3-1

Chapter 3

The Double-Entry Accounting System

General Comments for Chapter 3

Chapter 3 introduces recording procedures at a level designed to serve students who plan to

major in accounting as well as those who do not. Although advances in computer technology

have reduced the importance of recording procedures, debit and credit terminology continues

to be used in everyday business practice. Banks issue debit and credit cards. Customers are

told that their accounts have been debited or credited. Most medium– to large-size businesses

account for transactions using double-entry accounting with debits and credits. Therefore,

general business students as well as accounting majors need exposure to double-entry termi-

nology.

The traditional approach introduces technical terminology too early and in too much depth.

We believe you will find the two previous chapters have provided your students a back-

ground that facilitates their ability to master recording procedures. In other words, teaching

debits and credits should be easier under the concepts approach.

This text does omit many of the more detailed topics found in traditional texts. For example,

it does not include worksheets, special journals, and posting references. It does not use an

income summary account. The revenue, expense, and dividends accounts are closed directly

to retained earnings. Accounting majors will see these topics in their intermediate course,

and other business majors do not need the procedural detail. The text provides appropriate

background without overburdening detail.

Detailed Outline of a Lesson Plan for Chapter 3

I. Begin by introducing T-accounts. Observe that using columns of pluses and minuses

becomes increasingly unmanageable as the number of transactions increases. Introduce

the T-account as a means of simplifying the recording of events. Draw a large T on the

board and then write the accounting equation such that the ‘=’ sign is over the vertical

part of the T with ‘Assets’ on the left side and ‘Claims’ on the right side of the ‘=’ sign.

This will help students understand that Assets balances are typically on the left side of

the T account and Claims balances – Liabilities and Equity are on the right side of the T

account. Next, draw a T-account on the board and write the word assets across the hor-

izontal bar. Reference the initial T account with the accounting equation and suggest

that for assets we record increases on the left side of the T and decreases on the right

side. Then complete the accounting equation by drawing T-accounts for liabilities and

equity and suggest that increases for liability and equity accounts are recorded on the

right side of the T and decreases on the left side. Add the terms debit and credit as the

3-2

last part of your presentation. You may find it useful to demonstrate recording several

transactions in T-accounts before introducing debit and credit terminology. The terms

seem easier to digest if students first have time to grasp the plus and minus recording

scheme. Also, students might remember credits more readily by linking credit termi-

nology to the fact that creditors (including investors) are the ones that lay claims to the

assets of a company.

The treatment of pluses and minuses for expense and dividend accounts is particularly

important. Should you describe a debit to an expense account as a plus or a minus?

The debit is in fact both. Debits increase the expense but the expense decreases equity.

The plus or minus impact depends on whether the reference point is the expense or the

equity interest. The reference point you choose can make a big difference in how easily

students learn debit and credit terminology. If you use equity as the reference point, the

plus and minus scheme for the expense accounts is consistent with the other equity ac-

counts. On the claims side of the accounting equation, all debits are minuses and all

credits are pluses. If you use the expense account as the reference point, then the plus

and minus signs in the expense account are the reverse of the other equity accounts.

Since consistent patterns are easier to learn than inconsistent patterns, referencing the

equity account may work better than referencing the expense account. Furthermore,

referencing the equity account is consistent with the horizontal statements model used

throughout the text. The text uses the following pattern of plus and minus signs for

debit and credit terminology.

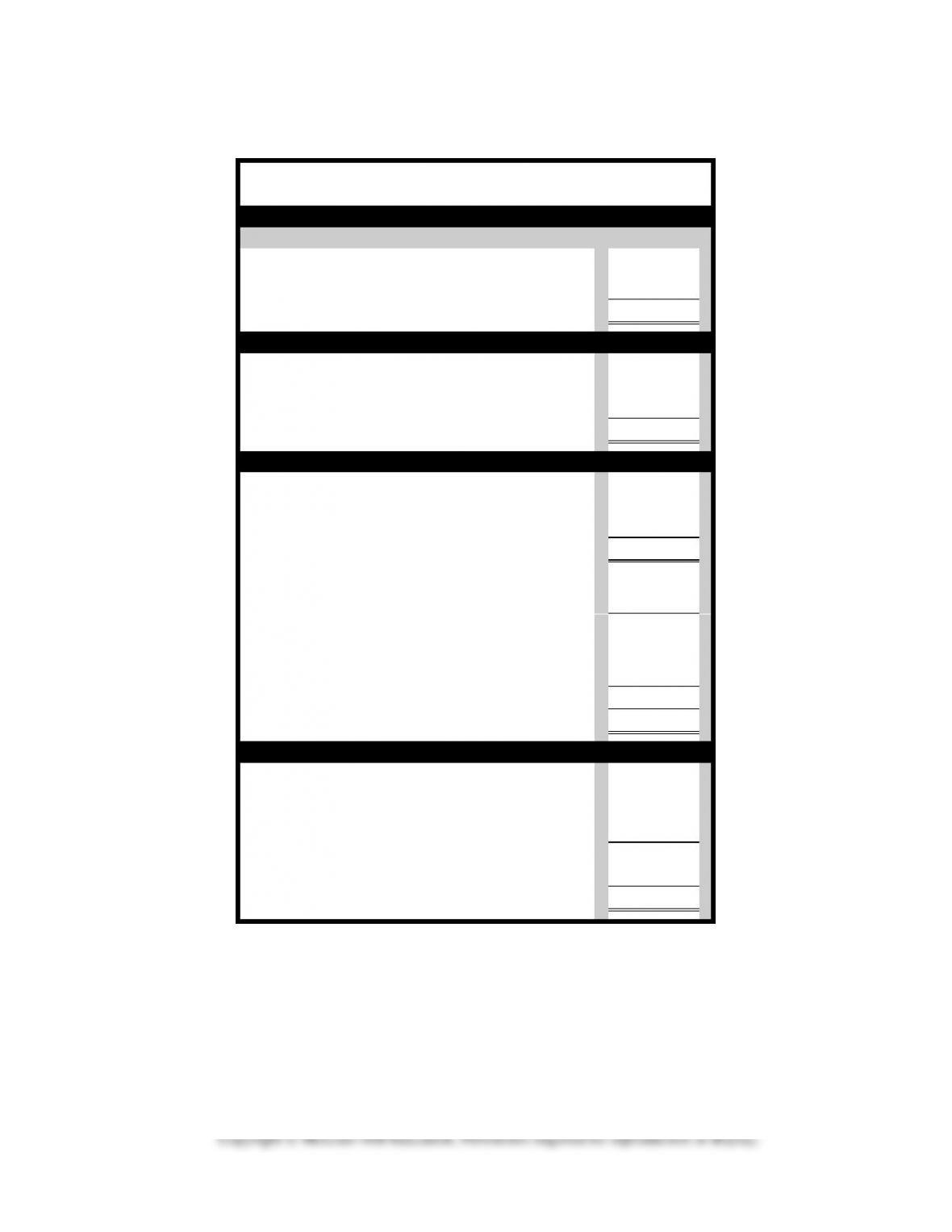

Illustration 1

Debit and Credit Relationships

Assets

=

Liabilities

+

Equity

Debit

Credit

Debit

Credit

Debit

Credit

+

–

–

+

–

+

Common Stock

Debit

Credit

–

+

Dividends

Debit

Credit

– Equity

+ Equity

+ Div.

– Div.

Revenue

Debit

Credit

– Equity

+ Equity

-Revenue

+Revenue

Expense

Debit

Credit

– Equity

+ Equity

+ Exp.

– Exp.

II. Immediately after introducing the plus and minus structure in T-account form,

give the students a demonstration problem that requires them to record several

events in T-accounts. Include accrual and deferral events in this problem so you can

also introduce other topics such as unadjusted and adjusted trial balances. We work

Demonstration Problem 3-1 step by step, encouraging students to work along with us.

For example, ask students to record each transaction in T-accounts before providing

them with the answer. After recording all the transactions, show the students how to

prepare an unadjusted trial balance. Next, ask the students to record the adjusting en-

tries and to prepare an adjusted trial balance. Then provide the answers so students can

check their work. Instruct the faster students to use the information in the adjusted trial

balance to prepare a set of financial statements. Finally, have the students prepare clos-

ing entries and a post-closing trial balance.

Keep the students actively involved. Let the problem drive your comments and sugges-

tions. For example, after introducing the trial balance, ask students what would happen

if a debit were incorrectly recorded in accounts receivable instead of cash. Would the

trial balance still balance? Point out that equal totals in a trial balance is evidence ra-

ther than proof of accuracy. Similarly, after preparing the post-closing trial balance,

you may ask the students: would real-world companies prepare only three trial balanc-

es during the year? How often should a trial balance be prepared? Questions such as

these help you emphasize that a trial balance is a method of checking debit and credit

balances. It is prepared whenever the accountant wants to check the accuracy of the re-

cording process. Most businesses prepare a trial balance at least daily. The “ask–

before-you-tell approach” keeps students actively involved. You can introduce points

such as those discussed above whenever it seems appropriate. Remember to use this

outline as a guide. Make every attempt to personalize your lesson plans.

III. After students have grasped debit and credit terminology, introduce journalizing.

Explain that the journal is a book of original entry. Note that the journal can take many

different forms. Today, electronic scanners, keyboards, and computer disks are more

3-4

ly, have them close the revenue account to retained earnings and prepare a post-closing

trial balance. Using a single event focuses attention on the steps in the accounting cy-

cle. Students do not become so involved in transaction data that they lose sight of the

sequence of events in an accounting cycle. Students should occasionally be required to

work through a problem without the benefit of workpapers. This exercise provides an

ideal opportunity to bypass using workpapers. The solution is simple and the need for

workpapers is minimal. Therefore, we have not provided solutions and workpapers for

this example.

V. Use the horizontal financial statements model to demonstrate the effects of busi-

ness events on financial statements as you deem appropriate. Use the horizontal fi-

nancial statements model in conjunction with recording procedures. For example, dis-

cuss accounting events in the following sequence. First, demonstrate how the business

event affects the financial statements by recording it in a horizontal financial statements

model. Next, show how to record the event with T-accounts or a general journal entry.

To reinforce the relationship between recording procedures and financial statement ef-

fects, you can write a journal entry on the board and have the students record the effects

of the journal entry in the horizontal financial statements model. For example:

XYZ Company experienced an accounting event that was recorded in its general jour-

nal as follows:

Cash

xxx

Accounts Receivable

xxx

Use a horizontal financial statements model to how this event would affect the company’s finan-

cial statements.

Assets

=

Liab.

+

Equity

Rev.

–

Exp.

=

Net Inc.

Cash Flow

+ Ä

NA

NA

NA

NA

NA

+ OA

VI. Time considerations and homework assignments. Spend approximately one hour

introducing recording procedures. You should have time to complete Demonstration

Problem 3-1 step by step while students work along with you. You should also have

time to introduce the general journal recording format and get started on Demonstration

Problem 3-2. If you do not have time to complete this problem in class, assign the re-

mainder as homework. You need not spend an enormous amount of time covering re-

cording procedures in class because the subject is not conceptually complex. Mastering

recording procedures requires drill which homework assignments can provide. If you

have any additional classroom time, consider the enrichment exercise described below.

If you want your students to get a good grasp of debit and credit terminology, assign a

generous supply of homework exercises and problems. Mastery requires considerable

practice. Exercises 3-5A or B, 3-14 A or B, and 3-19A or B are good for drill. Prob-

lems 3-33A or B and 3-32 A or B require using recording procedures for a complete

accounting cycle.

3-5

VII. Enrichment. We highly recommend that you use ATC Case 4-7 as an in-class assign-

ment. It is a comprehensive case that requires students to consider what information to

include in financial statements and to examine the limitations of accounting information

in decision-making. The case is set in medieval times and uses numbers of sheep as the

common unit of measure. Students have fun and learn accounting in the process. You

can work the case step by step. Start by drawing an accounting equation for each

brother. Record the first event (acquiring capital from the father) for the students, then

ask them to proceed on their own. After allowing students ample time to record the

events under the accounting equation, provide a solution to use as a guide for preparing

financial statements. Be accepting of student suggestions and observe that there is

more than one right answer. Explain, though, that useful results require consensus re-

garding measuring and recording transactions in order to produce comparable financial

statements. Next, have students prepare financial statements, then provide a solution so

they can check their answers. Finally, have students answer the questions. You may

use more or less structure than we propose. We find that students need help getting

started, so at least begin the case in class. Depending on the time available, assign parts

of the case as homework. The case is also an effective group project. It raises many is-

sues that students can debate. It is most effective when students share their ideas with

each other. Plan to spend a minimum of one hour of class time on the case.

EDGAR database cases. Internet cases that require students to access the Securities

and Exchange Commission’s EDGAR database are introduced in this chapter. Appen-

dix A discusses the EDGAR database in more detail. These cases focus on analyzing

10-K annual reports. They provide real-world exposure in a contemporary electronic

format. If your school has the computer facilities to access the EDGAR database, you

may want to include some of these cases in homework assignments.

3-6

Demonstration Problem 3-1 – Recording Procedures

The following events apply to Braxton Personnel Advisory Services Company (BPASC).

1. On January 1, 2015, issued common stock for $5,000 cash.

2. Paid $1,800 cash to rent office space for one year beginning on February 1, 2015.

3. Received a $2,400 cash advance as a retainer for services to be provided. Services were

to be provided evenly for one year beginning on March 1, 2015.

4. On December 1, 2015, paid dividends of $200 to the stockholders.

Required

a. Record the events in ledger T-accounts and prepare an unadjusted trial balance.

b. Record necessary adjusting entries in ledger T-accounts and prepare an adjusted trial

balance.

c. Use the adjusted trial balance to prepare an income statement, a statement of retained

earnings, a balance sheet, and a statement of cash flows.

d. Record the closing entries in ledger T-accounts and prepare a post-closing trial balance.

3-7

Demonstration Problem 3-2 – General Journal Entries

Required

Record the following transactions in general journal entry form. Record the event number in

the date column.

1. Issued common stock for $5,000 cash.

2. Borrowed $4,000 cash from a local bank.

3. Purchased $500 of supplies on account.

4. Recognized revenue of $8,000 for services provided on account.

5. Paid $3,900 cash for salaries expense.

6. Paid $2,400 cash in advance for a one-year lease to rent office space.

7. Purchased $3,500 of office furniture on account.

8. Received $1,800 cash for services to be performed in the future.

9. Collected $3,000 cash from accounts receivable.

10. Paid $1,200 cash for utilities.

11. Paid dividends of $1,000 cash to the stockholders.

12. Invested $2,000 cash in a certificate of deposit.

13. Repaid $1,600 of the bank loan described in Event No. 2.

14. Purchased land for $2,700 cash.

15. Recognized $400 of accrued interest expense.

16. Completed $1,800 of services on contract described in Event No. 8.

17. Counted supplies on hand at the end of the accounting period. Determined that $400 of

supplies were used during the accounting period.

18. Recognized accrued salary expense of $2,300.

19. Recognized $150 of accrued interest revenue.

3-8

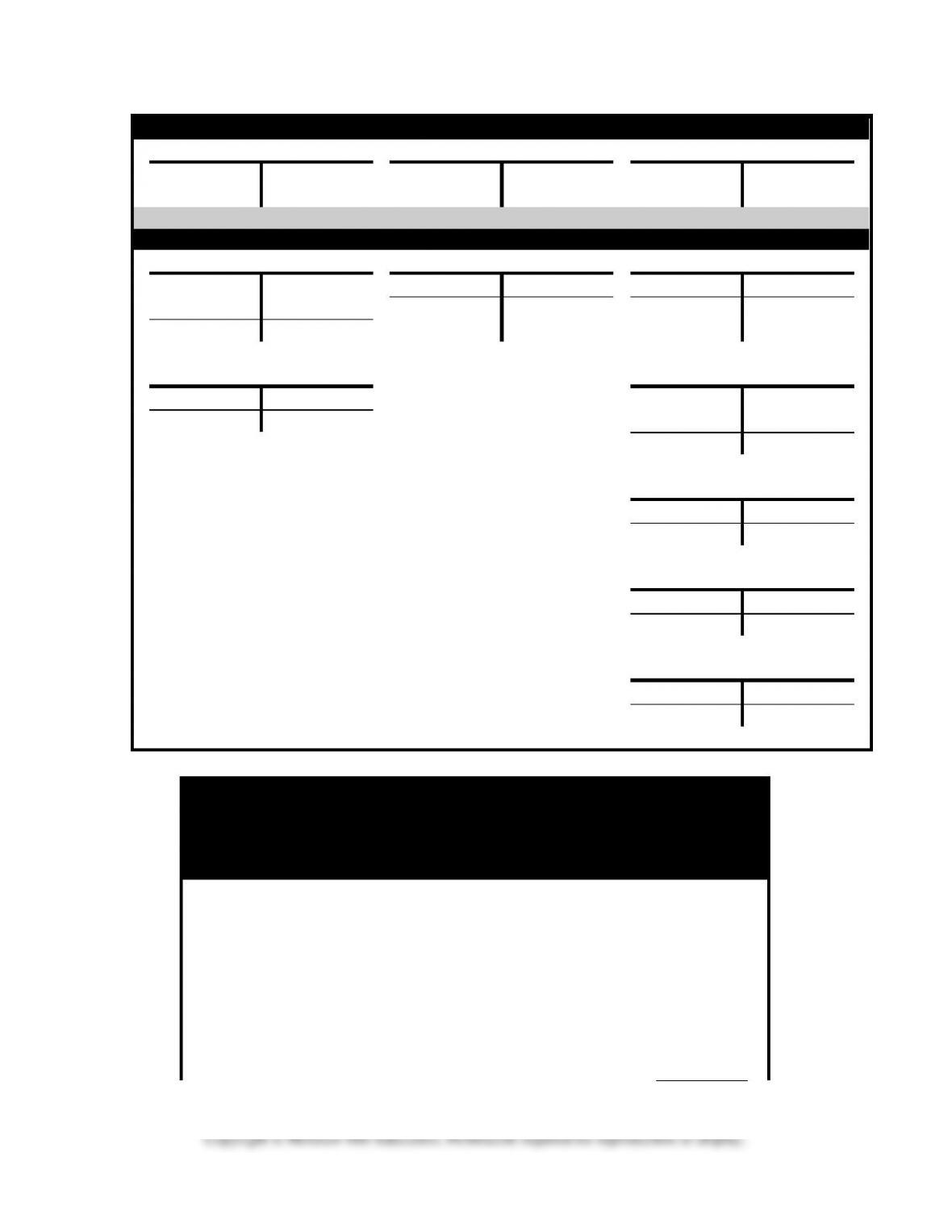

Demonstration Problem 3-1 Solution, part a.

T-Account Entries

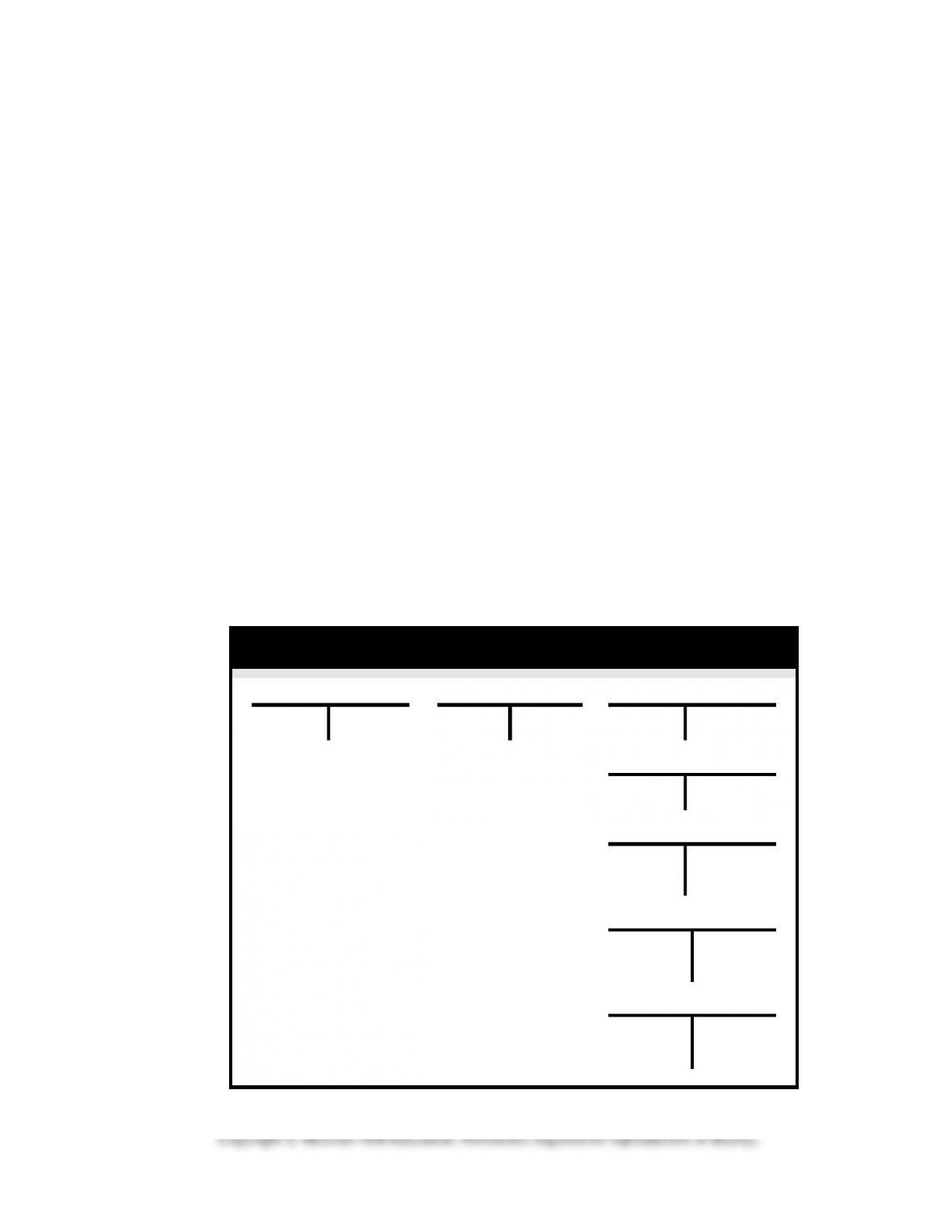

Panel 1 Recording Scheme Provided for Convenience

ASSETS

LIABILITIES

EQUITY

Debit

Credit

Debit

Credit

Debit

Credit

+

–

–

+

–

+

Panel 2 Ledger T-Accounts

Cash

Unearned Revenue

Common Stock

(1) 5,000

1,800 (2)

2,400 (3)

5,000 (1)

(3) 2,400

200 (4)

Bal. 5,400

Prepaid Rent

Dividends

(2) 1,800

(4) 200

Braxton Personnel Advisory Services Company

Unadjusted Trial Balance

December 31, 2015

Account Title

Debit

Credit

Cash

5,400

Prepaid rent

1,800

Unearned revenue

2,400

Common stock

5,000

Retained earnings

0

Services revenue

0

Rent expense

0

Dividends

200

Totals

7,400

7,400

3-9

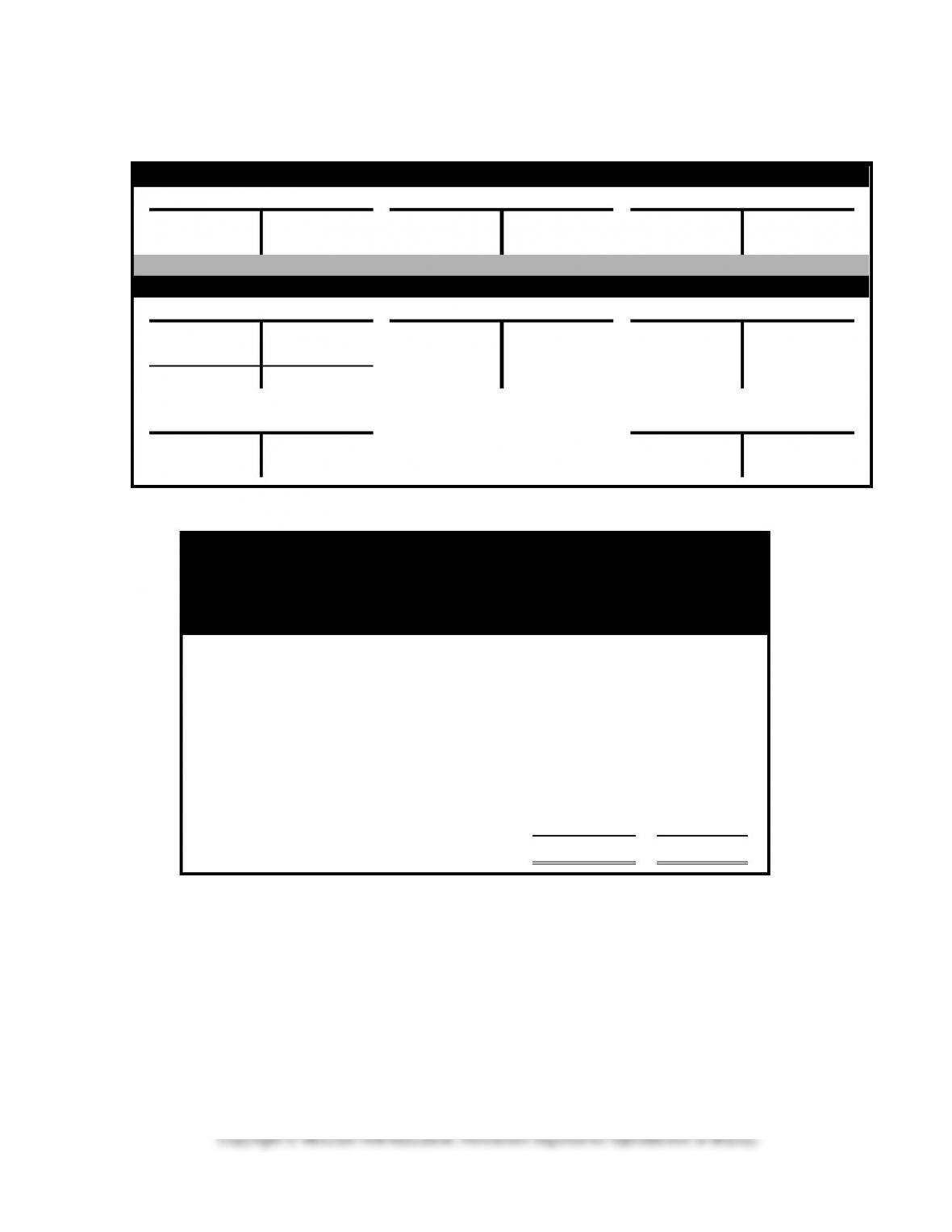

Demonstration Problem 3-1 Solution, part b.

T-Account Adjusting Entries

Panel 1 Recording Scheme Provided for Convenience

ASSETS

LIABILITIES

EQUITY

Debit

Credit

Debit

Credit

Debit

Credit

+

–

–

+

–

+

Panel 2 Ledger T-Accounts

Cash

Unearned Revenue

Common Stock

(1) 5,000

1,800 (2)

(adj2) 2,000

2,400 (3)

5,000 (1)

(3) 2,400

200 (4)

400 Bal.

Bal. 5,400

Prepaid Rent

Services Revenue

(2) 1,800

1,650 (adj1)

2,000 (adj2)

Bal. 150

Rent Expense

(adj1) 1,650

Dividends

(4) 200

Braxton Personnel Advisory Services Company

Adjusted Trial Balance

December 31, 2015

Account Title

Debit

Credit

Cash

5,400

Prepaid rent

150

Unearned revenue

400

Common stock

5,000

Retained earnings

0

Services revenue

2,000

Rent expense

1,650

Dividends

200

Totals

7,400

7,400

3-10

Demonstration Problem 3-1 Solution, part c. Financial Statements

Braxton Personnel Advisory Services Company

Financial Statements

Income Statement

For the Year Ended December 31,

2015

Services revenue

$ 2,000

Rent expense

(1,650)

Net income

$ 350

Statement of Retained Earnings

Beginning retained earnings

$ 0

Plus: Net income

350

Less: Dividends

(200)

Ending retained earnings

$ 150

Balance Sheet as of December 31, 2015

Assets

Cash

$ 5,400

Prepaid rent

150

Total assets

$ 5,550

Liabilities

Unearned revenue

$ 400

Stockholders’ equity

Common stock

5,000

Retained earnings

150

Total stockholders’ equity

5,150

Total liabilities and stockholders’ equity

$ 5,550

Statement of Cash Flows

Net cash flow from operating activities1

$ 600

Net cash flow from investing activities

0

Net cash flow from financing activities2

4,800

Net change in cash

5,400

Beginning cash balance

0

Ending cash balance

$ 5,400

1Net cash flow from operating activities: $2,400 inflow from clients less $1,800 outflow for

prepaid insurance ($2,400 – $1,800 = $600).

2Net cash flow from financing activities: $5,000 inflow from issuing common stock less

$200 outflow for dividends to stockholders. ($5,000 – $200 = $4,800).

3-11

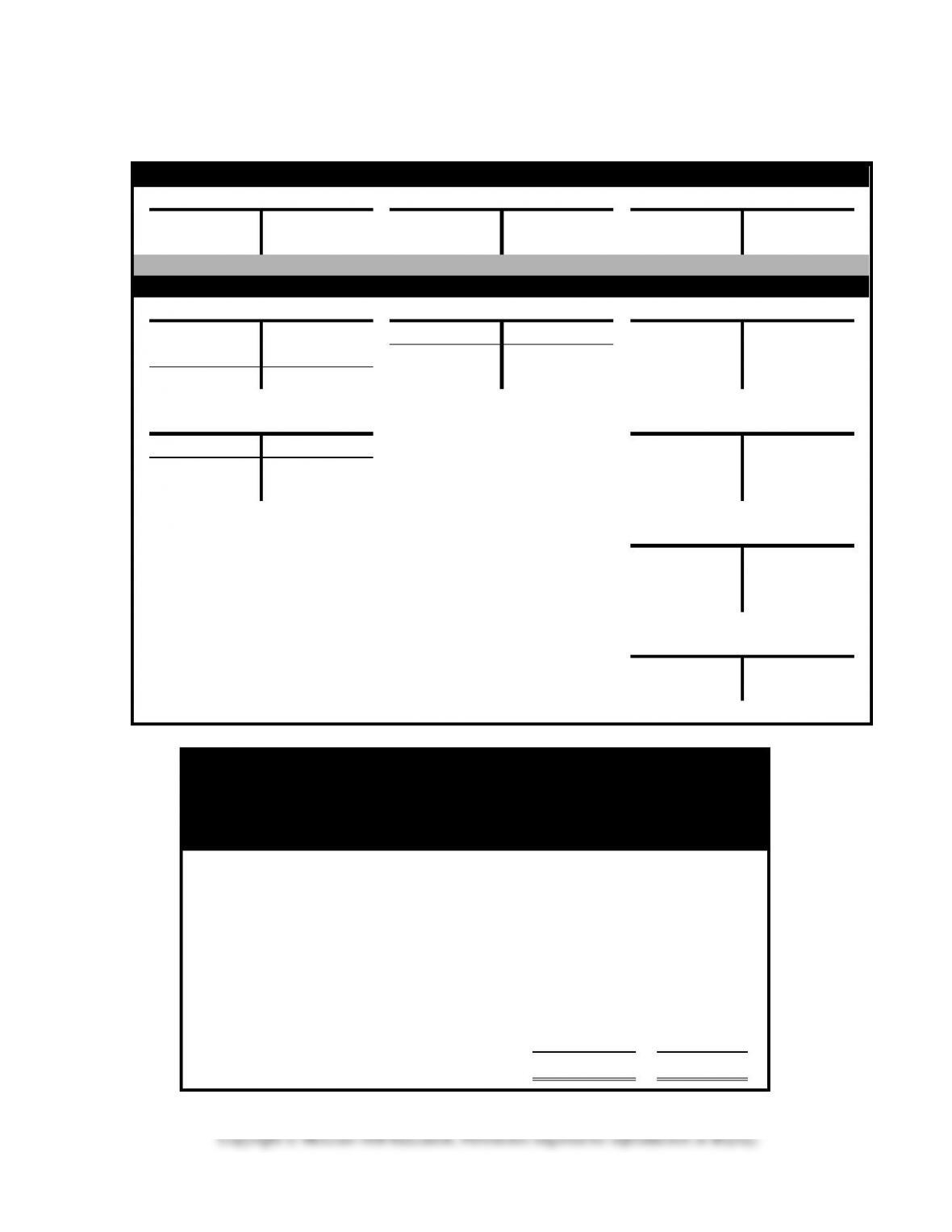

Demonstration Problem 3-1 Solution, part d. T-Account Closing Entries

Panel 1 Recording Scheme Provided for Convenience

ASSETS

LIABILITIES

EQUITY

Debit

Credit

Debit

Credit

Debit

Credit

+

−

−

+

−

+

Panel 2 Ledger T-Accounts

Cash

Unearned Revenue

Common Stock

(1) 5,000

1,800 (2)

(adj2) 2,000

2,400 (3)

5,000 (1)

(3) 2,400

200 (4)

400 Bal.

5,000 Bal.

Bal. 5,400

Prepaid Rent

Retained Earnings

(2) 1,800

1,650 (adj1)

(cl2) 1,650

2,000 (cl1)

Bal. 150

(cl3) 200

150 Bal.

Services Revenue

(cl1) 2,000

2,000 (adj2)

Rent Expense

(adj1) 1,650

1,650 (cl2)

Dividends

(4) 200

200 (cl3)

Braxton Personnel Advisory Services Company

Post-closing Trial Balance

December 31, 2015

Account Title

Debit

Credit

Cash

5,400

Prepaid rent

150

Unearned revenue

400

Common stock

5,000

Retained earnings

150

Services revenue

0

Rent expense

0

Dividends

0

Copyright © McGraw-Hill Education. Permission required for reproduction or display.

3-12

Totals

5,550

5,550