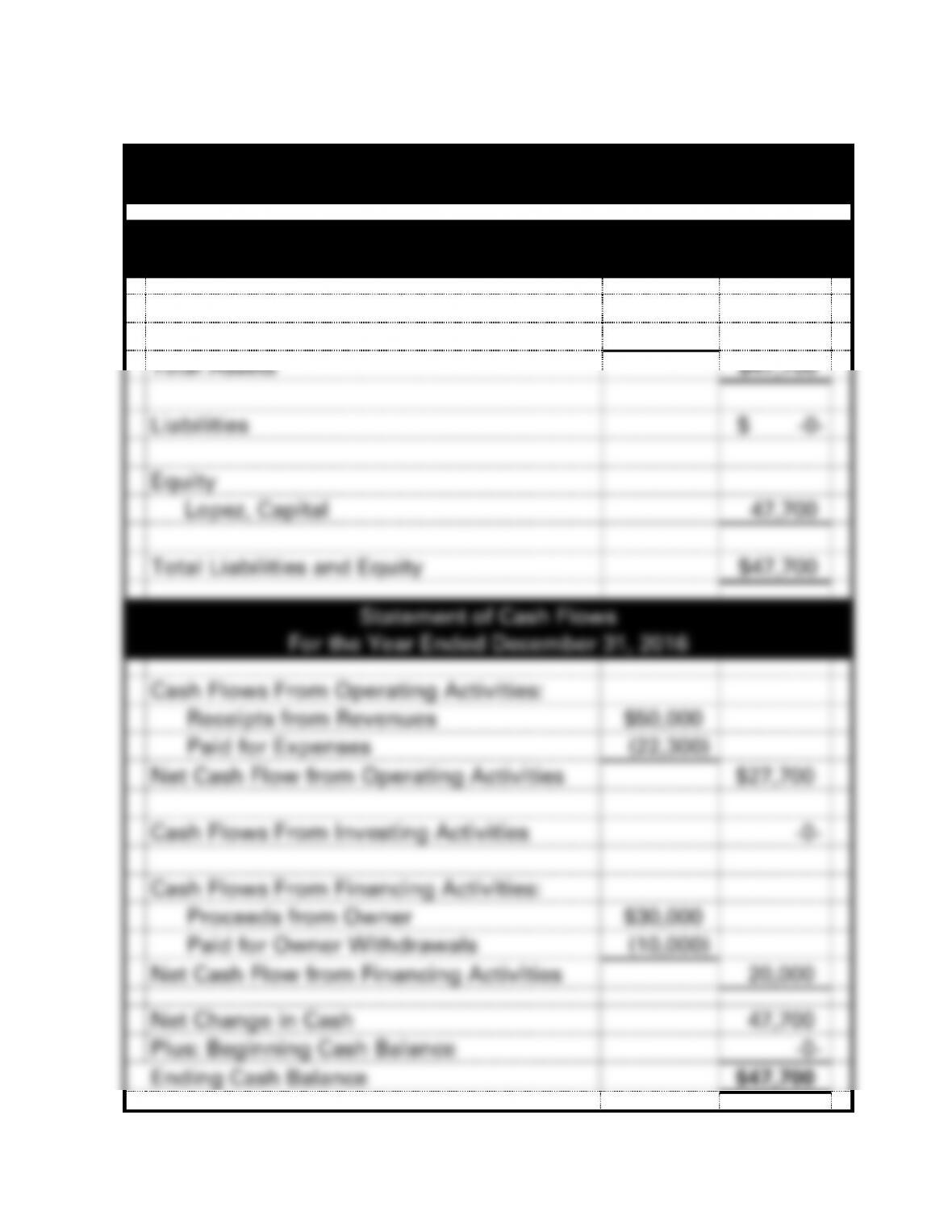

Liabilities

$ -0-

Equity

Lopez, Capital

47,700

Total Liabilities and Equity

$47,700

Statement of Cash Flows

For the Year Ended December 31, 2016

Cash Flows From Operating Activities:

Receipts from Revenues

$50,000

Paid for Expenses

(22,300)

Net Cash Flow from Operating Activities

$27,700

Cash Flows From Investing Activities

-0-

Cash Flows From Financing Activities:

Proceeds from Owner

$30,000

Paid for Owner Withdrawals

(10,000)

Net Cash Flow from Financing Activities

20,000

Net Change in Cash

47,700

Plus: Beginning Cash Balance

-0-

Ending Cash Balance

$47,700

EXERCISE 11-2B

Transactions:

Cash Contributions

D. Reed

$ 70,000

33.33%

J. Files

140,000

66.67%

Total

$210,000

100.00%

Revenues

$ 75,000

Expenses

39,000

Reed Withdrawal

2,000

Files Withdrawal

4,000

11–73

EXERCISE 11-2B (cont.)

Prepared for the instructor’s use:

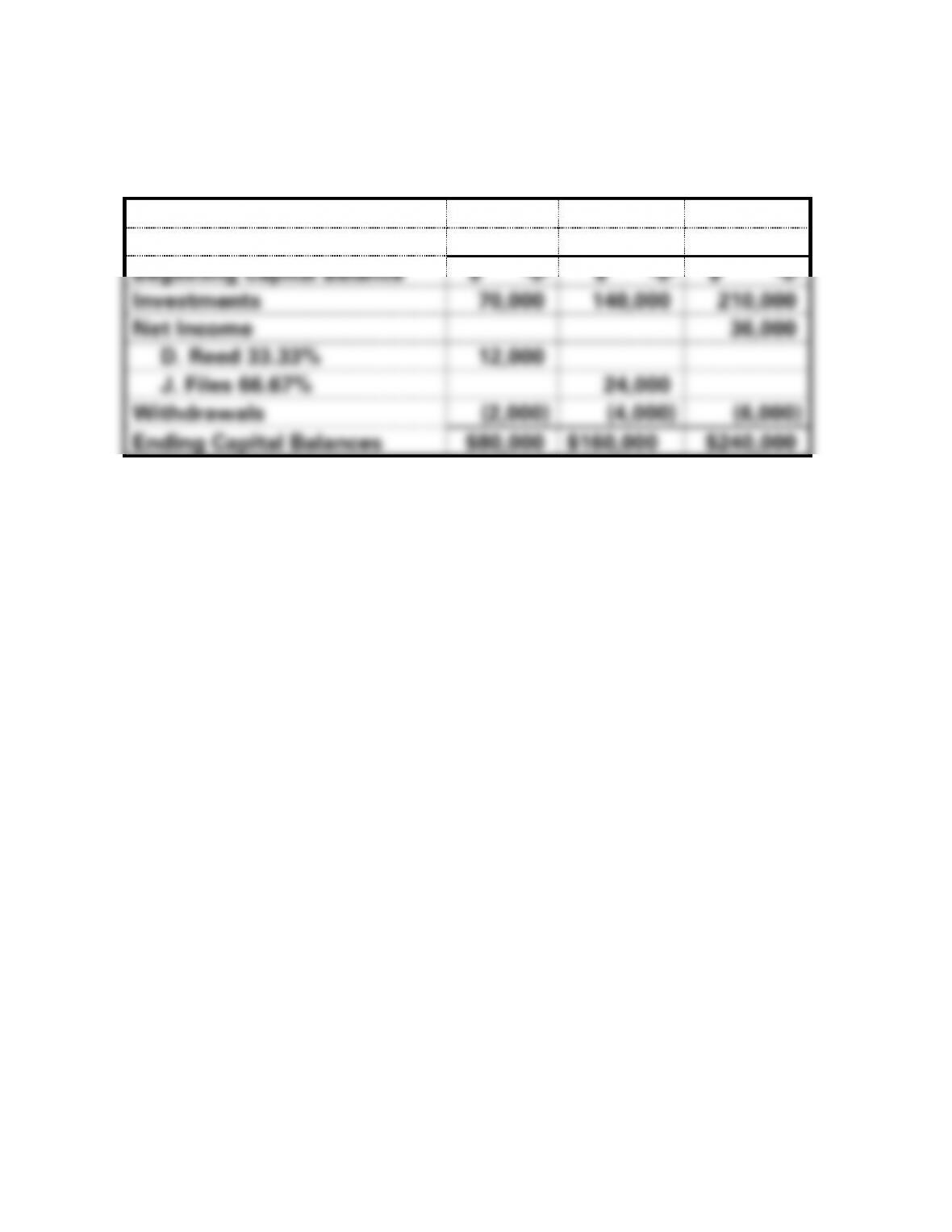

Analysis of Capital Accounts:

Reed

Files

Total

Beginning Capital Balance

$ -0-

$ -0-

$ -0-

Investments

70,000

140,000

210,000

Net Income

36,000

D. Reed 33.33%

12,000

J. Files 66.67%

24,000

Withdrawals

(2,000)

(4,000)

(6,000)

Ending Capital Balances

$80,000

$160,000

$240,000

11–74

EXERCISE 11-2B (cont.)

RF Partnership

Financial Statements

Balance Sheet

As of December 31, 2016

Assets

Cash

$240,000

Total Assets

$240,000

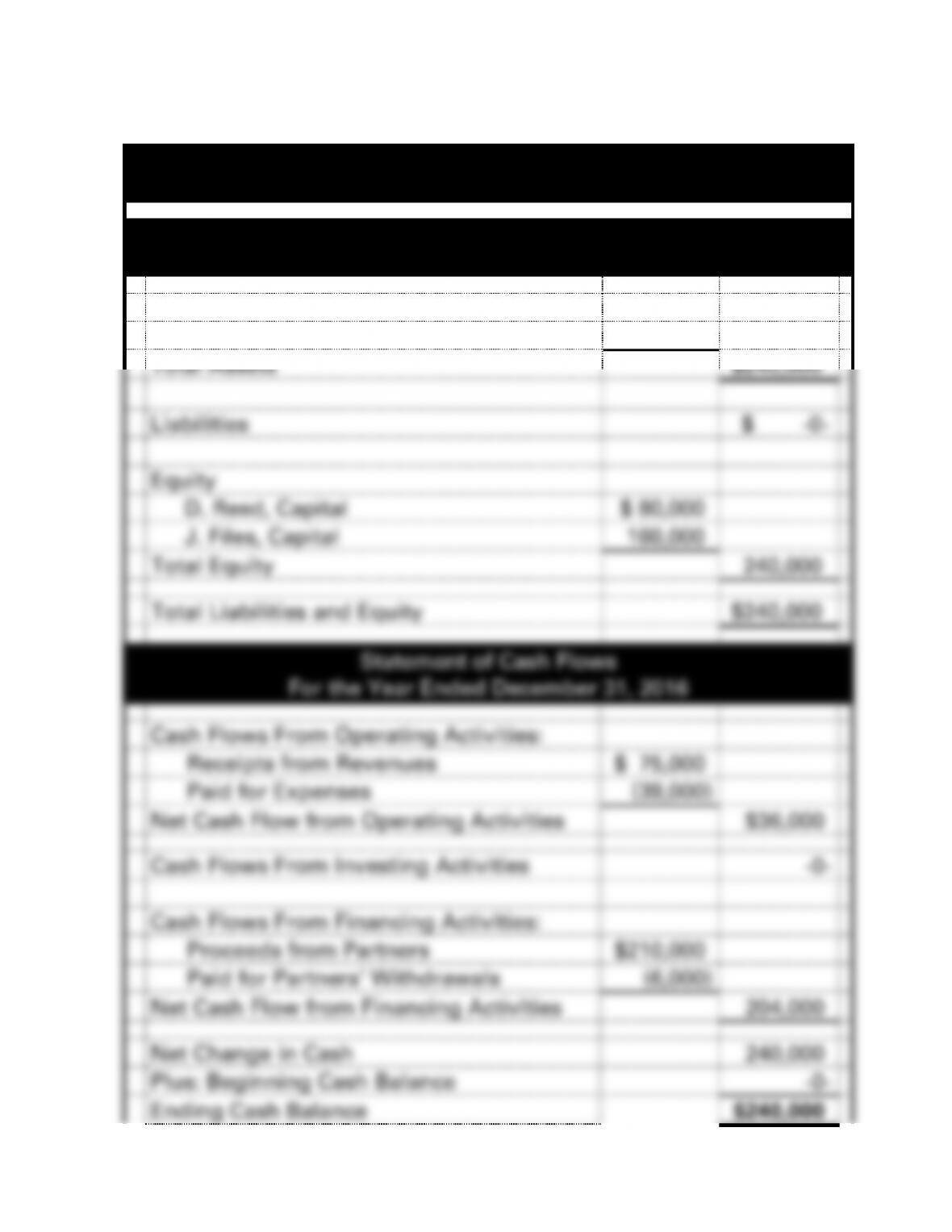

Liabilities

$ -0-

Equity

D. Reed, Capital

$ 80,000

J. Files, Capital

160,000

Total Equity

240,000

Total Liabilities and Equity

$240,000

Statement of Cash Flows

For the Year Ended December 31, 2016

Cash Flows From Operating Activities:

Receipts from Revenues

$ 75,000

Paid for Expenses

(39,000)

Net Cash Flow from Operating Activities

$36,000

Cash Flows From Investing Activities

-0-

Cash Flows From Financing Activities:

Proceeds from Partners

$210,000

Paid for Partners’ Withdrawals

(6,000)

Net Cash Flow from Financing Activities

204,000

Net Change in Cash

240,000

Plus: Beginning Cash Balance

-0-

Ending Cash Balance

$240,000

11–75

11–76

EXERCISE 11-3B

Transactions:

Issued 10,000 shares of $10 par stock @ $16

$160,000

Revenues

71,000

Expenses

46,500

Dividends Paid

5,000

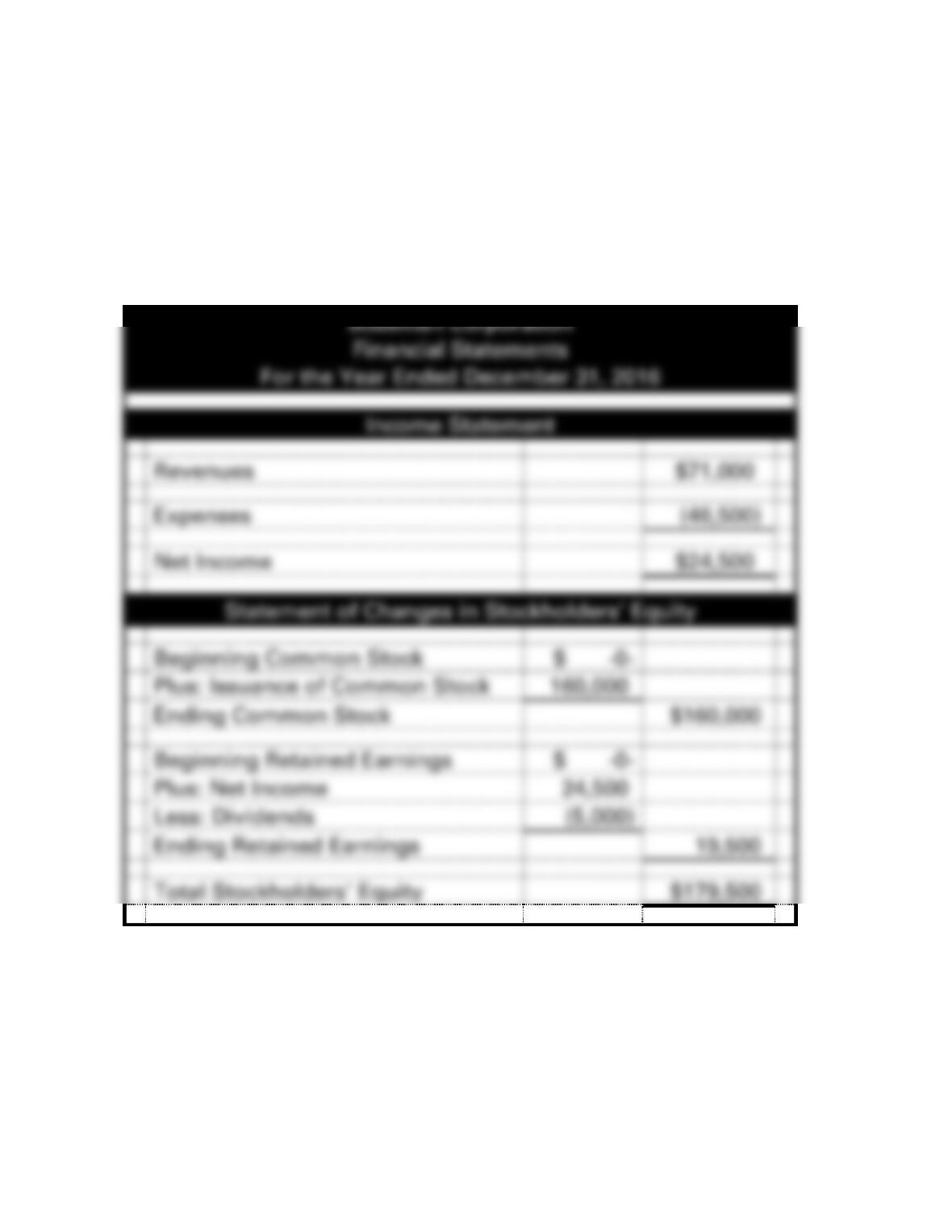

Bozeman Corporation

Financial Statements

For the Year Ended December 31, 2016

Income Statement

Revenues

$71,000

Expenses

(46,500)

Net Income

$24,500

Statement of Changes in Stockholders’ Equity

Beginning Common Stock

$ -0-

Plus: Issuance of Common Stock

160,000

Ending Common Stock

$160,000

Beginning Retained Earnings

$ -0-

Plus: Net Income

24,500

Less: Dividends

(5,000)

Ending Retained Earnings

19,500

Total Stockholders’ Equity

$179,500