Financial Reporting and Analysis (7th Ed.)

Chapter 2 Solutions

Accrual Accounting and Income Determination

Exercises

Exercises

E2-1. Distinguishing accrual-basis revenue from cash receipts

(AICPA adapted)

Because the subscription begins with the first issue of 2018, no

E2-2. Converting from cash receipts to accrual-basis revenue

(AICPA adapted)

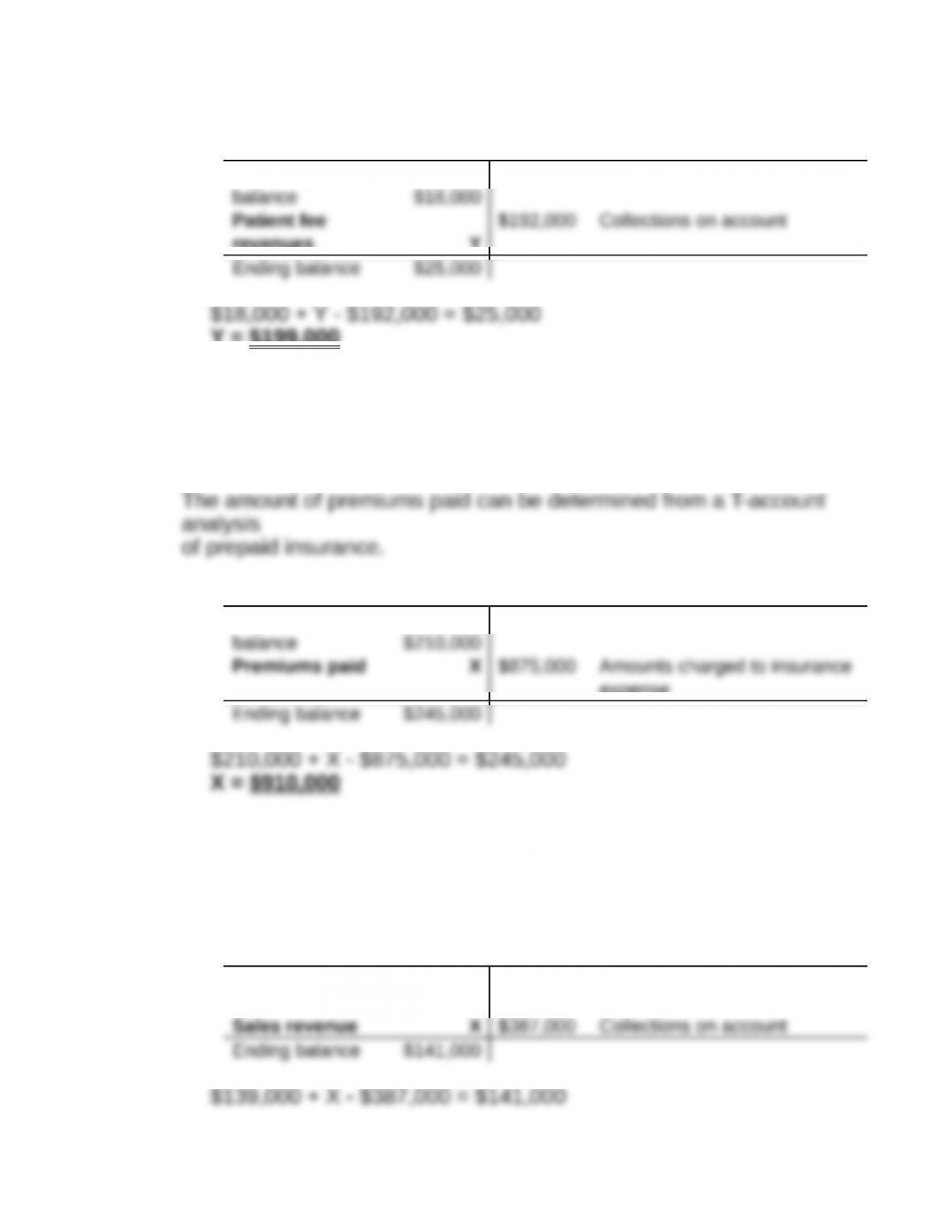

We first analyze the activity in the Deferred fee revenue account,

which is shown below. This account represents the liability to

Deferred Fee Revenue

$0 Beginning balance

$8,000 Ending balance

The account increased by $8,000, which is explained by $8,000

of payments received in advance of revenue being recognized.

In total, Dr. Hamilton received $200,000 from patients, so

Accounts Receivable

Beginning

Y = $199,000

E2-3. Distinguishing between accrual basis expense and cash

disbursement

(AICPA adapted)

Prepaid Insurance

Beginning

expense

E2-4. Converting from cash to accrual basis

We first determine sales revenue by analyzing Accounts receivable.

Accounts Receivable

Beginning

balance $139,000

X = $389,000

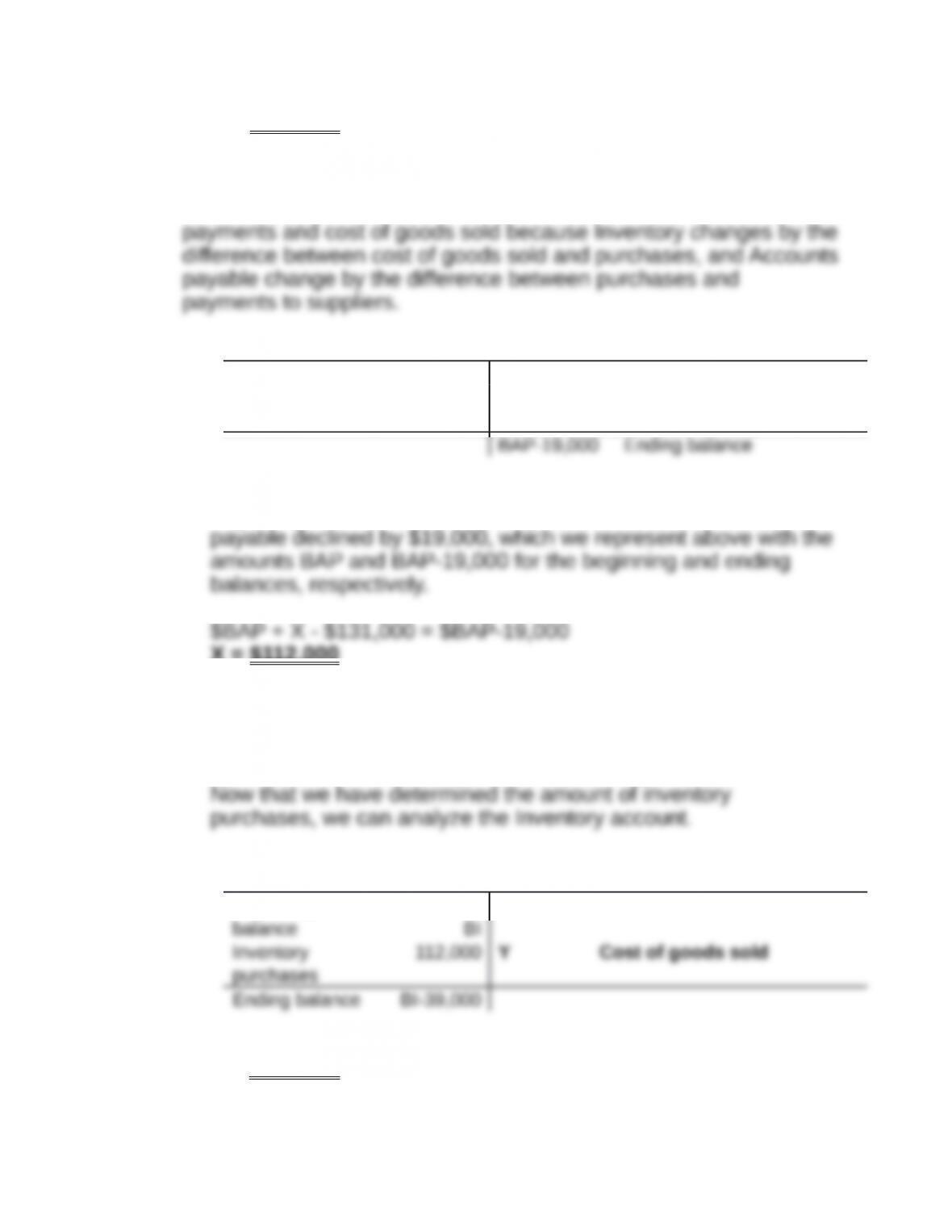

In order to determine cost of goods sold, we must analyze two

accounts – Inventory and Accounts payable. Each of these

accounts explains a portion of the difference between cash

Accounts Payable

BAP Beginning balance

Payments on

account

$131,000 X Inventory purchases

We do not know the amount of Accounts payable at either the

beginning or the end of the year, but we do know Accounts

X = $112,000

The analysis indicates that knowing the change in Accounts

payable is sufficient to determine the difference between

purchases and payments.

Inventory

Beginning

$BI + $112,000 – Y = $BI – $39,000

Y = $151,000

As was the case for Accounts payable, we do not know the

E2-5. Preparing a multiple-step income statement

Hardrock Mining Co.

Income Statement

Year Ended December 31, 2017

($ in 000)

The “Other, net” caption as originally reported is broken down as

follows:

* “Other, net” as originally reported ($ in 000)

$54,529

Less: Restructuring charge

(8,777)

Plus: Discontinued operations

12 ,000

Investment losses

$57 ,752

Discontinued operations are presented “net of tax” as calculated

below. The “restructuring loss” is infrequent, thus it is a separately

disclosed component of operating income. Removing these two

items from “Other, net” leaves only the investment losses in the

original caption, which should be relabeled “investment losses.”

The foreign currency loss ($55,000) does not surpass any

reasonable materiality threshold (e.g., greater than 1% of net

Per share disclosures are required on the face of the income

E2-6. Income statement presentation

Event 1 is a discontinued operation and would appear on the

income statement below income from continuing operations. To

qualify for discontinued operation treatment, the sold component

Event 2 would be reported as an unusual or infrequently occurring

Event 3 is also an unusual or infrequently occurring item, included in

Event 4 is a change in accounting principle and would require

presented for comparative purposes would be restated to reflect the

average cost method of inventory costing). The current year income

Event 5 is a change in accounting estimate and thus would be

included in income from continuing operations. No special income

statement disclosure of this event is required. Depreciation expense

Event 6 is an unusual on infrequently occurring item and thus would

Event 7 is an unusual or infrequently occurring item and thus would

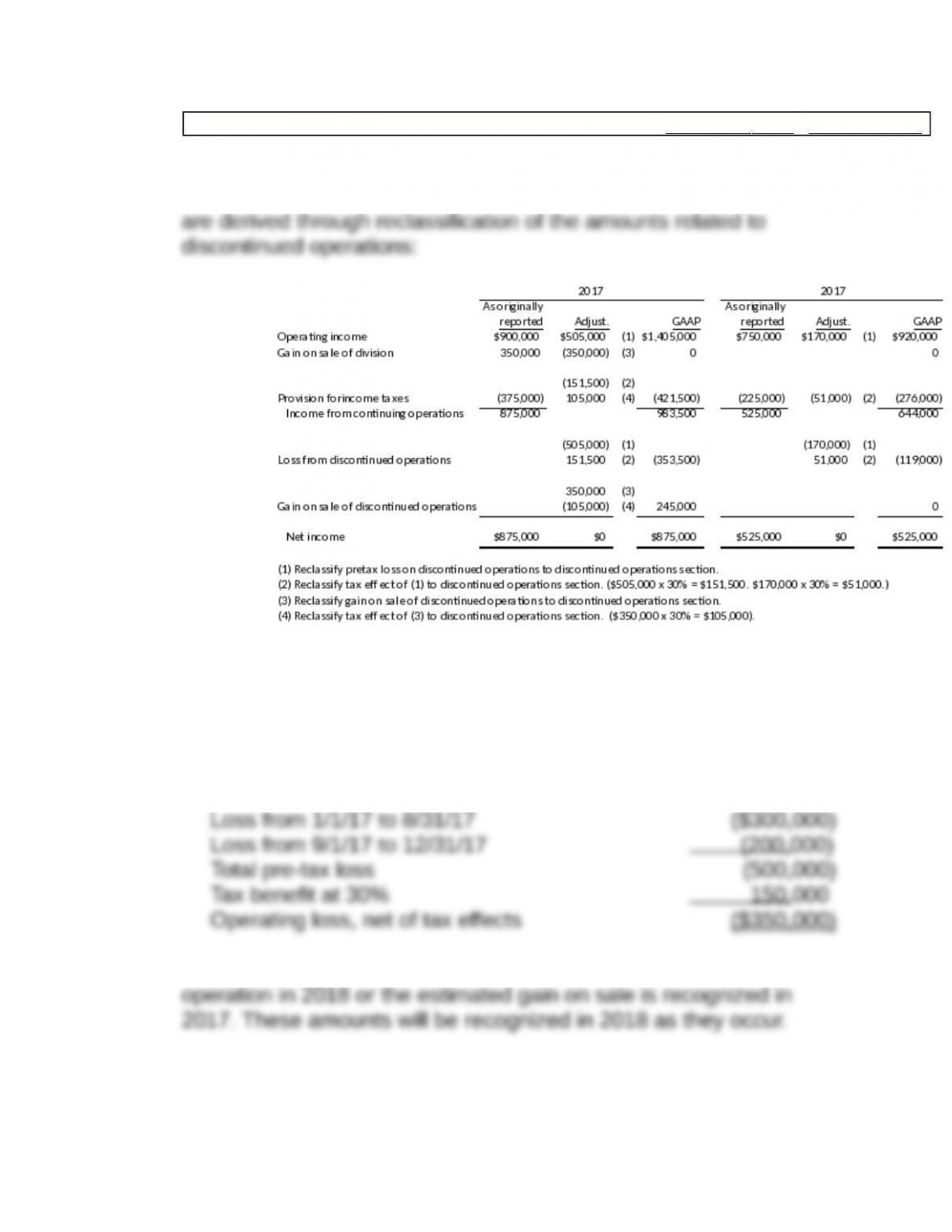

E2-7. Determining gain (loss) from discontinued operations

Munnster Corporation

Partial Income Statement

For the Years Ended December 31

2017 2016

Operating income

$ 1,405,000

$ 920,000

Provision for income taxes

421 ,500

276 ,000

Income from continuing operations 983,500 644,000

Discontinued operations:

Loss from discontinued division, net of

tax benefits of $151,500 in 2017 and

$51,000 in 2016

(353,500)

(119,000)

Gain from sale of discontinued division,

net of taxes of $105,000

245 ,000

– 0 –

Net income

$ 875 ,000

$ 525 ,000

The following analysis shows how the revised income statements

E2-8. Determining loss on discontinued operations

The results of operations of an entity classified as held for sale are

to be reported in discontinued operations in the periods in which

they occur (net of tax effects). For Revsine, the loss from operations

for the discontinued segment would be $350,000 determined as

follows:

None of the expected profit from operating the discontinued

E2-9. Determining period vs. product costs

Period Cost Traceable Cost

1These are product costs; i.e. costs incurred in the manufacturing

2Rent for inventory warehousing could be argued to be a product

3Bad debt expense is typically deducted from sales to arrive at Net

4Advertising is not part of the manufacturing process and typically

5Warranty expense is matched against sales in the period in which

the products subject to warranties are sold, not when the warranty

E2-10. Change in inventory methods

Requirement 1:

Retained earnings balance at January 1,

Requirement 2:

1/1/2017 To record a change in inventory method

E2-11. Determining effect of omitting year-end adjusting entries

OS = overstated

US = understated

NE = no effect

Net

Item Assets Liabilities Income

1. Supplies Inventory

Revenue not recorded = $6,000 from July 1, 2017 to December 31, 2017

3. Gasoline Expense

Direction of effect NE US OS

Interest expense for 9 months not accrued = $50,000 x 0.12 x 9/12 = $4,500

5. Depreciation Expense

Direction of effect OS NE OS