Answers to Questions

1. Ratios and trends are useful tools for analyzing financial

statements because they give the analyst a basis for comparing

2. “Liquidity” is the short-term ability to convert assets to cash or

3. Horizontal analysis is a tool for comparing the behavior of items

4. This ratio provides information about how rapidly a company is

selling its inventory.

5. The current ratio presents the number of dollars of current assets

to each dollar of current liabilities. The quick ratio, by omitting the

6. Absolute amounts are often insufficient because companies are of

different sizes, thus have different levels of materiality. One

7. ROI is a measure of income as a percentage of the total capital

8. a) Debt to equity ratio: Total Liabilities

———————————————

9. Because earnings per share is a combination of “net income” and

“average shares outstanding,” problems in either part affect the

figures.

10. ROI: Net Income

———————

Total Assets

11. Information overload refers to a situation where users of

12. Price-earnings ratio = Market Price per Share

––––––––––––––––––––––––

Earnings per Share

13. Some environmental factors that should be considered are (1) the

14. Accounting principles are the major determinants of the methods

used to account for assets, liabilities, expenses, and revenues. In

Exercise 13-1A

a.

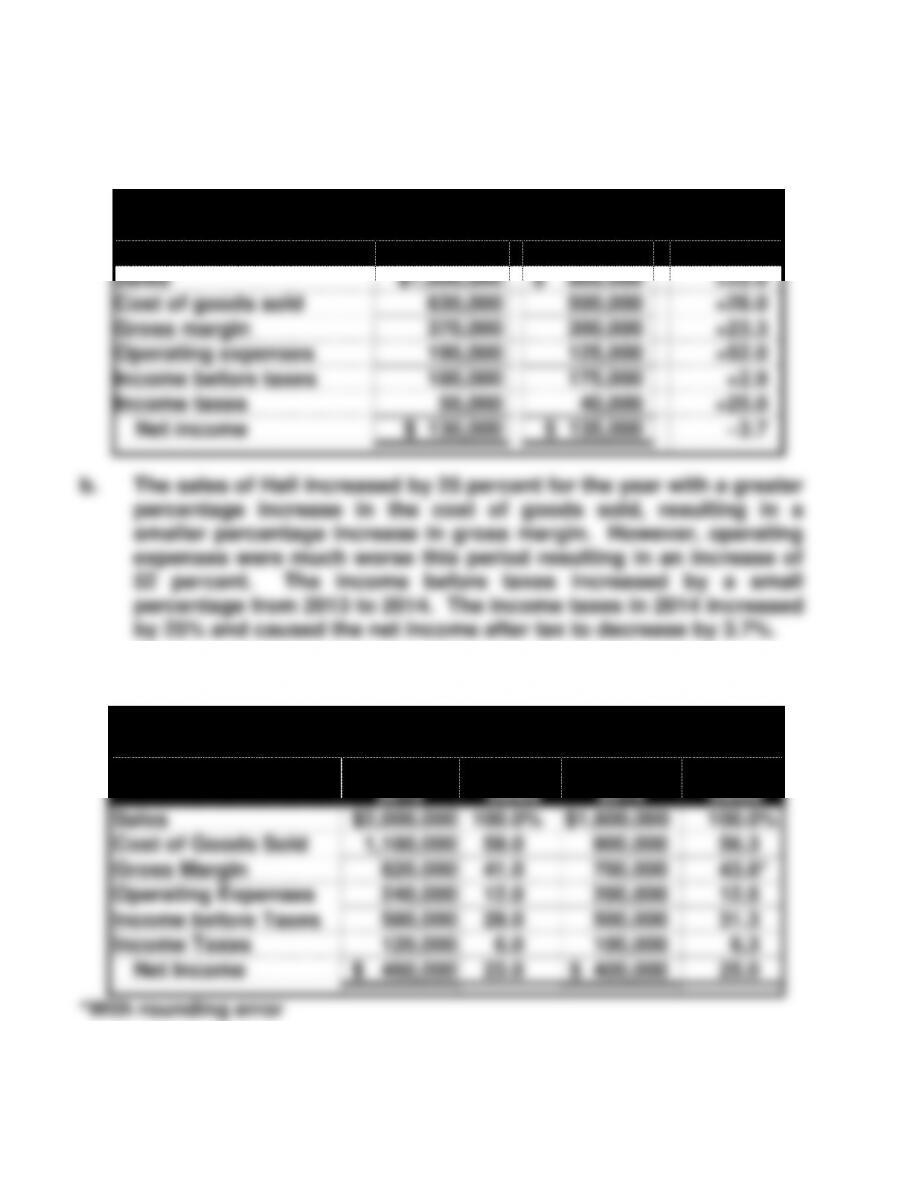

Hall Corporation

Income Statements

2014

2013

% Change

Sales

$1,000,000

$ 800,000

+25.0

Cost of goods sold

630,000

500,000

+26.0

Gross margin

370,000

300,000

+23.3

Operating expenses

190,000

125,000

+52.0

Income before taxes

180,000

175,000

+2.9

Income taxes

50,000

40,000

+25.0

Net income

$ 130,000

$ 135,000

–3.7

b. The sales of Hall increased by 25 percent for the year with a greater

percentage increase in the cost of goods sold, resulting in a

smaller percentage increase in gross margin. However, operating

expenses were much worse this period resulting in an increase of

52 percent. The income before taxes increased by a small

percentage from 2013 to 2014. The income taxes in 2014 increased

by 25% and caused the net income after tax to decrease by 3.7%.

Exercise 13-2A

Jordan Company

Vertical Analysis of Income Statements

2015

% of

Sales

2014

% of

Sales

Sales

$2,000,000

100.0%

$1,600,000

100.0%

Cost of Goods Sold

1,180,000

59.0

900,000

56.3

Gross Margin

820,000

41.0

700,000

43.8*

Operating Expenses

240,000

12.0

200,000

12.5

Income before Taxes

580,000

29.0

500,000

31.3

Income Taxes

120,000

6.0

100,000

6.3

Net Income

$ 460,000

23.0

$ 400,000

25.0

*With rounding error

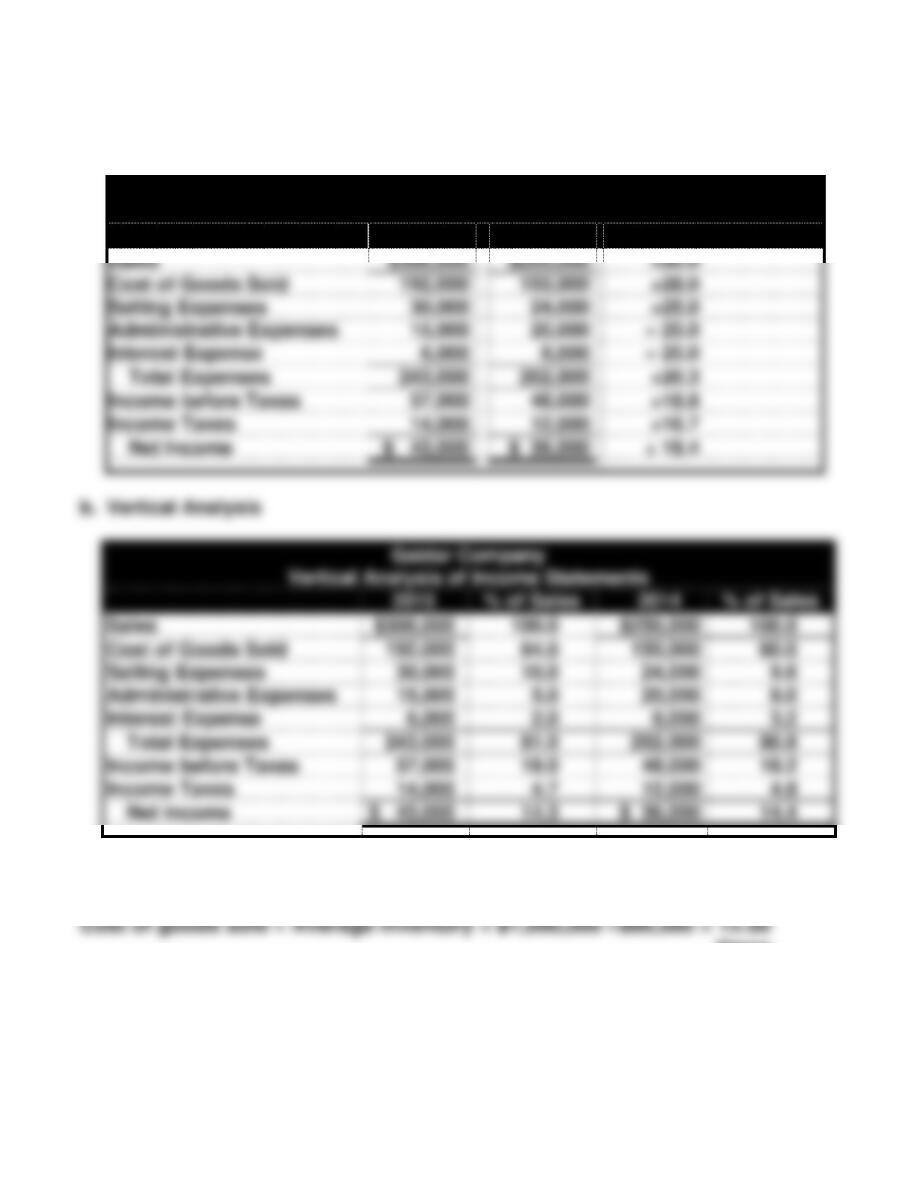

Exercise 13-3A

a. Horizontal Analysis

Gaidar Company

Horizontal Analysis of Income Statements

2015

2014

% Change over 2014

Sales

$300,000

$250,000

+20.0

Cost of Goods Sold

192,000

150,000

+28.0

Selling Expenses

30,000

24,000

+25.0

Administrative Expenses

15,000

20,000

– 25.0

Interest Expense

6,000

8,000

– 25.0

Total Expenses

243,000

202,000

+20.3

Income before Taxes

57,000

48,000

+18.8

Income Taxes

14,000

12,000

+16.7

Net Income

$ 43,000

$ 36,000

+ 19.4

b. Vertical Analysis

Gaidar Company

Vertical Analysis of Income Statements

2015

% of Sales

2014

% of Sales

Sales

$300,000

100.0

$250,000

100.0

Cost of Goods Sold

192,000

64.0

150,000

60.0

Selling Expenses

30,000

10.0

24,000

9.6

Administrative Expenses

15,000

5.0

20,000

8.0

Interest Expense

6,000

2.0

8,000

3.2

Total Expenses

243,000

81.0

202,000

80.8

Income before Taxes

57,000

19.0

48,000

19.2

Income Taxes

14,000

4.7

12,000

4.8

Net Income

$ 43,000

14.3

$ 36,000

14.4

Exercise 13-4A

times

Exercise 13-5A

When an account is written off, the net realizable value of accounts

Exercise 13-6A

a. Working capital before the transaction:

Current assets – Current liabilities

Exercise 13-7A

a. Working capital before the transaction:

Exercise 13-8A

Working capital = Current assets – Current liabilities

= $300,000 – $200,000 = $100,000

Exercise 13-9A

a. Current assets = $432,000 – $294,000 = $138,000

L = 0.8 SE

0.8 SE + SE = $432,000

1.8 SE = $432,000

SE = $240,000

But, CS = $300,000

Exercise 13-10A

Income before interest and taxes:

Exercise 13-11A

a. Net credit sales Average net receivables =

Exercise 13-12A

a. Earnings per share:

(Net income – Preferred dividend) ÷ Avg. O/S common shares

Exercise 13-13A

a. Current ratio: $77,000 ÷ $15,000 = 5.13:1

b. Earnings per share: $20,000 ÷ 880 = $22.73 per share

Exercise 13-14A

1. c 7. d

2. l 8. h

3. g 9. j

4. k 10. e

5. i 11. a

6. b 12. f

Exercise 13-15A

Current

Ratio

Working

Capital

Stockholders’

Equity

Book

Value

Retained

Earnings

a.

NC

NC

NC

NC

NC

b.

NC

NC

NC

NC

NC

c.

+

+

NC

NC

NC

d.

–

NC

NC

NC

NC

e.

–

–

–

–

–

f.

+

+

+*

+

+

g.

NC

NC

NC

–

–

h.

+

NC

NC

NC

NC

i.

+

+

–**

–

–

Problem 13-16A

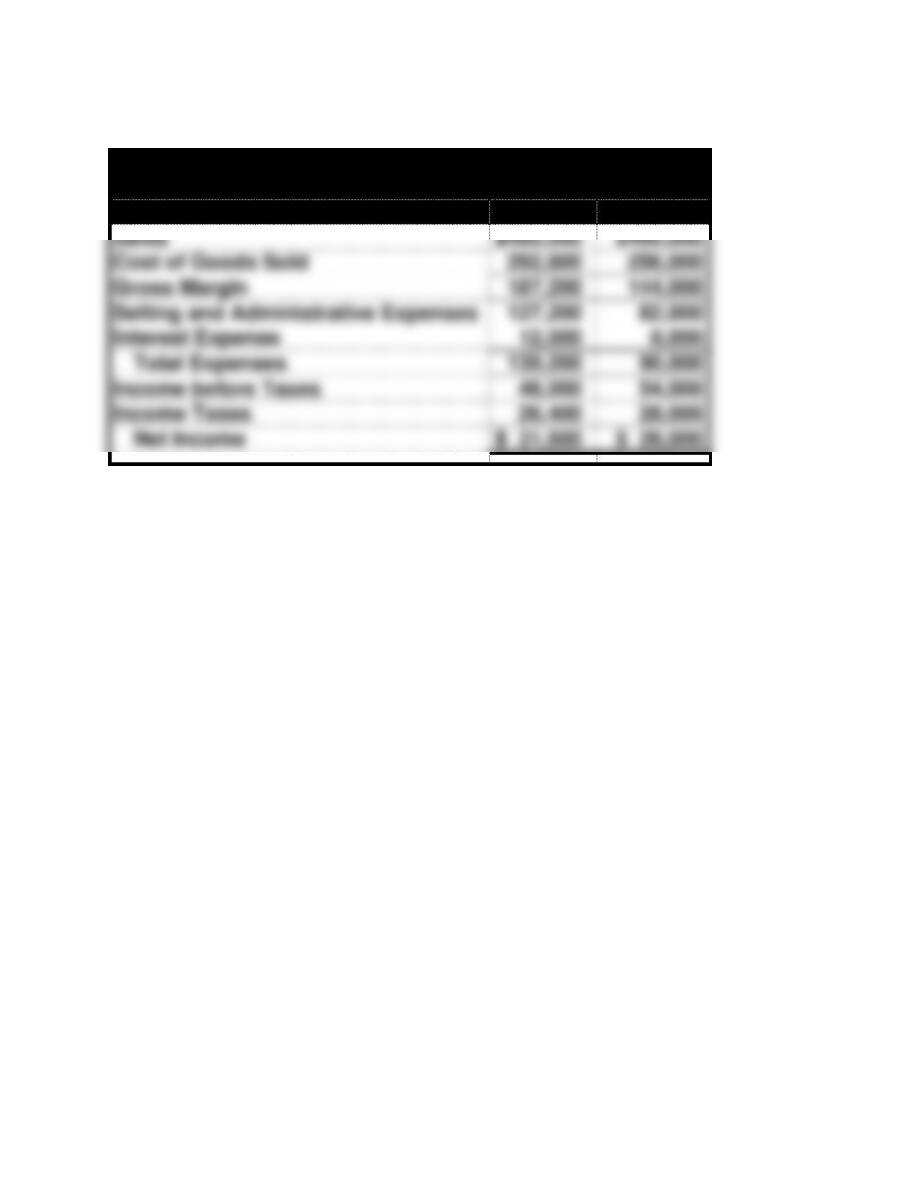

Safin Company

Income Statements

2015

2014

Sales

$480,000

$400,000

Cost of Goods Sold

292,800

256,000

Gross Margin

187,200

144,000

Selling and Administrative Expenses

127,200

82,000

Interest Expense

12,000

8,000

Total Expenses

139,200

90,000

Income before Taxes

48,000

54,000

Income Taxes

26,400

28,000

Net Income

$ 21,600

$ 26,000

Problem 13-17A

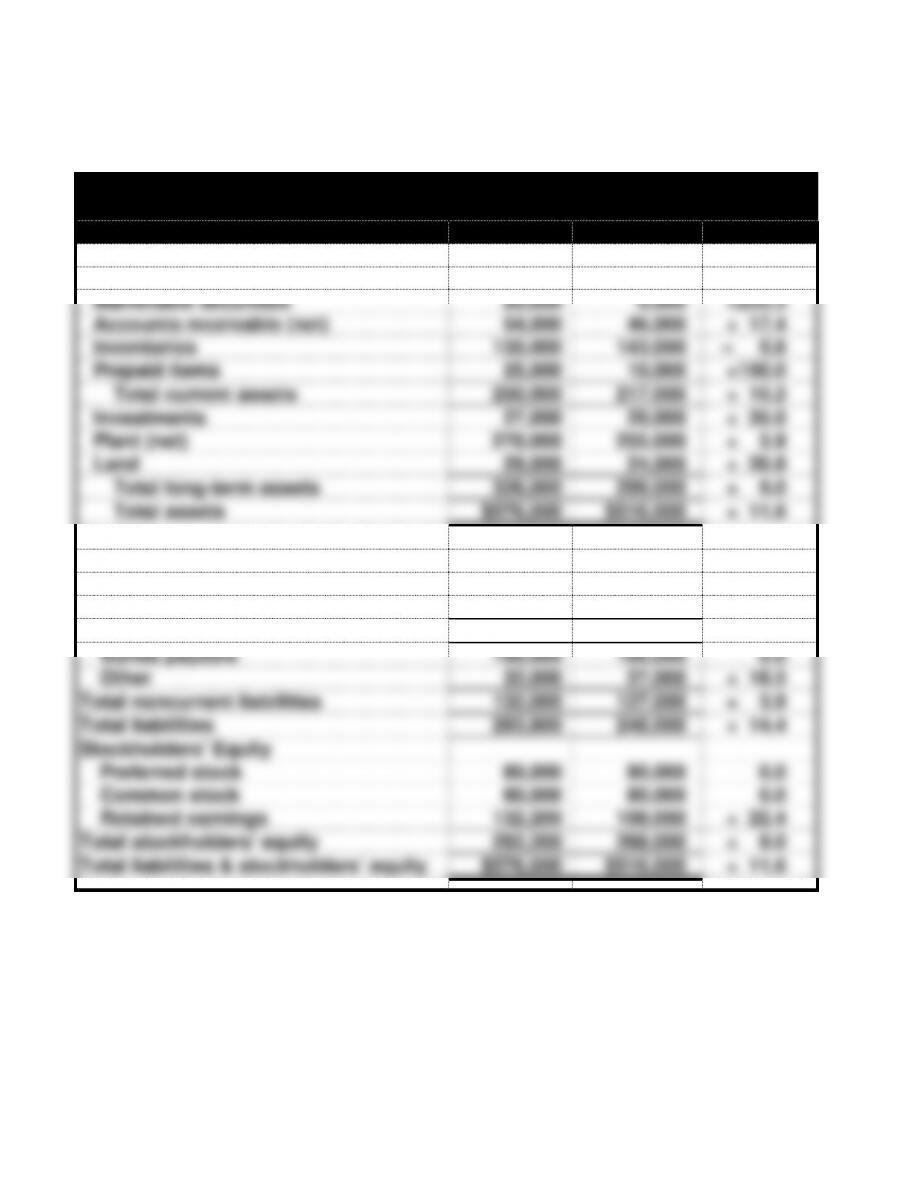

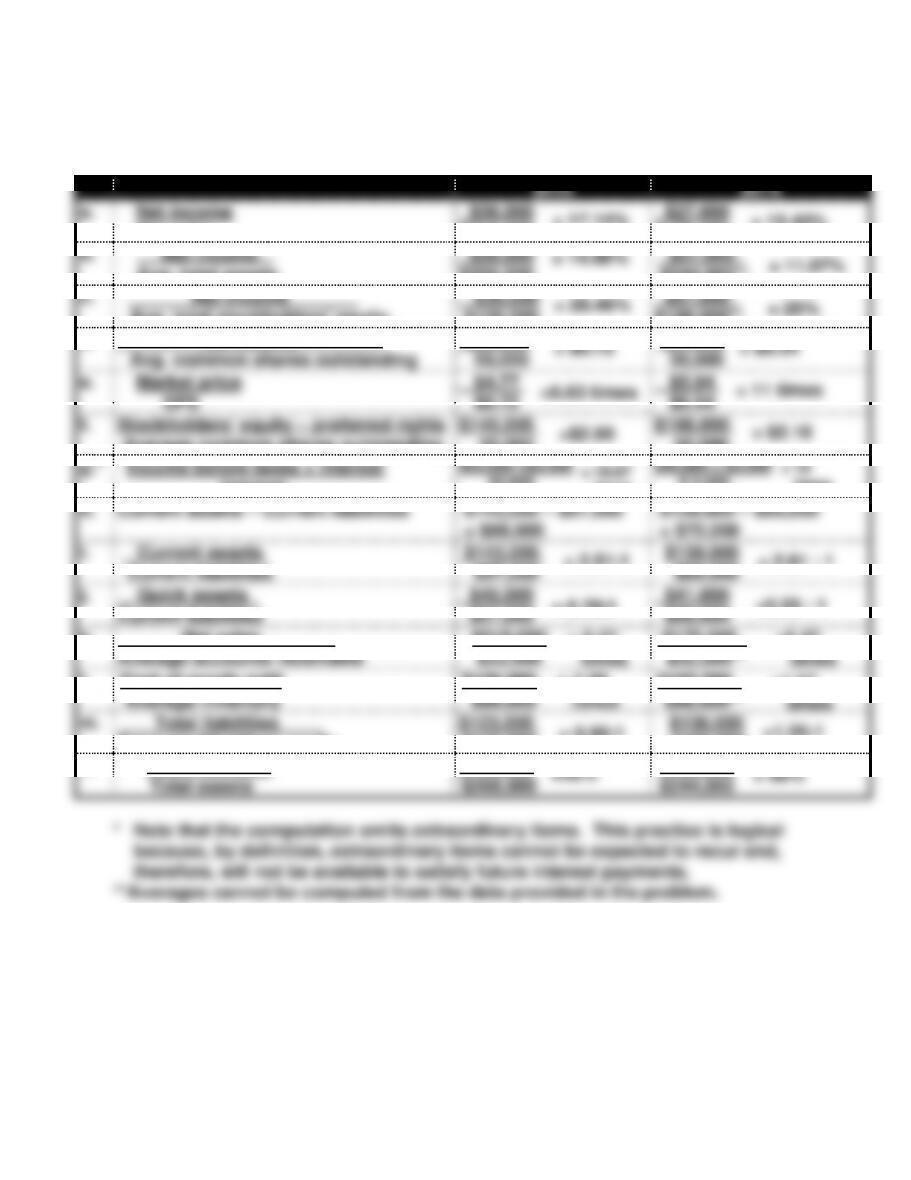

Revnik Company

Horizontal Analysis of Balance Sheets

2015

2014

% Change

Assets

Cash

$ 16,000

$ 12,000

+ 33.3%

Marketable securities

20,000

6,000

+233.3

Accounts receivable (net)

54,000

46,000

+ 17.4

Inventories

135,000

143,000

– 5.6

Prepaid items

25,000

10,000

+150.0

Total current assets

250,000

217,000

+ 15.2

Investments

27,000

20,000

+ 35.0

Plant (net)

270,000

255,000

+ 5.9

Land

29,000

24,000

+ 20.8

Total long-term assets

326,000

299,000

+ 9.0

Total assets

$576,000

$516,000

+ 11.6

Liabilities

Notes payable

$ 17,000

$ 6,000

+183.3

Accounts payable

113,800

100,000

+ 13.8

Salaries payable

21,000

15,000

+ 40.0

Total current liabilities

151,800

121,000

+ 25.5

Bonds payable

100,000

100,000

0.0

Other

32,000

27,000

+ 18.5

Total noncurrent liabilities

132,000

127,000

+ 3.9

Total liabilities

283,800

248,000

+ 14.4

Stockholders’ Equity

Preferred stock

80,000

80,000

0.0

Common stock

80,000

80,000

0.0

Retained earnings

132,200

108,000

+ 22.4

Total stockholders’ equity

292,200

268,000

+ 9.0

Total liabilities & stockholders’ equity

$576,000

$516,000

+ 11.6

Problem 13-17A (continued)

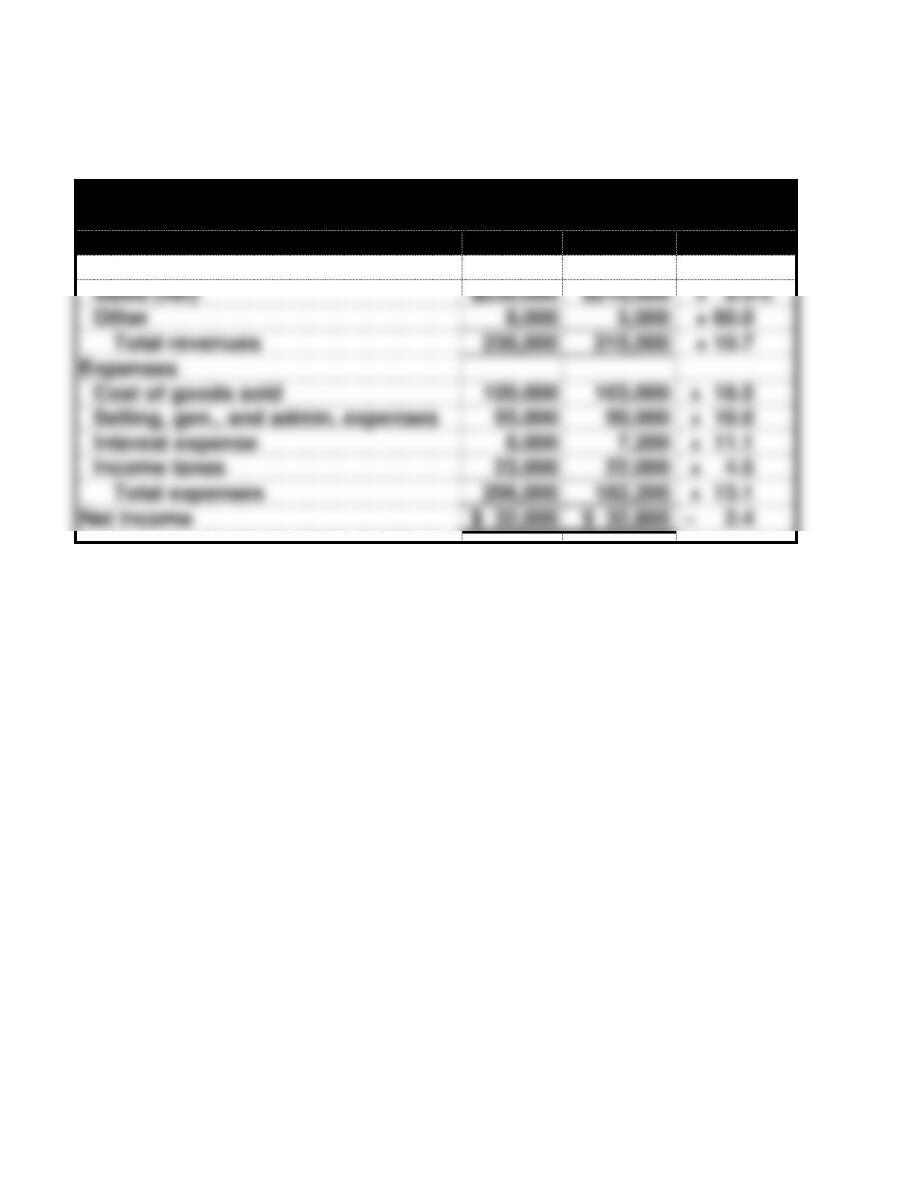

Revnik Company

Horizontal Analysis of Income Statements

2015

2014

% Change

Revenues

Sales (net)

$230,000

$210,000

+ 9.5%

Other

8,000

5,000

+ 60.0

Total revenues

238,000

215,000

+ 10.7

Expenses

Cost of goods sold

120,000

103,000

+ 16.5

Selling, gen., and admin. expenses

55,000

50,000

+ 10.0

Interest expense

8,000

7,200

+ 11.1

Income taxes

23,000

22,000

+ 4.5

Total expenses

206,000

182,200

+ 13.1

Net income

$ 32,000

$ 32,800

– 2.4

13-1

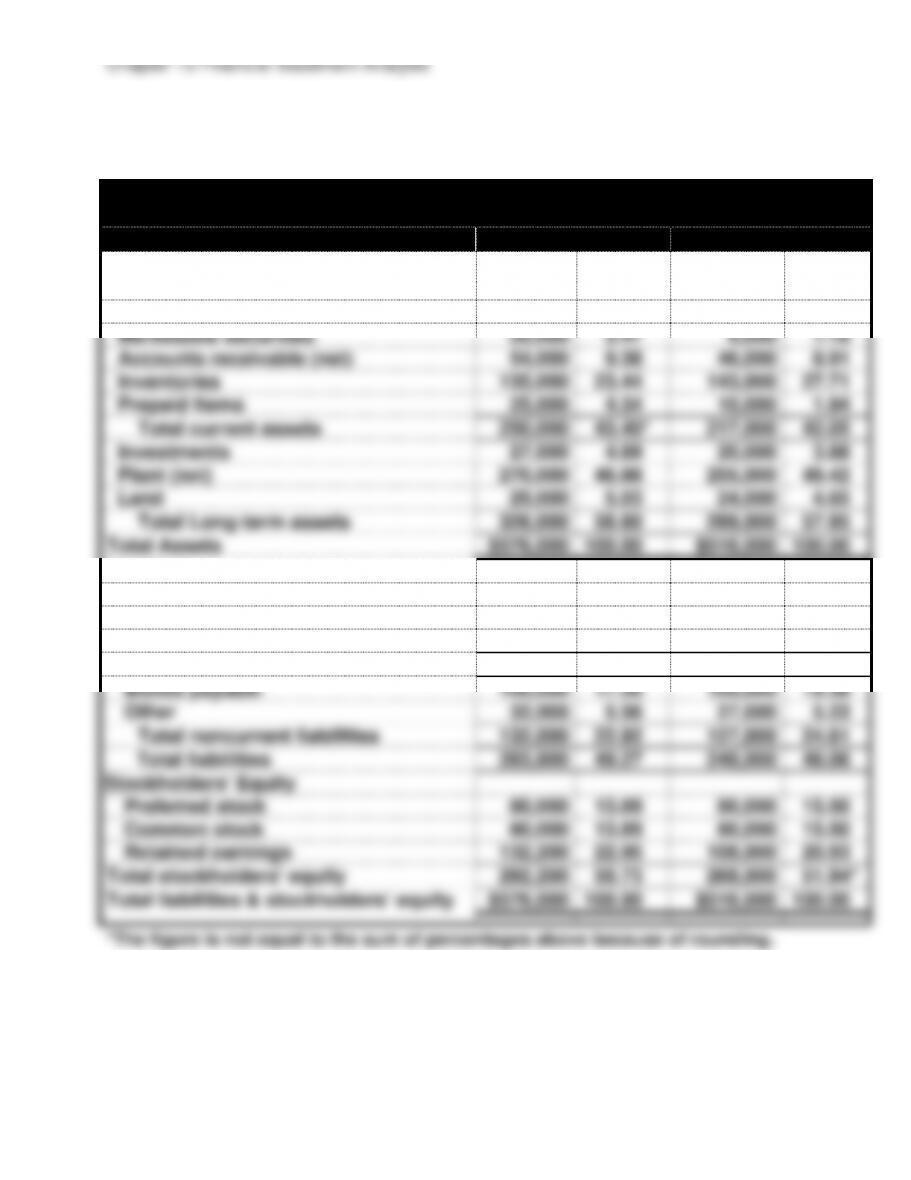

Problem 13-18A

Revnik Company

Vertical Analysis of Balance Sheets

2015

2014

Assets

Amount

% of

Total

Amount

% of

Total

Cash

$ 16,000

2.78%

$ 12,000

2.33%

Marketable securities

20,000

3.47

6,000

1.16

Accounts receivable (net)

54,000

9.38

46,000

8.91

Inventories

135,000

23.44

143,000

27.71

Prepaid Items

25,000

4.34

10,000

1.94

Total current assets

250,000

43.40*

217,000

42.05

Investments

27,000

4.69

20,000

3.88

Plant (net)

270,000

46.88

255,000

49.42

Land

29,000

5.03

24,000

4.65

Total Long-term assets

326,000

56.60

299,000

57.95

Total Assets

$576,000

100.00

$516,000

100.00

Liabilities

Notes payable

$ 17,000

2.95

$ 6,000

1.16

Accounts payable

113,800

19.76

100,000

19.38

Salaries payable

21,000

3.65

15,000

2.91

Total current liabilities

151,800

26.35*

121,000

23.45

Bonds payable

100,000

17.36

100,000

19.38

Other

32,000

5.56

27,000

5.23

Total noncurrent liabilities

132,000

22.92

127,000

24.61

Total liabilities

283,800

49.27

248,000

48.06

Stockholders’ Equity

Preferred stock

80,000

13.89

80,000

15.50

Common stock

80,000

13.89

80,000

15.50

Retained earnings

132,200

22.95

108,000

20.93

Total stockholders’ equity

292,200

50.73

268,000

51.94*

Total liabilities & stockholders’ equity

$576,000

100.00

$516,000

100.00

*The figure is not equal to the sum of percentages above because of rounding.

13-2

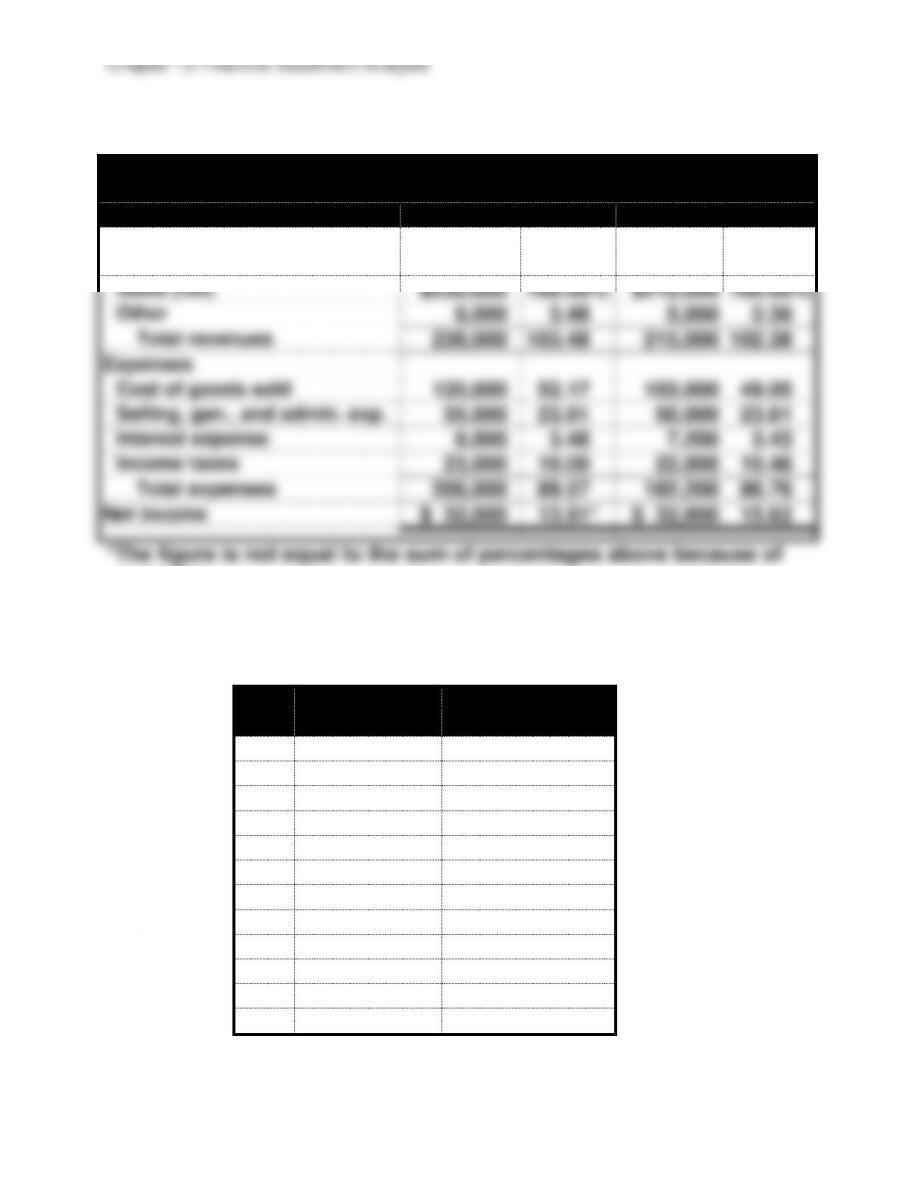

Problem 13-18A (continued)

Revnik Company

Vertical Analysis of Income Statements

2015

2014

Revenues

Amount

% of

Total

Amount

% of

Total

Sales (net)

$230,000

100.00%

$210,000

100.00%

Other

8,000

3.48

5,000

2.38

Total revenues

238,000

103.48

215,000

102.38

Expenses

Cost of goods sold

120,000

52.17

103,000

49.05

Selling, gen., and admin. exp.

55,000

23.91

50,000

23.81

Interest expense

8,000

3.48

7,200

3.43

Income taxes

23,000

10.00

22,000

10.48

Total expenses

206,000

89.57

182,200

86.76

Net income

$ 32,000

13.91*

$ 32,800

15.62

*The figure is not equal to the sum of percentages above because of

rounding.

Problem 13-19A

Current

Ratio

Working

Capital

a.

–

–

b.

NA

NA

c.

+

+

d.

+

+

e.

–

–

f.

–

NA

g.

NA

NA

h.

NA

NA

i.

NA

NA

j.

+

NA

k.

NA

NA

l.

NA

NA

Chapter 13 Financial Statement Analysis

13-3

Problem 13-20A

A. $111,000 F. $195,000

B. $255,000 G. $270,000

C. $498,000 H. $195,000

13-4

Problem 13-21A

a. Earnings per share:

$195,600 – $22,800*

———————————— = $4 per share

5

13-5

Problem 13-22A

a. Times interest earned

2013: $98,000 ÷ $8,000 = 12.25 times

2014: $120,000 ÷ $9,000 = 13.33 times

= 30.00%

e. Net margin:

6

13-6

Problem 13-23A

2015

2014

a.

Net income

Net sales

$36,000

$210,000

$27,000

$175,000

b.

Net income

Avg. total assets

$36,000

$256,000

$27,000

$244,000**

c.

Net income

Avg. total stockholders’ equity

$36,000

$126,500

$27,000

$108,000**

d.

Net income

Avg. common shares outstanding

$36,000

50,000

$27,000

50,000

e.

Market price

EPS

$4.77

$0.72

$5.94

$0.54

f.

Stockholders’ equity – preferred rights

Average common shares outstanding

$145,000

50,000

$108,000

50,000

g.*

Income before taxes + Interest

Interest

$53,000*+$3,000

$3,000

$45,000 + $3,000

$ 3,000

h.

Current assets – Current liabilities

$143,000 – $57,000

= $86,000

$139,000 – $69,000

= $70,000

i.

Current assets

Current liabilities

$143,000

$57,000

$139,000

$69,000

j.

Quick assets

Current liabilities

$40,000

$57,000

$41,000

$69,000

k.

Net sales

Average accounts receivable

$210,000

$33,500

$175,000

$32,000**

l.

Cost of goods sold

Average inventory

$126,000

$98,000

$103,000

$96,000**

m.

Total liabilities

Total stockholders’ equity

$123,000

$145,000

$136,000

$108,000

n.

Total liabilities

Total assets

$123,000

$268,000

$136,000

$244,000

= 17.14%

= 15.43%

= 28.46%

= 11.07%

= 14.06%

= 25%

= $0.72

= $0.54

=6.63 times

= 11 times

=$2.90

= $2.16

= 18.67

times

= 16

times

= 2.51:1

= 2.01 : 1

= 0.70:1

=0.59 : 1

= 6.27

times

=5.47

times

= 1.29

times

=1.07

times

= 0.85:1

=1.26:1

=46%

= 56%

7

13-7

Problem 13-24A

Because of space limitation, $ signs are omitted in these computations.

2015

2014

a.

Current assets – Current liabilities

250,000 – 151,800 = 98,200

217,000 – 121,000 = 96,000

b.

Current assets ÷ Current liabilities

250,000 ÷ 151,800 = 1.65 : 1

217,000 ÷ 121,000 = 1.79 : 1

c.

Quick assets ÷ Current liabilities

90,000 ÷ 151,800 = 0.59 : 1

64,000 ÷ 121,000 = 0.53 : 1

d.

Net sales ÷ Average accounts receivables

230,000 ÷ 50,000 = 4.60 times

210,000 ÷ 46,500 = 4.52 times

e.

365 ÷ Turnover (d.)

365 ÷ 4.60 = 79 days

365 ÷ 4.52 =81 days

f.

Cost of goods sold ÷ Avg. inventory

120,000 ÷ 139,000 = 0.86 times

103,000 ÷ 141,500 = 0.73 times

g.

365 ÷ Turnover (f.)

365 ÷ 0.86 = 424 days

365 ÷ 0.73 = 500 days

h.

Total liabilities ÷ Total assets

283,800 ÷ 576,000 = 49%

248,000÷516,000 = 48%

i.

Total liabilities ÷ Total stockholders’ equity

283,800 ÷ 292,200 = 0.97:1

248,000÷268,000 = 0.93:1

j.

(Income before interest + taxes)

Interest

(55,000 + 8,000) ÷ 8,000

= 7.88 times

(54,800 + 7,200) ÷ 7,200

= 8.61 times

k.

Plant assets ÷ Long-term debt

270,000 ÷ 132,000 = 2.05:1

255,000 ÷ 127,000 = 2.01 : 1

l.

Net income ÷ Net sales

32,000 ÷ 230,000 = 13.91%

32,800 ÷ 210,000 = 15.62%

m.

Net sales ÷ Avg. total assets

230,000 ÷ 546,000 = 0.42

210,000 ÷ 516,000 = 0.41*

n.

Net income ÷ Avg. total assets

OR (l.) x (m.)

32,000 ÷ 546,000 = 5.86%

32,800 ÷ 516,000 = 6.36%*

o.

Net income ÷ Avg. stockholders’ equity

32,000 ÷ 280,100 = 11.42%

32,800 ÷ 268,000 = 12.24%*

p.

Net income – Preferred dividend

Avg. common shares outstanding

(32,000 – 3,200) ÷ 10,000

= $2.88 per share

(32,800 – 3,200) ÷ 10,000

= $2.96 per Share

q.

Stockholders’ equity – Preferred rights

Avg. common shares outstanding

(292,200 – 80,000) ÷ 10,000

= $21.22 per Share

(268,000 – 80,000) ÷ 10,000

= $18.80 per Share

r.

Market price ÷ EPS

12.50 ÷ 2.88 = 4.34

11.75 ÷ 2.96 = 3.97

s.

Dividends per share ÷ Market price

0.46 ÷ 12.50 = 3.68 %

0.46 ÷11.75 = 3.91%

8

13-8

Exercise 13-1B

a.

Dyer Corporation

Income Statements

2015

2014

% Change

Sales

$275,000

$250,000

+10.0

Cost of Goods Sold

163,800

156,000

+5.0

Gross Margin

111,200

94,000

+18.3

Operating Expenses

43,700

38,000

+15.0

Income Before Taxes

67,500

56,000

+20.5

Income Taxes

17,000

12,000

+41.7

Net Income

$ 50,500

$ 44,000

+14.8

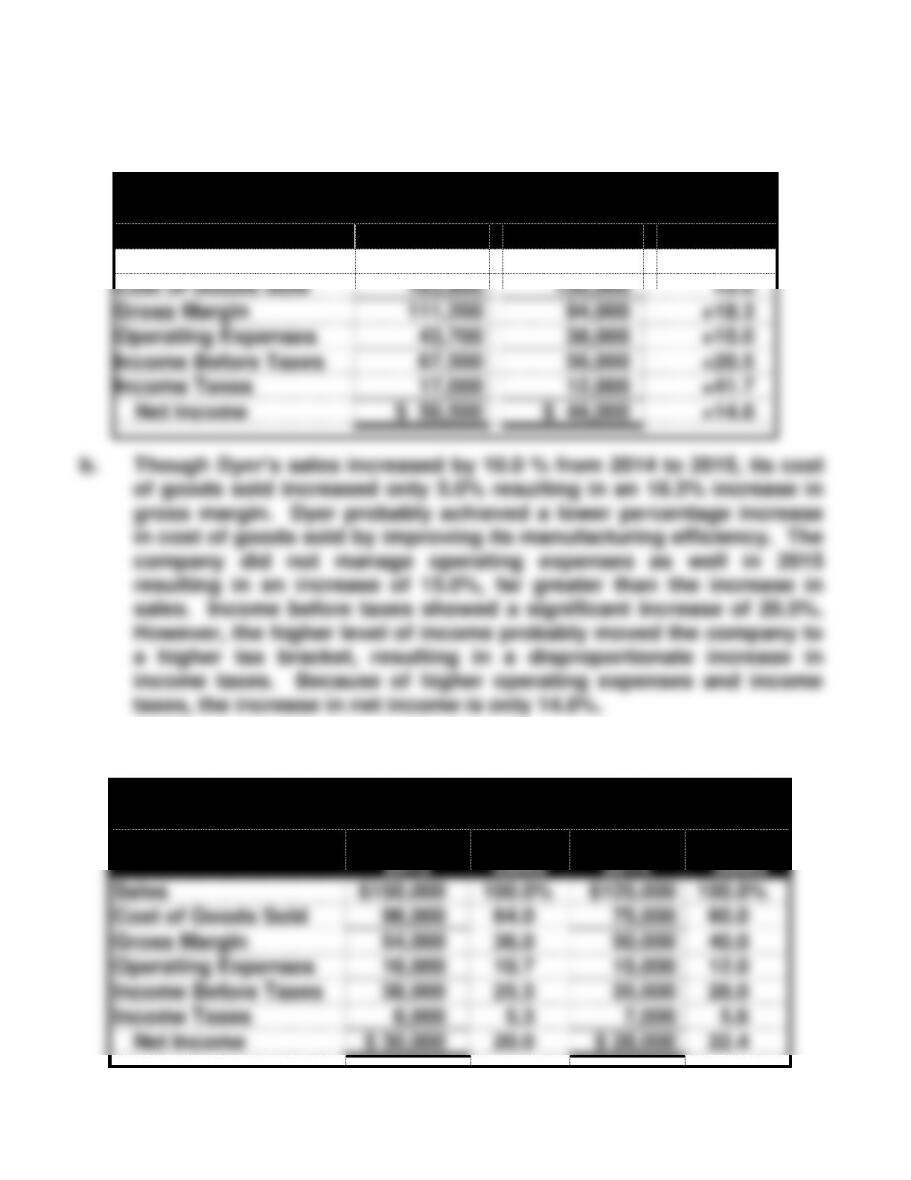

b. Though Dyer’s sales increased by 10.0 % from 2014 to 2015, its cost

of goods sold increased only 5.0% resulting in an 18.3% increase in

gross margin. Dyer probably achieved a lower percentage increase

in cost of goods sold by improving its manufacturing efficiency. The

company did not manage operating expenses as well in 2015

resulting in an increase of 15.0%, far greater than the increase in

sales. Income before taxes showed a significant increase of 20.5%.

However, the higher level of income probably moved the company to

a higher tax bracket, resulting in a disproportionate increase in

income taxes. Because of higher operating expenses and income

taxes, the increase in net income is only 14.8%.

Exercise 13-2B

Jarrett Company

Vertical Analysis of Income Statements

2015

% of

Sales

2014

% of

Sales

Sales

$150,000

100.0%

$125,000

100.0%

Cost of Goods Sold

96,000

64.0

75,000

60.0

Gross Margin

54,000

36.0

50,000

40.0

Operating Expenses

16,000

10.7

15,000

12.0

Income Before Taxes

38,000

25.3

35,000

28.0

Income Taxes

8,000

5.3

7,000

5.6

Net Income

$ 30,000

20.0

$ 28,000

22.4