7-1

Chapter 7

Accounting for Receivables

General Comments for Chapter 7

This chapter focuses on accounting for receivables – both collectible and uncollectible. This

chapter also includes accounting for credit card sales and discount notes. You can begin this

chapter by discussing how customers pay for purchases. Some companies allow customers

to pay on account while other companies accept credit cards as payment. Ask students if all

customers pay their account balances. Discuss how companies might handle situations

where it becomes evident that a customer is not going to pay what is owed. Help students

begin to think about how a company might handle situations where they know some custom-

ers won’t pay their amounts due – it’s just that the company doesn’t know which customers

won’t pay. This is a great time to bring company credit policies into the discussion. If a

company has a very strict credit policy, it might lose sales. On the flip side, if a company has

very flexible credit policies, it might find more customers that won’t pay their amounts due.

If you would like to begin the chapter with a problem-based learning exercise, see the notes

below.

Problem-Based Learning Case: Bad Debts

Instructions: The case appears on the following page in a format you can copy or display.

Distribute copies of the case to the class before providing an explanation of bad debt expens-

es. Ask students to read the case and individually develop answers. After allowing students

time to develop their individual answers, put them into groups to reach consensus on an an-

swer. Also, ask each group to select a spokesperson. Allow groups time to develop answers,

then call on some of the spokespersons to share their solutions. As you respond to the stu-

dent solutions, explain the basic concepts of accounting for bad debts and warranty expenses.

The correct answer is:

Fees revenue

$ 180,000

Bad debts expense

(9,000)

Other operating expenses

(120,000)

Net income

$ 51,000

7-2

Chapter 7 Problem-Based Learning Case:

Bad Debt Expense

Wilson Eye Care earned $180,000 of revenue on account during

2015. Based on past experience Wilson estimated 5% of the credit

sales would never be collected because some customers would be

unable to pay their bills. Wilson incurred $120,000 of other operat-

ing expenses during 2015. Using this information alone, what

amount of net income should Wilson report on its 2015 income

statement?

7-3

Detailed Outline of a Lesson Plan for Chapter 7

I. Explaining how bad debts affect financial statements requires a multicycle ex-

ample. Demonstration Problem 7-1 illustrates accounting for bad debts over two

cycles using the percent of sales method.

A. Start by instructing students to record the first two events under the appropriate

headings using the horizontal financial statements model. The first event involves

recognizing $4,000 of revenue earned on account, and the second event reflects

collecting $3,000 of the accounts receivable created in the first event. By now,

students should be able to record these events with little assistance.

B. Emphasize that the $1,000 balance in accounts receivable represents the total

amount of cash the company would collect if all the customers paid their bills.

Actual collections will likely be less because some customers will be unable to

pay. As a result, expenses are understated and assets are overstated. The compa-

ny can improve reporting accuracy by estimating an amount of credit sales that is

likely to be uncollectible and by deducting that amount from the balance in the re-

ceivables account. The amount of estimated uncollectible accounts is called an

allowance for doubtful accounts. This is the first time students have been intro-

duced to the concept of a contra account. Explain the fact that a contra account

is always associated with another account – accounts receivable in this instance.

If you have introduced debits and credits, you can explain that contra accounts

carry a credit balance when associated with asset accounts, since asset accounts

typically carry a debit balance. Likewise, contract accounts associated with a lia-

bility account would carry a debit balance, since liabilities typically carry credits

balances. Since allowance for doubtful accounts is associated with an asset – ac-

counts receivable – this contra account typically carries a credit balance while the

balance in the associated accounts receivable asset account is typically a debit

balance. If you have not introduced debits and credits, then you can discuss the

fact that the balance in this contra account is negative while the balance in the as-

sociated account is positive. Combining the contra account balance with the as-

sociated asset balance results in what called the net realizable value of receiva-

bles (the amount of cash the company ultimately expects to collect). The focus is

on matching expenses with sales revenues. The amount of bad debts expense to

recognize is determined by estimating the amount of sales expected to ultimately

be uncollectible. Record the event using the horizontal financial statements mod-

el. Point out that recognizing bad debts expense affects the balance sheet and the

income statement, but does not affect cash flow.

C. Events in the second accounting period illustrate accounting for the write-off of

an uncollectible account, the recovery of a previously written-off account receiv-

able, and recognizing bad debts expense for the second year.

7-4

1. The first event in the second year is the write-off of account receivables the

company has determined to be uncollectible. Record the event using the hori-

zontal financial statements model. Emphasize that the write-off does not af-

fect the income statement because the expense was previously recognized in

2015. Also, cash flow and total assets are unaffected. Students often struggle

with the concept of writing off uncollectible receivables when using the al-

lowance method. They think the write off should result in an entry to ex-

pense. You may want to spend some extra time emphasizing that the expense

was recognized in the prior year and was matched to the revenue that was es-

timated to be uncollectible.

2. Have students record Events 2 and 3 on their own. These are familiar events.

Having students record the events rather than doing it for them provides time

for students to think about the first event before they rush into the next seg-

ment of the problem. Take a look around the room with the aim of helping

students who are having difficulty. This strategy keeps students actively in-

volved in their learning. Whenever possible, have students do the work rather

than doing it for them.

3. Events 4 and 5 involve the recovery and collection of a previously written-off

account receivable. Explain reinstating the receivable as a reversal of the pre-

vious write-off. The collection is no different than any other collection of a

receivable and is usually easy for students to understand.

4. Estimate the amount of bad debts expense to recognize in Event No. 6. Note

that the expense is the same as it was the previous year except the percentage

has been reduced to reflect the first year’s experience. This would be a good

time to discuss how bad debt expenses are estimated. Discuss the two differ-

ent methods of calculating bad debt expense (called uncollectible accounts

expense in the textbook). One method is the percentage of revenue method (an

income statement focus), and the other is the aging of accounts receivable

method (a balance sheet approach).

When you record the event using the horizontal financial statements model,

stress that expense recognition comes at the end of the accounting cycle through

an adjusting entry. It affects the balance sheet by reducing the net realizable val-

ue of receivables and affects stockholders’ equity by reducing retained earnings.

The expense affects the balance sheet but not cash flow. These are critical points.

Do not let them become obscured by complications arising from computing the

amount of expense to recognize.

D. Record the events in T-accounts, close the revenue and expense accounts, and

compare the T-account balances with the balances in the statements model.

E. Point out that this Demonstration Problem highlighted accounting for uncollecti-

ble accounts using the allowance method. Point out that the creation of an ac-

count called allowance for doubtful accounts illustrates the fact that this company

uses the allowance method. The allowance method is the one required by gener-

7-5

ally accepted accounting principles. The direct write-off method is only allowed

if the uncollectible accounts are an immaterial amount. Then discuss how a com-

pany would handle bad debts if the direct write off method were used. In this

method, no allowance for doubtful accounts would be established. Only when ac-

counts are written off would bad debt expense be recorded. This would be a good

time to ask students if they thought the direct write off method properly matched

revenues earned with expenses incurred to earn those revenues. It would also be a

good time to ask students what kinds of companies should use the allowance

method and what kinds could appropriately use the direct write off method.

II. Use Demonstration Problem 7-2 to introduce accounting for credit card sales.

Point out that the full amount of the sale is shown as revenue and that the charge for

the use of the credit card is an expense. Also help the students see that the cash flow

impact of credit card sales differs from the manner in which revenue and expense are

recorded.

III. Use Demonstration Problem 7-3 to introduce accounting for notes receivable.

The problem covers two cycles. The note has a one-year term. Date of issue, accrual

of interest, and repayment of principal at maturity are covered. Before demonstrating

how to record the transactions, explain that notes receivable are just like accounts re-

ceivable but they are for a longer period of time. You can remind students of the in-

terest payable discussions in Chapter 2 and relate that information to the interest rev-

enue accrued on notes receivable. Now begin Demonstration Problem 7-3. Discuss

the manner in which interest receivable would be computed. Record the 2015 events

in T-accounts. Close the revenue and expense accounts for 2015. After recording the

2015 transactions in T-accounts, use the horizontal financial statements model to

show how each event will affect the financial statements. Finally, record the 2016

transactions in T-accounts. Emphasize that the interest receivable balance from 2015

carried forward as the beginning balance in 2016. After interest receivable is record-

ed in 2016, the interest receivable balance reflects the full year of interest that will be

received on the note maturity date.

IV. Time considerations and homework assignments. Plan to spend approximately

two hours of class time on this chapter. Accounting for bad debts requires the majori-

ty of this time. Students seem to struggle with this concept, especially when the al-

lowance method is used, because of the different ways to calculate the uncollectible

accounts expense. Use Demonstration Problem 7-1 to illustrate the basic concepts

and then assign Exercises 7-4 A or B or 7-6 A or B as homework. We recommend

that you help your students start these problems in class. Accounting for bad debts is

a difficult subject for most students and many of them will need your assistance.

Work as far into the problems as class time permits. Reserve approximately one-half

hour to cover accounting for credit card sales and notes receivable. Use Exercise 7-

14 A or B to reinforce students’ understanding of how credit card sales affect finan-

cial statements and Exercise 7-11 A or B to reinforce accounting for notes receivable

7-6

concepts. Exercise 7-15 A or B is an excellent comprehensive assignment that brings

together all the concepts covered in chapters 1 – 7.

7-7

Demonstration Problem 7-1 – Accounting for Bad Debts

The Solo Company was started on January 1, 2015. The following events occurred during

2015 and 2016.

2015

1. Provided $4,000 of services on account.

2. Collected $3,000 cash from accounts receivable.

3. Estimated uncollectible accounts expense to be 1.5% of 2015 credit sales.

2016

1. Wrote off $40 of accounts receivable that were deemed uncollectible.

2. Provided $6,500 of services on account.

3. Collected $5,400 cash from accounts receivable.

4. Received $5 from a bad debt that had been previously written off. Reinstated the ac-

count.

5. Recorded the $5 cash received from the receivable reinstated in Event No. 4.

6. Estimated uncollectible accounts expense to be 1% of 2016 credit sales.

Required

a. Record the events in T-accounts, including closing the revenue and expense accounts to

retained earnings.

b. Record the events using the horizontal financial statements model under the titles of the

affected accounts. Record a zero under each heading not affected by a given event.

Compare the final balances in the T-accounts from Part a with the ending balances in the

horizontal financial statements model.

Demonstration Problem 7-2 – Credit Card Sales

Versa Training Services provides instruction on how to pass the CPA examination. The fol-

lowing events pertain to a new course that was recently established by Versa.

1. Versa accepted credit card payments for $8,000 of instructional services it provided to

CPA exam candidates. The credit card company charged Versa a 5% service fee.

2. Versa collected the receivable due from the credit card company.

Required

a. Record the events in T-accounts, including closing the revenue and expense accounts to

retained earnings

b. Record the events using the horizontal financial statements model under the titles of the

affected accounts. Record a zero under each heading not affected by the event. Compare

7-8

the final balances in the T-accounts from Part a with the ending balances in the horizon-

tal financial statements model.

Demonstration Problem 7-3 – Notes Receivable

Money Lenders experienced the following accounting events in its first year of operation.

1. The company was started on January 1, 2015 when it received $50,000 in cash for the

sale of common stock.

2. Paid $4,200 cash for operating expenses.

3. Recognized $7,300 of cash service revenue.

4. Loaned $10,000 cash to Needy Company on July 1, 2015. Needy Company signed a

one-year note and agreed to pay 5% interest. Money Lenders recognized accrued inter-

est receivable at December 31, 2015.

Accounting events affecting 2016 were as follows:

1. On July 1, 2016 Needy Company repaid the note and interest. Money Lenders recog-

nized the accrued interest receivable just prior to this payment.

2. Recognized $9,500 of cash service revenue.

3. Paid $6,400 cash for operating expenses.

Required

a. Record the events for 2015 and 2016 in T-accounts.

b. Record the events for 2015 and 2016 using the horizontal financial statements model.

7-9

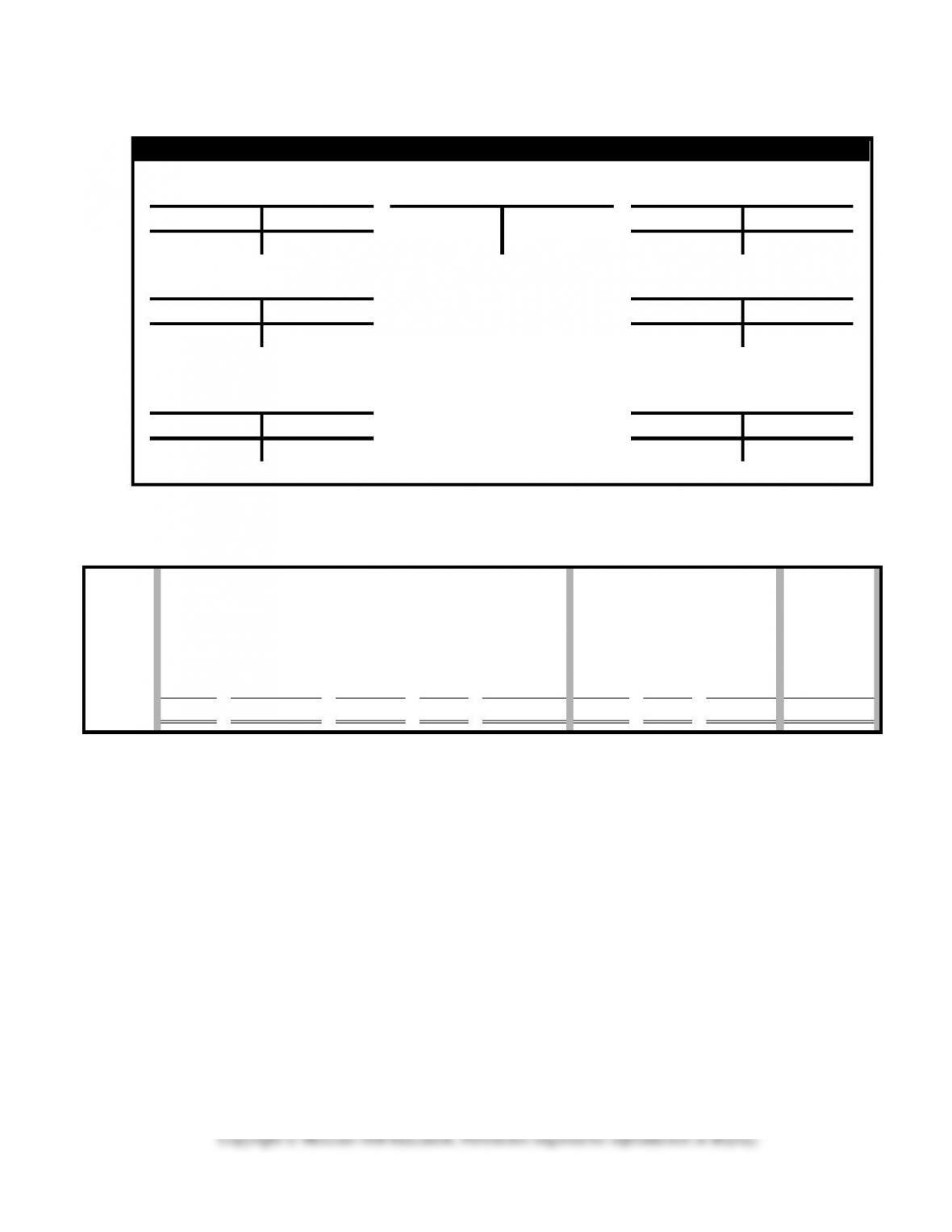

Demonstration Problem 7-1 Solution, part a. T-accounts, 2015

Ledger T-Accounts

Cash

Liabilities

Retained Earnings

(2) 3,000

3,940 cl.

Bal. 3,000

3,940 Bal.

Accounts Receivable

Services Revenue

(1) 4,000

3,000 (2)

cl. 4,000

4,000 (1)

Bal. 1,000

Allow. for Doubt. Accts.

Uncollect. Accts.

Expense

60 (3)

(3) 60

60 cl.

60 Bal.

Demonstration Problem 7-1 Solution, part b. Statements Model, 2015

Event

Assets

=

Liab.

+

Equity

Rev.

–

Exp.

=

Net Inc.

Cash Flow

No.

Cash

+

Accts. Rec.

+

(Allow.)

=

Ret. Earn.

Beg. bal.

0

+

0

+

0

=

0

+

0

0

–

0

=

0

0

1.

0

+

4,000

+

0

=

0

+

4,000

4,000

–

0

=

4,000

0

2.

3,000

+

(3,000)

+

0

=

0

+

0

0

–

0

=

0

3,000 OA

3.

0

+

0

+

(60)

=

0

+

(60)

0

–

60

=

(60)

0

Totals

3,000

+

1,000

+

(60)

=

0

+

3,940

4,000

–

60

=

3,940

3,000 NC

7-10

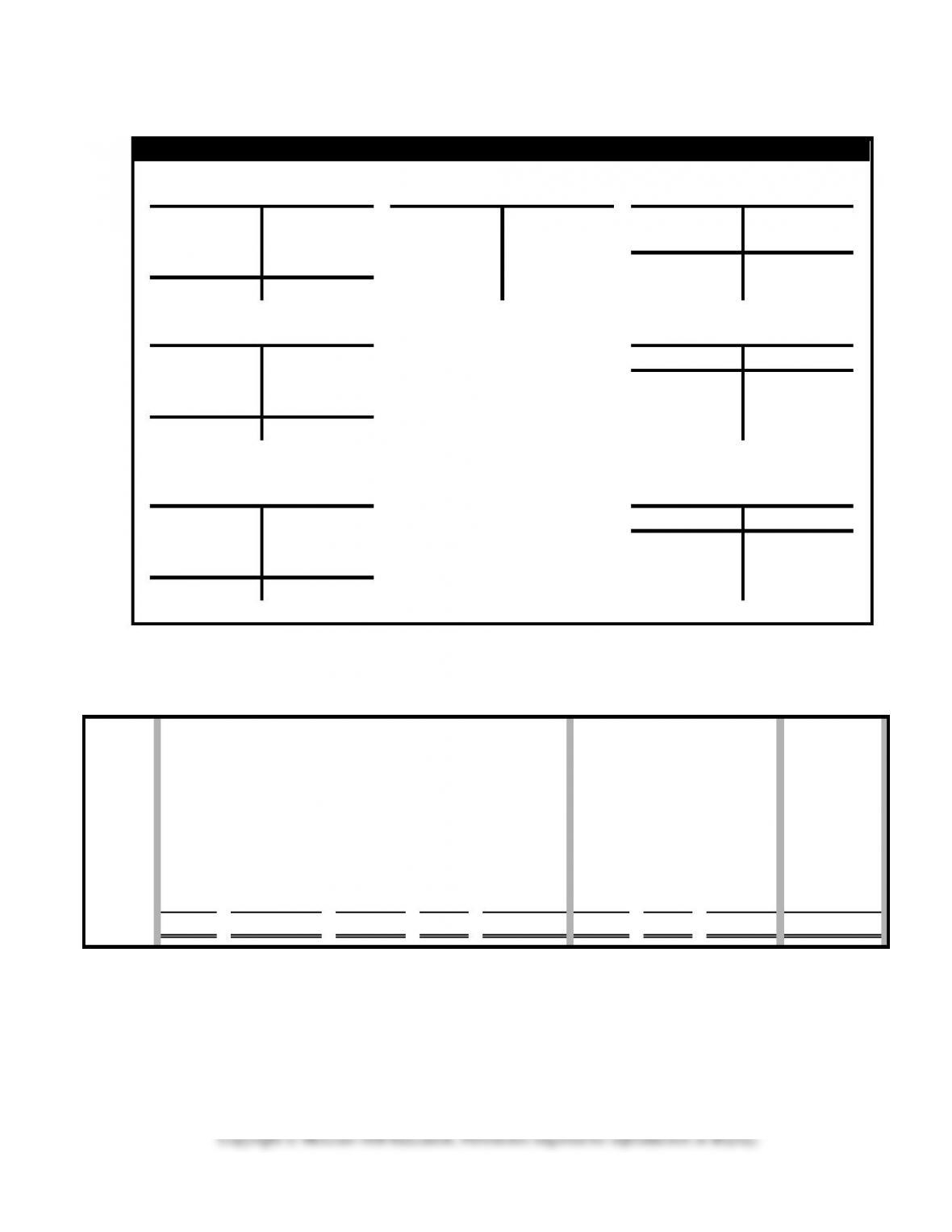

Demonstration Problem 7-1 Solution, part a. T-accounts, 2016

Ledger T-Accounts

Cash

Liabilities

Retained Earnings

Bal. 3,000

3,940Bal.

(3) 5,400

6,435 cl

(5) 5

10,375

Bal. 8,405

Accounts Receivable

Services Revenue

Bal. 1,000

40 (1)

cl. 6,500

6,500 (2)

(2) 6,500

5,400 (3)

(4) 5

5 (5)

Bal. 2,060

Allow. for Doubt. Accts.

Uncollect. Accts.

Expense

(1) 40

60 Bal.

(6) 65

65 cl

5 (4)

65 (6)

90 Bal.

Demonstration Problem 7-1 Solution, part b. Statements Model, 2016

Event

Assets

=

Liab.

+

Equity

Rev.

–

Exp.

=

Net Inc.

Cash Flow

No.

Cash

+

Accts. Rec.

+

(Allow.)

=

Ret. Earn.

Beg. bal.

3,000

+

1,000

+

(60)

=

0

+

3,940

0

–

0

=

0

0

1.

0

+

(40)

+

40

=

0

+

0

0

–

0

=

0

0

2.

0

+

6,500

+

0

=

0

+

6,500

6,500

–

0

=

6,500

0

3.

5,400

+

(5,400)

+

0

=

0

+

0

0

–

0

=

0

5,400 OA

4.

0

+

5

+

(5)

=

0

+

0

0

–

0

=

0

0

5.

5

+

(5)

+

0

=

0

+

0

0

–

0

=

0

5 OA

6.

0

+

0

+

(65)

=

0

+

(65)

0

–

65

=

(65)

0

Totals

8,405

+

2,060

+

(90)

=

0

+

10,375

6,500

–

65

=

6,435

5,405 NC

Copyright © McGraw-Hill Education. Permission required for reproduction or display.

7-11

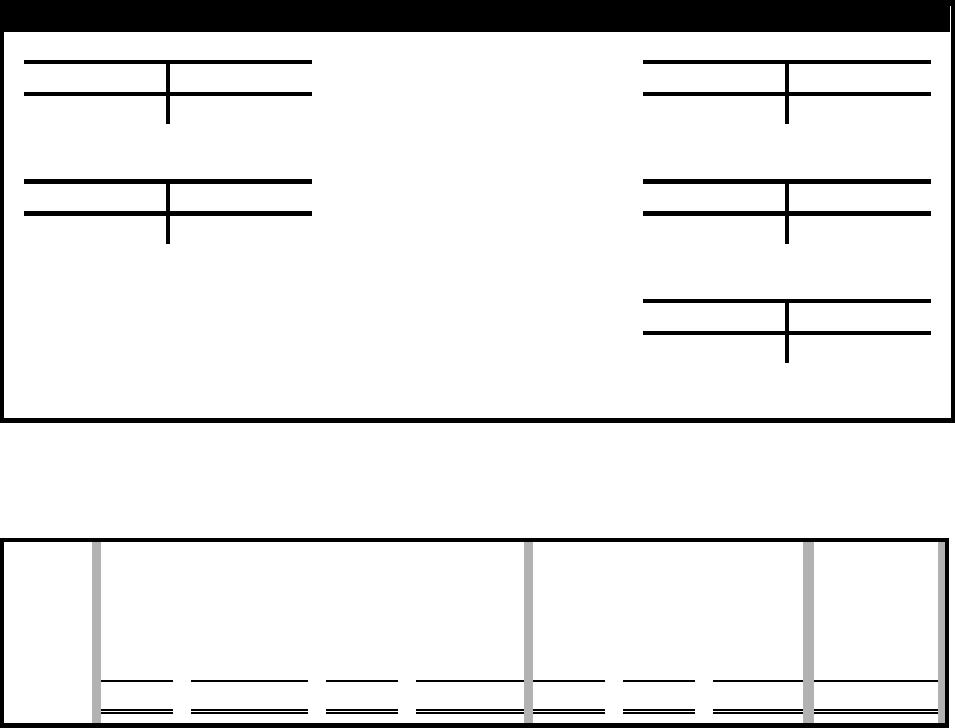

Demonstration Problem 7-2 Solution, part a. T-accounts

Ledger T-Accounts

Cash

Retained Earnings

(2) 7,600

7,600 cl

Bal. 7,600

7,600Bal.

Accounts Receivable

Service Revenue

(1) 7,600

7,600 (2)

cl. 8,000

8,000 (1)

Credit Card Expense

(1) 400

400 cl

Demonstration Problem 7-2 Solution, part b. Statements Model

Event

Assets

=

Liab.

+

Equity

Rev.

–

Exp.

=

Net Inc.

Cash Flow

No.

Cash

+

Accts. Rec.

=

W. Pay

Ret. Earn.

Beg. bal.

0

+

0

=

0

+

0

0

–

0

=

0

0

1.

0

+

7,600

=

0

+

7,600

8,000

–

400

=

7,600

0

2.

7,600

+

(7,600)

=

0

+

0

0

–

0

=

0

7,600 OA

Totals

7,600

+

0

=

0

+

7,600

8,000

–

400

=

7,600

7,600