P12-16. Evaluating sale and leaseback under ASC 840 and ASU 2016-02 (ASC 842) (LO

12-3, LO 12-4, LO 12-6)

Requirement 1: Lease type under ASC 840

This is a capital lease for Merchant because the lease meets at least one of the criteria

for capital lease treatment. In fact, the lease meets two of the capital lease criteria. The

lease term is 75% of the tractor’s remaining economic life (75% x 6 years = 4.5 years),

and the present value of the minimum lease payments exceeds 90% of the tractor’s fair

value:

Requirement 2: Gain on transaction under ASC 840

Since this is a sale and leaseback transaction, Merchant will not report the gain on its

Requirement 3: Journal entries under ASC 840

Journal entries at January 1, 2017:

Requirement 4: Sale-leaseback under ASC 842

Under normal circumstances, the lease would be classified as a finance lease. However,

under ASU 2016-02, the company would have continuing interest in the asset and would

P12-17. Visualizing the asset-liability relationship over time for a capital (finance)

lease (LO 12-1, LO 12-3, LO 12-6)

Requirement 1:

a) At 8%, the accrual of interest causes the liability at the end of the first year to total

$103,718.87 (i.e., a beginning balance of $96,035.99 plus accrued interest of

© 2018 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or

distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in

whole or part. 12-1

b) At 12%, the accrual of interest causes the liability at the end of the first year to total

$82,496.70 (i.e., a beginning balance of $73,657.77 plus accrued interest of

c) As in parts 1(a) and (b), the accrual of interest causes the liability to exceed the asset

Requirement 2:

a) With payments at the end of each year, the carrying value of the asset will never

b) Raising the interest rate and/or shortening the duration of the lease does not change

P12-18. Accounting for lessee with uneven payments under ASU 2016-02 and

IFRS 16 (LO 12-1, LO 12-5, LO 12-6)

Requirement 1: Journal entry at 1/1/2017 under ASU 2016-02

Payment

Number Payment

PV

assumption

8% PV

factor

Present

Value

To record first payment

© 2018 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or

distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in

whole or part. 12-2

Requirement 2: Amortization table

Total Interest Principal

Date Payment Expense Reduction Balance

Requirement 3: Journal entries at 12/31/2017

To record increase in liability for interest payable

(Straight-line expense of $12,700 less interest of

$3,502.09)

Requirement 4: Operating lease liability and right-of-use asset

Relation between lease liability and right-of-use asset

Less difference between prior cash

payments and rent expense –

Total payments for first two years of $21,000 less expense

© 2018 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or

distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in

whole or part. 12-3

Check, using journal entry and T-account approach:

31-Dec-18

Right-of-use asset

Requirement 5: Finance lease liability and right-of-use asset under IFRS 16

The book value of the asset under IFRS 16 is $2,514.77 less than the operating lease

asset under ASU 2016-02. This difference also represents the additional amortization

that was recognized as part of pretax income over the prior two years. This difference

would be reflected in Retained earnings. To keep the fundamental accounting equation

in balance, if assets are less, then equities also must be less.

P12-19. Analyzing ASC 840 and IAS 17 operating lease disclosures (LO 12-10, LO

12-11)

Requirement 1:

The United Continental Holdings note disclosure is more informative because it articulates

Requirement 2:

The aggregation of multiple years’ expected future minimum lease payment cash flows is

problematic because it makes it more difficult to estimate precisely discounted cash flows.

When estimating annual cash flows, the Appendix to this chapter suggests the analyst

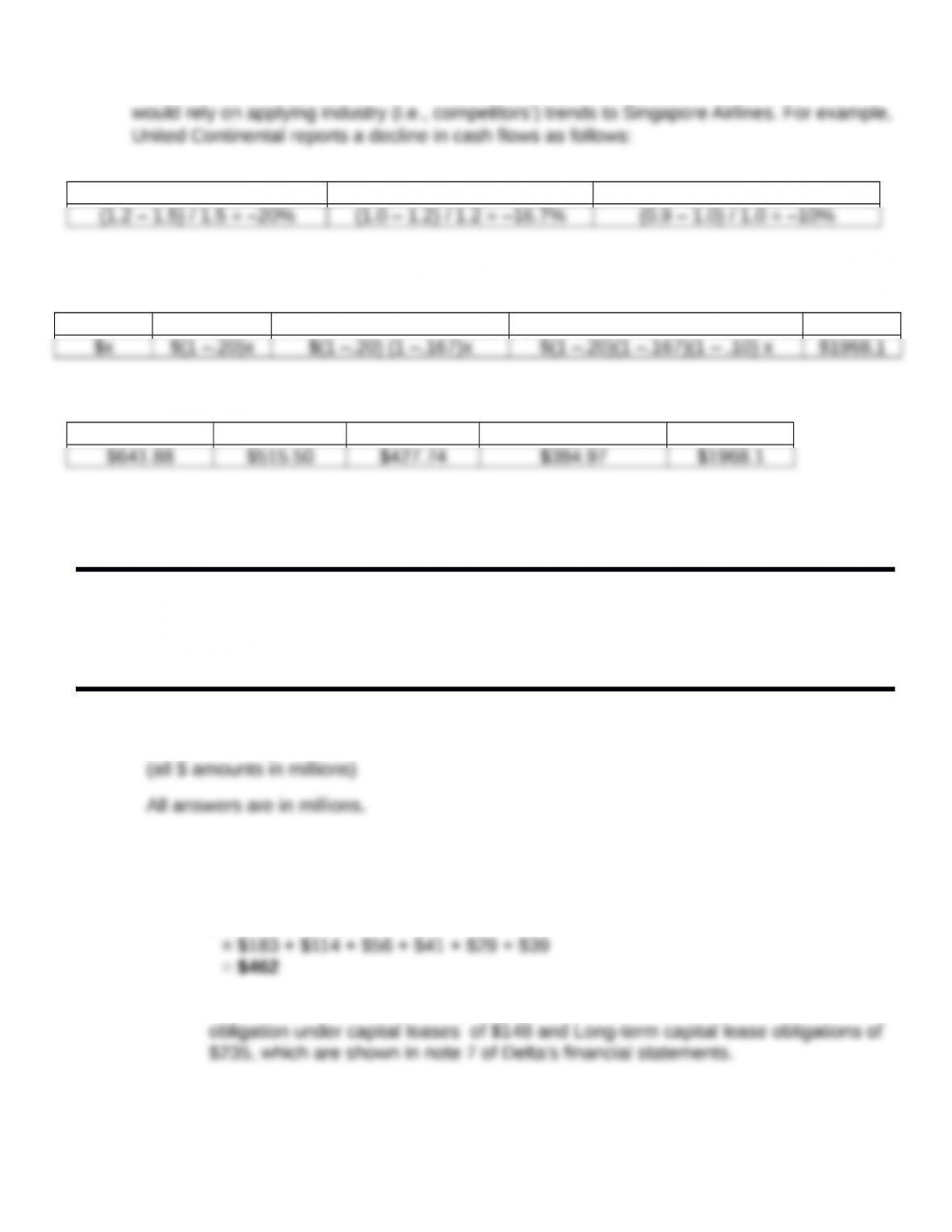

consider trends (e.g., declines) that are evident in the note. For Singapore Airlines, this is

© 2018 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or

distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in

whole or part. 12-4

estimate $1,968.1÷ 4 aggregated years to approximate an annual cash flow of 492.025 for

each of the years 2, 3, 4, and 5. Another alternative is somewhat more complicated and

Year 2-3 Year 3-4 Year 4-5

If we assume Singapore Airlines observes a similar decline trend (which we could also

validate from other competitors), we can algebraically compute the following:

Year 2 Year 3 Year 4 Year 5 Total

Solving for x, we would compute (approximations due to rounding error):

Year 2 Year 3 Year 4 Year 5 Total

The analysts’ assumptions matter because the net present value of the sum of these

discounted cash flows can vary materially based on the assumed cash flows through time.

Financial Reporting and Analysis (7th Ed.)

Chapter 12 Solutions

Financial Reporting for Leases

Cases

C12-1. Delta Air Lines Inc: Calculating the effects of ASU 2016-02 (LO 12-2, LO 12-5, LO

12-6, LO 12-11)

Requirement 1:

A. Total minimum lease payments is the sum of the annual payments of capital leases

listed in Note 7.

B. Present value of net minimum lease payments is $383. It is the sum of Current

© 2018 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or

distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in

whole or part. 12-5

Requirement 2: Capital lease net asset

From balance sheet information:

Requirement 3: Reason for difference between 1 and 2

A capital lease asset is amortized using Delta’s normal depreciation policies, whereas the

Requirement 4: Total debt to total assets

Requirement 5: Entry to record capital lease in 2016

Requirement 6: Operating lease obligation on the balance sheet

There appears to be $0 operating lease obligation on the balance sheet. However, note 7

Requirement 7: Present value of operating lease payments

Requirement 7 gives the assumed interest rate of 11%. However, it was estimated by

examining the relation between the 2016 interest expense and the average 2016 lease

liability for capital leases as follows:

© 2018 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or

distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in

whole or part. 12-6

To obtain the present value of the lease payments, the timing for the thereafter amount must be

estimated as follows:

Estimated life for thereafter

Estimate of thereafter annuity

Present value calculation

Discount

Rate 11.0%

Year

# of Years

discounte

d

Operatin

g Lease

Payment

PV

factor

@13.0%

PV of

Operating

Lease

The thereafter factor of 3.27108 equals an ordinary annuity for 12 years less an ordinary

© 2018 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or

distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in

whole or part. 12-7

Requirement 8: Entry to constructively capitalize the operating leases

Requirement 9: Change in debt to total assets ratio

In this case, the increase to the debt asset ratio is minor because of the existing high debt

asset ratio

C12-2. IFRS and FASB/IASB Exposure Draft (LO 12-10, LO 12-11)

Requirement 1: Differences from IAS 17

1. If we use British Airways in Exhibit 12.7 as an indication of accounting under IAS 17,

then we would expect to see more of Delta’s operating leases treated as capital

Requirement 2: Differences from IFRS 16

1. All of Delta’s operating leases would be capitalized using the implicit rate if known.

2. The existing capital leases would also be recomputed using the implicit rate if known.

© 2018 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or

distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in

whole or part. 12-8

operating section of the income statement, but the interest would be in the

nonoperating section. On the statement of cash flows, interest expense would be

C12-3.Walgreens Boots Alliance: Lessee reporting and constructively capitalizing operating

leases (LO 12-2, LO 12-5, LO 12-6, LO 12-11)

All answers are in millions of U.S. dollars.

Requirement 1: Debt-equity and Return-on-assets

Requirement 2: Present value of operating lease payments

Discount

Rate 5.0%

Year

# of Years

discounted

Operating

Lease

Payment

PV

factor

@5.0%

PV of

Operating

Lease

© 2018 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or

distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in

whole or part. 12-9

*9.89864 pvoa 14, 5% less 4.32948 pvoa 5, 5% = 5.56916

Requirement 3: Journal entry to capitalize operating leases

Requirement 4: Journal entries to record depreciation and interest

To record interest and payment for obligation

(Cash of $3,141 less interest of $1,355)

To record amortization of right-of-use asset

Requirement 5: Debt to equity ratio

Note from Requirement 3 that there is no effect on Shareholders’ equity. Therefore, we

compute a new amount of debt and compute the new ratio as follows.

Requirement 6: Return on assets

© 2018 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or

distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in

whole or part. 12-10

Under the ASC 842, there would be no adjustment to EBI for Walgreens Boots. The specific

calculations follow:

Requirement 7: Commentary on differences in ratios

Both of the revised ratios make Walgreens Boots look less healthy. The debt/equity ratio

increases by 72.2% and makes the company look riskier. The return-on-assets ratio

Requirement 8: Difference between IFRS 16 and ASC 842

Under IFRS 16, the right-of-use asset will be amortized using a firm’s normal depreciation

method, which is usually the straight-line method. This will result in a lower right-of-use

asset than we see under ASC 842. Consequently, equity will be lower, and the debt/equity

We can illustrate the higher ROA ratio simply by adjusting net income. The ratio would be

© 2018 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or

distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in

whole or part. 12-11

The 6.0% is 13.3% lower than the ASC 840 ratio of 6.9%, whereas the ASC 842 ratio of

4.9% is 29.0% lower.

© 2018 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or

distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in

whole or part. 12-12