P12-9. Recording capital lease for lessee and comparing to

operating lease treatment under ASC 840 (LO 12-2, LO12-3,

LO12-5)

Part A – June 30 reporting year

Requirement 1: Lease criteria

This is a capital lease for Burgundy because the lease meets the

third criterion (lease term greater than or equal to 75% of the

equipment’s economic life). In this case, the percentage is 80%

(lease term of 8 years divided by 10 year economic life. Criteria 1

Requirement 2: Amortization table

Part 2 – Amortization table

(A) (B) ( C) (D)

Interest Principal

Date Payment Expense Reduction Balance

.11 x prior (D) (A) – (B) Prior (D) – ( C)

© 2018 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for

sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or

posted on a website, in whole or part. 12-1

The table begins with the present value of minimum lease

Requirement 3: Journal entries

Requirement 3 – Journal entries

July 1, 2017 July 1, 2018

June 30, 2018 June 30, 2019

aLease asset of $239,912 ÷ lease term of 8

years)

bAfter the interest accrual at June 30, 2018, the obligation grows to $219,682

($197,912 + $21,770). The $42,000 payment reduces the obligation to

$177,682, which is shown in the table from Requirement 2.

Part B – December 31 reporting year

Requirement 1: Journal entries

Requirement 1 – Journal entries

December 31, 2017

DR Interest expense $ 10,885.00 c

© 2018 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for

sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or

posted on a website, in whole or part. 12-2

d6/12 x annual depreciation of $29,989

July 1, 2018

eAfter the accrual at December 31, 2017, the obligation is $208,797 ($197,912 + 0.5 x $21,770). The debit

for $31,115 removes this accrual and the difference between interest expense and the cash payment for the

lease year.

December 31, 2018

f6/12 x annual interest of $19,545

gAnnual depreciation of $29,989, assuming that no entry was made earlier in the year

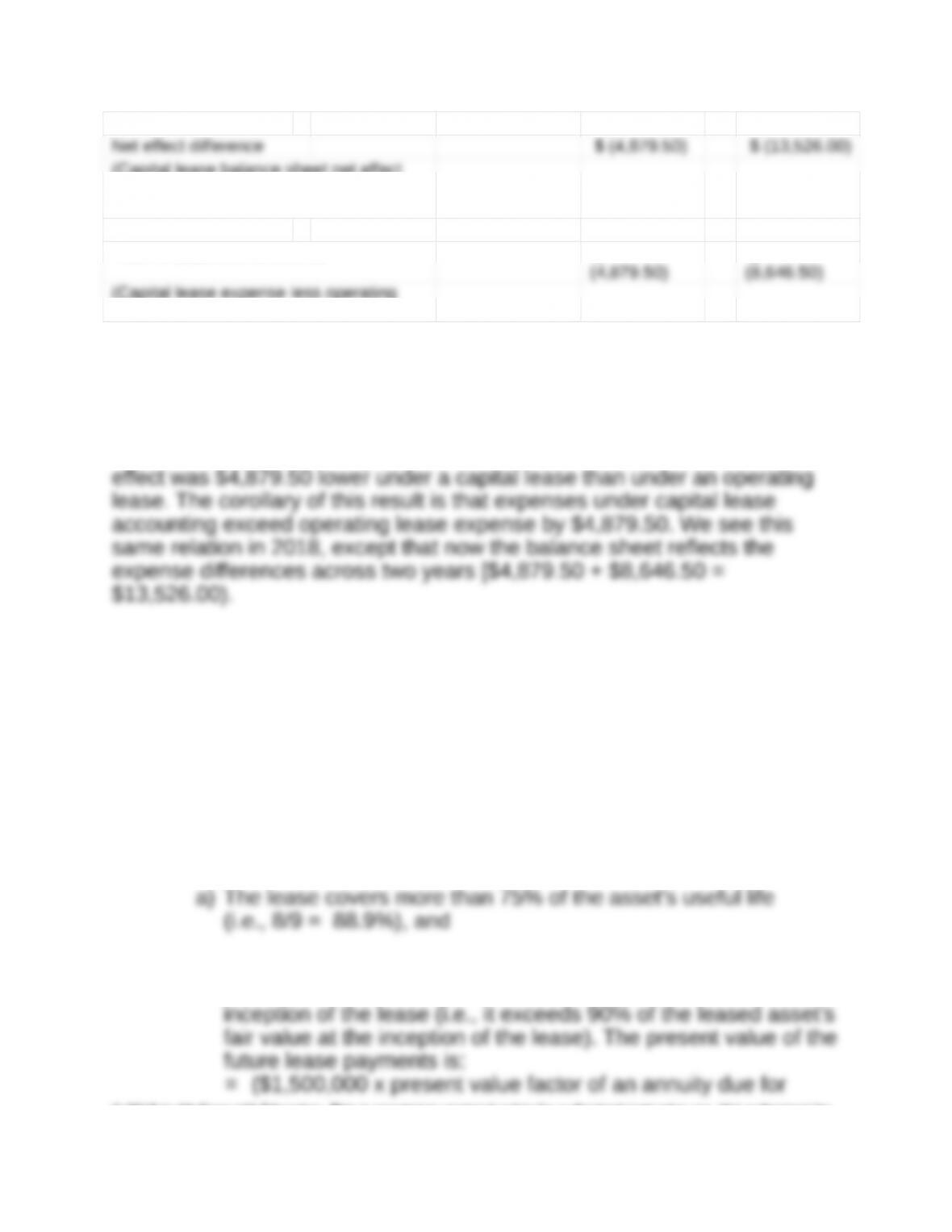

Requirement 2: Financial statement effects for the capital lease

The choice between capital lease and operating lease accounting

does not affect cash. Consequently, this analysis does not add the

complication of considering the effects on Cash.

Balance Sheet

Assets December 31

2017 2018

© 2018 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for

sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or

posted on a website, in whole or part. 12-3

Requirement 3: Financial statement effects for an operating

lease

Balance Sheet

Assets December 31

2017 2018

Liabilities

– –

Liability Effect – –

(6/12 x payment of $42,000 in 2017 and

$42,000 in 2018)

© 2018 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for

sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or

posted on a website, in whole or part. 12-4

(Capital lease balance sheet net effect

less operating lease balance sheet net

effect)

Income statement difference $

$

(Capital lease expense less operating

lease expense)

The top portion of the above schedule shows the balance sheet and

income statement effects of treating the lease as an operating lease. The

calculations below the income statement show the difference between

capital lease and operating lease treatment. In 2017, the net balance sheet

P12-10. Recording lessor sales-type lease under ASU 2016-02 (ASC

842) (LO 12-9)

Requirement 1: Lease classification

The lease must be accounted for as a sales-type lease because

two of the Type I characteristics (only one is required) are met. In

addition, there are no cash flow uncertainty or uncertainties

regarding unreimbursable costs.

The two Type I characteristics met are:

b) The present value of the future lease payments of $8,345,640

equals 95.4% of the leased asset’s $8,749,520 fair value at the

© 2018 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for

sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or

posted on a website, in whole or part. 12-5

Requirement 2: Amortization schedule

The amortization schedule for Railcar Leasing Incorporated is as

follows:

(A) (B) ( C) (D)

Interest Receivable

Date Payment Income Reduction Balance

.12 x prior (D) (A) – (B) Prior (D) – ( C)

*Rounded.

Requirement 3:

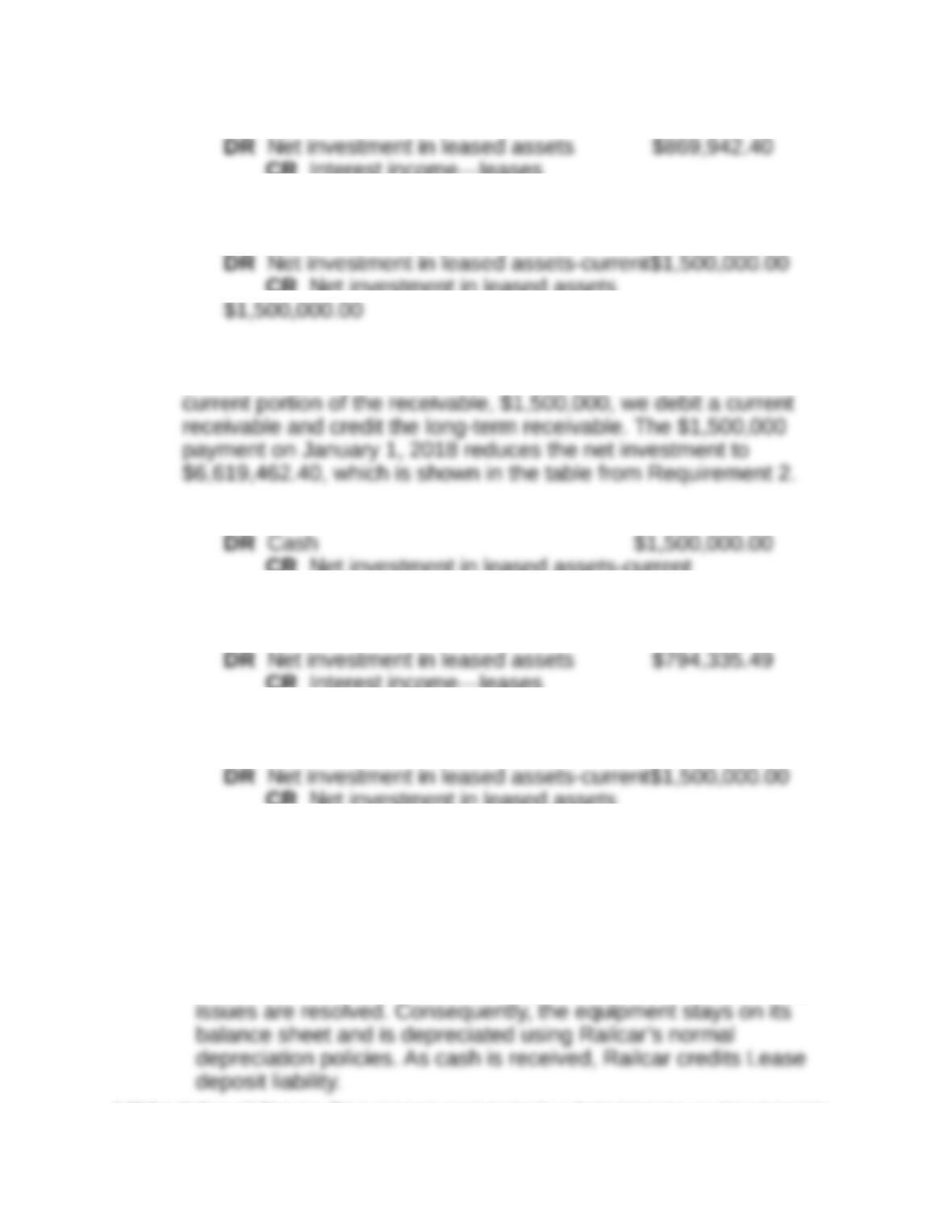

The journal entries are:

The journal entry to record the purchase of the boxcars by Railcar

Leasing Incorporated would be:

1/1/2017:

CR Net investment in leased assets

$1,500,000.00

© 2018 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for

sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or

posted on a website, in whole or part. 12-6

12/31/2017:

CR Interest income—leases

$869,942.40

12/31/2017:

CR Net investment in leased assets

After the interest accrual at December 31, 2017, the total receivable

grows to $8,119,462 ($7,249,520 + $869,942.40). To reflect the

1/1/2018:

CR Net investment in leased assets-current

$1,500,000.00

12/31/2018:

CR Interest income—leases

$794,335.49

12/31/2018:

CR Net investment in leased assets

$1,500,000.00

P12-11. Recording lessor sales-type lease under ASU 2016-02 (ASC

842) (LO 12-9)

Requirement 1: Journal entries when collectibility is an issue

The lease still meets the definition of a sales-type lease. However,

Railcar cannot treat it as a sales-type lease until the collectibility

© 2018 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for

sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or

posted on a website, in whole or part. 12-7

The annual lease payment would be recorded as follows:

12/31/2017 and 12/31/2018:

CR Lease deposit liability

$1,500,000

Until the collectibility issues are resolved, the lessor depreciates

the assets over 9 years, the remaining useful life at lease

commencement. The annual depreciation charge would be

$8,749,520/9 = $972,168.89. The journal entries would be:

12/31/2017 and 12/31/2018:

CR Accumulated depreciation

$972,168.89

Requirement 2: Income statement effects

Railcar would not recognize any interest income. Instead, it

recognizes additional depreciation expense of $972,168.89 in both

Requirement 3: Improved collectibility journal entry on

1/1/2020

When collectibility becomes probable, the lessor reverses the prior

accounting and begins accounting for the lease as if it had always

© 2018 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for

aPresent value of remaining payments and residual value

bCheck for selling profit

The small difference is due to rounding.

© 2018 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for

sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or

posted on a website, in whole or part. 12-9