E-1

SOLUTIONS TO EXERCISES – APPENDIX E

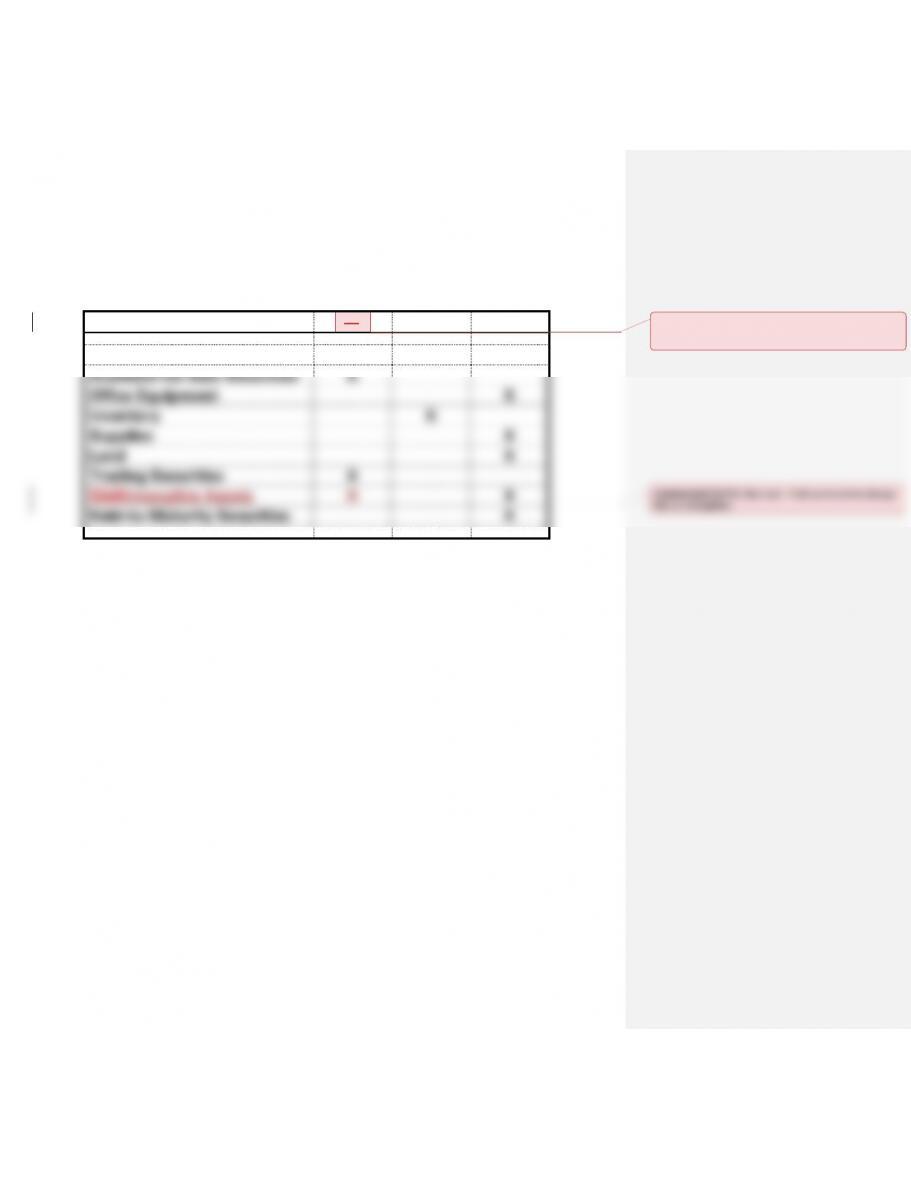

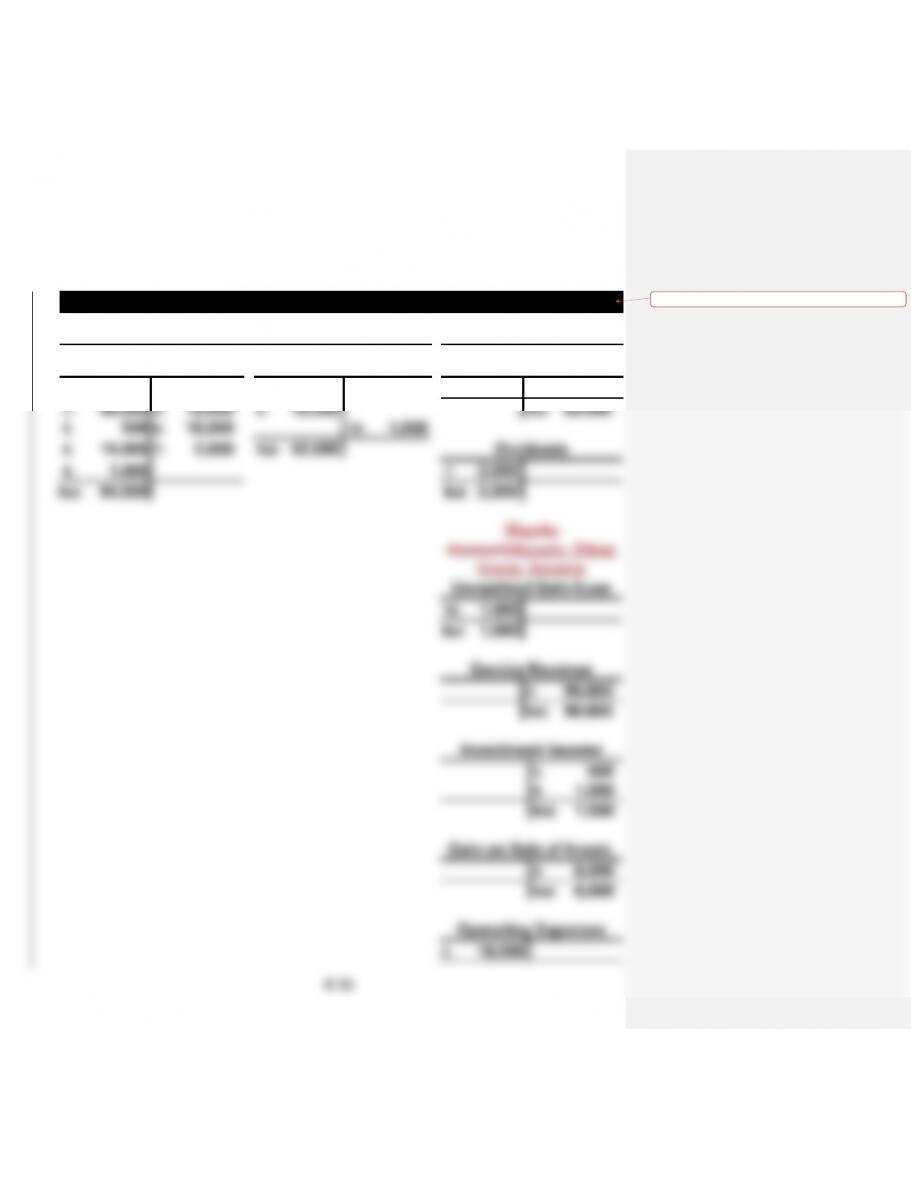

EXERCISE E1

Asset

FMV

LCM

HC/AC

Buildings

X

Available-for-Sale Securities

X

Office Equipment

X

Inventory

X

Supplies

X

Land

X

Trading Securities

X

CashIntangible Assets

X

X

Held-to-Maturity Securities

X

Commented [ILP1]: You can’t use FMV anymore – the

term is no longer used in authoritative literature (FASB

ASC)

Commented [ILP2]: See text – I left comment to change

this to intangibles

E-2

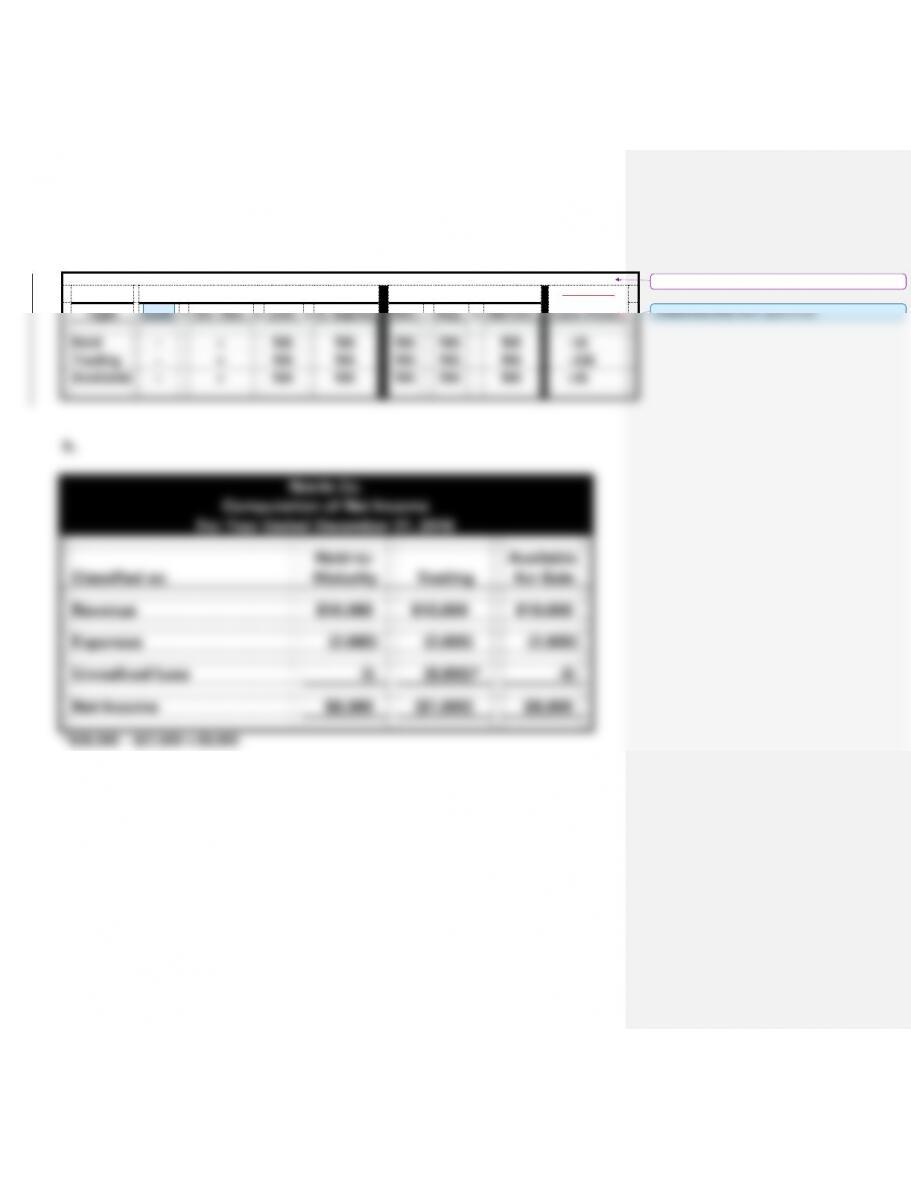

EXERCISE E2

a.

Balance Sheet

Income Statement

Stmt. of

Type

Cash

+

Inv. Sec.

=

Liab.

+

S. Equity

Rev.

−

Exp.

=

Net Inc.

Cash Flows

Held

−

+

NA

NA

NA

NA

NA

−IA

Trading

−

+

NA

NA

NA

NA

NA

−OA

Available

−

+

NA

NA

NA

NA

NA

−IA

b.

Norris Co.

Computation of Net Income

For Year Ended December 31, 2016

Classified as:

Held-to–

Maturity

Trading

Available

-for-Sale

Revenue

$10,000

$10,000

$10,000

Expenses

(2,000)

(2,000)

(2,000)

Unrealized Loss

-0-

(9,000)*

-0-

Net Income

$8,000

($1,000)

$8,000

*$36,000 – $27,000 = $9,000

Formatted Table

Commented [D3]: Add a space in box

E-3

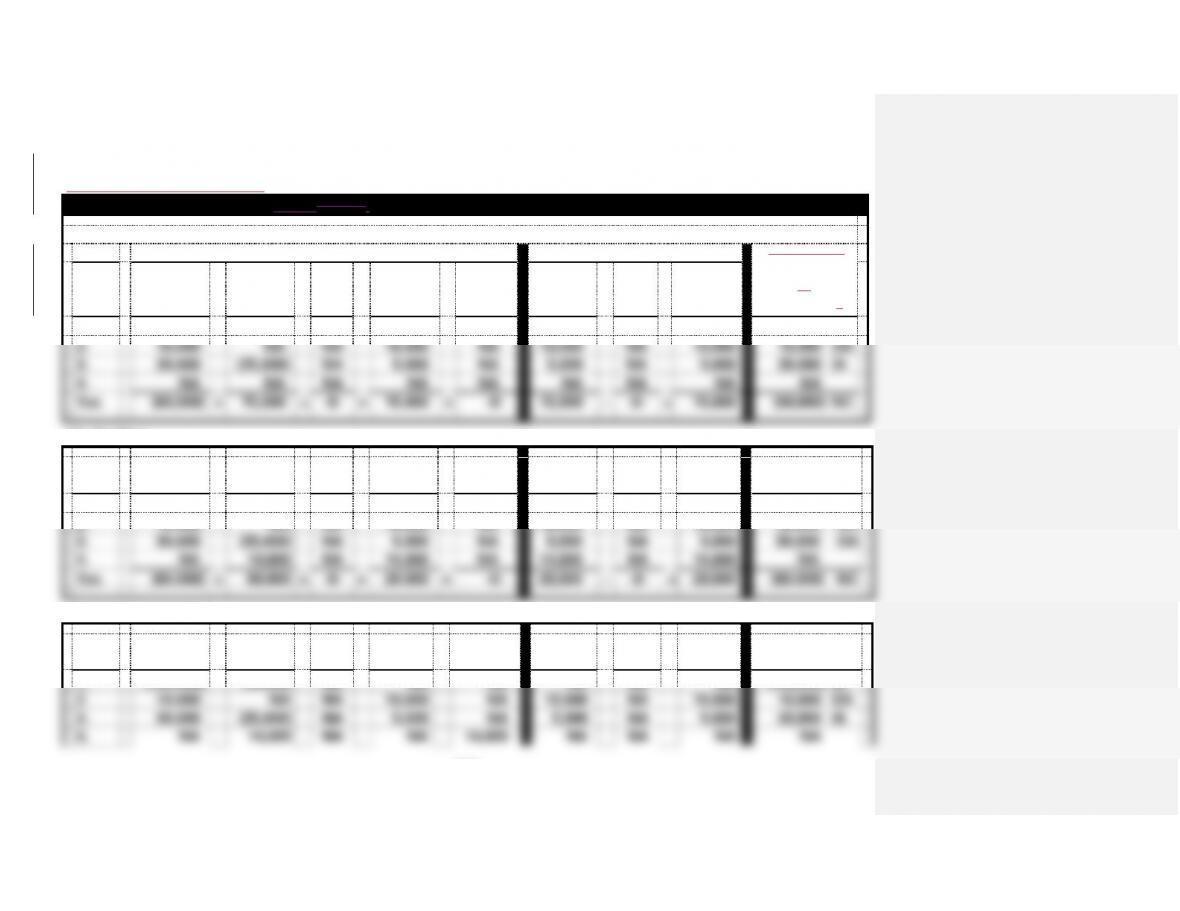

EXERCISE E3

NC = Net Change in Cash

BotterArnold Supply Co. Horizontal Statements Models

(1) Held-to-Maturity

Balance Sheet

Income Statement

Statement

Event

Cash

+

Inv. Sec.

=

Liab.

+

Ret. Ear.

+

Unreal.

Gain.

Rev./

Gain

−

Exp./

Loss

=

Net Inc.

of

Cash Flows

1.

(100,000)

100,000

NA

NA

NA

NA

NA

NA

(100,000) IA

2.

10,000

NA

NA

10,000

NA

10,000

NA

10,000

10,000 OA

3.

30,000

(25,000)

NA

5,000

NA

5,000

NA

5,000

30,000 IA

4.

NA

NA

NA

NA

NA

NA

NA

NA

NA

Tot.

(60,000)

+

75,000

=

-0-

+

15,000

+

-0-

15,000

−

-0-

=

15,000

(60,000) NC

(2) Trading

Event

Cash

+

Inv. Sec.

=

Liab.

+

Ret. Ear.

+

Unreal.

Gain

Rev./

Gain

−

Exp./

Loss

=

Net Inc.

Cash Flow

1.

(100,000)

100,000

NA

NA

NA

NA

NA

NA

(100,000) OA

2.

10,000

NA

NA

10,000

NA

10,000

NA

10,000

10,000 OA

3.

30,000

(25,000)

NA

5,000

NA

5,000

NA

5,000

30,000 OA

4.

NA

14,000

NA

14,000

NA

14,000

NA

14,000

NA

Tot.

(60,000)

+

89,000

=

-0-

+

29,000

+

-0-

29,000

−

-0-

=

29,000

(60,000) NC

(3) Available-for-Sale

Event

Cash

+

Inv. Sec.

=

Liab.

+

Ret.

Ear.

+

Unreal.

Gain

Rev./

Gain

−

Exp./

Loss

=

Net Inc.

Cash Flow

1.

(100,000)

100,000

NA

NA

NA

NA

NA

NA

(100,000) IA

2.

10,000

NA

NA

10,000

NA

10,000

NA

10,000

10,000 OA

3.

30,000

(25,000)

NA

5,000

NA

5,000

NA

5,000

30,000 IA

4.

NA

14,000

NA

NA

14,000

NA

NA

NA

NA

E-4

Tot.

(60,000)

+

89,000

=

-0-

+

15,000

+

14,000

15,000

−

-0-

=

15,000

(60,000) NC

Note: Cash is negative because these transactions do not reflect beginning balances.

E-5

EXERCISE E3 (cont.)

b. Held-to-Maturity $15,000

Trading $29,000

Available-for-Sale $15,000

E-6

EXERCISE E4

Transactions are recorded in the accounting equation for the use of the

instructor.

Assets

=

Stockholders’ Equity

Event

Cash

+

Inv. Sec.

=

C. Stock

+

Ret. Earn.

+

Unreal.

Gain

Beg. Bal.

100,000

-0-

100,000

-0-

-0-

1. Purchase. Secs.

(20,000)

20,000

-0-

-0-

-0-

2. Inv. Revenue.

600

-0-

-0-

600

-0-

3. Sold Secs.

14,000

(10,000)

-0-

4,000

-0-

4. Pur.chase Secs.

(7,000)

7,000

-0-

-0-

-0-

Totals

87,600

17,000

100,000

4,600

-0-

5. Mkt. Val.Fair

Value if HM

-0-

-0-

-0-

-0-

-0-

5. Mkt. Val.Fair

Value if TR

-0-

5,000

-0-

5,000

-0-

5. Mkt. Val.Fair

Value if AS

-0-

5,000

-0-

-0-

5,000

E-7

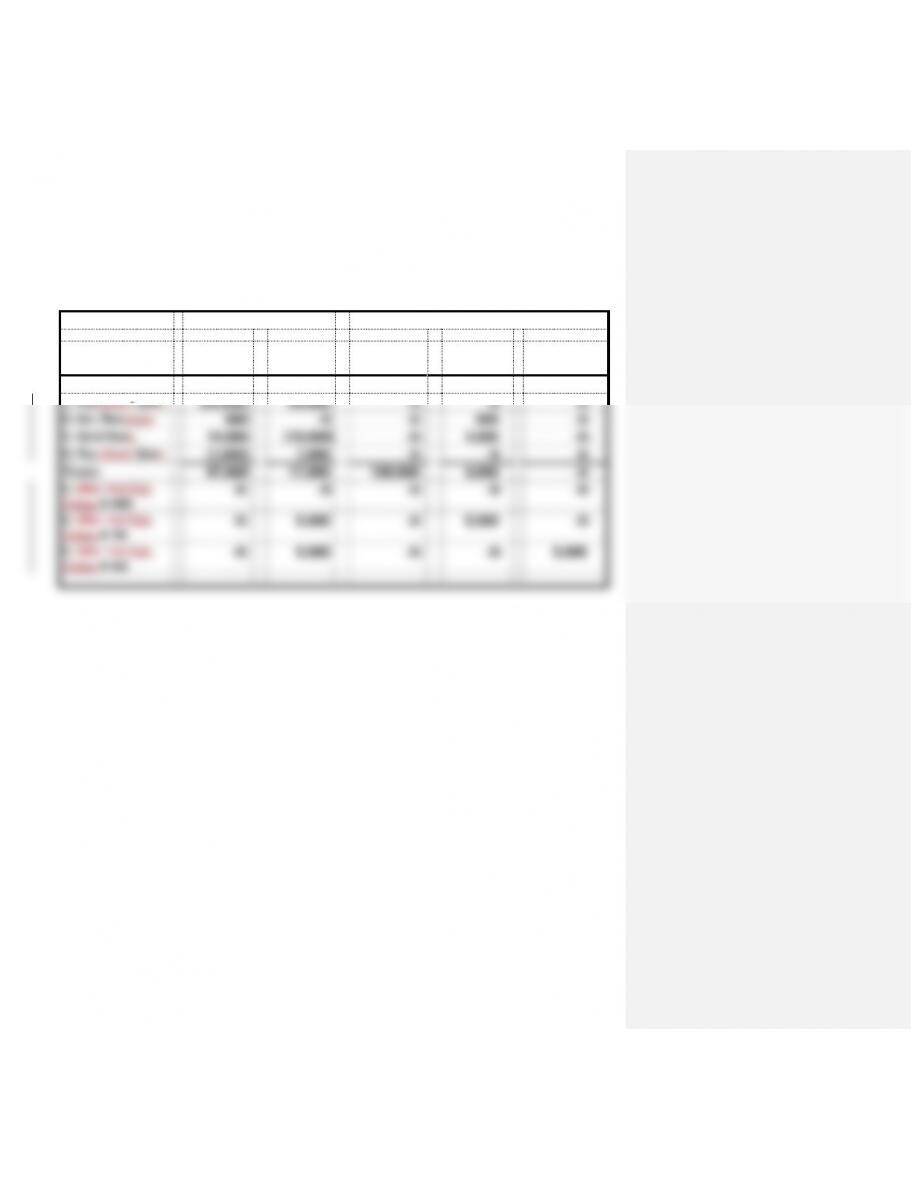

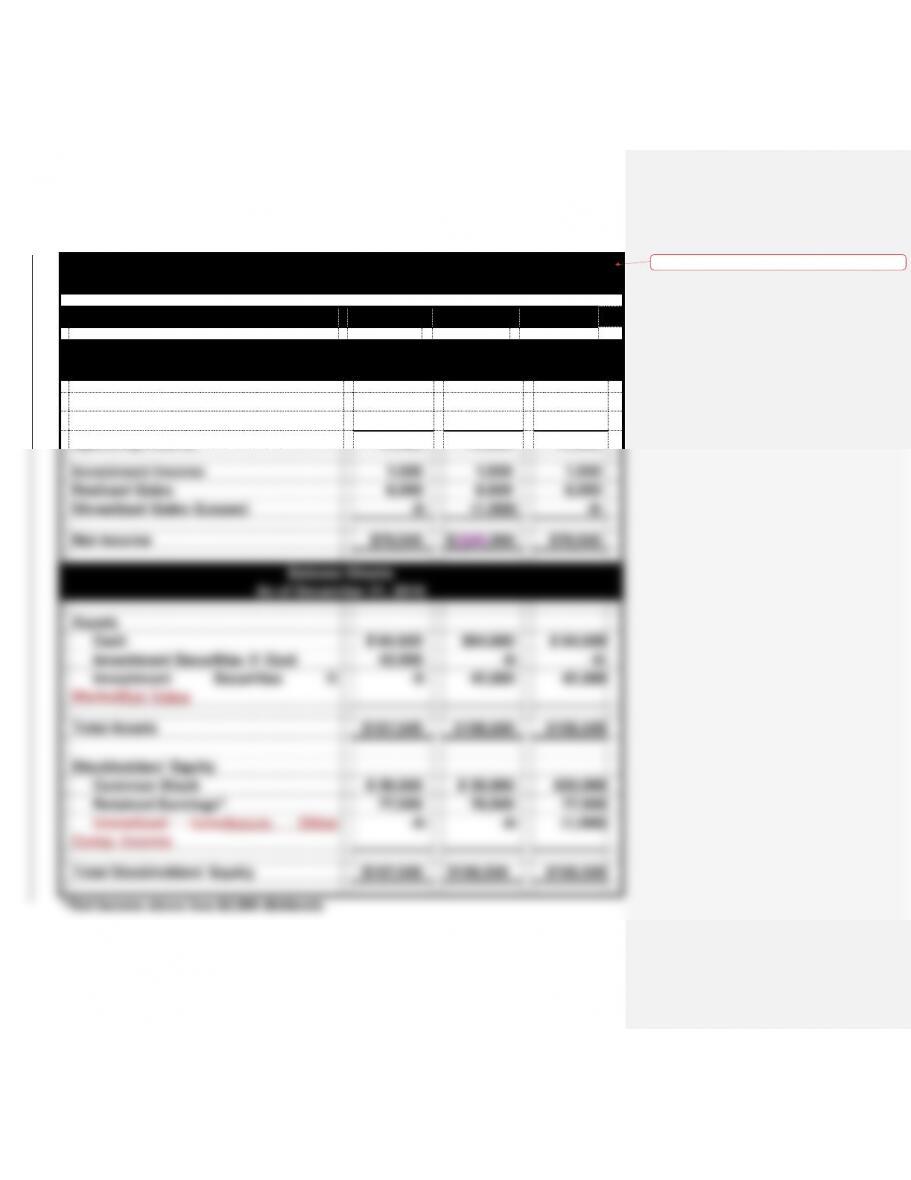

EXERCISE E4 (cont.)

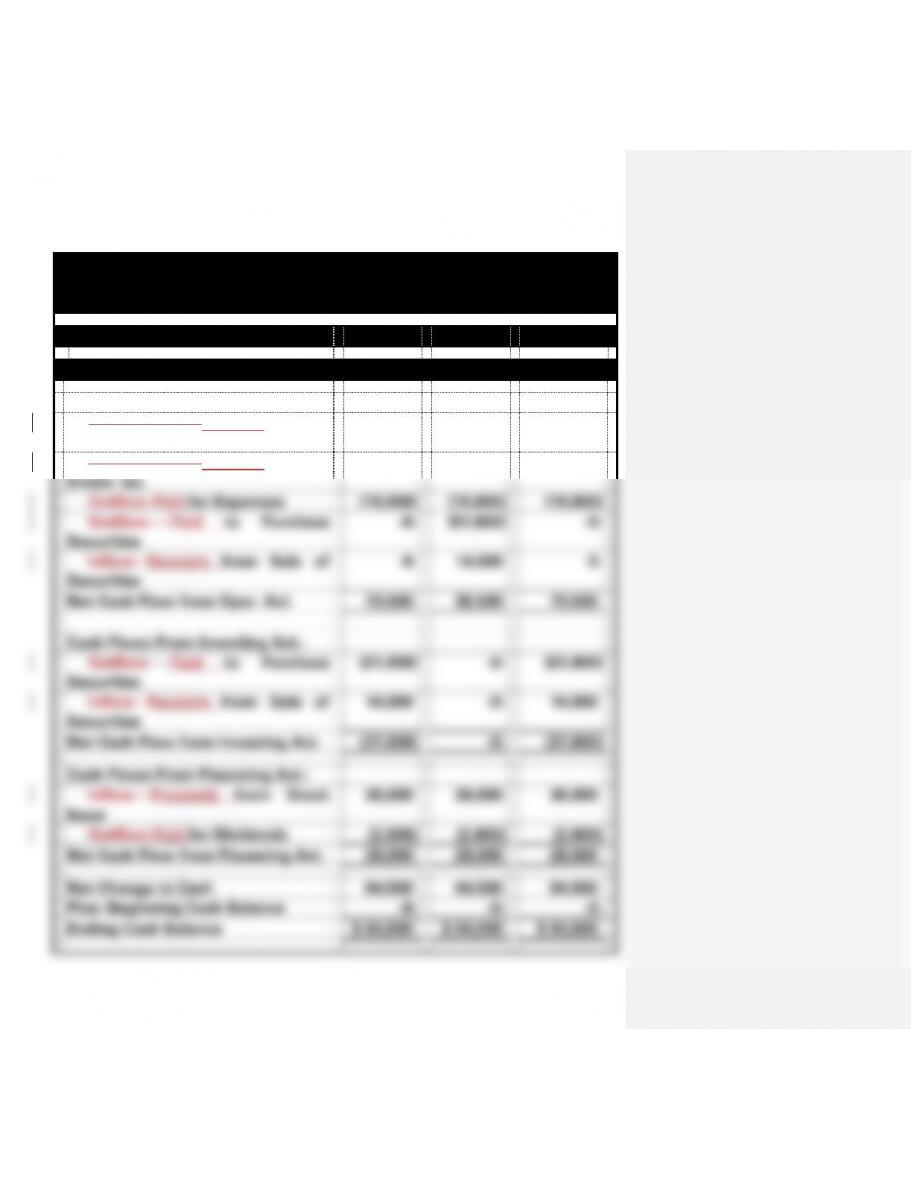

MoltenMedia, Inc.

Financial Statements For Year Ending 2016

Classified as:

Held

Trading

Available

Income Statements

Investment Revenue

$ 600

$ 600

$ 600

Realized Gain

4,000

4,000

4,000

Unrealized Gain

-0-

5,000

-0-

Net Income

$4,600

$9,600

$4,600

Balance Sheets

Assets

Cash

$ 87,600

$

8774,6200

$

8774,6200

Investment Securities

17,000

2241,000

2241,000

Total Assets

$104,600

$115,20010

9,600

$10915,62

00

Stockholders’ Equity

Common Stock

$100,000

$100,000

$100,000

Retained Earnings

4,600

9,600

4,600

Unrealized GainAccum. Other

Comp. Income

-0-

-0-

5,000

Total Stockholders’ Equity

$104,600

$109,600

$109,600

Statements of Cash Flows

Cash Flows From Operating Act.:

Inflow Receipts from Invest.

Revenue

$ 600

$ 600

$ 600

Paid to Outflow to Purchase

Securities

-0-

(27,000)

-0-

Receipts from Inflow from Sale of

Securities

-0-

14,000

-0-

Net Cash Flow from Oper. Act.

600

(12,400)

600

Cash Flows From Investing Act.:

OutflowPaid to Purchase

Securities

(27,000)

-0-

(27,000)

Inflow Receipts from Sale of

14,000

-0-

14,000

Formatted: Left, Tab stops: 2.99″, Left + 3.5″,

Centered

E-8

Securities

Net Cash Flow from Investing Act.

(13,000)

-0-

(13,000)

Cash Flows From Financing Act.

-0-

-0-

-0-

Net Change in Cash

(12,400)

(12,400)

(12,400)

Plus: Beginning Cash Balance

100,000

100,000

100,000

Ending Cash Balance

$ 87,600

$ 87,600

$ 87,600

E-9

EXERCISE E5

Investmen

t Category

Types of

Securities

Types of

Revenue

Recognized

Value Reported

on Balance Sheet

Recognition of

Unrealized

Gains/Losses

on the

Income Stmt.

Cash Flow from

Purchase or Sale of

Securities is

Classified As

Held

Debt

Interest

Amortized Cost

No

Investing Act.

Trading

Debt &

Equity

Interest &

Div.

Market Fair

Value

Yes

Operating Act.

Available

Debt &

Equity

Interest &

Div.

Market Fair

Value

No

Investing Act.

Formatted Table

E-10

EXERCISE E6

(a) Held-to-Maturity

T-Accounts

Assets

=

Equity

Cash

Investment Sec.

Common Stock

1. 30,000

3. 35,000

3. 35,000

8. 8,000

1. 30,000

2. 90,000

4. 18,000

6. 16,000

Bal. 30,000

5. 500

6. 16,000

Bal. 43,000

8. 14,000

7. 2,000

Dividends

9. 1,000

7. 2,000

Bal. 64,500

Bal. 2,000

Service Revenue

2. 90,000

Bal. 90,000

Investment Income

5. 500

9. 1,000

Bal. 1,500

Gain on Sale of Invest.

8. 6,000

Bal. 6,000

Operating Expenses

4. 18,000

Bal. 18,000

E-11

EXERCISE E6 (cont.)

(b) Trading

T-Accounts

Assets

=

Equity

Cash

Investment Sec.

Common Stock

1. 30,000

3. 35,000

3. 35,000

8. 8,000

1. 30,000

2. 90,000

4. 18,000

6. 16,000

Bal. 30,000

5. 500

6. 16,000

10. 1,000

8. 14,000

7. 2,000

Bal. 42,000

Dividends

9. 1,000

7. 2,000

Bal. 64,500

Bal. 2,000

Service Revenue

2. 90,000

Bal. 90,000

Investment Income

5. 500

9. 1,000

Bal. 1,500

Gain on Sale of Invest.

8. 6,000

Bal. 6,000

Operating Expenses

4. 18,000

Bal. 18,000

(Income Statement

Account)

Unrealized Gain/Loss

10. 1,000

Bal. 1,000

E-12

EXERCISE E6 (cont.)

(c) Available-for-Sale

T-Accounts

Assets

=

Equity

Cash

Investment Securities

Common Stock

1. 30,000

3. 35,000

3. 35,000

8. 8,000

1. 30,000

2. 90,000

4. 18,000

6. 16,000

Bal. 30,000

5. 500

6. 16,000

10. 1,000

8. 14,000

7. 2,000

Bal. 42,000

Dividends

9. 1,000

7. 2,000

Bal. 64,500

Bal. 2,000

(Equity

Account)Accum. Other

Comp. Income

Unrealized Gain/Loss

10. 1,000

Bal. 1,000

Service Revenue

2. 90,000

Bal. 90,000

Investment Income

5. 500

9. 1,000

Bal. 1,500

Gain on Sale of Invest.

8. 6,000

Bal. 6,000

Operating Expenses

4. 18,000

Formatted Table

E-14

Bal. 18,000

E-15

EXERCISE E6 a., b., & c. (cont.)

Harrison Imports

Comparative Financial Statements

Investment Securities Classified As

Held

Trading

Available

Income Statements

For the Year Ended 2013

Services Revenue

$90,000

$90,000

$90,000

Operating Expenses

(18,000)

(18,000)

(18,000)

Operating Income

72,000

72,000

72,000

Investment Income

1,500

1,500

1,500

Realized Gains

6,000

6,000

6,000

Unrealized Gains (Losses)

-0-

(1,000)

-0-

Net Income

$79,500

$7880,500

$79,500

Balance Sheets

As of December 31, 2016

Assets

Cash

$ 64,500

$64,500

$ 64,500

Investment Securities @ Cost

43,000

-0-

-0-

Investment Securities @

MarketFair Value

-0-

42,000

42,000

Total Assets

$107,500

$106,500

$106,500

Stockholders’ Equity

Common Stock

$ 30,000

$ 30,000

$30,000

Retained Earnings*

77,500

76,500

77,500

Unrealized LossAccum. Other

Comp. Income

-0-

-0-

(1,000)

Total Stockholders’ Equity

$107,500

$106,500

$106,500

Formatted Table

E-16

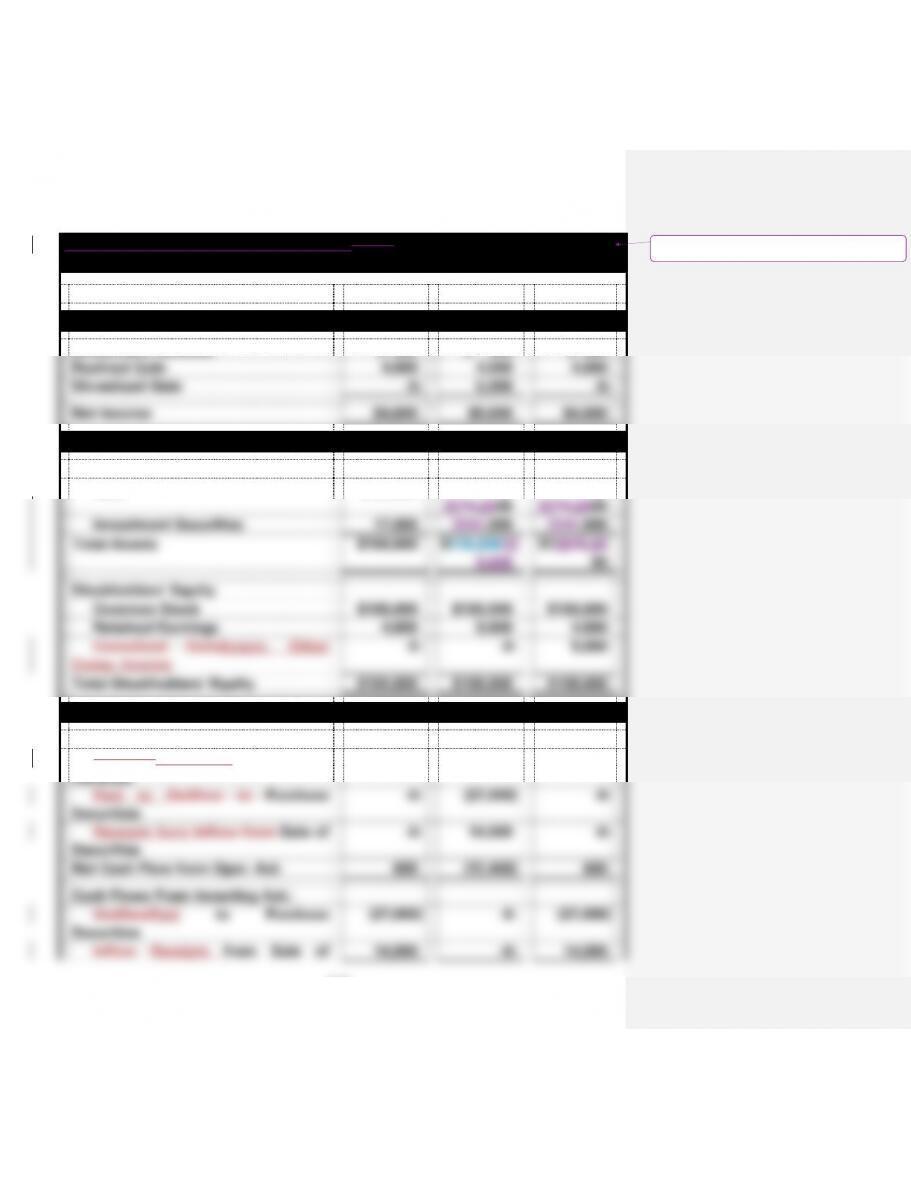

EXERCISE 6 a., b., & c. (cont.)

Harrison Imports

Comparative Financial Statements

For the Year Ended 2016

Investment Securities Classified as

Held

Trading

Available

Statements of Cash Flows

Cash Flows From Operating Act.:

Cash InflowReceipts from

Customers

$ 90,000

$ 90,000

$ 90,000

Cash InflowReceipts from

Invest. Inc.

1,500

1,500

1,500

Outflow Paid for Expenses

(18,000)

(18,000)

(18,000)

Outflow Paid to Purchase

Securities

-0-

(51,000)

-0-

Inflow Receipts from Sale of

Securities

-0-

14,000

-0-

Net Cash Flow from Oper. Act.

73,500

36,500

73,500

Cash Flows From Investing Act.:

Outflow Paid to Purchase

Securities

(51,000)

-0-

(51,000)

Inflow Receipts from Sale of

Securities

14,000

-0-

14,000

Net Cash Flow from Investing Act.

(37,000)

-0-

(37,000)

Cash Flows From Financing Act.:

Inflow Proceeds from Stock

Issue

30,000

30,000

30,000

Outflow Paid for Dividends

(2,000)

(2,000)

(2,000)

Net Cash Flow from Financing Act.

28,000

28,000

28,000

Net Change in Cash

64,500

64,500

64,500

Plus: Beginning Cash Balance

-0-

-0-

-0-

Ending Cash Balance

$ 64,500

$ 64,500

$ 64,500

E-17

E-18

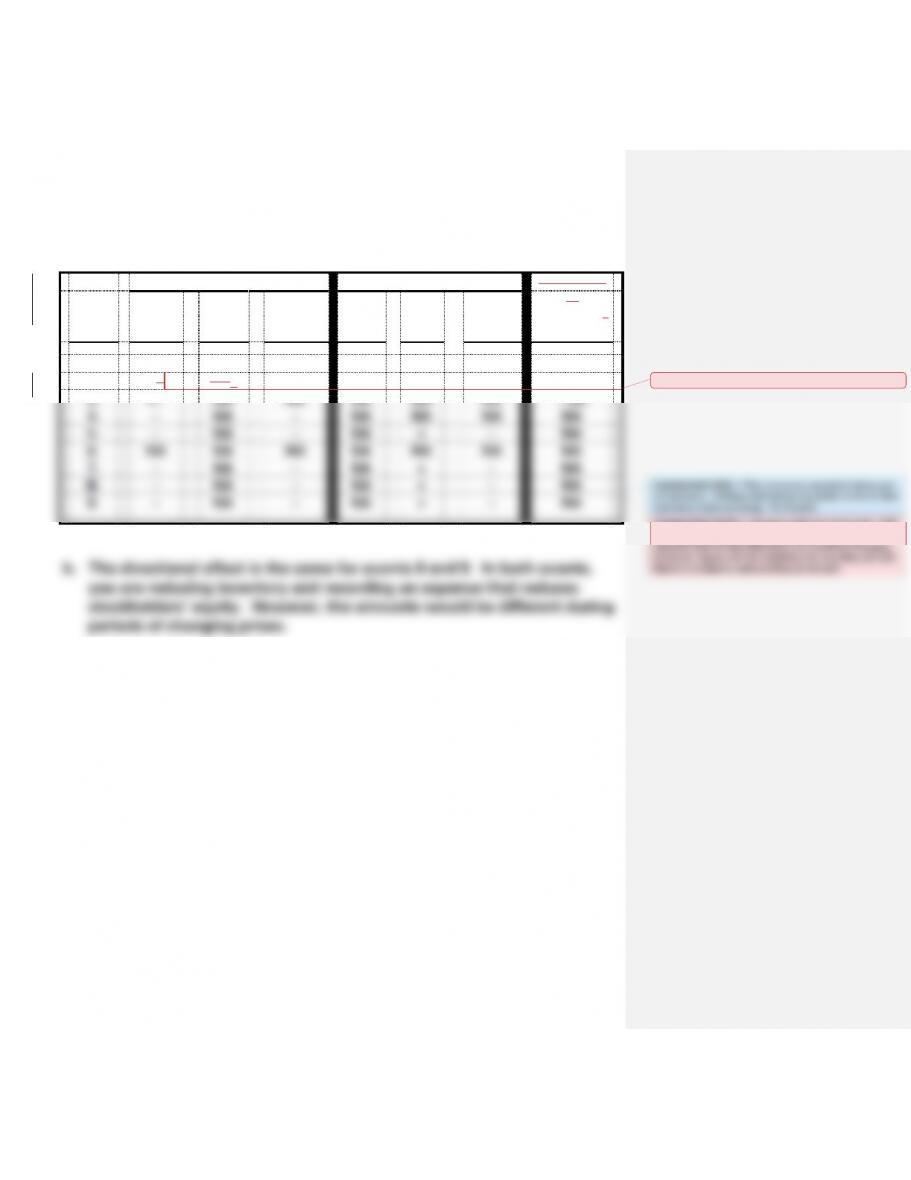

EXERCISE E7

a.

Balance Sheet

Income Statement

Statement

Event

Assets

=

Liab.

+

S.

Equity

Rev./

Gain

−

Exp./

Loss

=

Net Inc.

of

Cash Flows

1.

+

NA

+

NA

NA

NA

+ FA

2.

+−

NA+

NA

NA

NA

NA

NA

3.

+−

NA

NA

NA

NA

NA

− OA

4.

–

NA

–

NA

NA

NA

NA

5.

–

NA

–

NA

+

–

NA

6.

NA

NA

NA

NA

NA

NA

NA

7.

−

NA

−

NA

+

−

NA

8.

−

NA

−

NA

+

−

NA

9.

−

NA

−

NA

+

−

NA

there is no need to add anything to the text

Commented [ILP4]: Purch inventory on account

Commented [D5]: ? This is true in a period of rising cost

of inventory. Perhaps that should be stated in the ex that

inventory costs are rising. For 8 and 9

Commented [ILP6]: I disagree with that comment. CGS

will reduce net income no matter what. The next

question asks for the difference and mentions changing