Financial Reporting and Analysis (7th Ed.)

Chapter 11 Solutions

Financial Instruments and Liabilities

Problems/Discussion Questions

Problems

P11-1. Imputing interest (LO 11-3)

Requirement 1:

To verify that the imputed interest rate on the dealer’s loan is 6%,

compute the present value of the payment stream using a 6%

Present

value

Down payment Payment factor

Requirement 2:

Greg has the funds needed to make the down payment, but must

borrow the remaining amount of purchase price. The dealer has

P11-2. Reporting bonds issued at a discount (LO 11-2)

Requirement 1:

The issuance price of the bonds on July 1, 2017 is equal to the

present value of the principal repayment plus the present value of

the semi-annual interest payments. Since the bonds pay interest

semi-annually, the present value calculations are based on a

Present value of the interest payments:

Requirement 2:

The amortization schedule appears below:

Effective Amortization of Bond Discount for McVay Corp.

[Market Interest Rate of 5% (semi-annual)]

(a) (b) (c) (d) (e)

Date

Interest

Expense

(0.05 x e)

Cash Payment

(Fixed)

Amortization

of Bond

Discount

(a – b)

Discount on B/P

(Beginning Balance

minus c)

Carrying Amount

($15,000,000

minus d)

Requirement 3:

The journal entries for the first four interest payments are:

12/31/17:

12/31/18:

6/30/19:

Requirement 4:

The balance sheet presentation at 12/31/17 would be:

The balance sheet presentation at 12/31/18 would be:

P11-3. Reporting bonds issued at a premium (LO 11-2)

Requirement 1:

The issuance price of the bonds on January 1, 2017, is equal to the

present value of the principal repayment plus the present value of

the semi-annual interest payments. Since the bonds pay interest

Present value of the interest payments:

Issue price of the bonds:

Requirement 2:

The amortization schedule appears below:

Effective Amortization of Bond Premium for Fleetwood Inc.

[Market interest rate of 3% (semi-annual)]

(a) (b) (c) (d) (e)

Date

Interest

Expense

(0.03 x e)

Cash Payment

(Fixed)

Amortization

of Bond

Premium

(b – a)

Premium on B/P

(Beginning

Balance

minus c)

Carrying

Amount

($25,000,000

plus d)

Requirement 3:

The journal entries for the first four interest payments are:

6/30/17:

CR Cash

$1,000,000.00

12/31/17:

CR Cash

$1,000,000.00

6/30/18:

CR Cash

$1,000,000.00

12/31/18:

CR Cash

$1,000,000.00

Requirement 4:

The balance sheet presentation at 12/31/17 would be:

The balance sheet presentation at 12/31/18 would be:

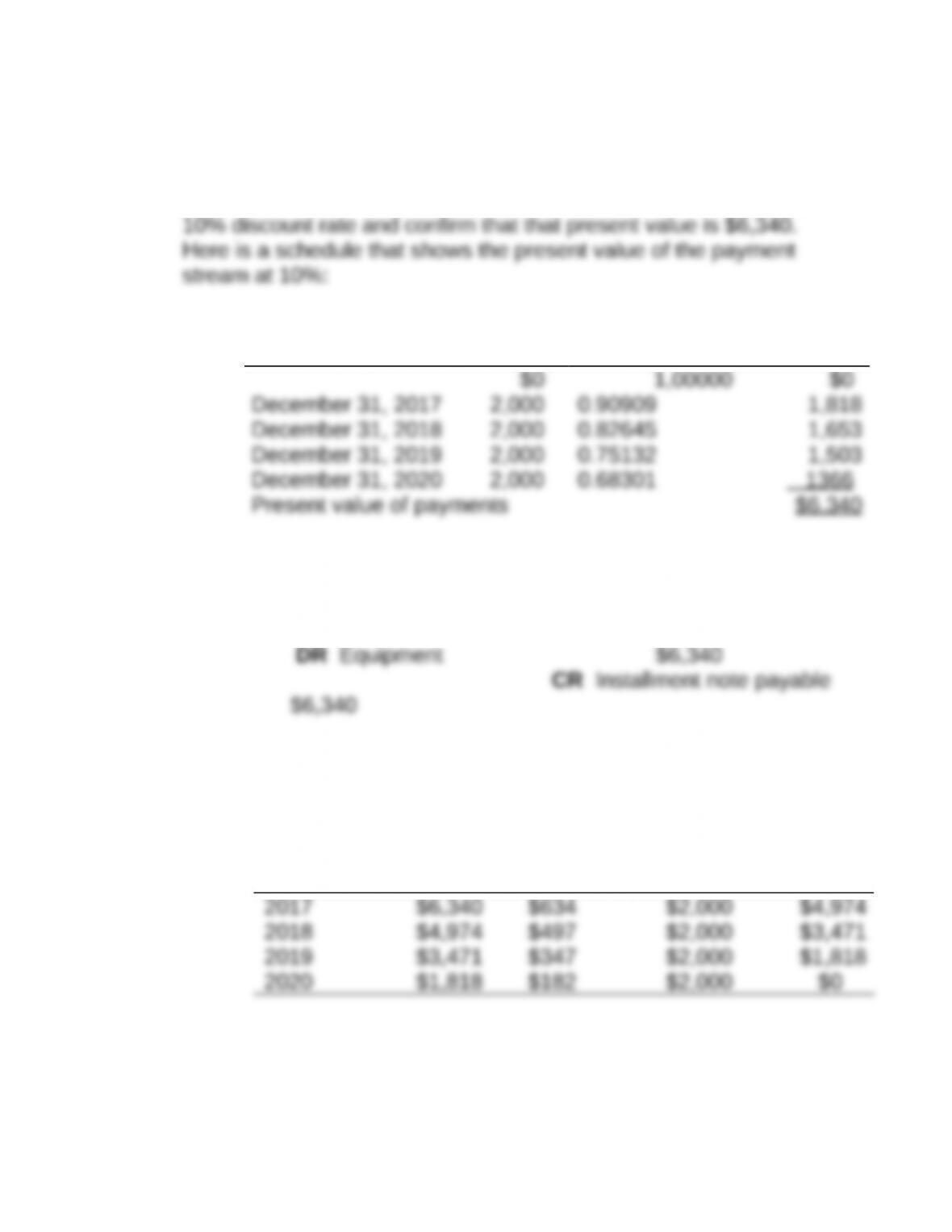

P11-4. Analyzing installment note and imputed interest (LO 11-3)

Requirement 1:

To verify that the imputed interest rate on the installment note is

10%, we compute the present value of the payment stream using a

Present value

Down payment Payment factor

Requirement 2:

The following journal entry would be made on January 1, 2017 to

record the purchase:

Requirements 3 and 4:

The following schedule shows interest expense and the loan

balance for each year:

Balance at

start of year

Interest

at 10%

Loan

payment

Balance at

end of year

Interest expense for 2017 would be $634 and the loan balance at

year-end would be $4,974. Interest expense for 2018 would be

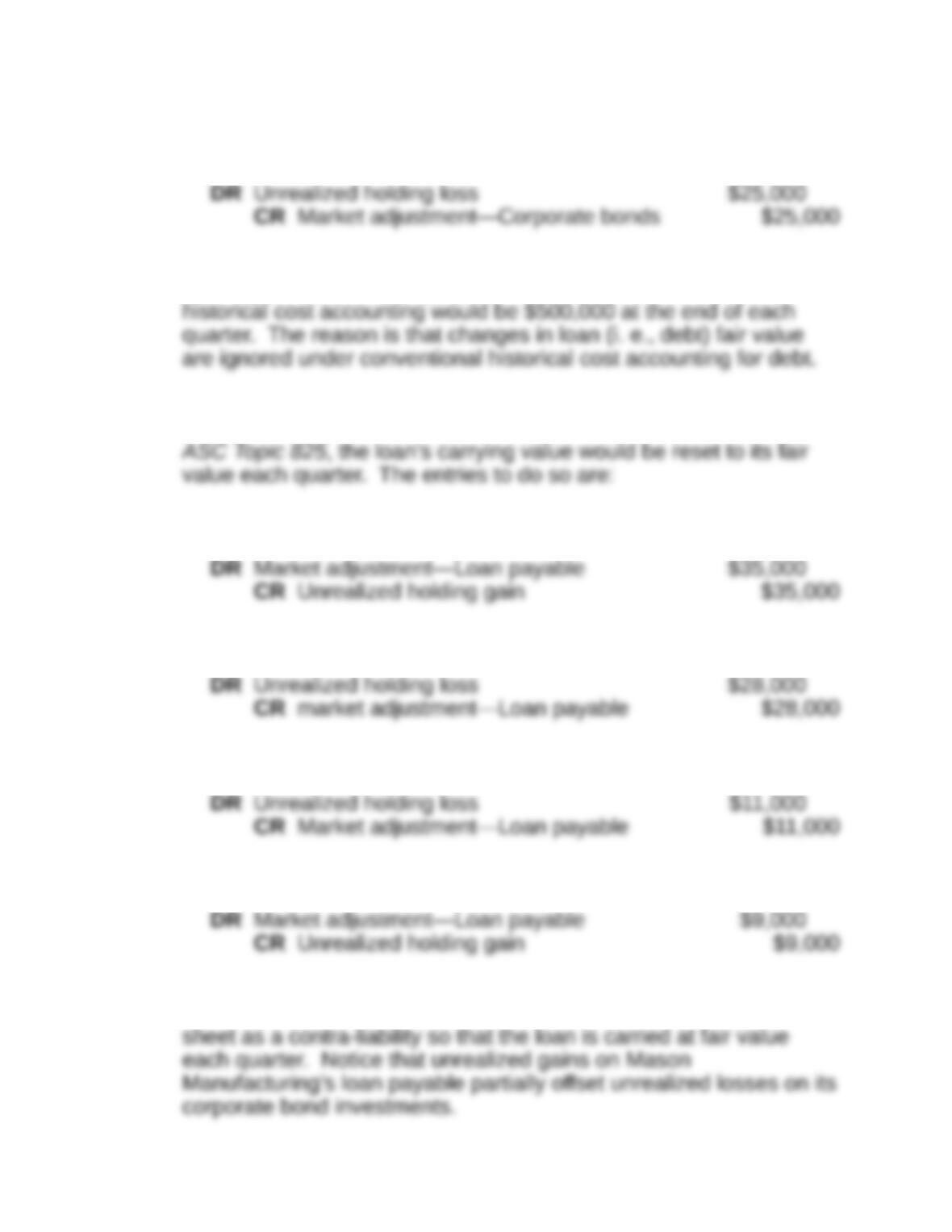

P11-5. Understanding the Fair Value Option (LO 11-5)

Requirement 1:

Mason would make the following entry to record the borrowing and

initial purchase of its corporate bond investment:

January 1, 2017:

DR Cash

As described in more detail in Chapter 16, Mason Manufacturing

would make the following entries to record the fair value of its

corporate bond investment at the end of each quarter. Unrealized

March 31, 2017:

June 30, 2017:

September 30, 2017:

December 31, 2017:

Requirement 2:

Ignoring interest, the carrying value of the loan under conventional

Requirement 3:

If Mason elects to use the fair value option for debt permitted by

March 31, 2017:

June 30, 2017:

September 30, 2017:

December 31, 2017:

As before, unrealized holding gains and losses flow to the income

statement. The Market adjustment account flows to the balance

Requirement 4:

Proponents of the fair value option for debt argue that this offset

feature (described in Requirement 3) helps to insulate the income

statement from artificial volatility when inter-corporate investments