Archives

978-1259722653 Appendix Appendix

Financial Reporting and Analysis (7th Ed.) Appendix B Solutions Essentials of Financial Statement Analysis Exercises EB-1 Determining reportable segments (LO B-1) (AICPA adapted) ASC 280 provides quantitative guidelines for reporting segments. A company must report separate segment information if either […]

978-1259722653 Chapter 1 Solution Manual Part 1

Financial Reporting and Analysis (7th Ed.) Chapter 1 Solutions The Economic and Institutional Setting for Financial Reporting Problems Problems P1-1. Demand for accounting information (LO 1-1) Requirement 1: a) Existing shareholders use financial accounting information as part of their ongoing […]

978-1259722653 Chapter 1 Solution Manual Part 2

P1-6. Relevance versus faithful representation (LO 1-1) Requirement 1: The Blue Book average price is more relevant to the car buying decision than is the list (or fisticker”) price shown on the manufacturer’s web site. Why? Because it better represents […]

978-1259722653 Chapter 1 Solution Manual Part 3

P1-14. Debt Covenants and Aggressive Accounting Practices (LO 1-4) Requirement 1: When a company violates its debt covenants, lenders can respond in any of several ways. They can simply waive the violation which is akin to a “slap on the […]

978-1259722653 Chapter 10 Solution Manual Part 1

Financial Reporting and Analysis (7th Ed.) Chapter 10 Solutions Long-Lived Assets and Depreciation Exercises Exercises E10-1. Capitalizing costs (LO 10-2) Phoenix may capitalize the following costs to the Machine account: The finder’s fee, list price, transportation fee and installation fee […]

978-1259722653 Chapter 10 Solution Manual Part 2

Financial Reporting and Analysis (6th Ed.) Chapter 10 Solutions Long-Lived Assets and Depreciation Problems Problems P10-1. Computing depreciation expense – SL, DDB, SYD, and UP (LO 10-7) (AICPA adapted) The table below shows the amount of depreciation expense in 2017 […]

978-1259722653 Chapter 10 Solution Manual Part 3

P10-16. Making asset age and intercompany comparisons (LO 10-3) Requirement 1: ROA for Gardenia Co. (000s omitted): Jan. 1 Dec. 31 Dec. 31 Dec. 31 Dec. 31 Dec. 31 2017 2017 2018 2019 2020 2021 © 2018 by McGraw-Hill Education. […]

978-1259722653 Chapter 10 Solution Manual Part 4

P10-21. IFRS impairment and revaluation (LO 10-10) Requirement 1: Cost model 12/31/2016: No entry 12/31/2017: 12/31/2018: DR Land €100,000 CR Impairment reversal: land €100,000 Requirement 2: Revaluation model 12/31/2016: DR Land €150,000 CR Revaluation surplus €150,000 12/31/2017: DR Revaluation surplus […]

978-1259722653 Chapter 11 Solution Manual Part 1

Financial Reporting and Analysis (7th Ed.) Chapter 11 Solutions Financial Instruments and Liabilities Exercises Exercises E11-1. Finding the issue price (LO 11-2) (AICPA adapted) We know that the bonds were priced to yield 8% when the contract interest rate was […]

978-1259722653 Chapter 11 Solution Manual Part 2

Financial Reporting and Analysis (7th Ed.) Chapter 11 Solutions Financial Instruments and Liabilities Problems/Discussion Questions Problems P11-1. Imputing interest (LO 11-3) Requirement 1: To verify that the imputed interest rate on the dealer’s loan is 6%, compute the present value […]

978-1259722653 Chapter 11 Solution Manual Part 3

P11-6. Call options as investments (LO 11-7) Required entries for 1 through 3: July 1, 2017: July 31, 2017: DR Unrealized holding loss on stock options $75 CR Market adjustment—stock options $75 August 31, 2017: DR Market adjustment—stock options $1,950 […]

978-1259722653 Chapter 11 Solution Manual Part 4

P11-11. Discount and premium amortization (LO 11-2) Requirement 1: The carrying values of both bonds in each of the two years presented is simply equal to the present value of the principal and interest payments discounted over the remaining life […]

978-1259722653 Chapter 11 Solution Manual Part 5

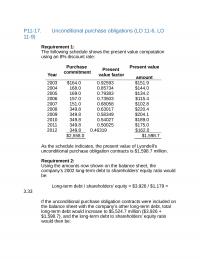

P11-17. Unconditional purchase obligations (LO 11-6, LO 11-9) Requirement 1: The following schedule shows the present value computation using an 8% discount rate: Year Purchase commitment Present value factor Present value amount Requirement 2: Using the amounts now shown on […]

978-1259722653 Chapter 11 Solution Manual Part 6

P11-23. Hedging a Planned Sale (LO 11-7, LO 11-8) Requirement 1: Newton plans to sell some of its corn inventory next March, six months from now (October). This sale will take place at the March market price. However, Newton does […]

978-1259722653 Chapter 11 Solution Manual Part 7

C11-2 Tuesday Morning Corporation: Interpreting long-term debt disclosures Requirement 1: Requirement 2: $1,298 from the cash flow statement Requirement 3: The difference is $104. This appears to suggest that payment on the note payable in Note 5 was not made […]

978-1259722653 Chapter 12 Solution Manual Part 1

Financial Reporting and Analysis (7th Ed.) Chapter 12 Solutions Financial Reporting for Leases Exercises Exercises E12-1. Accounting for lessee with purchase option under ASC 840 (LO 12-3) Requirement 1: Amount capitalized by Leland at 07/01/2017 The $100,000 represents a bargain […]

978-1259722653 Chapter 12 Solution Manual Part 2

E12-8. Determining lease payment and depreciation amounts for a capital lease (LO 12-1, LO 12-3, LO 12-5) Note that the calculations will be the same for a finance lease under ASC 842. Part 1 – Lease payment computations Case 1 […]

978-1259722653 Chapter 12 Solution Manual Part 3

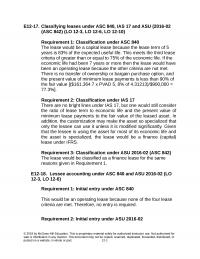

E12-17. Classifying leases under ASC 840, IAS 17 and ASU (2016-02 (ASC 842) (LO 12-3, LO 12-6, LO 12-10) Requirement 1: Classification under ASC 840 The lease would be a capital lease because the lease term of 5 years is […]

978-1259722653 Chapter 12 Solution Manual Part 4

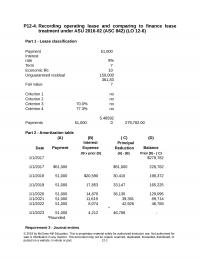

P12-4. Recording operating lease and comparing to finance lease treatment under ASU 2016-02 (ASC 842) (LO 12-6) Part 1 – Lease classification Part 2 – Amortization table (A) (B) ( C) (D) Interest Principal Date Payment Expense Reduction Balance .09 […]

978-1259722653 Chapter 12 Solution Manual Part 5

P12-9. Recording capital lease for lessee and comparing to operating lease treatment under ASC 840 (LO 12-2, LO12-3, LO12-5) Part A – June 30 reporting year Requirement 1: Lease criteria This is a capital lease for Burgundy because the lease […]

978-1259722653 Chapter 12 Solution Manual Part 6

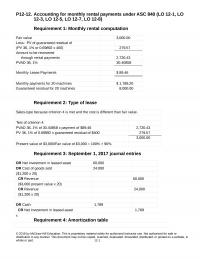

P12-12. Accounting for monthly rental payments under ASC 840 (LO 12-1, LO 12-3, LO 12-5, LO 12-7, LO 12-8) Requirement 1: Monthly rental computation Requirement 2: Type of lease Sales-type because criterion 4 is met and the cost is different […]

978-1259722653 Chapter 12 Solution Manual Part 7

P12-16. Evaluating sale and leaseback under ASC 840 and ASU 2016-02 (ASC 842) (LO 12-3, LO 12-4, LO 12-6) Requirement 1: Lease type under ASC 840 This is a capital lease for Merchant because the lease meets at least one […]

978-1259722653 Chapter 13 Solution Manual Part 1

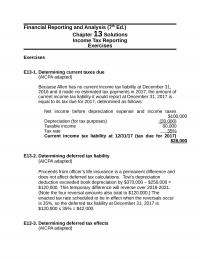

Financial Reporting and Analysis (7th Ed.) Chapter 13 Solutions Income Tax Reporting Exercises Exercises E13-1. Determining current taxes due (AICPA adapted) Because Allen has no current income tax liability at December 31, 2016 and it made no estimated tax payments […]

978-1259722653 Chapter 13 Solution Manual Part 2

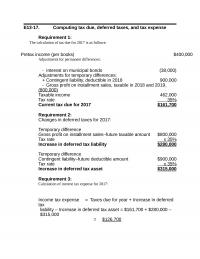

E13-17. Computing tax due, deferred taxes, and tax expense Requirement 1: The calculation of tax due for 2017 is as follows: Requirement 2: Changes in deferred taxes for 2017: Temporary difference Gross profit on installment sales–future taxable amount $800,000 Tax […]

978-1259722653 Chapter 13 Solution Manual Part 3

P13-7. Tax rate reconciliation schedules for IFRS vs. U.S. GAAP Note: If the weighted average tax rate or effective rate is rounded before doing Calculations relevant to both reconciliations: Country X Country Y Total Pre-tax Book Income (1) $1,250,000 $1,100,000 […]

978-1259722653 Chapter 13 Solution Manual Part 4

P13-15. Financial statement effects of tax rate change Requirement 1: Both companies project pretax income of $100 million. Because there are no permanent differences and no change in cumulative temporary differences in 2017 for either company, both are also Requirement […]

978-1259722653 Chapter 13 Solution Manual Part 5

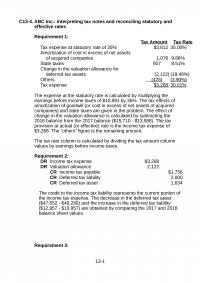

C13-4. ABC Inc.: Interpreting tax notes and reconciling statutory and effective rates Requirement 1: Tax Amount Tax Rate The expense at the statutory rate is calculated by multiplying the earnings before income taxes of $10,891 by 35%. The tax effects […]

978-1259722653 Chapter 14 Solution Manual Part 1

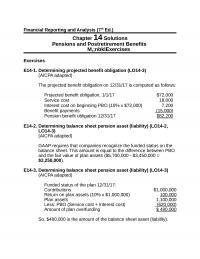

Financial Reporting and Analysis (7th Ed.) Chapter 14 Solutions Pensions and Postretirement Benefits M,;nbklExercises Exercises E14-1. Determining projected benefit obligation (LO14-3) (AICPA adapted) The projected benefit obligation on 12/31/17 is computed as follows: Pension benefit obligation 12/31/17 $82 ,200 E14-2. […]

978-1259722653 Chapter 14 Solution Manual Part 2

E14-16. Determining postretirement health care expenses and plan assets and liabilities balances (LO14-7) Requirement 1: Determination of postretirement health care expense for 2017: Service cost $20,000 Interest on accumulated benefit obligation Recognized actuarial loss 7 ,000 Postretirement expense $58 ,000 […]

978-1259722653 Chapter 14 Solution Manual Part 3

Financial Reporting and Analysis (7th Ed.) Chapter 14 Solutions Pensions and Postretirement Benefits Problems Problems P14-1. Determining components of pension expense (LO14-3, LO14-4, LO14-6) Requirement 1: Interest cost Beginning balance of PBO $600,000 Requirement 2: Expected dollar return on plan […]

978-1259722653 Chapter 14 Solution Manual Part 4

P14-5. Calculating PBO, ABO and pension expense (LO 14-1, LO 14-2, LO 14-3) Requirement 1: Calculation of PBO on January 1, 2017: Annual pension benefits starting on 12/31/2031 and continuing for 10 years thereafter (11 years total = 76 – […]

978-1259722653 Chapter 14 Solution Manual Part 5

Requirement 1: Annual pension expense Assumptions: Discount rate = 8% and rate of return on plan assets = 10% End of Year 1 Annual Salary 2 Cumulative Salary 3 Total Vested Pension 4 Vested During the Year 5 Discount Period […]

978-1259722653 Chapter 14 Solution Manual Part 6

P14-12 Evaluating the effects of unreasonable rate of return assumptions (LO14-3, LO14-4, LO14-6, LO14-9) Requirement 1: US GAAP pension expense New Service Cost $300.00 0 = Pension expense / (income) ($223.80) *0.075 x $6,200 = $465 **[$900 actuarial loss – […]

978-1259722653 Chapter 15 Solution Manual Part 1

Financial Reporting and Analysis (7th Ed.) Chapter 15 Solutions Financial Reporting for Owners’ Equity Exercises Exercises E15-1.Understanding Shareholders’ Equity (LO 15-1, LO 15-3, LO 15-6, LO 15-7) Requirement 1: Preferred stock is a class of “capital stock” that pays dividends […]

978-1259722653 Chapter 15 Solution Manual Part 2

P15-5. Analyzing convertible debt (LO 15-9) (AICPA adapted) Requirement 1: Journal entry to record the original issuance of the $10 million convertible bond at par: Notice that this entry does not assign any value to the conversion option. The FASB […]

978-1259722653 Chapter 15 Solution Manual Part 3

P15-12. Calculating EPS when the capital structure is complex (LO 15-6) Requirement 1: The preferred stock pays a 10% dividend ($500,000), so there must be $5 million of preferred stock outstanding. Since each each $100 par value preferred share must […]

978-1259722653 Chapter 15 Solution Manual Part 4

P15-19. Stock option accounting: Transitioning to current GAAP (LO 15-6) Requirement 1: Under the intrinsic value method allowed by pre-Codification SFAS No. 123, but later disallowed by pre-Codification SFAS No. 123(R), share. In this case, Riley would record $300 of […]

978-1259722653 Chapter 15 Solution Manual Part 5

C15-4. Salesforce.com: Interpreting Share-based Compensation Disclosures (LO 15-7, LO 15-8) All answers involving financial statement amounts are in thousands. Requirement 1: 2015 share-based compensation expense and classification The total amount of share-based compensation expense is $564,765. It The entry would […]

978-1259722653 Chapter 16 Solution Manual Part 1

Financial Reporting and Analysis (7th Ed.) Chapter 16 Solutions Intercorporate Investments Exercises Exercises E16-1. Accounting for trading and available-for-sale securities (AICPA adapted) Requirement 1: Only the unrealized holding gains/losses from trading securities are fair value from 12/31/16 to 12/31/17 = […]

978-1259722653 Chapter 16 Solution Manual Part 2

Financial Reporting and Analysis (7th Ed.) Chapter 16 Solutions Intercorporate Investments Exercises Exercises E16-1. Accounting for trading and available-for-sale securities (AICPA adapted) Requirement 1: Only the unrealized holding gains/losses from trading securities are recognized as income. from 12/31/16 to 12/31/17 […]

978-1259722653 Chapter 16 Solution Manual Part 3

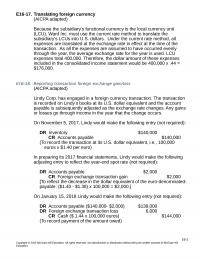

E16-17. Translating foreign currency (AICPA adapted) Because the subsidiary’s functional currency is the local currency unit (LCU), Ward Inc. must use the current rate method to translate the included in the consolidated income statement would be 400,000 x .44 = […]

978-1259722653 Chapter 16 Solution Manual Part 4

P16-4. Equity method and fair value option Requirement 1: The determination of excess cost and its allocation is as follows: 2017 Journal entries: January 1, 2017 – Initial acquisition DR Investment in Delta Crating $250 $100 million) To record additional […]

978-1259722653 Chapter 16 Solution Manual Part 5

P16-8. Elimination entries and consolidated balance sheet under acquisition method 16-1 Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. Requirement 3: Plate Salad Eliminations Consolidated Dr Cr Balance […]

978-1259722653 Chapter 17 Solution Manual Part 1

Financial Reporting & Analysis (7th Ed.) Chapter 17 Solutions Statement of Cash Flows Exercises Exercises E17-1. Deriving a direct method presentation of cash flow from operating activities ABC Mining Company Cash Flow from Operations For the Year Ended December 31, […]

978-1259722653 Chapter 17 Solution Manual Part 2

P17-2. Cash flow statement under indirect method 17-1 Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. P17-3. Determining amounts reported on statement of cash flows (AICPA adapted) Requirement […]

978-1259722653 Chapter 17 Solution Manual Part 3

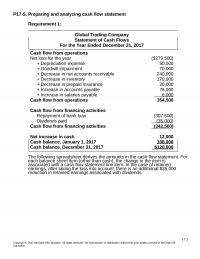

P17-5. Preparing and analyzing cash flow statement Requirement 1: Global Trading Company Statement of Cash Flows For the Year Ended December 31, 2017 Cash flow from operations Net loss for the year ($279,500) Cash flow from operations 354,500 Cash flow […]

978-1259722653 Chapter 17 Solution Manual Part 4

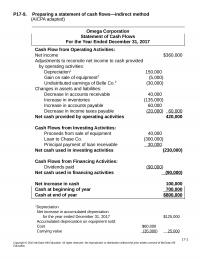

P17-9. Preparing a statement of cash flows—indirect method (AICPA adapted) Omega Corporation Statement of Cash Flows For the Year Ended December 31, 2017 Cash Flow from Operating Activities: Net income $360,000 Adjustments to reconcile net income to cash provided by […]

978-1259722653 Chapter 17 Solution Manual Part 5

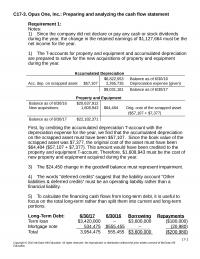

C17-3. Opus One, Inc.: Preparing and analyzing the cash flow statement Requirement 1: Notes: 1) Since the company did not declare or pay any cash or stock dividends 1) The T-accounts for property and equipment and accumulated depreciation are prepared […]

978-1259722653 Chapter 2 Solution Manual Part 1

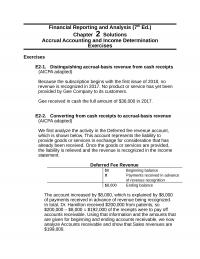

Financial Reporting and Analysis (7th Ed.) Chapter 2 Solutions Accrual Accounting and Income Determination Exercises Exercises E2-1. Distinguishing accrual-basis revenue from cash receipts (AICPA adapted) Because the subscription begins with the first issue of 2018, no E2-2. Converting from cash […]

978-1259722653 Chapter 2 Solution Manual Part 2

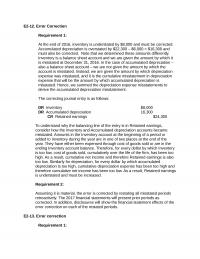

E2-12. Error Correction Requirement 1: At the end of 2016, inventory is understated by $8,000 and must be corrected. Accumulated depreciation is overstated by $22,300 – $6,000 = $16,300 and must also be corrected. Note that we determined these amounts […]

978-1259722653 Chapter 2 Solution Manual Part 3

P2-3. Understanding the accounting equation Flaps Inc. Balance Sheet Year 2016 2017 2018 2019 2020 Assets Stockholders’ Equity Common stock 138 139 140 142 144 Additional paid-in capital 2,202 2,216 2,247 2,280 2,296 Contributed capital 2,340 2,355 2,387 2,422 2,440 […]

978-1259722653 Chapter 2 Solution Manual Part 4

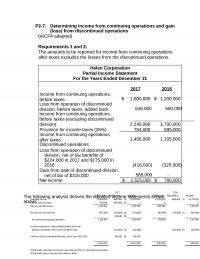

P2-7. Determining income from continuing operations and gain (loss) from discontinued operations (AICPA adapted) Requirements 1 and 2: The amounts to be reported for income from continuing operations after taxes excludes the losses from the discontinued operations. Helen Corporation Partial […]

978-1259722653 Chapter 2 Solution Manual Part 5

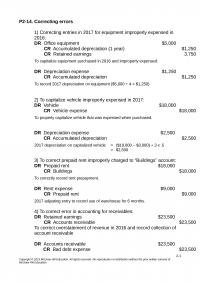

P2-14. Correcting errors 1) Correcting entries in 2017 for equipment improperly expensed in 2016: To capitalize equipment purchased in 2016 and improperly expensed. DR Depreciation expense $1,250 CR Accumulated depreciation $1,250 To record 2017 depreciation on equipment ($5,000 ÷ 4 […]

978-1259722653 Chapter 3 Solution Manual Part 1

Financial Reporting and Analysis (7th Edition) Chapter 3 Solutions Revenue Recognition Exercises Note: Exercises E3-1 through E3-4 deal with when a contract subject to the revenue recognition rules exists. In order for a contract to exist that is subject to […]

978-1259722653 Chapter 3 Solution Manual Part 2

E3-20. Breakage The following analysis shows the amount of breakage revenue Ashley recognizes in each year. At the end of 2019, Ashley estimates that $300 of gift cards will not be redeemed. Gift card redemptions to date have totaled $12,000 […]

978-1259722653 Chapter 3 Solution Manual Part 3

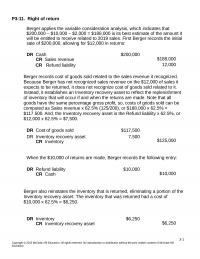

P3-11. Right of return Berger applies the variable consideration analysis, which indicates that $200,000 – $10,000 – $2,000 = $188,000 is its best estimate of the amount it will be entitled to receive related to 2019 sales. First Berger records […]

978-1259722653 Chapter 4 Solution Manual Part 1

Financial Reporting and Analysis (7th Ed.) Chapter 4 Solutions Structure of the Balance Sheet and Statement of Cash Flows Exercises Exercises E4-1. Analyzing balance sheet classification b Long-term receivables (d) Accumulated amortization f Current maturities of long-term debt c Machinery […]

978-1259722653 Chapter 4 Solution Manual Part 2

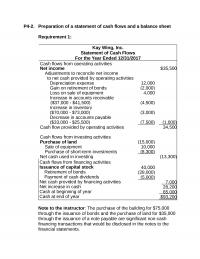

P4-2. Preparation of a statement of cash flows and a balance sheet Requirement 1: Kay Wing, Inc. Statement of Cash Flows For the Year Ended 12/31/2017 Cash flows from operating activities Net income $35,500 Adjustments to reconcile net income to […]

978-1259722653 Chapter 4 Solution Manual Part 3

P4-10. Understanding the relation between operating cash flows and accrual earnings Requirement 1: Sales1 ($28,000 + $3,000) $31,000 Less: 1Collections from customers + decrease in accounts receivable. 2Payment to suppliers for purchases + increase in accounts payable – increase in […]

978-1259722653 Chapter 4 Solution Manual Part 4

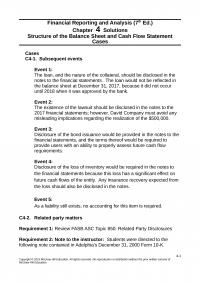

Financial Reporting and Analysis (7th Ed.) Chapter 4 Solutions Structure of the Balance Sheet and Cash Flow Statement Cases Cases C4-1. Subsequent events Event 1: The loan, and the nature of the collateral, should be disclosed in the notes to […]

978-1259722653 Chapter 5 Solution Manual Part 1

Financial Reporting and Analysis (7th Ed.) Chapter 5 Solutions Essentials of Financial Statement Analysis Exercises Exercises E5-1 Calculating profitability ratios (AICPA adapted) E5-2 Determining inventory turnover (AICPA adapted) E5-3 Determining receivable turnover (AICPA adapted) Accounts receivable turnover = Total credit […]

978-1259722653 Chapter 5 Solution Manual Part 2

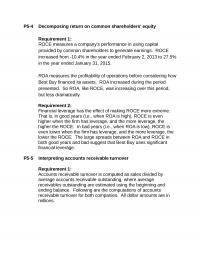

P5-4 Decomposing return on common shareholders’ equity Requirement 1: ROCE measures a company’s performance in using capital provided by common shareholders to generate earnings. ROCE ROA measures the profitability of operations before considering how Best Buy financed its assets. ROA […]

978-1259722653 Chapter 5 Solution Manual Part 3

P5-14 Explaining changes in financial ratios (AICPA adapted) 1) a,b,d Inventory turnover is defined as the cost of goods sold divided by average inventory. A lower inventory would cause the inventory turnover ratio to increase, as would a higher cost […]

978-1259722653 Chapter 6 Solution Manual Part 1

Financial Reporting and Analysis (7th Ed.) Chapter 6 Solutions The Role of Financial Information in Valuation and Credit Risk Assessment Problems/Discussion Questions Exercises E6-1. Free cash flow valuation Requirement 1: Although the exact definition of “free cash flow” varies in […]

978-1259722653 Chapter 6 Solution Manual Part 2

Financial Reporting and Analysis (7th Ed.) Chapter 6 Solutions The Role of Financial Information in Valuation and Credit Risk Assessment Problems/Discussion Questions Problems P6-1 Interpreting stock price changes Requirement 1: AMD’s announcement differed from analysts’ expectations and presumably also from […]

978-1259722653 Chapter 6 Solution Manual Part 3

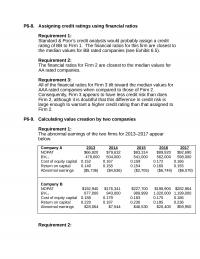

P6-8. Assigning credit ratings using financial ratios Requirement 1: Standard & Poor’s credit analysts would probably assign a credit Requirement 2: The financial ratios for Firm 2 are closest to the median values for AA rated companies. Requirement 3: All […]

978-1259722653 Chapter 6 Solution Manual Part 4

Financial Reporting and Analysis (7th Ed.) Chapter 6 Solutions The Role of Financial Information in Valuation, Cash Flow Analysis, and Credit Risk Assessment Cases Cases C6-1. Illinois Tool Works: Abnormal earnings valuation Requirements 1 and 2: The template solution (shown […]

978-1259722653 Chapter 7 Solution Manual Part 1

Financial Reporting and Analysis (7th Ed.) Chapter 7 Solutions The Role of Financial Information in Contracting Exercises Exercises E7-1. Understanding debt covenants Debt covenants are restrictive provisions written into loan agreements. They are designed to reduce potential conflicts of interest […]

978-1259722653 Chapter 7 Solution Manual Part 2

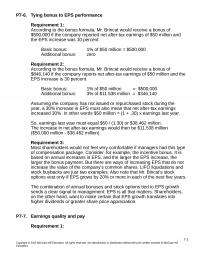

P7-6. Tying bonus to EPS performance Requirement 1: According to the bonus formula, Mr. Brincat would receive a bonus of $500,000 if the company reported net after-tax earnings of $50 million and the EPS increase was 10 percent. Requirement 2: […]

978-1259722653 Chapter 8 Solution Manual Part 1

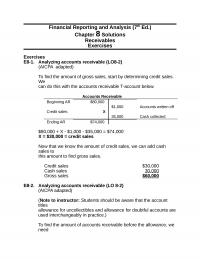

Financial Reporting and Analysis (7th Ed.) Chapter 8 Solutions Receivables Exercises Exercises E8-1. Analyzing accounts receivable (LO8-2) (AICPA adapted) To find the amount of gross sales, start by determining credit sales. We can do this with the accounts receivable T-account […]

978-1259722653 Chapter 8 Solution Manual Part 2

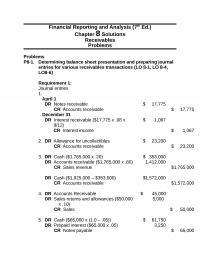

Financial Reporting and Analysis (7th Ed.) Chapter 8 Solutions Receivables Problems Problems P8-1. Determining balance sheet presentation and preparing journal entries for various receivables transactions (LO 8-1, LO 8-4, LO8-6) Requirement 1: Journal entries 1. April 1 x .10) CR […]

978-1259722653 Chapter 8 Solution Manual Part 3

P8-7. Scheduling interest received (LO 8-4) Effective interest table in 000’s ( a ) ( b ) ( c ) ( d ) Date Interest income – prior (d) x 11.12%) Note payment received (given) Total cash received (a) + […]

978-1259722653 Chapter 8 Solution Manual Part 4

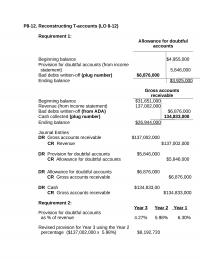

P8-12. Reconstructing T-accounts (LO 8-12) Requirement 1: Allowance for doubtful accounts Gross accounts receivable Beginning balance $31,651,000 Revenue (from income statement) 137,002,000 Bad debts written-off (from ADA) $6,876,000 Cash collected (plug number) 134,833,000 Ending balance $26,944,000 Journal Entries DR Gross […]

978-1259722653 Chapter 8 Solution Manual Part 5

P8-15. Accounting for transfer of receivables (LO 8-6) It seems that Ricoh Company is treating the discounting of receivables as a sale. Note that Ricoh indicates that “trade notes receivable discounted are contingent liabilities.” If Ricoh had treated the Crown […]

978-1259722653 Chapter 9 Solution Manual Part 1

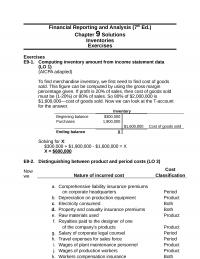

Financial Reporting and Analysis (7th Ed.) Chapter 9 Solutions Inventories Exercises Exercises E9-1. Computing inventory amount from income statement data (LO 1) (AICPA adapted) To find merchandise inventory, we first need to find cost of goods sold. This figure can […]

978-1259722653 Chapter 9 Solution Manual Part 2

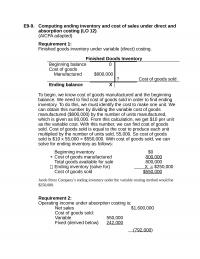

E9-9. Computing ending inventory and cost of sales under direct and absorption costing (LO 12) (AICPA adapted) Requirement 1: Finished goods inventory under variable (direct) costing. Finished Goods Inventory To begin, we know cost of goods manufactured and the beginning […]

978-1259722653 Chapter 9 Solution Manual Part 3

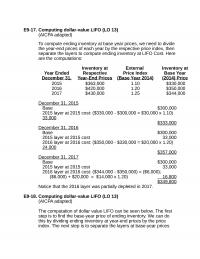

E9-17. Computing dollar-value LIFO (LO 13) (AICPA adapted) To compute ending inventory at base year prices, we need to divide the year-end prices of each year by the respective price index, then separate the layers to compute ending inventory at […]

978-1259722653 Chapter 9 Solution Manual Part 4

P9-4. Determining the effects of absorption and variable costing (LO 12) Requirement 1: Absorption Cost: 2017 Ending inventory [55,000 @ $8] Absorption Cost: 2018 Sales revenue [85,000 @ $10] $850,000 Cost of goods sold: From beginning inventory [55,000 @ $8] […]

978-1259722653 Chapter 9 Solution Manual Part 5

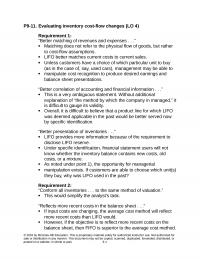

P9-11. Evaluating inventory cost-flow changes (LO 4) Requirement 1: “Better matching of revenues and expenses . . .” Matching does not refer to the physical flow of goods, but rather to cost-flow assumptions. “Better correlation of accounting and financial information […]

978-1259722653 Chapter 9 Solution Manual Part 6

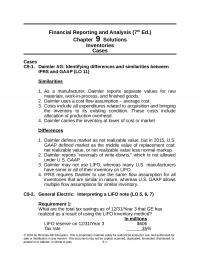

Financial Reporting and Analysis (7th Ed.) Chapter 9 Solutions Inventories Cases Cases C9-1. Daimler AG: Identifying differences and similarities between IFRS and GAAP (LO 11) Similarities 1. As a manufacturer, Daimler reports separate values for raw 2. Daimler uses a […]

Accounting Chapter 1 1 The SEC retains enforcement authority over financial reporting in the

Chap001 The Economic and Institutional Setting for Financial Reporting True/False [QUESTION] 1. The role of financial accounting information is to facilitate economic transactions and to foster efficient allocation of resources among businesses and individuals. Answer: True Learning Objective: 01-01 Difficulty: […]

Accounting Chapter 1 2 only when managers wanted to raise additional capital

Learning Objective: 01-02 Difficulty: 2 Medium AACSB: Reflective Thinking AICPA: BB Resource Management AICPA: FN Risk Analysis Blooms: Understand Topic: Financial statements―For decision-maker needs [QUESTION] 53. Which of the following people outside the company do not demand financial statement information […]

Accounting Chapter 10 1 Us Coast Guard January 2018 And completed Construction

Chap010 Long-Lived Assets and Depreciation True/False [QUESTION] 1. The method of measuring long-lived assets at their estimated value in an output market is the expected benefit approach. Answer: True Learning Objective: 10-01 Difficulty: 1 Easy AACSB: Reflective Thinking AICPA: FN […]

Accounting Chapter 10 2 A liability is recorded with a credit entry in a contra-asset account

[QUESTION] 54. The FASB has been able to guard against management manipulation of earnings as a result of asset impairments by a. fining any managers found guilty of such manipulation. b. requiring restoration of previously recognized impairment losses. c. prohibiting […]

Accounting Chapter 10 3 Due The Rapid Rate Technological Change The industry

Difficulty: 2 Medium AACSB: Knowledge Application AICPA: FN Measurement AICPA: BB Critical Thinking Blooms: Apply Topic: Costs apportioned from lump-sum purchase [QUESTION] 87. Denver Co. acquired a large rotary forge to be used in its manufacturing process from a competitor […]

Accounting Chapter 11 1 The gain or loss on the early retirement of a bond is

CHAPTER 11 Financial Instruments and Liabilities Chapter 11 Financial Instruments and Liabilities True-False 1. A liability that is satisfied through the payment of cash is referred to as a denominational lia- bility. Answer: False Learning Objective: 11-01 Difficulty: 1 Easy […]

Accounting Chapter 11 2 For the year ending December 31, 2019, Ross will report an unrealized

CHAPTER 11 Financial Instruments and Liabilities Use the following to answer questions 53 and 54: REFERENCE: Ref. 11_03 Dot Company issued $200,000 of bonds on January 1, 2018 with interest payable each year. The bonds had a stated rate of […]

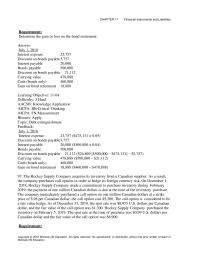

Accounting Chapter 11 3 Access Cost effective Financing can Result Interest Rate Andor

CHAPTER 11 Financial Instruments and Liabilities Requirement: Determine the gain or loss on the bond retirement. Answer: July 1, 2018 Interest expense 23,757 Discount on bonds payable 3,757 Interest payable 20,000 Bonds payable 500,000 Discount on bonds payable 21,112 Carrying […]

Accounting Chapter 12 1 Measurement blooms Analyze topic Lessee Incentives For Type Lease topic

Chapter 12 Financial Reporting for Leases True-False 1. Under ASC 840, when accounting for an operating lease, a liability is recognized when the lease is signed by the lessee. Answer: False Learning Objective: 12-01 Difficulty: 1 Easy AACSB: Reflective Thinking […]

Accounting Chapter 12 2 Which The Following Does Not Properly

CHAPTER 12 Financial Reporting for Leases AACSB: Knowledge Application AICPA: BB Critical Thinking AICPA: FN Measurement Blooms: Apply Topic: ASC 840―Lessor accounting Topic: ASC 842―Lessor accounting Feedback: Manufacturing profit = selling price $32,000 – manufacturing cost $25,000 = $7,000 [QUESTION] […]

Accounting Chapter 12 3 December 31 2018 With Respect Toconroy Companys

CHAPTER 12 Financial Reporting for Leases d. Cash receipts from leases are shown in the operating activities section of the statement of cash flows. Answer: a Learning Objective: 12-09 Difficulty: 2 Medium AACSB: Reflective Thinking AICPA: BB Critical Thinking AICPA: […]

Accounting Chapter 13 1 To Ref 130237 Income Tax Expense Reported

CHAPTER 13 Income Tax Reporting 185 Chapter 13: Income Tax Reporting True-False 1. Taxable income is governed by the doctrine of constructive receipt or ability to pay. Answer: True Learning Objective: 13-01 Difficulty: 1 Easy AICPA: BB Critical Thinking AICPA: […]

Accounting Chapter 13 2 Generating Deferred Tax Liabilities Always Increases Cash

CHAPTER 13 Income Tax Reporting 205 AACSB: Knowledge Application Blooms: Apply Topic: Tax rate changes Feedback: $100,000 × 2% [42% − 40%*] = $2,000 increase in the deferred tax liability which increases income tax expense. * The current tax rate […]

Accounting Chapter 13 3 Shuman Purchased Landscape Maintenance Firm 12

CHAPTER 13 Income Tax Reporting 219 Requirement: Prepare the journal entry to record income tax expense for the year ended December 31, 2019. Answer: December 31, 2019 Income tax expense 159,080 Deferred tax asset 30,000 (3) Deferred tax liability 64,000 […]

Accounting Chapter 14 1 The Company Contributes 130000 Cash The

Chapter 14 Pensions and Postretirement Benefits True-False 1. The return on the pension fund impacts the employer’s periodic pension expense for defined contribution pension plans. Answer: False Learning Objective: 14-01 Difficulty: 2 Medium AICPA: BB Critical Thinking AICPA: FN Measurement […]

Accounting Chapter 14 2 Analysts Reporting Companies Will Pay Close

CHAPTER 14 Pensions and Postretirement Benefits DR Pension asset 10,000 CR Cash 130,000 c. DR Pension expense 130,000 CR Cash 130,000 d. DR Pension expense 160,000 CR Cash 130,000 CR Pension asset (liability) 30,000 Answer: d Learning Objective: 14-03 Difficulty: […]

Accounting Chapter 14 3 The projected benefit obligation as of January 1, 2018

CHAPTER 14 Pensions and Postretirement Benefits 87. The income statement reporting for other postretirement benefits (OPEB) is based on the a. cash basis of accounting. b. accrual basis of accounting. c. cash or accrual basis of accounting. d. regulations established […]

Accounting Chapter 15 1 The Revised Model Business Corporation Act would potentially

Chapter 15 Financial Reporting for Owners’ Equity True-False 1. Net income or loss generally arises from transactions with owners who provide net capital to the firm. Answer: False Learning Objective: 15-01 Difficulty: 2 Medium AICPA: BB Critical Thinking AICPA: FN […]

Accounting Chapter 15 2 Apb No Approach Expense The Fair Value

CHAPTER 15 Financial Reporting for Owners’ Equity What is the weighted average number of shares to be used in the calculation of basic earnings per share for 2018? a. 268,500 b. 243,500 c. 248,000 d. 278,000 Answer: b Learning Objective: […]

Accounting Chapter 15 3 Purchased 5,000 shares of its common stock for $9.75 per share

CHAPTER 15 Financial Reporting for Owners’ Equity c. Black-Scholes method. d. par value method. Answer: b Learning Objective: 15-09 Difficulty: 2 Medium AICPA: BB Resource Management AICPA: FN Measurement AACSB: Reflective Thinking Blooms: Remember Topic: Convertible debt 87. Financial statement […]

Accounting Chapter 16 1 The Shasta Corporation Began Operations 2018

Chapter 16 Intercorporate Investments True-False 1. For an investor each share of common stock and each share of preferred stock owned usually entitles the owner to one vote. Answer: False Learning Objective: 16-01 Difficulty: 1 Easy AICPA: BB Legal AACSB: […]

Accounting Chapter 16 2 Which of the following is not an accurate description of the consolidated balance sheet

CHAPTER 16 Intercorporate Investments Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. 21 Topic: Fair value option accounting Feedback: $28,000 = $10,000 {unrealized gain: $210,000(fair value) – $200,000 […]

Accounting Chapter 16 3 Amc Corporation For 2000000 Amcs Net Assets

CHAPTER 16 Intercorporate Investments Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. 34 AACSB: Diversity AACSB: Knowledge Application Blooms: Apply Topic: IFRS―Investments 84. Susqua, Inc. has held-to-maturity debt […]

Accounting Chapter 17 1 Accrual accounting net income can differ from operating cash flows for all of the

Chapter 17 Statement of Cash Flows True-False 1. Accrual accounting involves subjective judgments that can introduce measurement errors and uncertainty into reported earnings. Answer: True Learning Objective: 17-02 Difficulty: 1 Easy AICPA: BB Critical Thinking AICPA: FN Measurement AACSB: Reflective […]

Accounting Chapter 17 2 The Pulaski Corporation reported the following for the year ended December 31, 2018

CHAPTER 17 Statement of Cash Flows REFER TO: Ref. 17_04 55. The cash flow from investing activities for 2019 is a a. $200,000 outflow. b. $400,000 inflow. c. $400,000 outflow. d. $600,000 inflow. Answer: c Learning Objective: 17-04 Difficulty: 3 […]

Accounting Chapter 17 3 The Following Information And Financial Statements

CHAPTER 17 Statement of Cash Flows [QUESTION] REFER TO: Ref. 17_05 87. Autumn Company uses IFRS to prepare its external financial reporting. During 2018, Autumn Company had the following transactions related to cash flows: Dividends paid 16,000 Interest paid 20,000 […]

Accounting Chapter 2 1 To get revenue and expense account balances to zero

Chap002 Accrual Accounting and Net income determination True/False [QUESTION] 1. Accrual accounting decouples measured earnings from operating cash inflows and outflows. Answer: True Learning Objective: 02-01 Difficulty: 2 Medium AACSB: Reflective Thinking AICPA: FN Measurement Blooms: Understand Topic: Accrual versus […]

Accounting Chapter 2 2 Us Gaap Allows More Opportunities For Managers

58. When using the retrospective approach for a change in accounting principle, disclosure rules require that a. prior years’ income statements presented for comparative purposes be restated to reflect use of the new principle unless it is impractical to do […]

Accounting Chapter 2 3 April 30 2019 Anestimated Gain 250000 The

a. Manipulating accrual estimates to impact expenses. b. Misapplications of GAAP deemed immaterial on an account by account basis. c. Big bath restructuring charges. d. All of these answer choices are correct. Answer: d Learning Objective: 02-12 Difficulty: 2 Medium […]

Accounting Chapter 3 1 Both public U.S. companies and companies reporting under IFRS must

Chapter 3 Revenue Recognition True/False [QUESTION] 1. The underlying principal in ASC Topic 606 is that an entity recognizes revenue to depict the transfer of promised goods or services to customers in an amount that reflects the consideration expected to […]

Accounting Chapter 3 2 Payments to a customer for slotting fees

Blooms: Understand Topic: Recognize revenue―Point in time or over time [QUESTION] 55. Which of the following statements is not applicable to revenue recognition guidance under ASC Topic 606? a. Firms must disaggregate revenues into categories that depict how revenue is […]

Accounting Chapter 3 3 The Cash Has Been Received For Goods

AICPA: FN Measurement Blooms: Understand Topic: Identify the contract [QUESTION] 86. Which of the following statements is not true regarding the software developer example provided in ASC Topic 606 guidance for revenue recognition? a. The example deals with the license […]

Accounting Chapter 4 1 Ifrs And Gaap Differences Cash Flow

File: Chapter 4 Structure of the Balance Sheet and Statement of Cash Flows True/False [QUESTION] 1. Liquidity refers to how quickly noncurrent assets will be converted into cash to pay liabilities. Answer: False Learning Objective: 04-01 Difficulty: 2 Medium AACSB: […]

Accounting Chapter 4 2 an increase in Accounts Payable is added to determine cash flow from

AACSB: Analytical Thinking AICPA: FN Critical Thinking Blooms: Analyze Topic: Balance sheet—Classification [QUESTION] 63. A consolidated balance sheet a. includes the net assets of the parent company and all of its subsidiaries. b. reports separately the net assets of the […]

Accounting Chapter 5 1 In the highest-risk Standard &Poor’s rating category that

Chap005 Essentials of Financial Statement Analysis True/False [QUESTION] 1. An analyst interested in learning the degree to which a company’s earnings have fluctuated historically in relation to changes in economic growth would employ cross-sectional analysis. Answer: False Learning Objective: 05-01 […]

Accounting Chapter 5 2 Which The Following Does Not Describe

[QUESTION] REFER TO: Ref. 05_03 58. In a common size balance sheet for 2019, accounts receivable is expressed as: a. 86%. b. 116.3%. c. 32.4%. d. 16.3%. Answer: c Feedback: $267,500 ÷ $825,000 = 32.4%. Learning Objective: 05-01 Difficulty: 2 […]

Accounting Chapter 5 3 Why is Sara Lee less profitable than Panera Bread?

Topic: Information from cash flow to assess credit risk [QUESTION] 87. Which of the following factors does not negatively impact operating cash flows? a. Accounts receivable are increasing. b. Inventories are increasing. c. Operating costs are increasing faster than sales. […]

Accounting Chapter 6 1 If securities markets are rational and efficient in that they

Chapter 6 The Role of Financial Information in Valuation and Credit Risk Assessment True/False [QUESTION] 1. The discounted cash flow valuation approach expresses current value of a firm as the discounted present value of expected future cash flows. Answer: True […]

Accounting Chapter 6 2 The Two Ways Implement The Discounted

[QUESTION] REFER TO: Ref. 06_02 55. What are the abnormal earnings for Firm C? a. $(2,400) b. $(4,800) c. $4,800 d. $9,600 Answer: b Feedback: Abnormal earnings = Actual earnings – (equity cost of capital beginning book value) = […]

Accounting Chapter 7 1 Failure Abide Covenantc Paying Interest And Principal

Chap007 The Role of Financial Information in Contracting True/False [QUESTION] 1. Contract terms can be designed to eliminate or reduce conflicting incentives that arise in business relationships. Answer: True Learning Objective: 07-01 Topic Area: Conflicts of interest―Contract effects Difficulty: 1 […]

Accounting Chapter 7 2 The Prevalence Stock Options Executive Pay

AICPA: BB Legal AICPA: FN Measurement Blooms: Understand Topic Area: Contracts for compensation purposes [QUESTION] 57. Information about a company’s executive compensation practices can be found in a company’s a. annual report. b. form 10-K. c. proxy statement. d. form […]

Accounting Chapter 8 1 The Firm Adopts New Credit Terms That

Chapter 8 Receivables True/False [QUESTION] 1. Under the sales revenue approach to estimating uncollectible accounts receivable, a loss percentage is applied to gross accounts receivable. Answer: False Learning Objective: 08-01 Difficulty: 2 Medium AACSB: Reflective Thinking AICPA: BB Critical Thinking […]

Accounting Chapter 8 2 ratios like debt-to-equity are consequently distorted by the

[QUESTION] REFER TO: Ref. 08_05 52. If the note were discounted on August 1 under the terms of agreement with National Bank, which one of the following journal entries would Jones record? a. DR Cash $39,867 CR Note payable—National Bank […]

Accounting Chapter 8 3 As a result of a review and aging of accounts

AACSB: Reflective Thinking AICPA: BB Resource Management AICPA: FN Risk Analysis Blooms: Understand Topic: Receivables management―Sale Essay and Computational Questions [QUESTION] 86. For the month of December 2018, the records of Seal Corporation show the following information: Cash received on […]

Accounting Chapter 9 1 For ratio analysis, a distortion in the current ratio under

Chapter 9 Inventories True/False [QUESTION] 1. Cost of goods available for sale is always the same regardless of the inventory cost flow assumption in use. Answer: False Feedback: While the dollar amount for purchases of the period are not dependent […]

Accounting Chapter 9 2 Lifouse The Following Answer Questions 82reference

Income before taxes overstated $10,000 Learning Objective: 09-14 Difficulty: 3 Hard AACSB: Knowledge Application AICPA: BB Critical Thinking AICPA: FN Measurement Blooms: Apply Topic Area: Inventory errors [QUESTION] REFER TO: Ref. 09_02 58. If no correcting entries were made at […]

Accounting Chapter 9 3 What is the cost of the inventory at January 31

c. IFRS permits inventory reductions due to lower of cost or market writedowns to be reversed if the market recovers. d. Since the use of LIFO is not allowed under IFRS, inventory holding gains are included in income. Answer: b […]