E2-12. Error Correction

Requirement 1:

At the end of 2016, inventory is understated by $8,000 and must be corrected.

Accumulated depreciation is overstated by $22,300 – $6,000 = $16,300 and

must also be corrected. Note that we determined these amounts differently.

Inventory is a balance sheet account and we are given the amount by which it

The correcting journal entry is as follows:

To understand why the balancing line of the entry is in Retained earnings,

consider how the Inventory and Accumulated depreciation accounts became

misstated. Amounts in the Inventory account at the beginning of a period or

added to Inventory during the year are in one of two places at the end of the

Requirement 2:

Assuming it is material, the error is corrected by restating all misstated periods

retroactively. The 2017 financial statements will present prior periods as

E2-13. Error correction

Requirement 1:

At the end of 2016, Inventory is understated by $40,000. In addition, Equipment

To understand why the balancing line of the entry is in Retained earnings,

consider how the Inventory, Equipment, and Accumulated depreciation accounts

became misstated. Amounts in the Inventory account at the beginning of a period

or added to Inventory during the year are in one of two places at the end of the

year. They have either been expensed through cost of goods sold or are in the

ending Inventory account balance. Therefore, for every dollar by which Inventory

is too low, cost of goods sold, cumulatively over the life of the firm, has been too

Requirement 2:

Assuming it is material, the error is corrected by restating all misstated periods

retroactively. The 2017 financial statements will present prior periods as

E2-14. Correction of errors

Requirement 1:

a) This error affected ending inventory in 2016 and beginning inventory in 2017.

Because inventory errors “self-correct” over a two-year period, and the 2017

financial statements have been issued, no entry is required. However, if

comparative financial statements are issued in 2018, income as presented for

b) To correct error and reflect remaining insurance at January 1, 2018:

DR Prepaid insurance $21,000

CR Retained earnings $21,000

c) To correct error and reflect equipment and accumulated depreciation:

DR Equipment $100,000

CR Retained earnings $80,000

CR Accumulated depreciation 20,000

Requirement 2:

a) This error does not affect the 2018 financial statements.

b) Insurance expense should be recorded at the rate of $12,000 per year as

the policy expires. If the error were not corrected, income in 2018 would be

c) Failure to correct this error would leave total assets understated by $60,000

at the end of 2018. ($100,000 equipment cost – $40,000 accumulated

E2-15. Preparing comprehensive income statement

JDW Corporation

Income Statement and Statement

of Comprehensive Income

For the Year Ended December 31, 2017

Sales $ 2,929,500

Cost of goods sold (1,786,995)

Gross profit 1,142,505

*$556,605 x 30% = $166,982

**$22,000 x 30% = $6,600

***$7,000 x 30% = $2,100

E2-16. Wellington International Airport Limited – Reporting asset revaluations in

OCI.

Requirement 1:

Revaluations occur when the company hires and then receives a valuation report

from a professional appraiser. The company has no current interest in selling the

land or property, plant, and equipment, so any changes in value are unrealized.

Requirement 2:

The values of land and property, plant, and equipment went up because the

Requirement 3:

U.S. GAAP does not allow for upward Revaluation of land or property, plant, and

equipment. Therefore there would be no entry observed for Revaluation in Other

Comprehensive Income.

Financial Reporting and Analysis (7th Ed.)

Chapter 2 Solutions

Accrual Accounting and Income Determination

Problems

Problems

P2-1. Preparing journal entries and statement

Requirement 1:

1/1/17: To record cash contributed by owners

3/1/17: No entry upon signing of contract

7/1/17: To record purchase of office equipment

12/31/17: To record advance-consulting fees received from Norbert Corp.

Only one year’s rent is expensed in the income statement for 2017. The

balance will be expensed in next year’s income statement.

Revenue is recognized in 2017 because Frances Corp. has fulfilled its

obligation to provide services.

To accrue salaries expense for December 2017.

Requirement 3:

Frances Corporation

Income Statement

For Year Ended December 31, 2017

Requirement 4:

Frances Corporation

Balance Sheet

December 31, 2017

Assets

Equipment $100,000

Less: Accumulated depr. 10 ,000

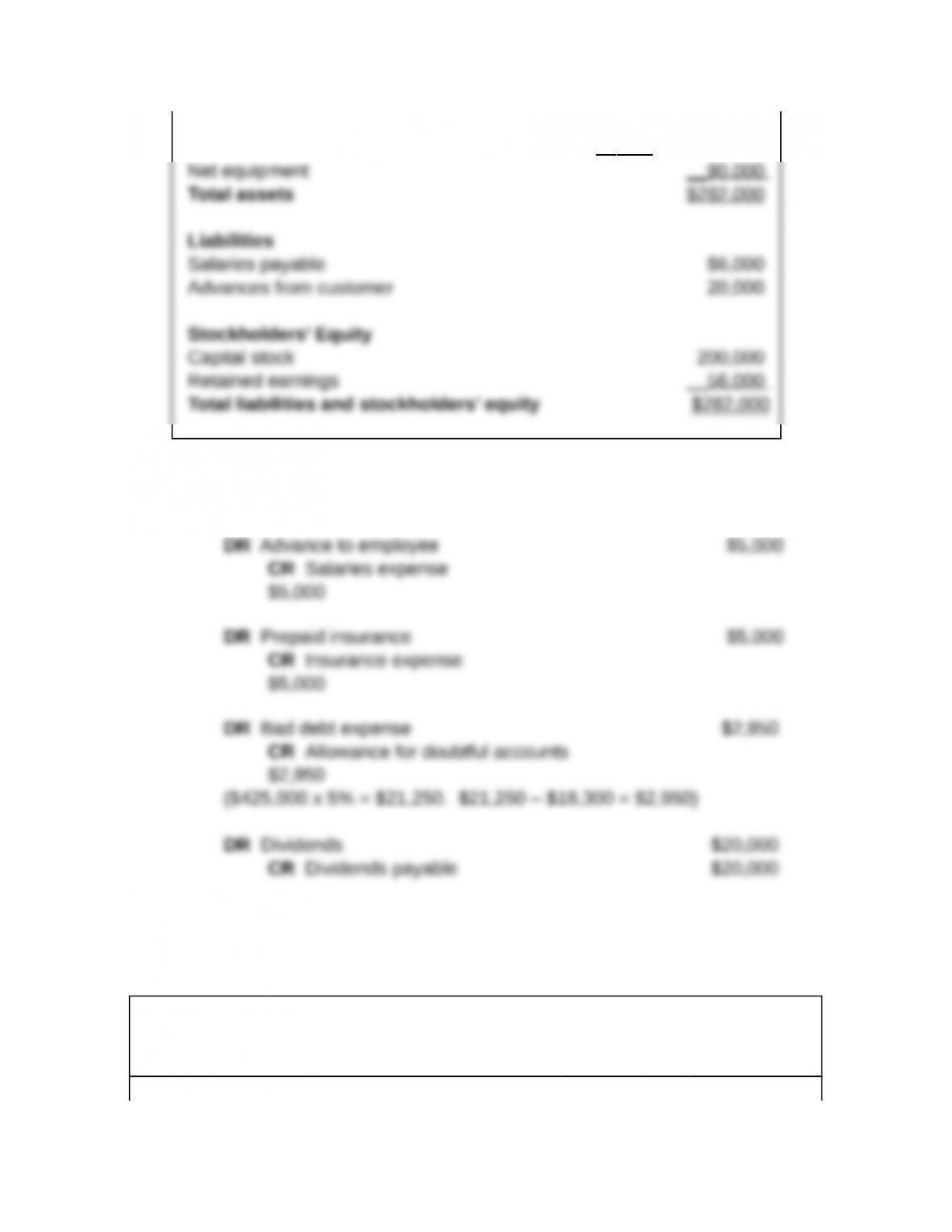

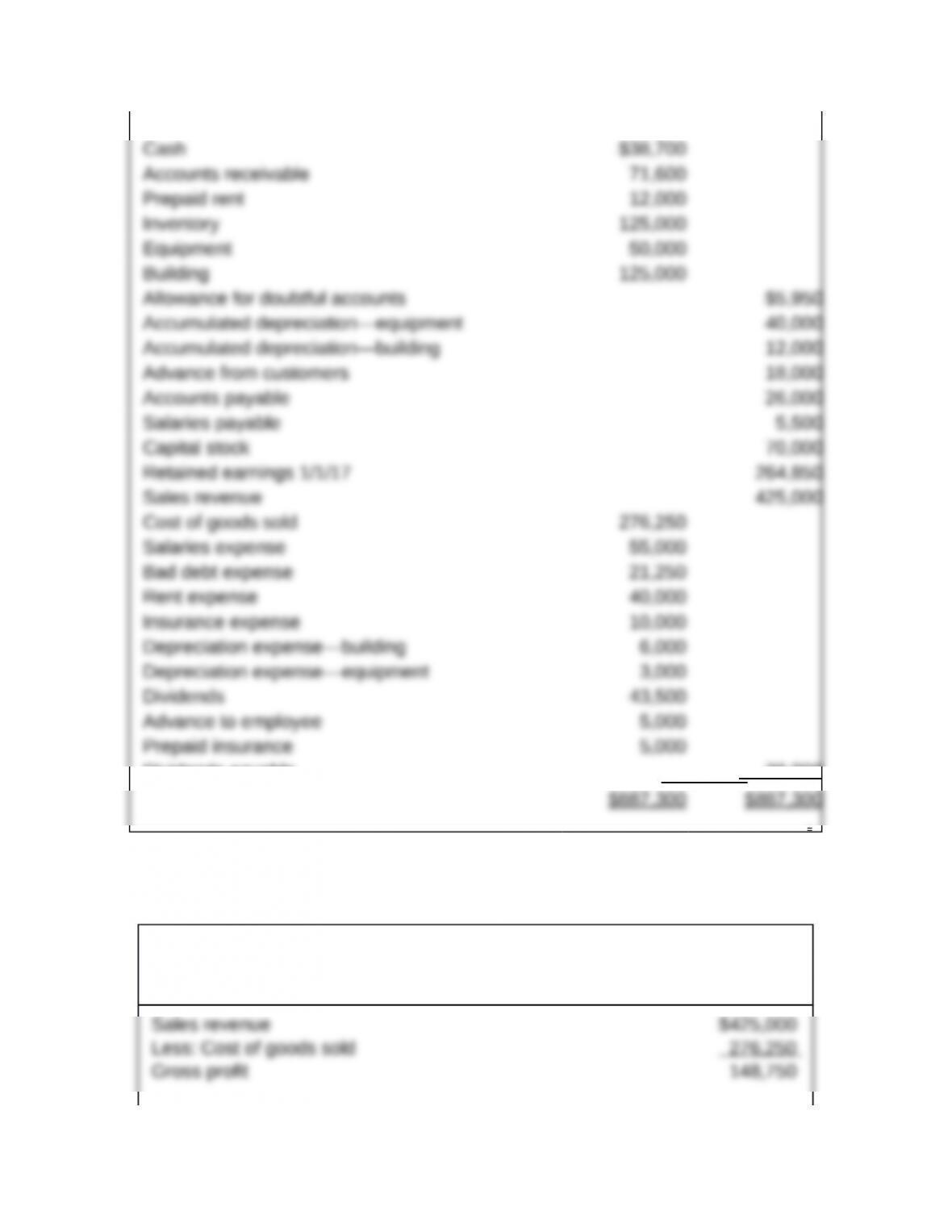

P2-2. Making adjusting entries and statement preparation

Requirement 1:

Before preparing the financial statements, let us re-construct the trial balance

after incorporating all the adjusting entries:

Ralph Retailers, Inc.

Adjusted Preclosing Trial Balance

As of December 31, 2017

Debit Credit

Dividends payable 20 ,000

Requirement 2:

Ralph Retailers, Inc.

Income Statement

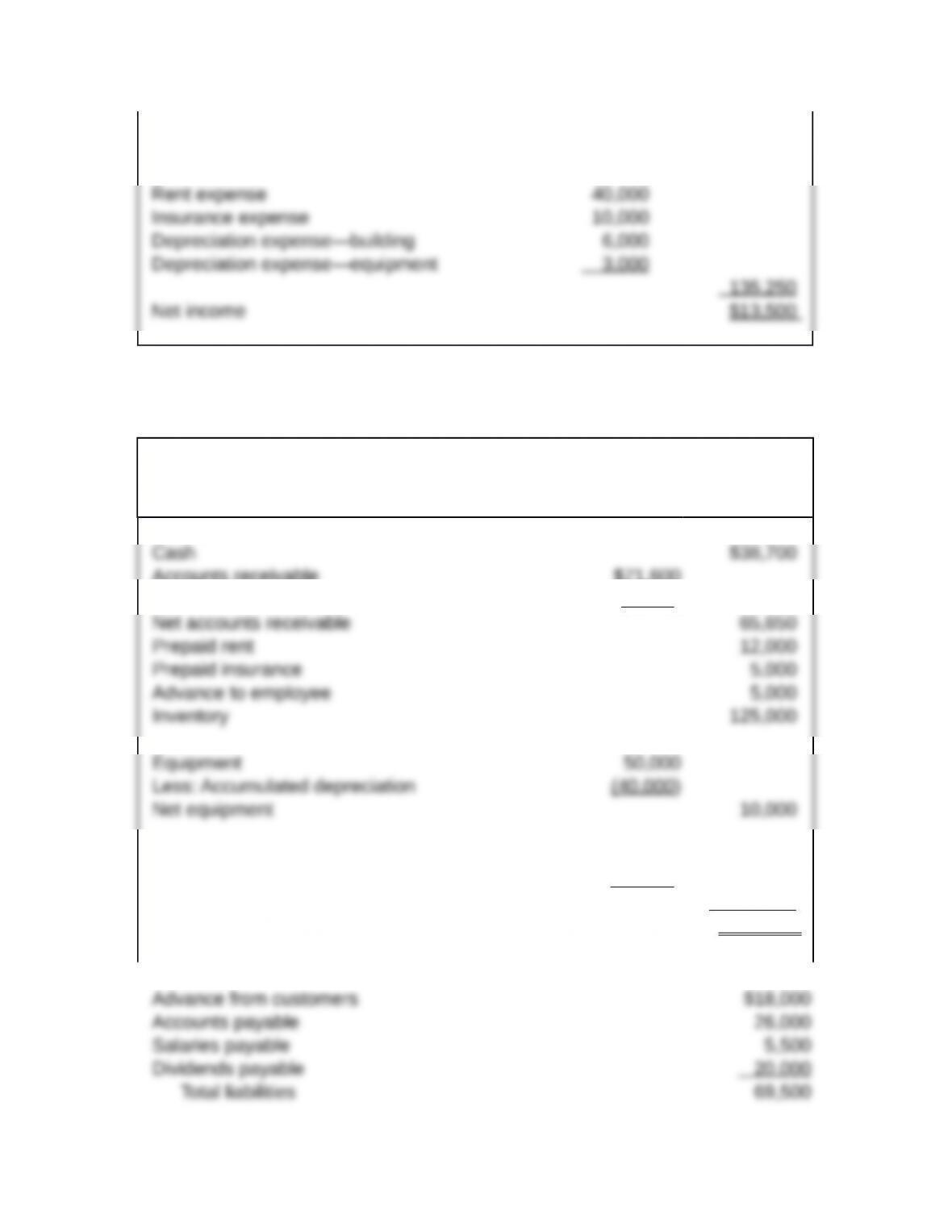

For Year Ended December 31, 2017

Less: Operating expenses

Salaries expense $55,000

Bad debt expense 21,250

Requirement 3:

Ralph Retailers, Inc.

Balance Sheet

December 31, 2017

Assets

Accounts receivable $71,600

Less: Allowance for doubtful accounts (5 ,950)

Building 125,000

Less: Accumulated depreciation (12 ,000)

Net building 113,000

Total assets $374,350

Liabilities

Shareholders’ equity