P8-15. Accounting for transfer of receivables (LO 8-6)

It seems that Ricoh Company is treating the discounting of receivables

as a sale. Note that Ricoh indicates that “trade notes receivable

discounted are contingent liabilities.” If Ricoh had treated the

Crown Crafts appear to use a similar accounting treatment, i.e., the

money received from the factor is considered as a liquidation of the

receivables.

There are substantial differences in the economics of the transactions.

Crown Craft transfers the receivable without recourse as to credit

losses, i.e., in effect, the factor becomes the “true” owner of the

receivables by bearing the credit risk. Whereas, Ricoh is still

responsible for all the credit risk since the transfers are with full

recourse, i.e., Ricoh retains the economic risk (i.e., risk of credit

losses) of owning the receivables. However, Foxmeyer falls

P8-16. Determining whether existing receivables represent real sales

(LO 8-3)

Requirement 1:

© 2018 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale

or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted

on a website, in whole or part. 8-1

The shipment of the 19 motors to Macco Corporation do not represent

sales, but a transfer of inventory from one point (Moto-Lite’s factory) to

The remaining ten aircraft engines at Macco’s represent consigned

Requirement 2:

As stated above, the aircraft engines at Macco’s facility represent

Moto-Lite (consigned) inventory until they are placed into Macco’s

production process. The nine engines used by Macco would be

included in Moto-Lites sales for the quarter ending October 31.

Moto-Lite Company

Summary of Overstatements

Accounts Gross Profit

Description Receivable Sales (35% of sales)

Originally recorded:

Inventory is understated by $39,000. This is determined as follows.

The average cost of each engine is $3,900 (i.e., $6,000 selling price

© 2018 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale

or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted

on a website, in whole or part. 8-2

Financial Reporting and Analysis (7th Ed.)

Chapter 8 Solutions

Receivables

Cases

Cases

C8-1. Garrels Company: Analyzing allowances—Comprehensive (LO

8-2)

Requirement 1:

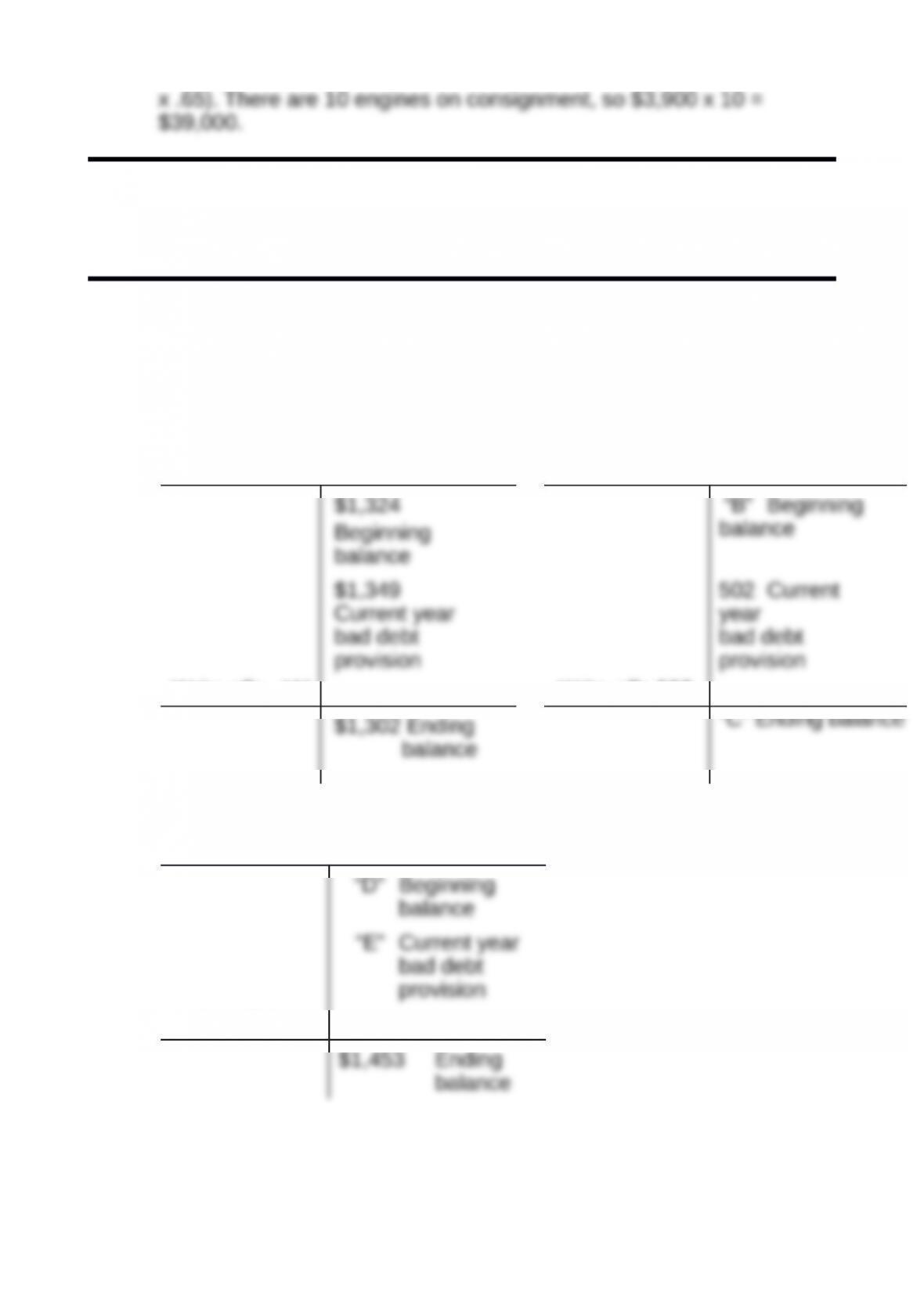

Allowance for Doubtful Accounts

(2015)

Allowance for doubtful

accounts (2016)

Write-offs “A” Write-offs 622

“C” Ending balance

Allowance for Doubtful Accounts

(2017)

Write-Offs 1

2015:

© 2018 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale

or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted

on a website, in whole or part. 8-3

End. balance = beg. Balance + current year bad debt provision –

write-offs

2016:

B = Beginning balance in 2016 = ending balance in 2015 = $1,302

End. Balance 2016 = Beg. balance + current year bad debt provision –

write-offs

C = $1,302 + $502 – $622

2017:

D = Beginning balance in 2017 = ending balance in 2016 = $1,182

End. balance 2017 = Beg. balance + current year bad debt provision –

write-offs

Requirements 2 & 3:

Allowance method Direct write-off

2015

DR Allowance for doubtful

2016

DR Allowance for doubtful

© 2018 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale

or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted

on a website, in whole or part. 8-4

CR Allowance for doubtful

Requirement 4:

The allowance method is consistent with the matching principle

underlying the accrual accounting model, whereas the direct write-off

method is not.

Requirement 5:

The cumulative income difference is equal to the change in the

balance of the allowance account from 2015 to 2017.

So income under the allowance method would be $129 lower since

the allowance has increased by $129. To “prove” this, subtract the

Income

Difference

Year

Requirement 6:

If the firm wanted to be conservative, the initial provision could be

increased by the entire $300,000. If the firm wanted to be optimistic,

© 2018 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale

or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted

on a website, in whole or part. 8-5

make an estimate of the probability that the customer will go bankrupt

(e.g., 35.0%), and then the initial provision could be increased by this

probability times the $300,000(i.e., $105,000). Management’s

Requirement 7:

a) Here, the CFO might want to take the entire $300,000 thousand as

an additional provision because earnings before income taxes of $11

million is well below the bonus plan minimum of $17 million. In other

b) Here, the CFO might not want to take any additional bad debt

provision because earnings before income taxes of $18.02 million is

above the bonus plan minimum of $17 million. Every dollar of extra

c) Here, the CFO might want to take the entire $300,000 as an

additional bad debt provision because earnings before income taxes

of $38.25 million exceeds the ceiling of the bonus plan ($27 million).

Here, management doesn’t lose any bonus money by taking any or all

d) Here, management might want to take an additional provision of

$150,000 because earnings before income taxes of $27.15 million

The moral of the story is that management’s financial reporting

decisions are not going to be made in isolation of other factors.

Requirement 8:

© 2018 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale

or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted

on a website, in whole or part. 8-6

Managers might use the provision for bad debts to help avoid violation

of debt covenant restrictions that are written in terms of accounting

numbers. Some debt contracts contain minimum (or maximum) levels

that various financial ratios must adhere to or the firm will be declared

Requirement 9:

“Managing” a financial statement item suggests the ability to influence

net income and the pattern of net income growth from year to year.

a) Depreciation method choice.

C8-2. Citigroup, Inc.: Analyzing allowance for loan losses (LO 8-2, LO 8-7)

Requirement 1 – Allowance for loans

Details of Citigroup’s Credit Loss Experience are reproduced below (in

millions).

2009 2008 2007 2006 2005

© 2018 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale

or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted

on a website, in whole or part. 8-7

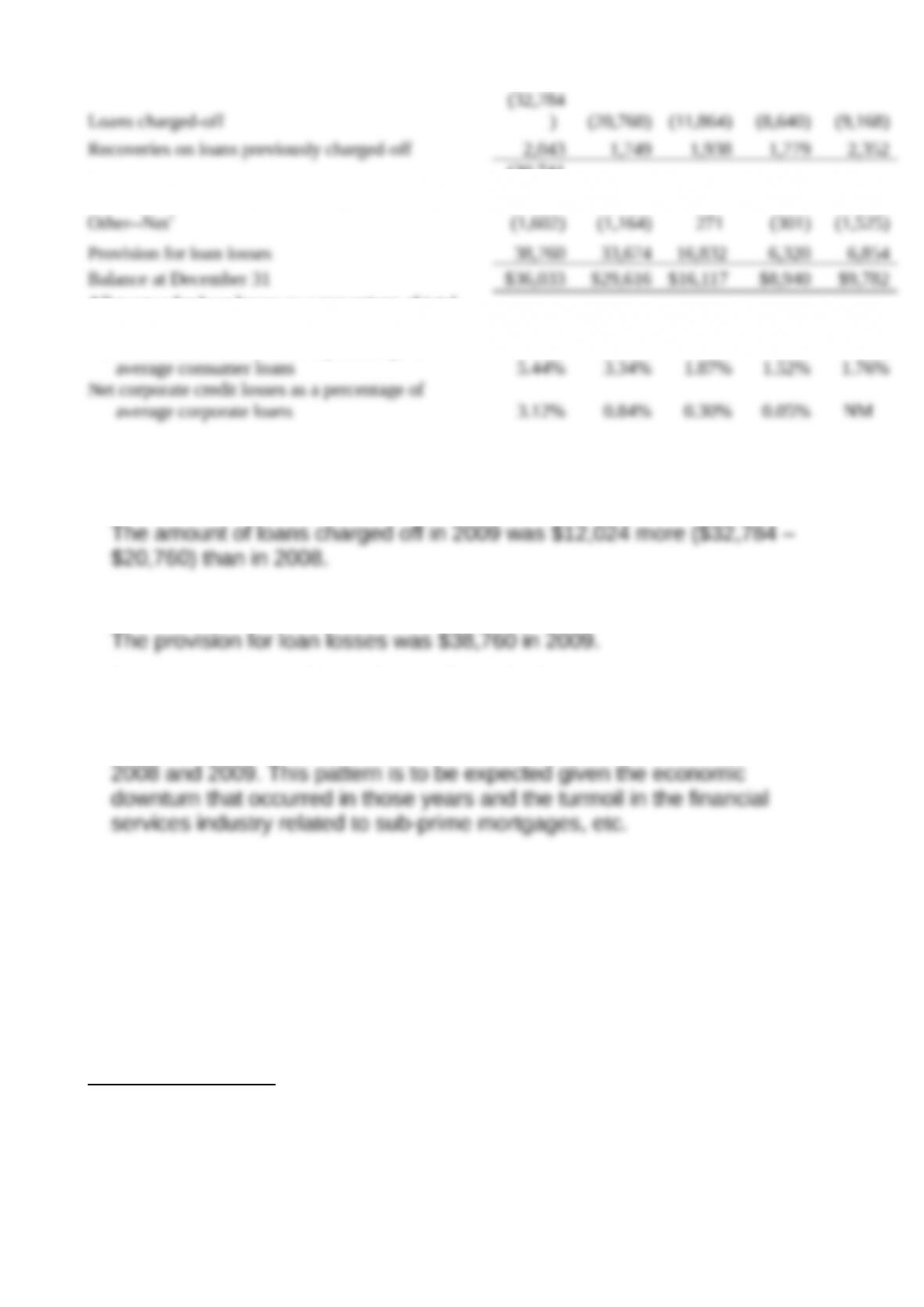

Net loans charged-off

(30,741

) (19,011) (9,926) (6,861) (6,816)

Allowance for loan losses as a percentage of total

loans 6.09% 4.27% 2.07% 1.32% 1.68%

Net consumer credit losses as a percentage of

Requirement 1.a. – Comparison of charge-offs for 2008 and 2009

Requirement 1.b. – Provision for loan losses

Requirement 1.c. – Trend in provision for loan losses to total loans

The provision as a percentage of total loans has increased substantially

since 2005 with the largest increases in the percentage occurring in

1 Other—net includes reductions to the loan loss reserve related to securitizations and the sale or

transfers to held-for-sale of various loans.

© 2018 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale

or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted

on a website, in whole or part. 8-8

Requirement 2 – Evaluation of loan performance

Based on the increases to the allowance and provision account, we

would expect that the loans on the books in 2009 are lower quality and

that defaults should be higher than in past years. Management

acknowledges that 2009 was a difficult year, but that signs of

improvement in the economy were in evidence. The company took a

number of steps in 2009 to improve its financial position and operating

2010 BUSINESS OUTLOOK

While showing signs of improvement, the macroeconomic environment going into

2010 remains challenging, with U.S. unemployment still elevated. The U.S.

government has indicated its intention to continue scaling back programs put in

place to support the market during 2008 and 2009. The impact of the U.S.

government’s exit from many of these programs is a source of uncertainty in 2010,

In addition, the potential impact of new laws and regulations (e.g., The Credit Card

Accountability Responsibility and Disclosure Act of (CARD Act)), potential new

capital standards, and other legislative and regulatory initiatives is a source of

Citigroup’s loan loss experience in 2010, and beyond, will certainly be

affected by events like those mentioned that are largely beyond their

control.

Requirement 3 – Effect of FAS 166 and FAS 167 on Citigroup

Adopting FAS 166 and FAS 167 will impact Citigroup’s regulatory capital

ratios by requiring Citigroup to include in its consolidated financial

statements certain variable interest entities and qualifying special purpose

© 2018 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale

or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted

on a website, in whole or part. 8-9

© 2018 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale

or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted

on a website, in whole or part. 8-10