Financial Reporting and Analysis (7th Ed.)

Chapter 8 Solutions

Receivables

Exercises

Exercises

E8-1. Analyzing accounts receivable (LO8-2)

(AICPA adapted)

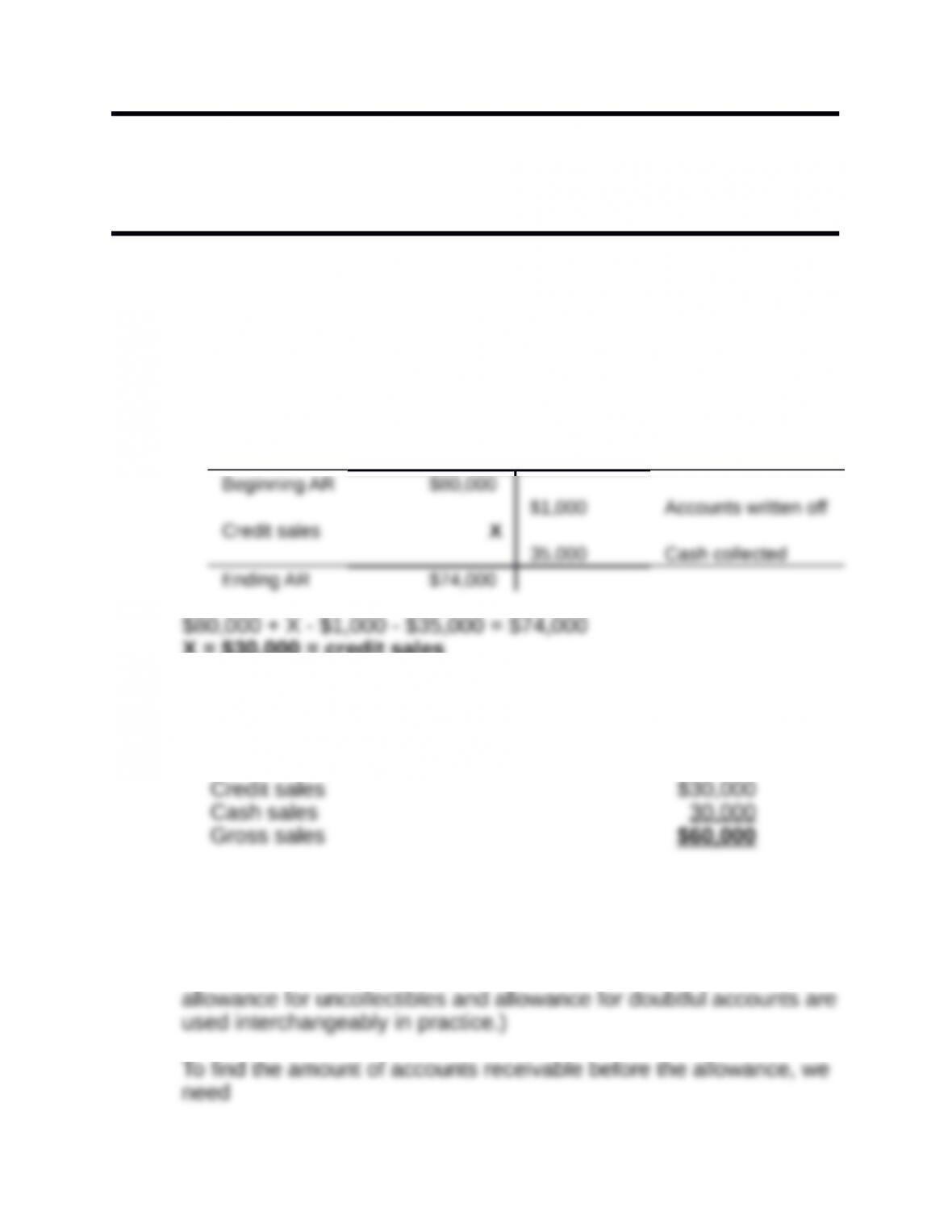

To find the amount of gross sales, start by determining credit sales.

We

can do this with the accounts receivable T-account below.

Accounts Receivable

X = $30,000 = credit sales

Now that we know the amount of credit sales, we can add cash

sales to

this amount to find gross sales.

E8-2. Analyzing accounts receivable (LO 8-2)

(AICPA adapted)

(Note to instructor: Students should be aware that the account

titles

to recreate the journal entries that affected accounts receivable and

CR Allowance for doubtful accounts

Based on the two entries above, the balance in the allowance for

doubtful accounts at the end of the year was $10,000. The amount

of

E8-3. Determining ratio effects of write-offs (LO 8-2)

(AICPA adapted)

1. The current ratio [$30,000/$10,000 = 3:1] does not change as a

result of the write-off to the allowance account. Accounts receivable

2. Net accounts receivable [prior: $3,300 − $300 = $3,000] does not

change as a result of the write-off to the allowance account [after:

b. X equals Y

3. Gross accounts receivable will be lower after the write-off than

before the write-off because accounts receivable is credited for the

a. X greater than Y

E8-4. Determining bad debt provision (LO 8-1)

(AICPA adapted)

Requirement 1:

Allowance for doubtful accounts

$1,450 Beginning balance

1,500 Provision for bad debts

Accounts written off $1,800

X Additional provision for bad debts

$1,600 Ending Balance

Solving for the additional provision for bad debts:

Total bad debt provision for the year ended December 31, 2017

should be:

Requirement 2:

To record the original provision for bad debts

To record the write-off of bad debts

To record the additional provision for bad debts

E8-5. Preparing an amortization schedule (LO 8-4)

(AICPA adapted)

The amortization table for Lake Company appears below.

Date Payments

Interest

Income

Reduction

of Principal

Net Installments

Due

*rounded

E8-6. Discounting a note (LO 8-6)

(AICPA adapted)

First, determine the value of the principal plus the interest.

Next, find the interest charged by the bank, discounted at 15% for

one-half year.

E8-7. Recording note receivable carrying amount and fair value

option (LO 8-4, LO 8-5) (AICPA adapted)

Requirement 1:

Calculation of the present value of Fletcher’s note at a 10% effective

rate of interest:

Present value of $200,000 principal repayment in 5 years at 10%

Present value of five interest payments of $12,000

($200,000 x .05) each at 10%:

Requirement 2:

$16,209

Requirement 3:

The difference between interest revenue and cash received increases

Requirement 4:

Calculation of the present value of Fletcher’s note at a 12% effective

rate of interest:

Present value of four remaining interest payments of

$12,000 ($200,000 x .05) each at 12%:

Requirement 5:

value= $10,823

E8-8. Aging accounts receivable (LO 8-1)

(AICPA adapted)

The estimated uncollectible accounts at December 31, 2017, total:

So, Vale should report an Allowance for uncollectible accounts of

$4,800.

E8-9. Analyzing accounts receivable and fair value option (LO 8-5)

(AICPA adapted)

Accounts receivable

Beginning balance $ 750,000

Ending balance X

The FASB defines fair value as “The price that would be received to

sell an asset or paid to transfer a liability in an orderly transaction

ending account balance or $1,320,700 = [$1,405,000 x 94%].

Because this offer was to purchase the receivables without

E8-10. Accounting for a securitization (LO-7)

Requirement 1:

FASB ASC 860-10-40-3 states that a financial asset should be

considered sold and therefore should be derecognized if it is

transferred and control is surrendered. As the problem’s

specifications state this to be the case, the entry to record the sale

follows:

DR Cash (or receivable from SE) $ 24,000,000

Requirement 2:

When control over the receivables is not surrendered, as in this

scenario, the transaction should be treated as a collateralized

borrowing:

E8-11. Determining whether it is a real sale (LO 8-3)

Years Ending December 31,

2017 2018 2019

Assuming that sales occur more or less uniformly over the course of

each month, approximately 15 days, on average, lapse before

Requirement 1: Sales growth

Sales grew by 3% in 2018 ([$1,839,559 – $1,785,980] ÷

$1,785,980), while receivables grew by 3.5% ([$227,896 –

Requirement 2: Potential problems

The data in 2018 do not suggest any potential problems because

growth rates in sales and accounts receivable should be roughly

Requirement 3: Possible explanations

A change in sales terms would not necessarily require any

corrective

be expected to experience difficulty in paying (promptly) and an

increase in the Allowance for uncollectibles is probably warranted.

accounts

E8-12. Calculating imputed interest on noninterest-bearing note (LO

8-4)

The cash selling price of the equipment is found by taking the

Data needed for the solution of this exercise is found in the following

amortization table.

(1) (2) (3)

Interest on Ending

Annual Previous Loan

Payment Balance* Balance

*(Column 3 for previous year times 12%)

E8-13. Factoring receivables with recourse (LO 8-6)

Requirement 1:

Requirement 2:

(or Gain on sale if received in a subsequent year)

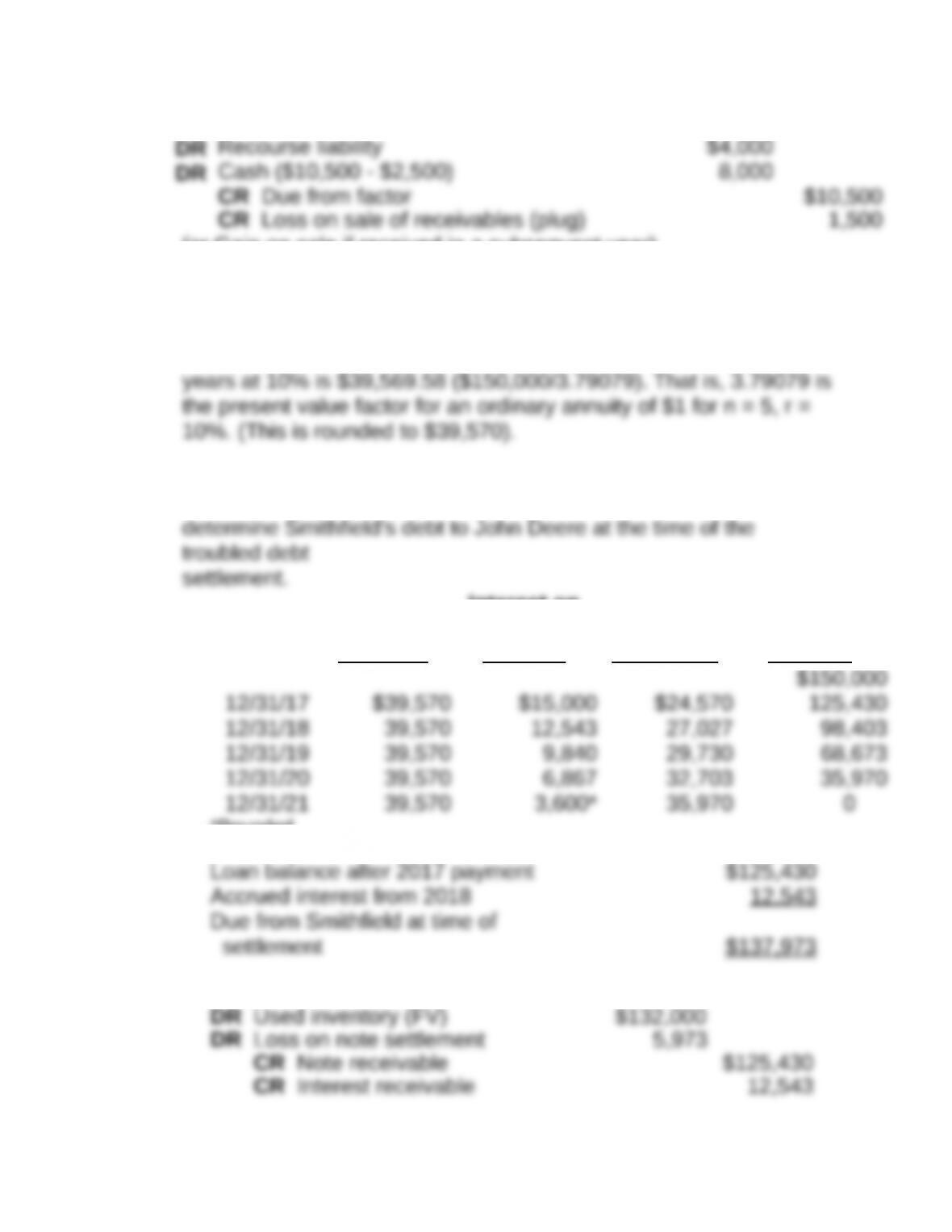

E8-14. Recording troubled debt settlement (LO 8-8)

The annual payment required to amortize the $150,000 loan over 5

The amortization table below schedules the principal and interest

breakdown for each of the required payments and can be used to

Interest on

Annual Previous Principal Loan

Payment Balance Reduction Balance

*Rounded

Journal entry:

E8-15. Recording troubled debt restructuring (LO 8-8)

CVC (borrower)

(a) To record the modified note (restructured cash flows less than

note

book value):

Buffalo Supply (lender)

(a) To record the modified note (restructured cash flows less than

note book value):

DR Restructured note receivable

The lender records the restructured note as the present value of the

future cash flows from the modified note using the effective interest