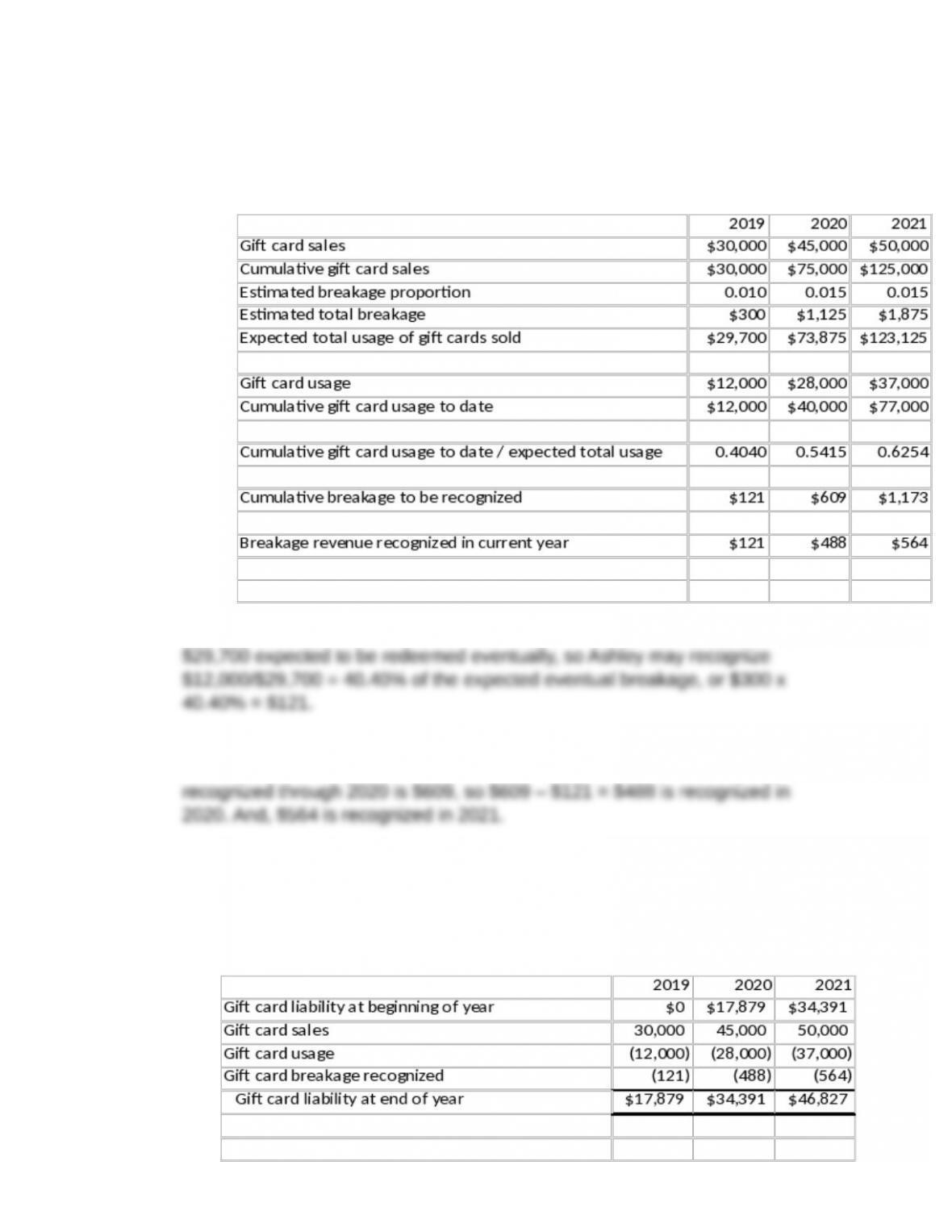

E3-20. Breakage

The following analysis shows the amount of breakage revenue Ashley recognizes in

each year.

At the end of 2019, Ashley estimates that $300 of gift cards will not be redeemed.

Gift card redemptions to date have totaled $12,000 out of the $30,000 – $300 =

At the end of 2020, a similar analysis is done, but on cumulative amounts and based

on a revised estimate of breakage. Total breakage revenue that may be

Requirement 2:

The following is an analysis of the amount of gift card liability to be reported at each

balance sheet date:

E3-21. Allocating the transaction price

The bike and the tune-ups are separate performance obligations. Under the residual

E3-22. Allocating the transaction price

The bike and the tune-ups are separate performance obligations. The standalone

Financial Reporting and Analysis (7th Edition)

Chapter 3 Solutions

Revenue Recognition

Problems

Problems

P3-1. Determining royalty revenue

(AICPA adapted)

Revenue recognition does not depend on when cash is collected. Royalty

revenue should be recognized as goods are transferred to the customer.

Royalties to be recognized in 2019 are as follows:

P3-2. Revenue recognition over time and at a point in time under ASC Topic 606

Requirement 1:

At the end of 2019, the project is 1/3 complete in terms of costs incurred ($8

million out of a current estimate of $24 million (8+16) in total costs). Given the

assumption that costs incurred measures the extent to which the performance

Requirement 2:

If revenue is measured at a point in time (i.e. upon completion of the project

Requirement 3:

Cornwell must evaluate the contract and determine whether any of the

following criteria are met:

The customer simultaneously receives and consumes the goods and

services as the performance obligation is satisfied.

Given the information provided, it is unlikely that either of the first two criteria

would be met. Cornwell is providing new construction, so the customer is

unlikely to be able to benefit from partial completion. Further, the customer

probably does not control the asset during the construction process. The third

criterion allows firms to recognize revenue over time even when the customer

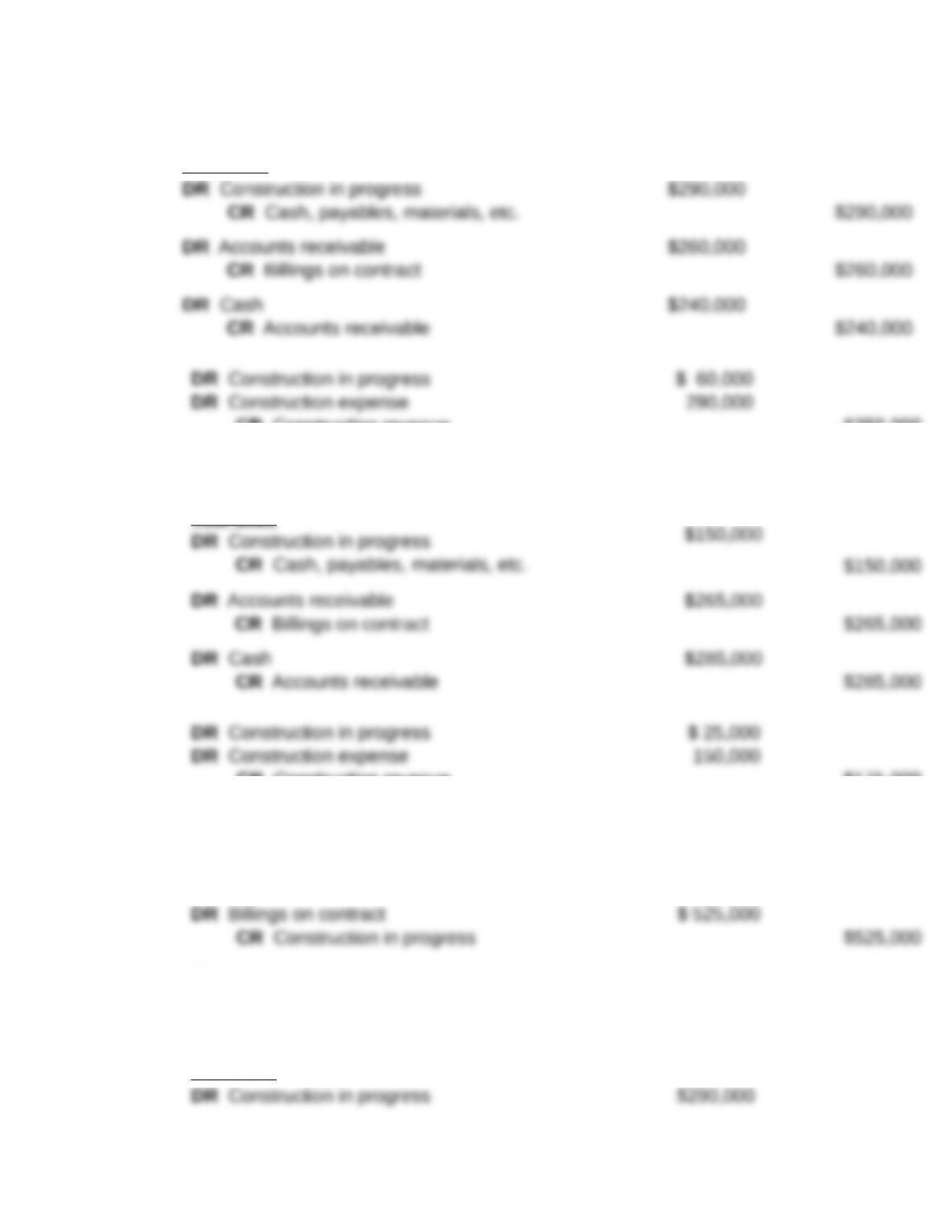

P3-3. Revenue recognition over time and at a point in time under ASC Topic 606

(AICPA adapted)

Requirement 1:

Revenue recognition over time

Year 2019

CR Construction revenue

$350,000

Revenue earned during the period: ($290,000/$435,000) x $525,000 = $350,000

Year 2020

CR Construction revenue

$175,000

Revenue earned during the period: ($440,000/$440,000) x $525,000 – $350,000

= $175,000

DR Billings on contract

$ 525,000

CR Cash, payables, materials, etc. $290,000

Because the project is incomplete, no revenue is recognized for the year

2019.

Year 2020

A comparison of amounts recognized under each method:

Recognition over time Recognition at a point in

time

Total 2019 2020 2019 2020

P3-4. Combining multiple contracts

Requirement 1:

Teuvo must combine the two contracts and treat them as a single contract

because they were entered into around the same time and serve a single

Requirement 2:

Teuvo now identifies the performance obligations. There are two performance

obligations: the goods from Contract A and the goods from Contract B. These

performance obligations have standalone selling prices of $85,000 and

Requirement 3:

Revenue should be recognized for each of the performance obligations when

P3-5. Combining multiple contracts

Requirement 1:

Panarin must combine the two contracts and treat them as a single contract

Requirement 2:

Panarin now identifies the performance obligations. There are two performance

obligations: the goods from Contract A and the goods from Contract B. These

Requirement 3:

Revenue should be recognized for each of the performance obligations when

P3-6. Multiple performance obligations

Requirement 1:

Quenneville must allocate the $500,000 transaction price to the two

the service contract and the remainder, or $410,000, to the equipment. (This

approach is appropriate if the price of the equipment is highly variable.) In

Requirement 2:

Quenneville expenses the $300,000 cost to manufacture the equipment,

resulting in earnings before taxes (EBT) related to the equipment of $500,000 –

$300,000 = $200,000. For the service contract, Quenneville expenses

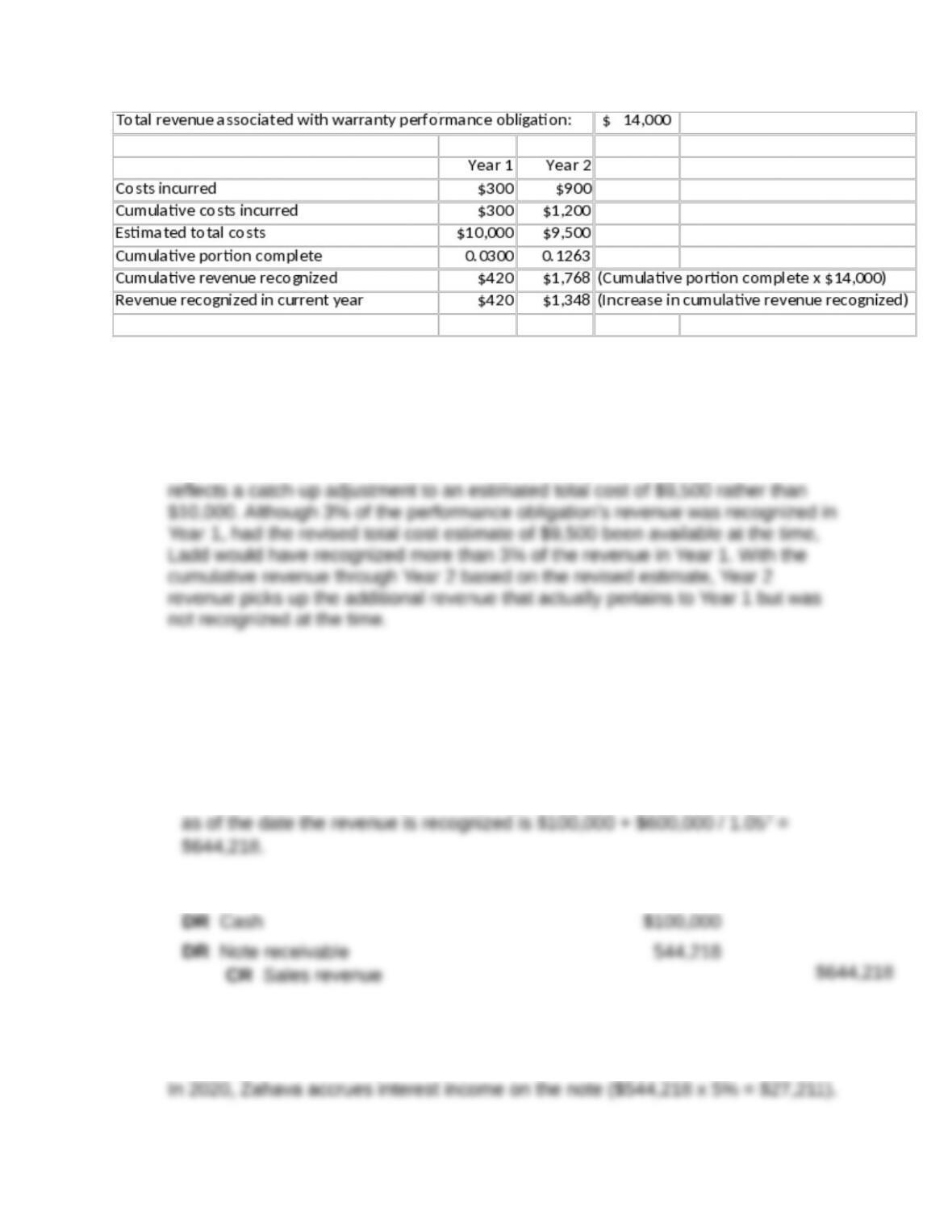

P3-7. Warranty; Revenue recognition over time

Requirement 1:

Ladd first determines the standalone price of the extended warranty to be

$10,000 x 140% = $14,000. Then Ladd applies the residual approach. It

Requirements 2 and 3:

Revenue on the extended warranty must be recognized over time, as the

customer obtains the benefits. Further, the pattern of revenue recognition

should reflect the transfer of benefits to the customer, which is not necessarily

The following analysis determines the amount of warranty revenue Ladd should

recognize in Year 1 and Year 2. The analysis determines for each year the

Ladd recognizes $420 of revenue in Year 1, resulting in Year 1 profit on the

warranty in of $420 – $300 = $120. In Year 2, revenue is $1,348 for profit of

$1,348 – $900 = $448. Note that revenue is more than proportionally greater in

Year 2 than Year 1. Although costs incurred were three times as great in Year 2

as Year 1, revenue was about 3.2 times greater ($1,348/$420), because it also

P3-8. Significant financing component

Requirement 1:

This transaction involves a significant financing component, with Zahava

providing its customer (Ari) with financing. The present value of Ari’s payments

Requirement 2:

Requirement 3:

In 2021, Zahava accrues additional interest income on the note. At the beginning

These two entries could be combined into a single entry with a credit to Notes

receivable of $571,429.

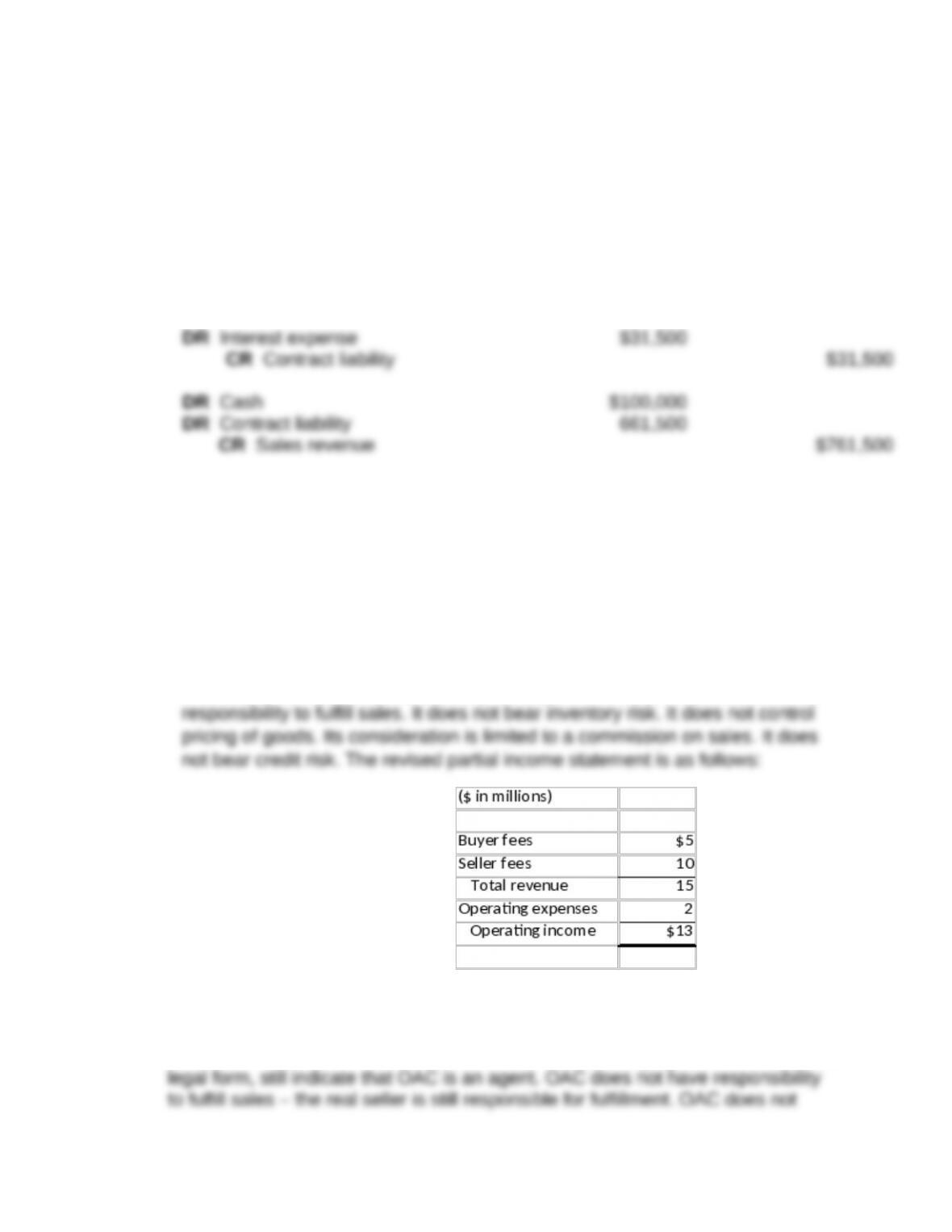

P3-9. Significant financing component

Requirement 1:

This transaction involves a significant financing component, with the customer

(Ari) providing Zahava with financing. The future value of Ari’s payments as of

Requirement 2:

5% = $30,000).

Requirement 3:

In 2021, Zahava accrues additional interest expense on the contract liability. At

the beginning of the year, the balance was $600,000 + $30,000 = $630,000, so

interest expense in 2021 is $630,000 x 5% = $31,500, bringing the contract

liabilty balance to $661,500. Combined with the $100,000 to be paid on

December 31, 2021, the total is the $761,500 to be recognized as sales revenue.

These two entries could be combined into a single entry with a debit to Contract

liability of $630,000.

P3-10. Principal vs. agent

Requirement 1:

OAC is clearly an agent, not a principal. Every one of the indicators provided in

ASC Topic 606 that an entity is an agent are present: OAC does not have

Requirement 2:

Altering the legal form of the transaction does not change the underlying

economics. All of the indicators, which relate to the underlying economics, not the

bear inventory risk. It does not control pricing of goods. Although legally