Financial Reporting and Analysis (7th Ed.)

Chapter 13 Solutions

Income Tax Reporting

Exercises

Exercises

E13-1. Determining current taxes due

(AICPA adapted)

Because Allen has no current income tax liability at December 31,

2016 and it made no estimated tax payments in 2017, the amount of

current income tax liability it would report at December 31, 2017 is

equal to its tax due for 2017, determined as follows:

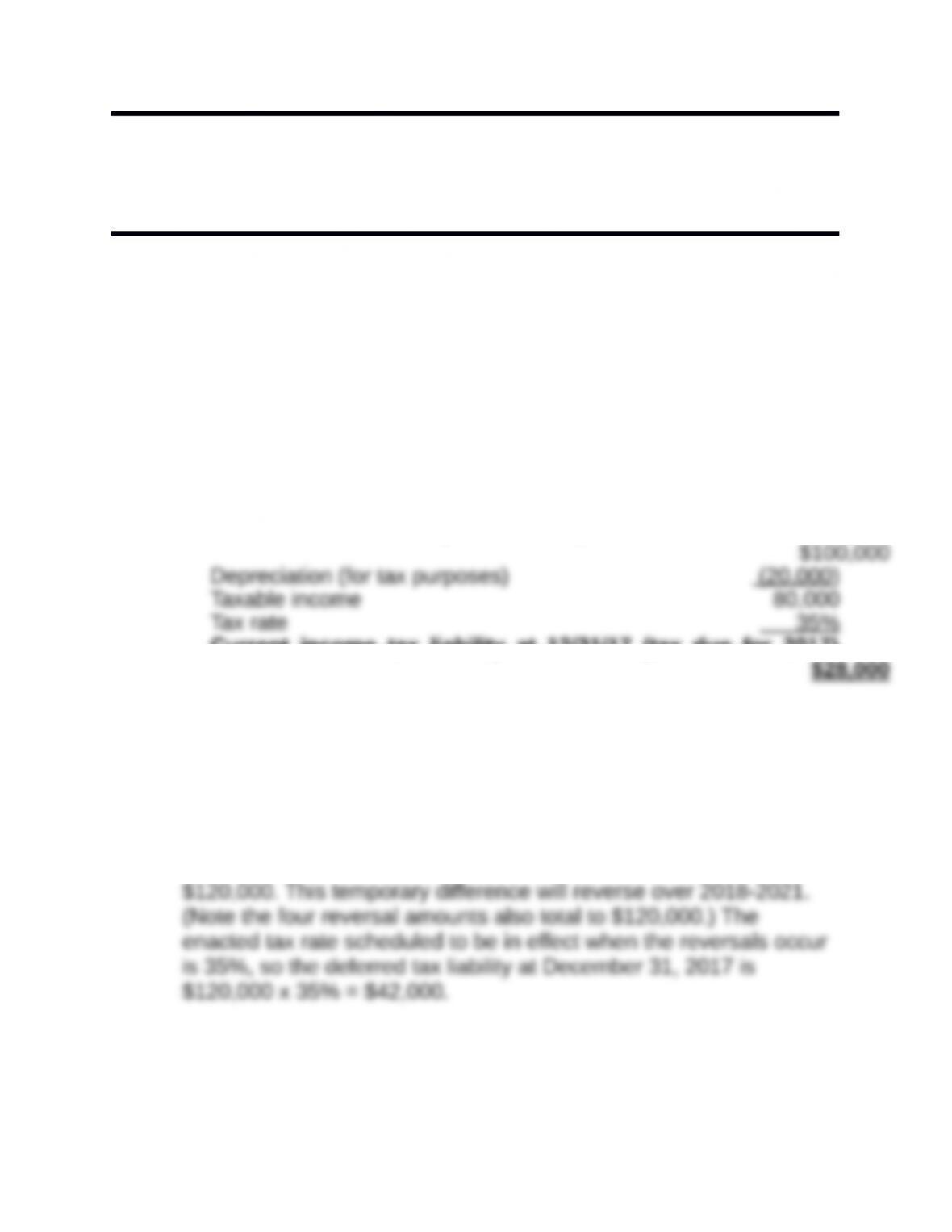

Net income before depreciation expense and income taxes

Current income tax liability at 12/31/17 (tax due for 2017)

E13-2. Determining deferred tax liability

(AICPA adapted)

Proceeds from officer’s life insurance is a permanent difference and

does not affect deferred tax calculations. Tow’s depreciation

deduction exceeded book depreciation by $370,000 – $250,000 =

E13-3. Determining deferred tax effects

(AICPA adapted)

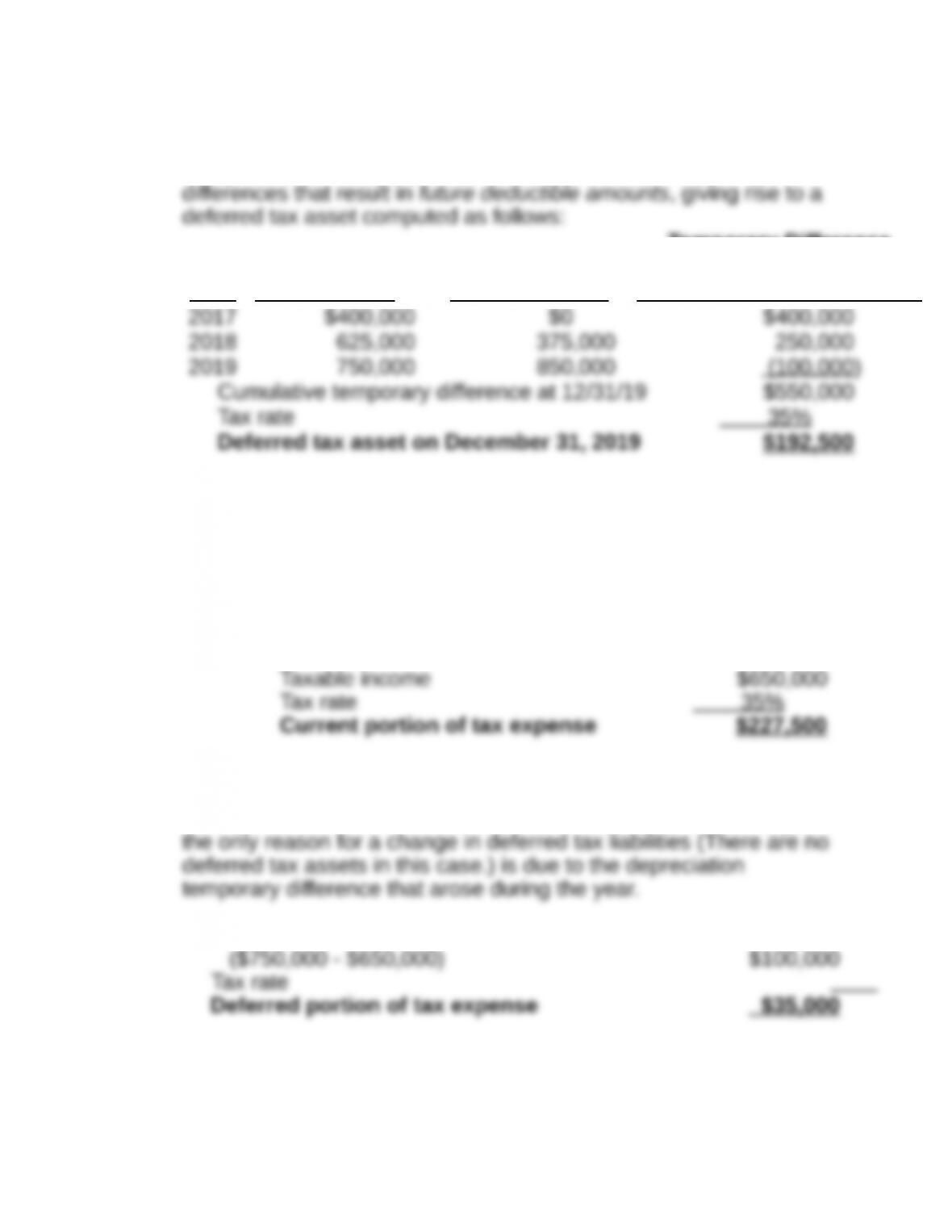

Because income recognized for tax purposes exceeds the income

recognized for book purposes, Mill has cumulative temporary

Year Tax purposes Book purposes

Temporary Difference

Increase (Decrease) in

Future Deductible Amounts

E13-4. Determining current portion of tax expense

(AICPA adapted)

Requirement 1:

The current portion of tax expense is the tax due to the IRS for

2017.

Requirement 2:

The deferred portion of tax expense is determined by the change in

deferred tax assets and liabilities. As the tax rate did not change,

Depreciation temporary difference in 2017

Requirement 3:

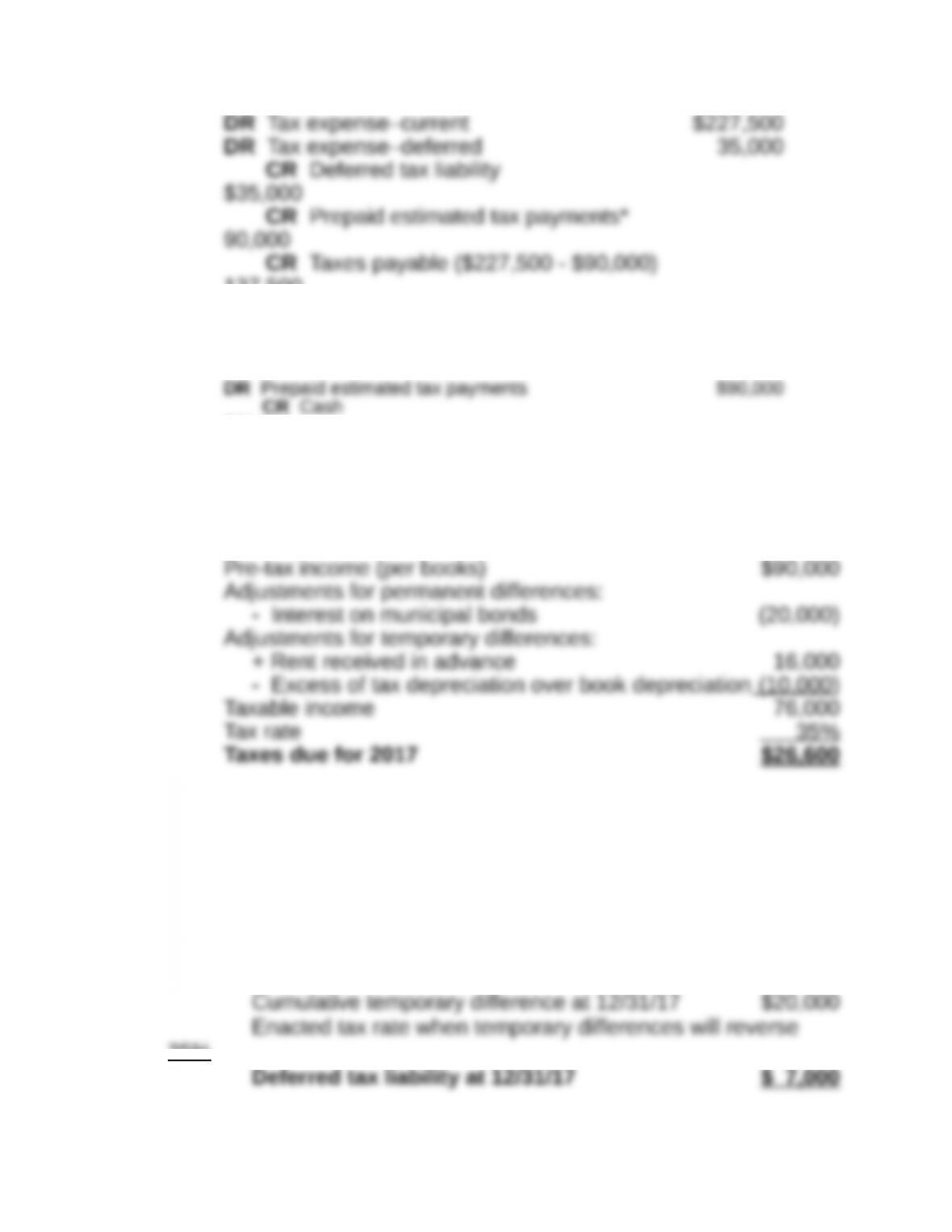

Journal entry to record tax expense for 2017:

137,500

*This credit assumes the following entry was made when Tyre made its

estimated tax payment during 2017:

CR Cash

$90,000

E13-5. Determining current taxes due

(AICPA adapted)

The calculation of Dunn’s taxes due for 2017 is as follows:

E13-6. Determining deferred tax liability and current portion of tax

expense

(AICPA adapted)

Requirement 1:

Deferred tax liability at December 31, 2017

35%

Requirement 2:

Current portion of 2017 tax expense

E13-7. Determining deferred tax asset amounts

(AICPA adapted)

(15,000)

E13-8. Determining deferred tax asset amounts

(AICPA adapted)

Requirement 1:

The warranty temporary differences give rise to future deductible

Requirement 2:

The future deductible amounts are multiplied by the enacted tax

Year

Reversal of Warranty

Temporary Difference

Enacted

Tax Rate

Deferred

Tax Asset

E13-9. Reporting deferred portion of tax expense

(AICPA adapted)

E13-10. Assessing temporary and permanent differences

(AICPA adapted)

Undistributed earnings that will be taxed in the

future when distributed as dividends (future

E13-11. Determining tax effects of loss carryback and carryforward

(AICPA adapted)

Requirement 1:

Tax benefit reported in 2017 income statement:

Requirement 2:

Deferred tax asset reported in 12/31/17 balance sheet:

Deferred tax asset reported in 12/31/17 balance sheet$

35,000

Requirement 3:

Amount of taxes paid related to 2018 tax return (current tax

provision):

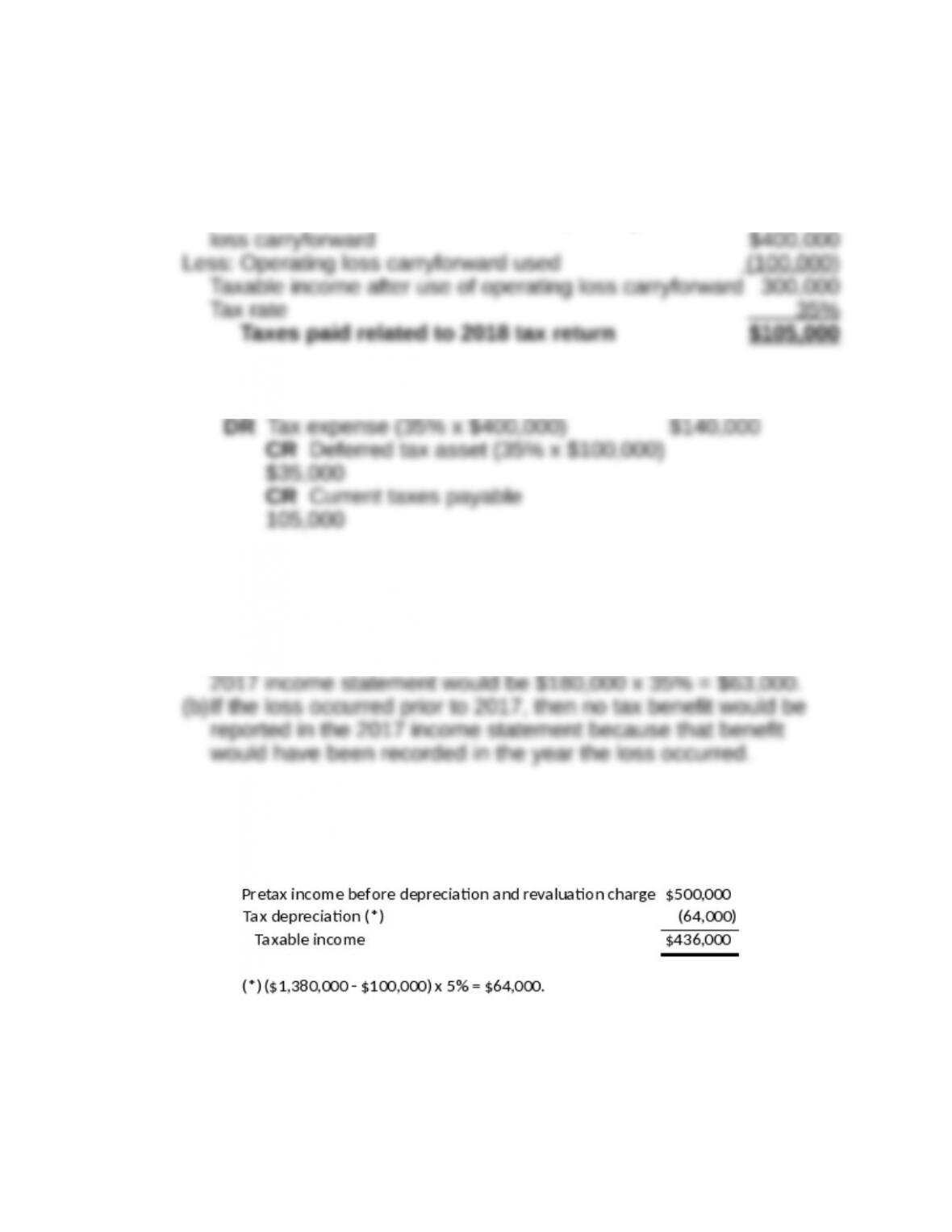

Taxable income in 2018 before use of operating

Entry to record 2018 taxes (not required):

E13-12. Accounting for loss carryforwards

(AICPA adapted)

(a)If the loss occurred in 2017, then the tax benefit reported in the

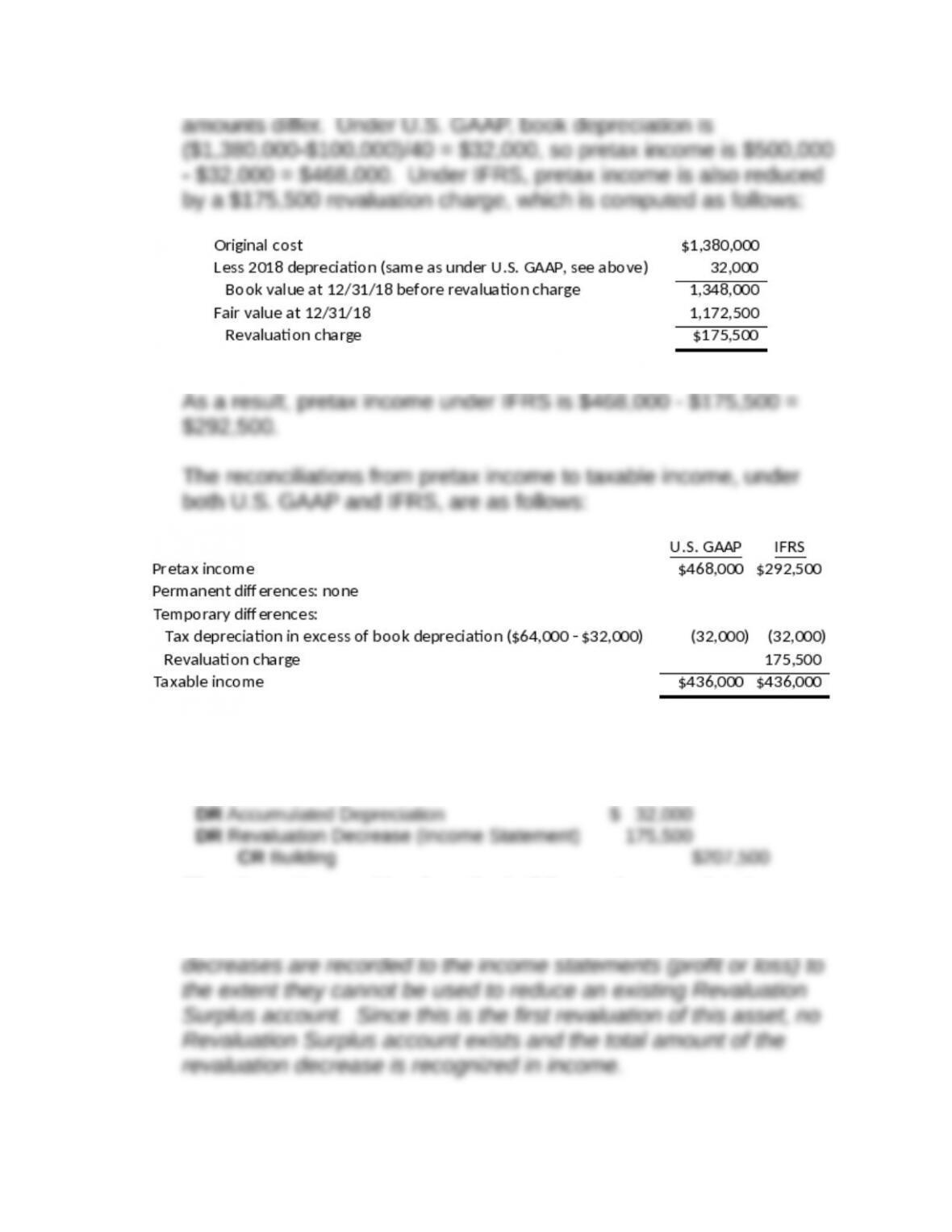

E13-13. IFRS vs. US GAAP tax entries

Requirement 1:

Note that taxable income can also be computed by reconciling from

pretax income for financial reporting purposes, and the result is the

same under U.S. GAAP and IFRS, although the reconciling

Note: The following is one of the allowed methods for recording the

revaluation.

The alternative would reduce the building and accumulated

depreciation accounts proportionately, so that the net book value

would equal fair value at the date of the revaluation. Revaluation

Requirement 2:

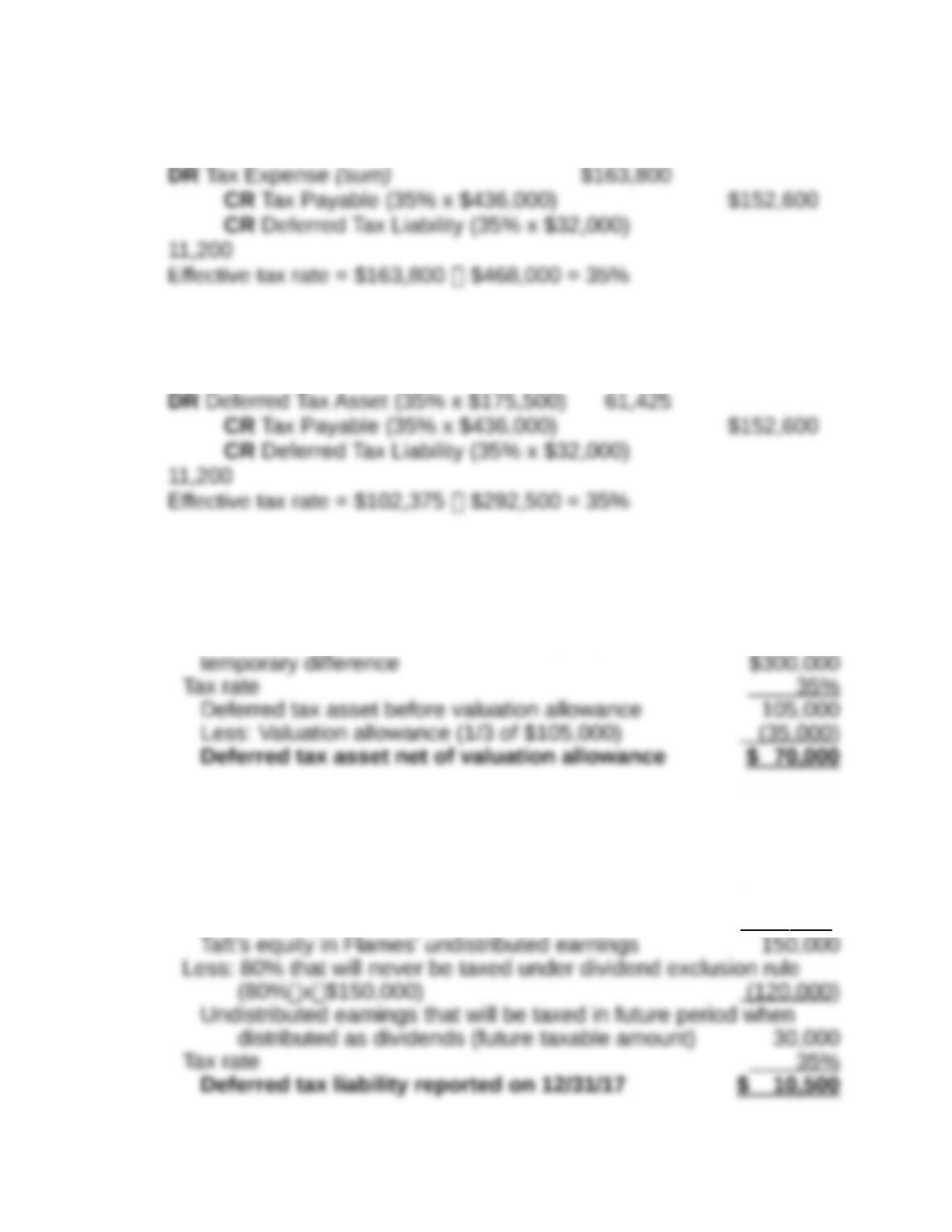

US GAAP:

Requirement 3:

IFRS:

DR Tax Expense (sum) $102,375

E13-14. Computing deferred tax asset and valuation allowance

(AICPA adapted)

Future deductible amount from warranty expense

E13-15. Determining deferred tax liability for equity method earnings

(AICPA adapted)

Taft’s equity in Flame’s earnings $180,000

Less: Dividends received from Flame (30 ,000)

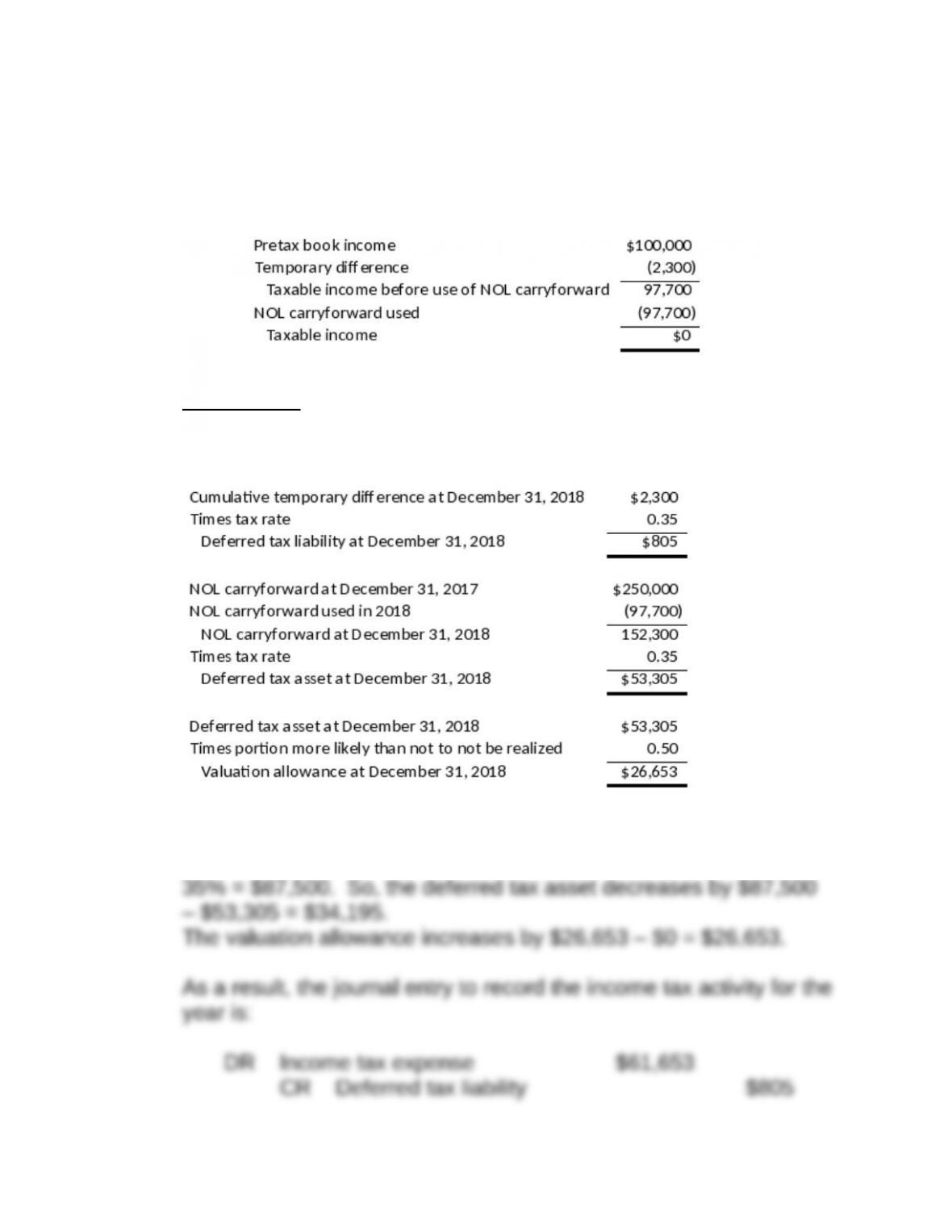

E13-16. IFRS vs. U.S. GAAP tax entries

The following reconciles TRR’s book income (which is the same

under U.S. GAAP and IFRS) and taxable income for 2018:

U.S. GAAP:

The following are the resulting amounts for deferred tax liability,

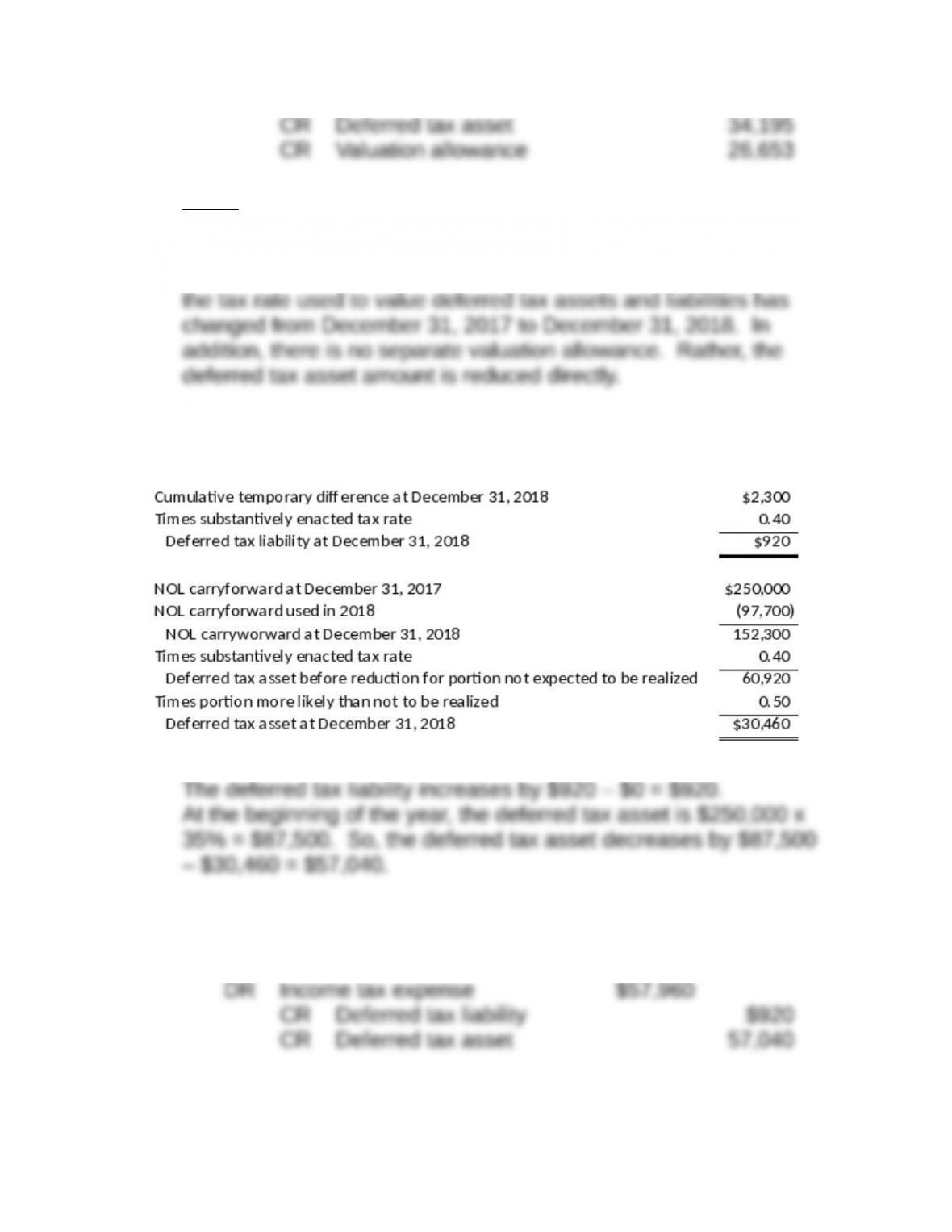

deferred tax asset, and valuation allowance at December 31, 2018:

The deferred tax liability increases by $805 – $0 = $805.

At the beginning of the year, the deferred tax asset is $250,000 x

IFRS:

There are several differences under IFRS relative to U.S. GAAP. At

December 31, 2018, the substantively enacted tax rate, which is

40%, is used to value deferred tax assets and liabilities. As a result,

The following are the resulting amounts for deferred tax liability and

deferred tax asset at December 31, 2018:

As a result, the journal entry to record the income tax activity for the

year is:

Note that the difference between the income tax expense amounts

under U.S. GAAP and IFRS ($61,653 – $57,960 = $3,693) can be

Note that if, as expected, legislation is fully completed in 2019 and