Financial Reporting and Analysis (7th Ed.)

Chapter 6 Solutions

The Role of Financial Information in Valuation,

Cash Flow Analysis, and Credit Risk Assessment

Cases

Cases

C6-1. Illinois Tool Works: Abnormal earnings valuation

Requirements 1 and 2:

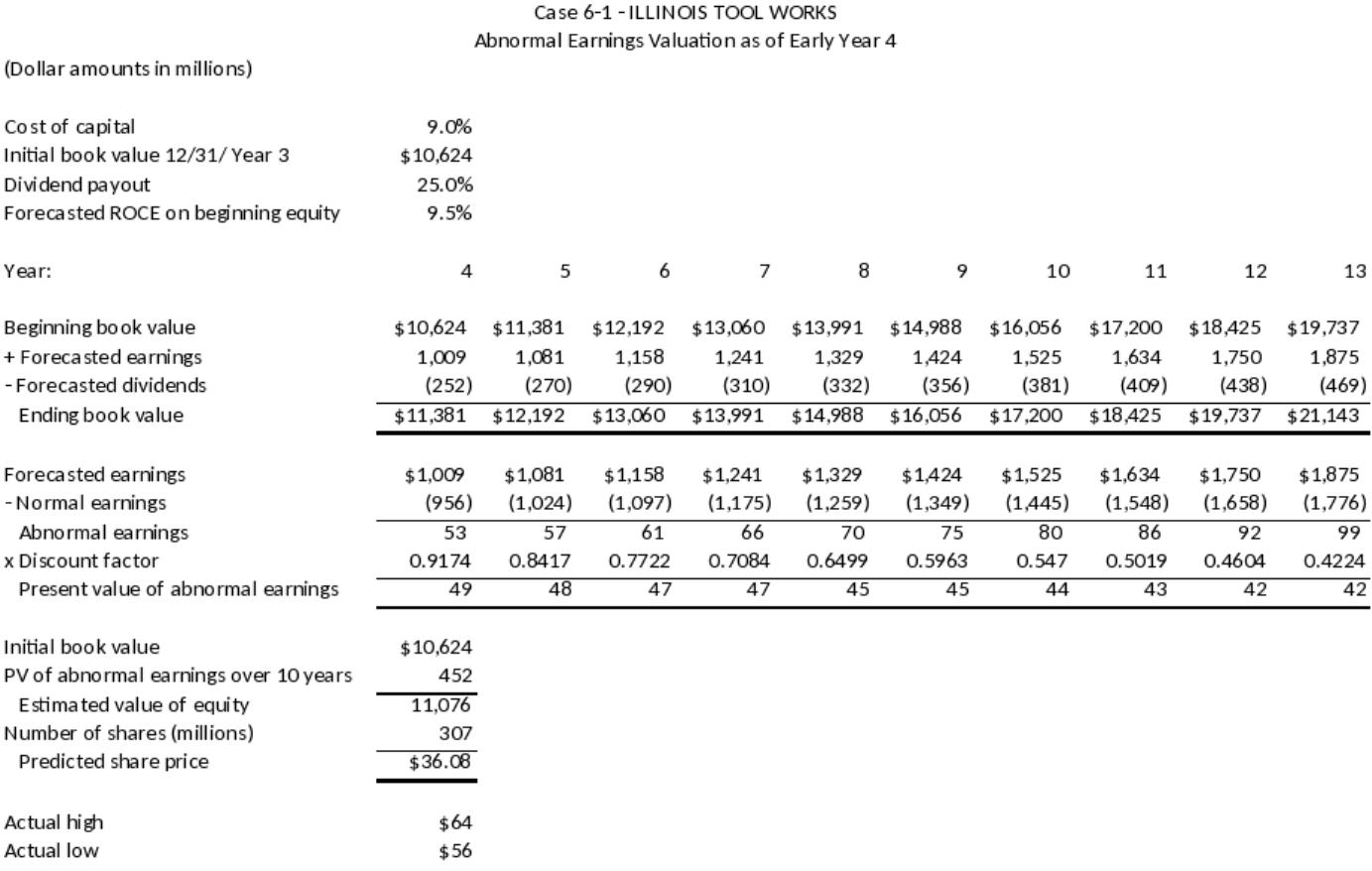

The template solution (shown on the next page) yields an estimated stock price of $36.08 per share. This

estimate is considerably below the company’s trading range of $56-$64 in the first quarter of Year 4. One

Requirement 3:

When forecasted ROCE is raised to 16%, the value estimate increases to $59.79. This amount corresponds

6-1

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education.

6-2

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education.

C6-2. Sunny Day Stores Inc. : Analyzing debt covenants and

financial distress

Note to instructors: This is a challenging case based on a

real company, Sunshine Junior Stores, Inc. As a result,

some instructors find that it is best suited for class

discussion of the issues surrounding loan renegotiations

Requirement 1:

With regard to the amount of collateral, given that Sunny

Day violated its earlier lending agreements, lenders are

likely to demand collateral in an amount equal to face value

of the debt.

The revised lending agreement stated that: The

Company will pledge as collateral its interest in

Requirement 2:

The fact that Sunny Day defaulted on the earlier lending

agreement is a clear indication that the company’s credit

risk has increased. To compensate for the added risk,

lenders often require a higher interest rate.

The actual revised lending agreement stated the

following: The interest rates on the loan agreements will

6-3

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written

consent of McGraw-Hill Education.

be increased to 9.43% and prime plus 1.5% for Prudential

and First Florida, respectively.

Requirement 3:

As stated in the revised lending agreement, lenders could

require the company to use the proceeds from any asset

sale to reduce outstanding debt. In addition to limitations on

The actual revised lending agreement stated the

following (with dates changed to correspond to those

in the case): Additional principal reductions in the amount

Requirement 4:

This will be a difficult question for students to answer in a

precise fashion. We recommend making the following point

before sharing the actual revisions with them. Lenders are

The actual revised lending agreement stated the

following: The new financial covenants, all calculated

based on inventories accounted for on a FIFO basis, are as

follows:

Minimum FIFO

Fixed

Coverage

Working

Ratio, as

6-4

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written

consent of McGraw-Hill Education.

Period ending Net Worth Capital

(deficit) defined

March 2018 $20,000,000

($5,500,000) 1.30:1.0

Note that the revised covenants are based on FIFO

inventory values even though Sunny Day uses LIFO for

financial reporting purposes (see the balance sheet). One

Requirement 5:

Sunny Day defaulted on the earlier loan and is clearly

experiencing some financial difficulty. Allowing the company

company should not be allowed to resume the dividend.

The actual revised lending agreement stated the

following: Negative covenants in the Company’s debt

agreements prohibit the payment of dividends.

C6-3. Microsoft Corporation: Unearned revenues and earnings

management

6-5

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written

consent of McGraw-Hill Education.

Requirement 1:

The net profit margin is equal to net income divided by

sales. For Microsoft, the rates are:

Fourth quarter of 1996:

Fourth quarter of 1997:

Year 1996:

Year 1997:

By any standard, Microsoft’s net profit margin is very

Requirement 2:

Microsoft just exceeded analysts’ expectations in the fourth

Requirement 3:

Ending balance = Beginning balance + additions –

reductions

Requirement 4:

Income effect per share = increase in income/shares used

Requirement 5:

Ending balance = Beginning balance + additions –

reductions

$1,418 = $560 + additions – $188.0; additions = $1,046.0

Requirement 6:

Income effect per share = increase in income/shares used

to calculate fourth quarter EPS

6-6

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written

consent of McGraw-Hill Education.

= $1046.0/1,312

= $0.80 or 80 cents

Requirement 7:

This answer is the balance in the account of $1,418 divided

Requirement 8:

In periods when the firm’s earnings are less than

management would like to report, the balance in the

In periods when the firm is doing very well, management

Requirement 9:

This is a tough task for the analyst. One thing that the

analyst might do is monitor the firm’s balance sheets on a

quarter-to-quarter basis, paying special attention to the

Unearned revenues account. What the analyst could watch

for are large increases in the account balance in periods

when the firm is doing very well, and perhaps, more

Requirement 10:

No. It might very well be that the firm’s managers believe

that the proper matching of revenues and expenses

requires that some of the revenues collected from

customers in a given year be deferred and recognized in a

later period when product upgrades are delivered and/or

various types of services are provided.

6-7

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written

consent of McGraw-Hill Education.

6-8

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written

consent of McGraw-Hill Education.