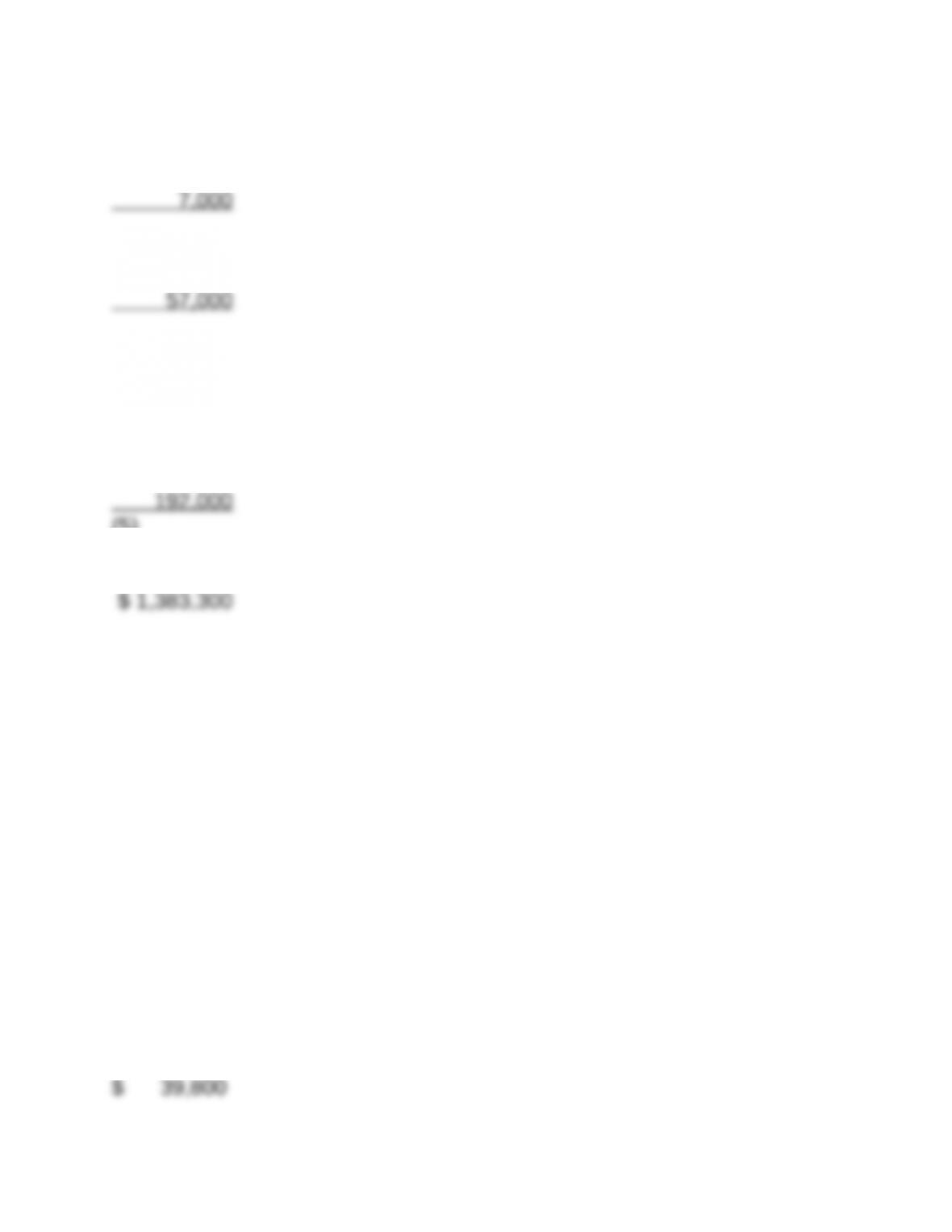

P4-2. Preparation of a statement of cash flows and a balance sheet

Requirement 1:

Kay Wing, Inc.

Statement of Cash Flows

For the Year Ended 12/31/2017

Cash flows from operating activities

Net income

$35,500

Adjustments to reconcile net income

to net cash provided by operating activities

Depreciation expense

12,000

Gain on retirement of bonds

(2,000)

Loss on sale of equipment

4,000

Increase in accounts receivable

($37,000 – $41,500)

(4,500)

Increase in inventory

($70,000 – $73,000)

(3,000)

Decrease in accounts payable

($33,000 – $25,500)

(7 ,500)

(1 ,000)

Cash flow provided by operating activities

34,500

Cash flows from investing activities

Purchase of land

(15,000)

Sale of equipment

10,000

Purchase of short-term investments

(8 ,300)

Net cash used in investing

(13,300)

Cash flows from financing activities

Issuance of capital stock

40,000

Retirement of bonds

(28,000)

Payment of cash dividends

(5 ,000)

Net cash provided by financing activities

7 ,000

Net increase in cash

28,200

Cash at beginning of year

65 ,000

Cash at end of year

$93

,200

Note to the instructor: The purchase of the building for $75,000

through the issuance of bonds and the purchase of land for $35,000

Requirement 2:

Kay Wing, Inc.

Balance Sheet

December 31, 2017

Cash

$ 93,200

Accounts receivable

41,500

Short-term investments

8,300

(1)

Inventory

73,000

Long-term investments

20,000

Land

89,000

(2)

Plant and equipment (net)

158,000

(3)

Total assets

$ 483,000

Accounts payable

$ 25,500

Taxes payable

4,000

Notes payable

35,000

(4)

Bonds payable

125,000

(5)

Capital stock

130,000

(6)

Retained earnings

163 ,500

(7)

Total liabilities and stockholders’ equity $ 483 ,000

(1) $0 + $8,300

P4-3. Preparing a balance sheet

Short Erin Company

Balance Sheet

December 31, 2017

Assets

Current assets:

Cash

(1)

Accounts receivable

(2)(4)

Allowance for doubtful trade accounts

(3)

Inventory

Total current assets

Long-term investments:

Nontrade receivables

(4)

Property, plant and equipment:

Land

(5)

Accumulated depreciation—buildings

(5)

Production equipment

Accumulated depreciation—

production equipment

Total property, plant and equipment

Intangible assets:

Patents

Leasehold

Total intangible assets

Other assets:

Held for sale plant assets

(5)

Total assets

Liabilities and Stockholders’ equity

Current liabilities:

Accounts payable

(2)

Accrued salaries

Notes payable-current

(6)

Current portion of installment note payable

(8)

Total current liabilities

Long-term liabilities:

Notes payable—long-term

(6)

Deferred income taxes

(8)

Installment note payable

(7)

Bonds payable

Total liabilities

Stockholders’ equity:

Total stockholders’ equity

(1) The U.S. treasury bills are considered cash equivalents and are

properly included in the cash balance. The $8,500 stock

(4) The $15,500 receivable from the company president is a

non-trade receivable and should be listed separately from trade

(5) The land ($82,000), building ($175,000), and accumulated

depreciation ($175,000 – $110,000 = $65,000) from the Katy,

(6) The $50,000 note that matures in 2018 is a current liability; the

(7) The portion of the installment note that will be repaid within one

(8) The $61,250 in deferred taxes should be separately classified

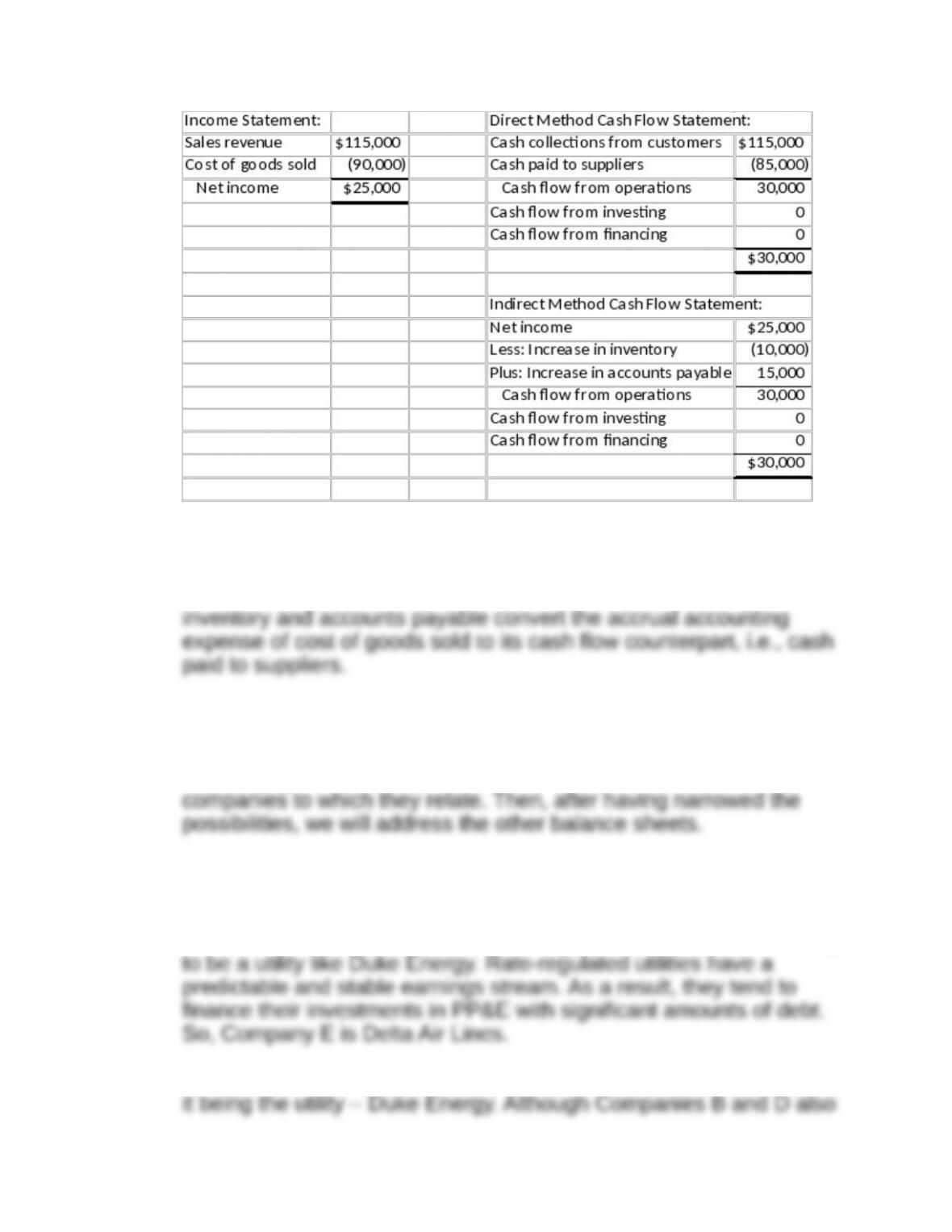

P4-4. Preparing the income statement and statement of cash flows

Requirement 1:

Requirement 2:

Because all sales are cash sales, sales revenue equals cash

collected from customers. The adjustments made for changes in

P4-5. Analyzing common-size financial statements

We will begin with the balance sheets with extremes and identify the

Company E has no inventory, so we can immediately rule out Alcoa

and Pfizer, two manufacturing concerns, as well retailer JCPenney.

That leaves only Duke Energy and Delta Air Lines as possibilities.

However, Company E does not have significant debt, so it is unlikely

Company A has significant PP&E and debt, which is consistent with

have significant amounts of PP&E and debt, those two companies

Company D has very large inventories and no receivables. The

large inventories suggest the retailer – JCPenney. The lack of

receivables is consistent with the company not providing any credit

That leaves Companies B and C for Alcoa and Pfizer. Company B

has significantly more PP&E while Company C has far more

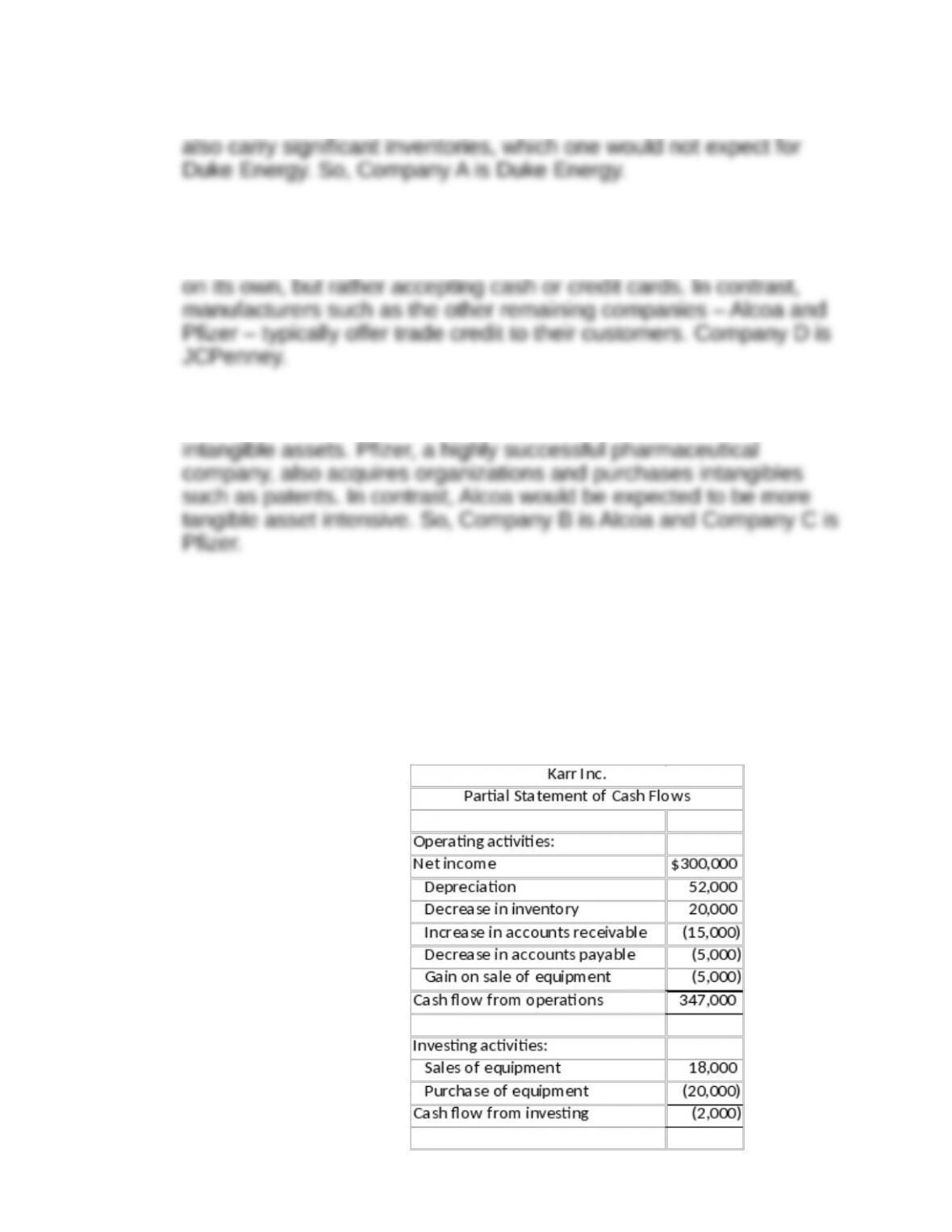

P4-6. Determining cash flows from operating and investing activities

(AICPA adapted)

Requirements 1 and 2:

Cash flow from operations and investing activities are computed

below.

Note that the purchase of equipment is shown at $20,000, not

$50,000. The $30,000 financed through Notes payable is excluded

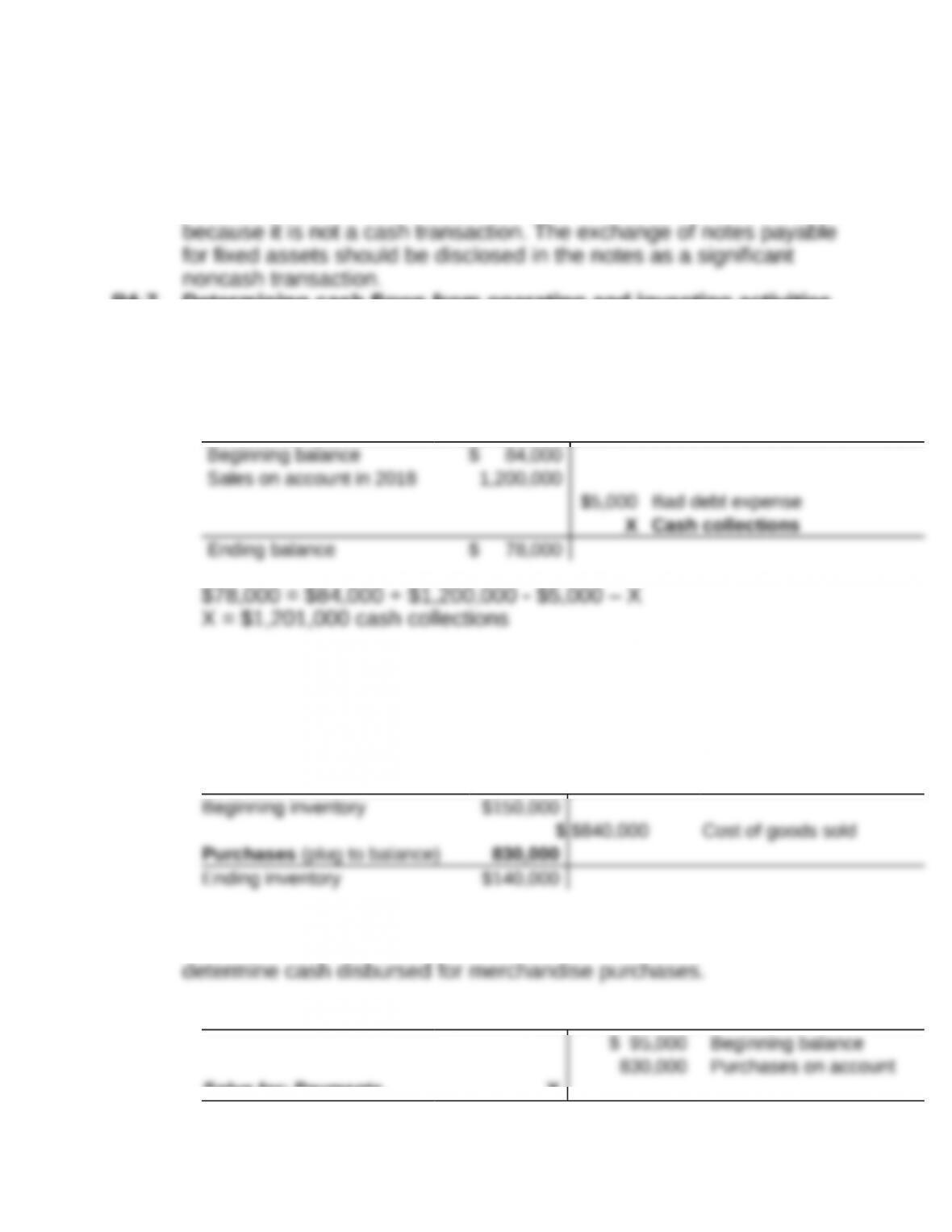

P4-7. Determining cash flows from operating and investing activities

(AICPA adapted)

Requirement 1:

Cash collected during 2018 can be shown by a T-account analysis:

Accounts Receivable – Net

Requirement 2:

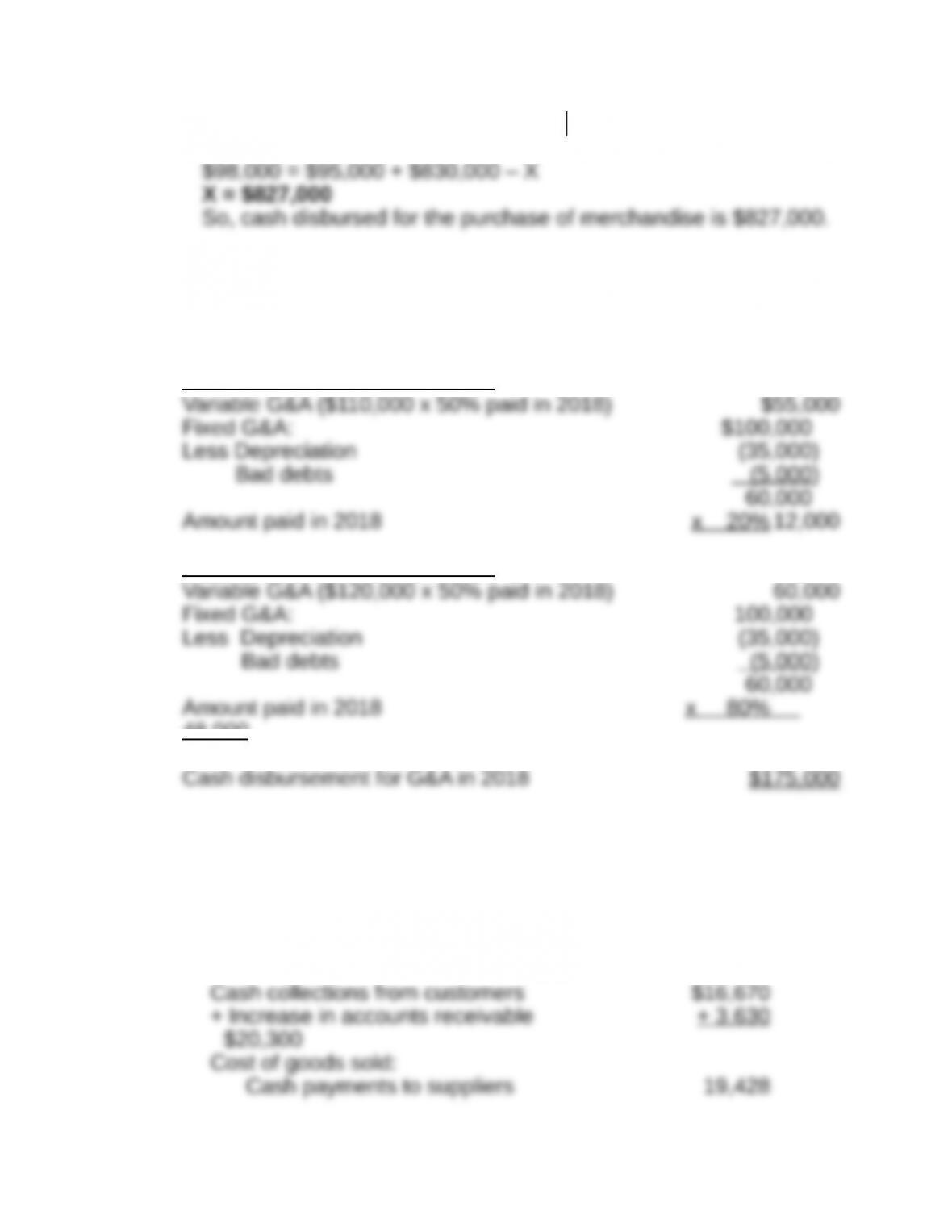

Cash disbursed for purchases of merchandise can be derived by

using

two T-accounts, inventory and accounts payable.

Inventory

Using the purchases on account we can analyze accounts payable

to

Accounts Payable

Solve for: Payments X

$ 98,000 Ending balance

Requirement 3:

Cash disbursed for general and administrative expenses in 2018 is

computed

below.

For expenses incurred in 2017

For expenses incurred in 2018

48,000

P4-8. Understanding the relation between the income statement,

cash flow statement, and changes in balance sheet accounts

Requirement 1:

Income statement

Sales:

Operating expenses:

Income before taxes

Income tax expense:

Net income

Requirement 2:

Cash provided by operating activities:

Net income

Plus/minus noncash items:

Plus/minus changes in current asset and liability accounts:

_(13,666)

Requirement 3:

Net income is $609, but cash used by operating activities is

$10,106. There are several causes of the difference. Accounts

inventory was purchased than is reported as cost of goods sold in

the income statement), accounts payable decreased in 2017 (i.e.,

cash paid to suppliers covered 2017 purchases as well as some

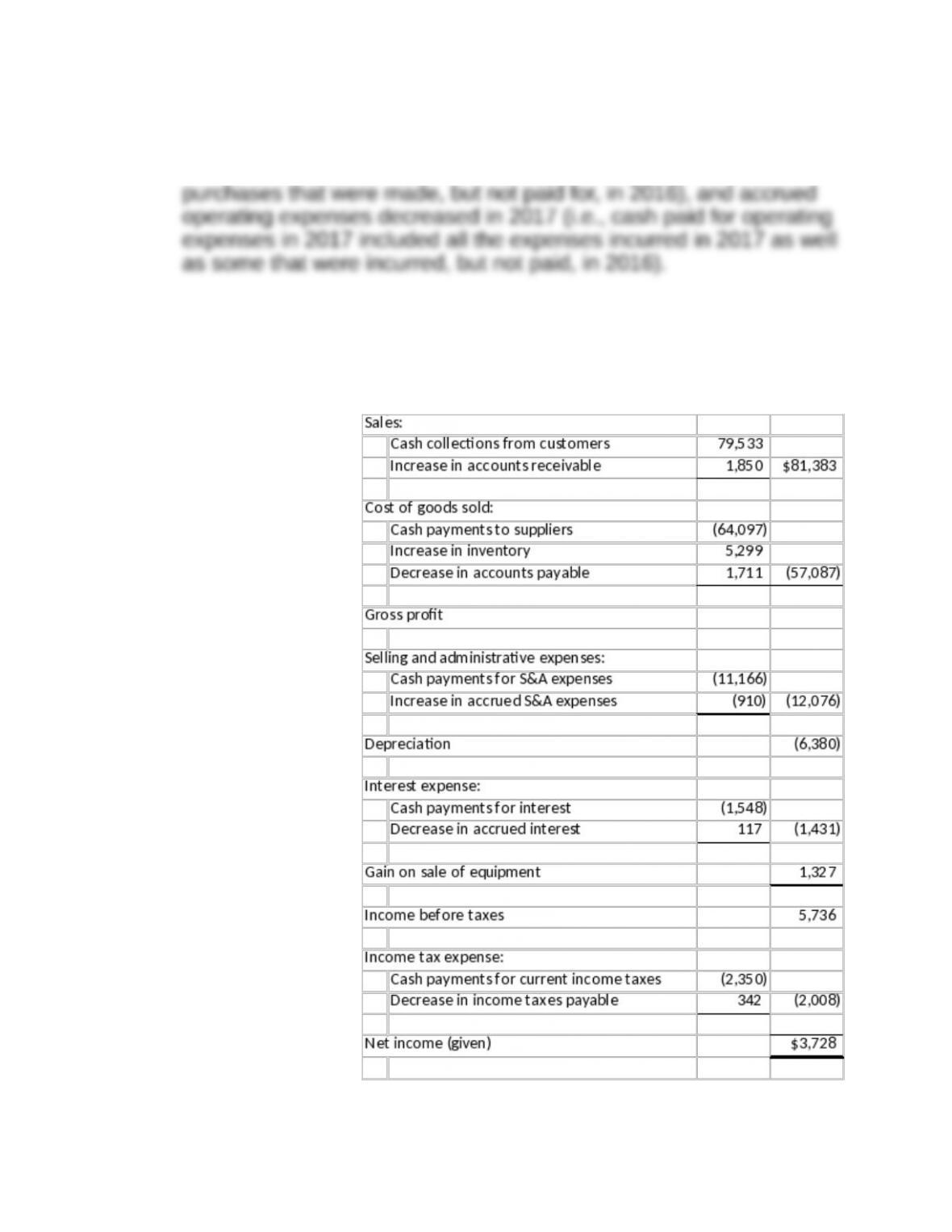

P4-9. Understanding the relation between income statement, cash

flow statement, and changes in balance sheet accounts

Requirement 1:

Requirement 2:

Cash provided by operating activities:

Plus/minus changes in current

asset and liability accounts:

– Increase in accounts receivable (1,850)

– Increase in inventory (5,299)

– Decrease in accounts payable (1,711)

+ Increase in accrued selling and

Requirement 3:

Net income is $3,728, while cash provided by operating activities is

only $372. There are several causes of the difference. First, $6,380

of depreciation expense reduced income, but it did not reduce cash

flow, so it is added back to net income to obtain cash from

operations. Accounts receivable increased during the year (i.e., not