E12-17. Classifying leases under ASC 840, IAS 17 and ASU (2016-02

(ASC 842) (LO 12-3, LO 12-6, LO 12-10)

Requirement 1: Classification under ASC 840

The lease would be a capital lease because the lease term of 5

years is 83% of the expected useful life. This meets the third lease

criteria of greater than or equal to 75% of the economic life. If the

Requirement 2: Classification under IAS 17

There are no bright lines under IAS 17, but one would still consider

the ratio of lease term to economic life and the present value of

minimum lease payments to the fair value of the leased asset. In

Requirement 3: Classification under ASU 2016-02 (ASC 842)

E12-18. Lessee accounting under ASC 840 and ASU 2016-02 (LO

12-3, LO 12-6)

Requirement 1: Initial entry under ASC 840

Requirement 2: Initial entry under ASU 2016-02

© 2018 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for

sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or

posted on a website, in whole or part. 12-1

The $1,332,565 is determined by multiplying the lease payment by

the PVOA factor for five years and 7%. Specifically, we make the

following calculation:

$325,000 × 4.10020 = $1,332,565

Requirement 3: Financial Statement effects under ASU

2016-02

Most of the information needed comes from the amortization table

presented below. Although only the first three rows are needed to

answer this question, the table for all five years of the lease is

presented.

Interest Principal

Date Expens

e

Payment Reduction Balance

01/01/2017 $ 1,332,565

12/31/2017 $93,280 $ 325,000 $

231,720

1,100,845

12/31/2018 77,059 325,000

247,941

852,904

12/31/2019 59,703 325,000

265,297

587,607

12/31/2020 41,132 325,000

283,868

303,739

12/31/2021 21,261 325,000

303,739

–

© 2018 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for

sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or

posted on a website, in whole or part. 12-2

For an operating lease under ASU 2016-02, asset

amortization equals the difference between rent expense

(based on dividing total lease payments divided by the

number of payments) and interest expense on the obligation.

The accounting for the obligation follows the normal

approach for amortizing a loan or lease. The Lease obligation

Although amortization and interest expense comprise total

lease expense, the depreciation and interest expense are not

handled separately in the income statement or on the

Balance sheet at December 31, 2017

Income statement for year ended December 31, 2017

Statement of cash flows for year ended December 31, 2017

© 2018 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for

sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or

posted on a website, in whole or part. 12-3

(Direct method)

Cash from operating activities

© 2018 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for

sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or

posted on a website, in whole or part. 12-4

Financial Reporting and Analysis (7th Ed.)

Chapter 12 Solutions

Financial Reporting for Leases

Problems

Problems

P12-1. Making computations and journal entries for lessee under ASC

840 (LO 12-3, LO 12-5)

Requirement 1: Lease classification

Criterion 2:

Criterion 4:

Present value of an ordinary annuity factor for 3 years at 9%

Criterion 4 is not met.

Requirement 2: Amortization table

Amortization Table

(1) (2) (3) (4) (5) (6)

Date

Total

Payment

Interest

Expense

Principal

Payment

Lease

Obligation

Balance

Amortization

of Asset

Total Annual

Capital

Lease Expense

(Col. 2 + Col. 5)

$18,985

Requirement 3: Journal entries for first two years

© 2018 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for

sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or

posted on a website, in whole or part. 12-5

01/01/17

CR Cash $ 7,500

DR Depreciation Expense—Capital Lease $ 6,328

CR Accum. Depreciation—Capital Lease $ 6,328

12/31/18

Requirement 4: Useful life of six years

Because criterion 2 is no longer met, this must be recorded as an

operating lease. Therefore, the same journal entry will be prepared

each year for the three-year lease term:

Requirement 5: Financial statement effects

Effects on assets, liabilities, and equity of capital versus operating

lease treatment:

Assets Liabilities Equity

Capital lease

12/31/17

© 2018 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for

sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or

posted on a website, in whole or part. 12-6

Differential effect as

So comparing across the two methods at December 31, 2017,

assets would

P12-2. Making comparisons for lessee and lessor under ASC 840 (LO

12-1, LO 12-3, LO 12-5, LO 12-7)

Requirement 1:

The computation of the annual lease payments is shown below:

Requirement 2:

Since the residual value is not guaranteed, it is not included in the

lease obligation. The computation of the lessee’s lease obligation at

signing is illustrated below.

*Rounded

Requirement 3:

Partial lease amortization schedules appear below for the lessee

and lessor, assuming a 10% discount rate. Note that the entire

© 2018 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for

sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or

posted on a website, in whole or part. 12-7

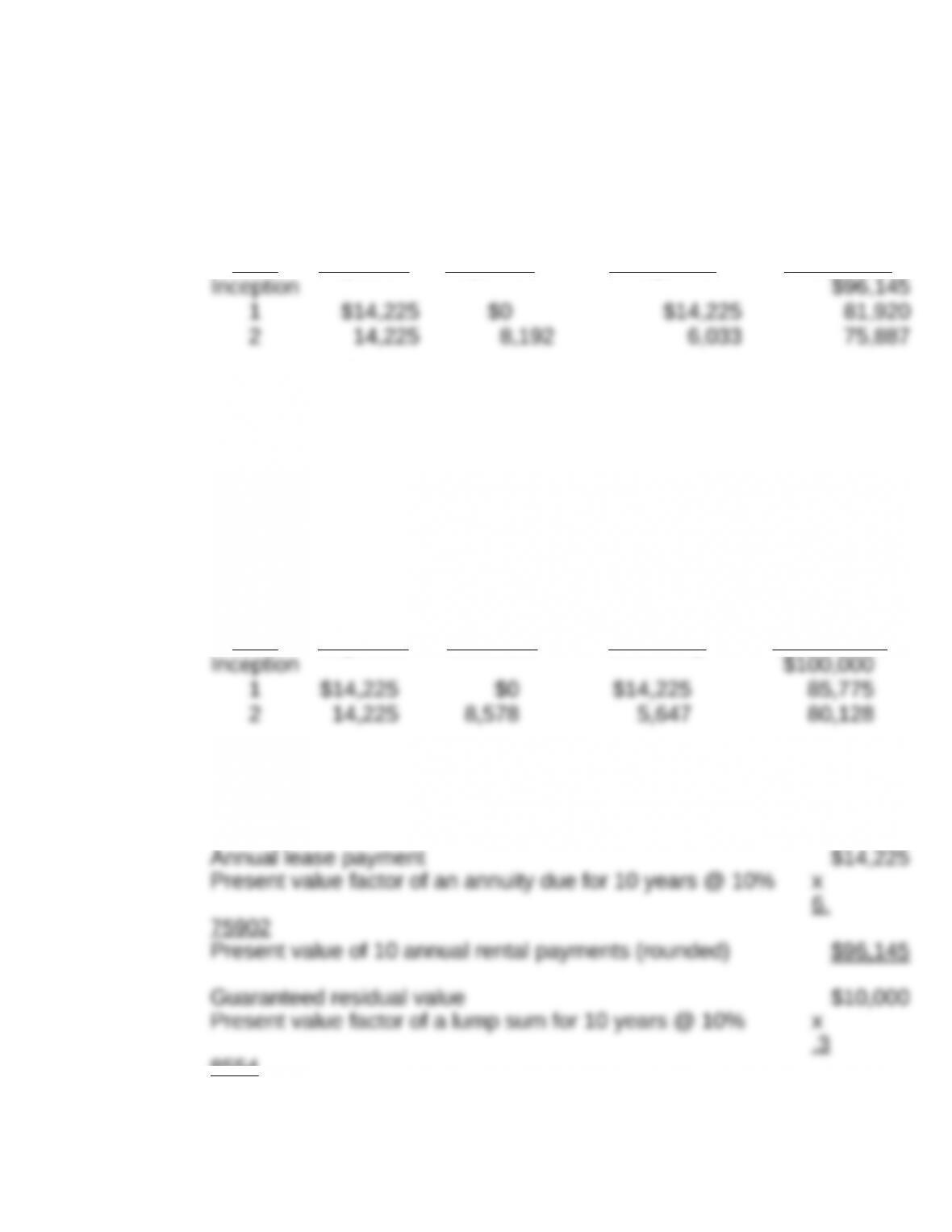

$8,192 of interest expense based on the present value of the lease

obligation of $81,920 following the initial payment.

Lessee Co. Lease Amortization Schedule

Year

Annual

Payment

Interest

Expense

Reduction of Lease

Obligation

Lease

Obligation

The lessor will recover $100,000 because the machine will have

residual value at the end of the lease, even though it may be

unguaranteed. Thus, by the end of the first year the lessor has

earned $8,578 in interest revenue from the lease based on the

present value of the net investment of $85,775 following the initial

payment.

Lessor Co. Lease Amortization Schedule

Year

Annual

Payment

Interest

Revenue

Net Investment

Recovery

Net

Investment

Requirement 4:

a) If the residual value were guaranteed, it would change the lease

obligation as follows:

8554

© 2018 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for

sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or

posted on a website, in whole or part. 12-8

b) A revised amortization table for Lessee Co. follows:

Year

Annual

Payment

Interest

Expense

Reduction of Lease

Obligation

Lease

Obligation

As shown in the table, the interest expense for Lessee Co. for year

1 is now $8,578 instead of $8,192 under Requirement 3.

The computation for Lessor Co. would not change if the residual

P12-3. Accounting for lessee capital leases under ASC 840 (LO 12-3,

LO 12-5)

Requirement 1: Rationale for classification

Given that the leased asset has an expected useful life of 6 years,

Requirement 2: Calculation of present value and amortization

table

Present value of future lease payments:

Appearing below is the amortization schedule for the lease liability:

Amortization of Capital Lease Liability

© 2018 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for

sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or

posted on a website, in whole or part. 12-9

Seven Wonders Incorporated

(In thousands)

Interest Cash

Reduction of

Lease Lease

Date Portion1Payment2Obligation3Obligation4

*Rounded by $1.85

1 The interest portion is 12% of the carrying amount at the beginning of the

period.

2 The cash payment is fixed by the lease at $277,409.44.

Requirement 3:

The journal entries are:

1/1/2017:

CR Obligations under capital leases

$1,000,000.00

12/31/2017:

CR Cash

$277,409.44

12/31/2018:

CR Cash

$277,409.44

© 2018 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for

sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or

posted on a website, in whole or part. 12-10

2017 and 2018:

Requirement 4:

Under the capital lease method, the total expense recognized in

2017 is the interest expense of $120,000 plus the depreciation of

$200,000 for a total of $320,000. Under the operating lease method,

© 2018 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for

sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or

posted on a website, in whole or part. 12-11