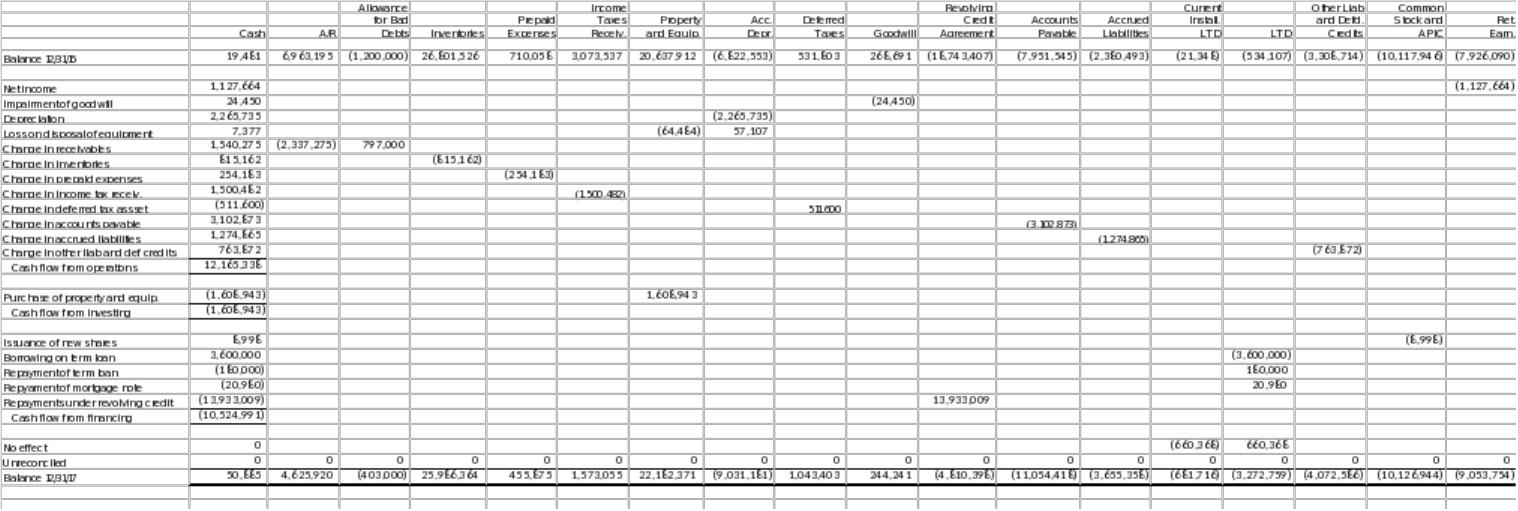

C17-3. Opus One, Inc.: Preparing and analyzing the cash flow statement

Requirement 1:

Notes:

1) Since the company did not declare or pay any cash or stock dividends

1) The T-accounts for property and equipment and accumulated depreciation

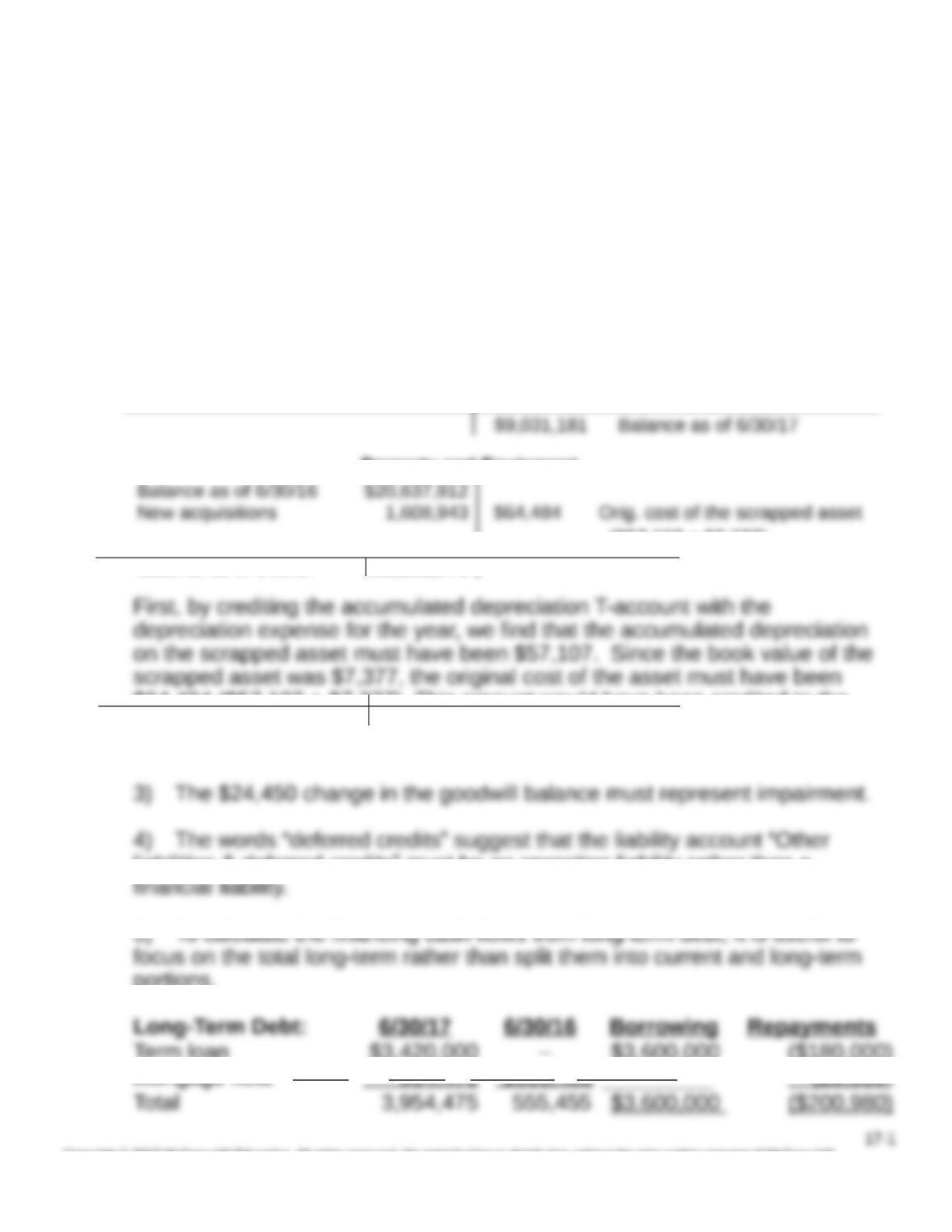

Accumulated Depreciation

$6,822,553 Balance as of 6/30/16

($57,107 + $7,377)

Balance as of 6/30/17 $22,182,371

First, by crediting the accumulated depreciation T-account with the

depreciation expense for the year, we find that the accumulated depreciation

new property and equipment acquired during the year.

4) The words “deferred credits” suggest that the liability account “Other

5) To calculate the financing cash flows from long-term debt, it is useful to

Long-Term Debt: 6/30/17 6/30/16 Borrowing Repayments

17-1

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

– Current installments (681 ,716) (21 ,348)

6) Although revolving credit agreements appear as a current liability, they are

Opus One, Inc.

Statement of Cash Flows

For the Year Ended 6/30/2017

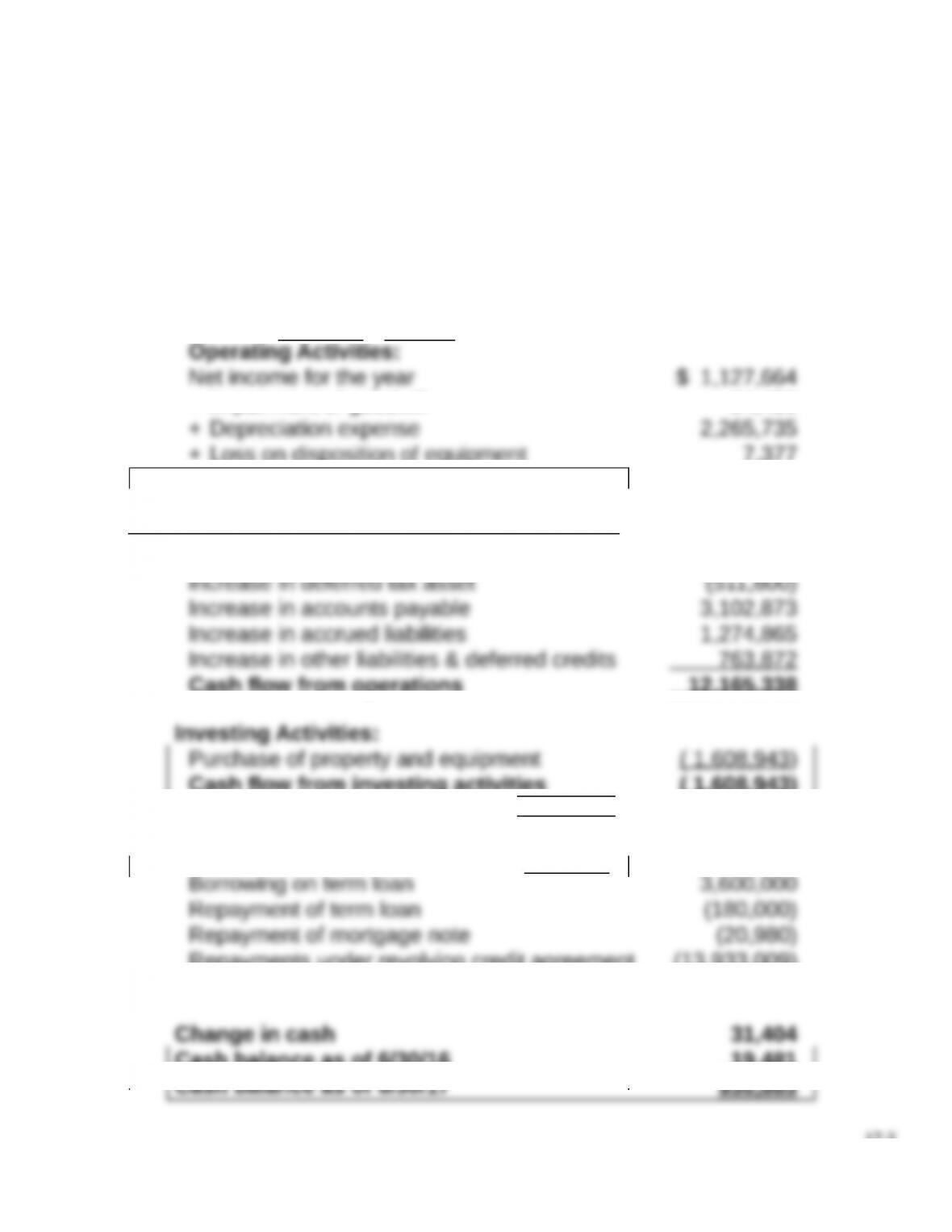

Operating Activities:

Net income for the year $ 1,127,664

Decrease in prepaid expenses 254,183

Increase in other liabilities & deferred credits 763 ,872

Cash flow from operations 12 ,165,338

Investing Activities:

Purchase of property and equipment ( 1 ,608,943)

Borrowing on term loan 3,600,000

Repayment of term loan (180,000)

Repayment of mortgage note (20,980)

Change in cash 31,404

17-2

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

17-3

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

17-4

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education.

Requirement 2:

Caveat: The analysis is limited by the information available in the problem. The

learning objective of this assignment is to enable the students to evaluate the

cash flow statement rather than perform a comprehensive analysis of the

financial performance of Opus One, Inc.

The cash flow from operations (CFO) of Opus One, Inc., is almost 11 times the

net income of the company. Given the Wall Street adage that “Cash Flow is

King and Earnings Don’t Matter,” does this mean that the financial performance

of Opus One is really 11 times better than that indicated by its net income? Let

us examine the sources of the high CFO to see whether Opus One can sustain

this level of cash flow in the future.

First of all, the company’s receivables decreased by more than $1.5 million,

meaning the company collected that much more cash than the revenue

booked in the income statement. This might be good news if the company has

improved its collection efforts. Even so, this is unlikely to happen year after

year. Consequently, this is likely to be a temporary phenomenon.

A second source of the higher cash flow is the drop in the level of inventory.

One possibility is that the drop is due to an unexpected sale at the end of the

year. However, this is unlikely since the company experienced a drop in the

receivables also; i.e, if there were unexpectedly large sales at the end of the

year, we might expect the accounts receivable to have gone up. More

importantly, inventory level provides a signal about future demand; i.e,

companies are likely to build up (decrease) inventories when they expect a

surge (fall) in demand. Therefore, another possibility is that the company saved

some cash in the current year by buying less inventory, but it might generate

less cash during the next year by selling less inventory. In any case, it is

unlikely that inventory levels can continue to decrease when companies are

growing. (In fact, in the following year, the company built up almost $10 million

of inventory which resulted in a negative CFO.) The main message here is that

neither cash flows nor accounting income by itself can tell the whole story. A

joint examination of the two is likely to be instructive.

A third factor is the increase in accounts payable by more than $3 million. More

credit from suppliers is not necessarily a bad sign; i.e, suppliers are unlikely to

extend credit when they believe their customers have impending financial

difficulties. However, an increase in accounts payable often coincides with a

buildup of inventory. Consequently, one should examine why Opus One’s

accounts payable are increasing when its inventory level is falling. One

possibility is that the company was “forced” to pay off its revolving credit under

the current agreement (see financing cash flow). This might have delayed

payments to suppliers.

17-5

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

A fourth item is the cash received from the decrease in the income tax refund

receivable. When is it likely for a company to have an asset called income tax

refund receivable? There are two possibilities. First, the company paid more

taxes during a year when compared to what it owed the IRS based on its

actual taxable income; i.e, the actual income was less than the anticipated

income. A second possibility is that the company incurred a net loss in the

recent past, and, using the loss carryback provision, the company is expecting

to receive a tax refund. Either scenario suggests that the company has

encountered difficulties in the recent past. (In fact, Opus One incurred a net

loss of almost $2.5 million during the next year.)

Similar comments can be made on other operating assets and liabilities.

The fact that the company arranged a term loan of $3.6 million is a positive

signal. First of all, the company has convinced a creditor to lend it money.

Secondly, the loan is a long-term one, and therefore, a substantial portion of

the principal payments are unlikely to be due in the near term. The company

has paid back about 5% of the term over a 4-month period. On an annual

basis, this translates into 15% of the loan; i.e, the company has the potential to

use the term loan to finance a part of its working capital needs over the next

several years.

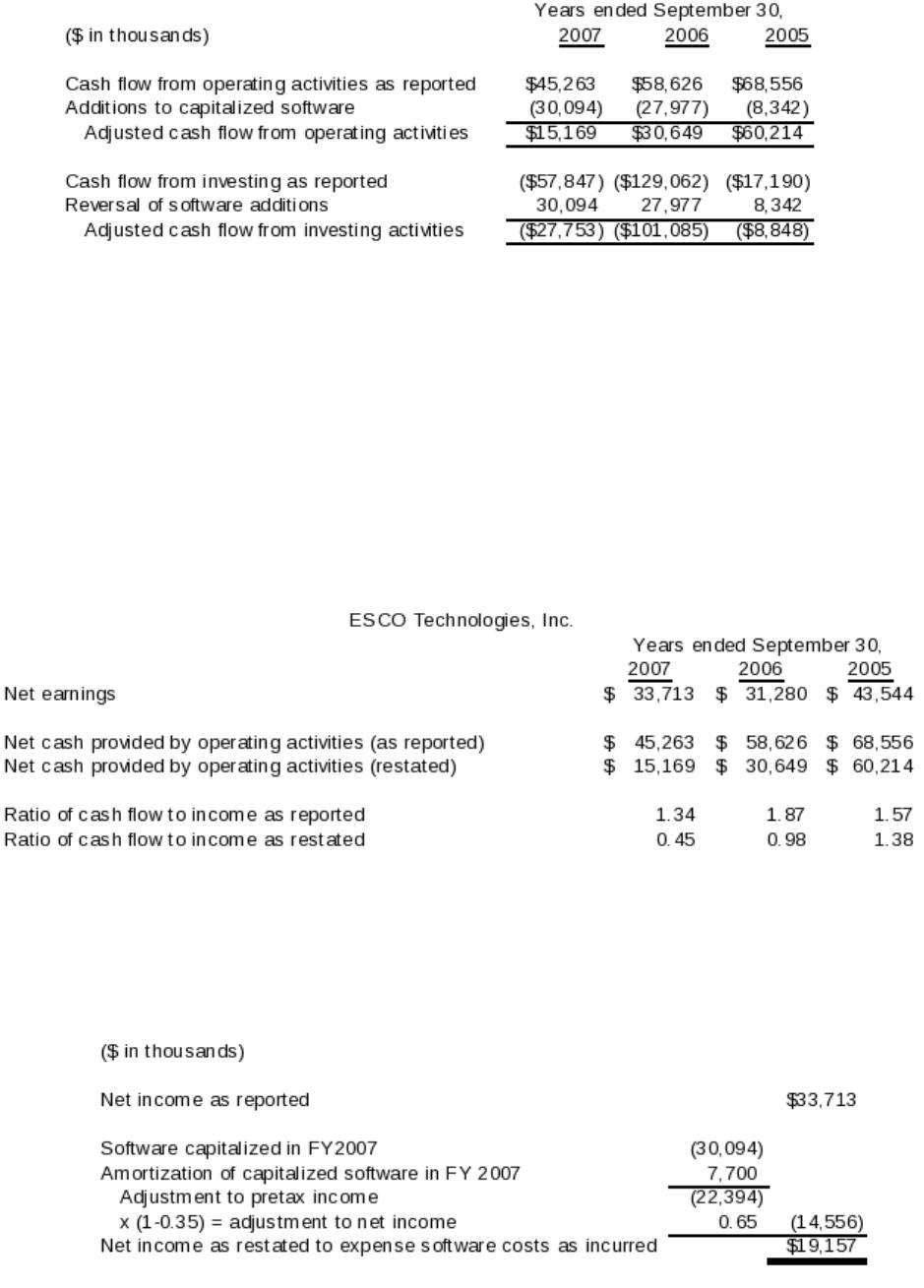

C17-4. Capitalizing software development costs

Requirement 1:

Some analysts believe that the amount of capitalized software costs should be

deducted from operating cash flows to improve inter-firm comparability and to

correct for a firm’s possible attempt to improve operating cash flows by

lowering the technological feasibility threshold in the current period relative to

prior periods. In keeping with this belief, no adjustment is needed because

Take-Two already includes capitalized software costs among its operating cash

flow items.

Requirement 2:

Some analysts believe that the amount of capitalized software costs should be

deducted from operating cash flows to improve inter-firm comparability and to

correct for a firm’s possible attempt to improve operating cash flows by

lowering the technological feasibility threshold in the current period relative to

prior periods. Thus, capitalized software costs—which originally appeared in

the investing section of ESCO’s cash flow statement—have been moved to the

operating section in the following restatement of ESCO’s cash flow statement.

17-6

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

Requirement 3:

Healthy companies generate (1) positive operating cash flows, and (2)

operating cash flows that typically exceed income due to the inclusion of

non-cash expenses (e.g., depreciation, amortization, losses on asset sales,

etc.) in income. This expected pattern appears in ESCO’s original financial

statements, but disappears when operating cash flows are adjusted to include

capitalized software costs as shown below. Note that ESCO’s seemingly

healthy cash flows (as reported) appear to be rapidly deteriorating when

restated.

Requirement 4:

ESCO’s reported income (ignoring income taxes) may be adjusted to what it

would have been if software costs were expensed as follows:

Clearly, ESCO’s software capitalization policies result in a significant increase

in reported net income, an effect that will continue as long as the company’s

17-7

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

software expenditures keep increasing each year (as they have during the

three year period ended FY2007).

Requirement 5:

Both companies appear to establish technological feasibility (the point at which

they begin to capitalize software costs) upon completion of program design

which—as Take-Two notes—tends to be early in the development cycle.

Consequently, the impact on income—at least in the short run—is to defer

considerable software development costs by capitalizing them and then

amortizing them over the life of the software instead of expensing them

immediately as research and development costs.

Note to Instructor: The best-known and oldest software development

process is the “waterfall model” where developers (roughly) follow these steps

in order:

1. state requirements

2. analyze requirements

3. design a solution approach

4. architect a software framework for that solution

5. develop code

6. test

7. deploy, and

8. Post Implementation.

After each step is finished, the process proceeds to the next step. From each

company’s software capitalization footnote, it appears that both companies

capitalize costs incurred after the completion of step 3. Companies taking a

more conservative approach could justify not declaring establishment of

“technological feasibility” until after testing is complete, thereby capitalizing few,

if any, development costs.

Requirement 6:

Software Development Costs and Licenses

Beginning balance 2007 $ 116,561 $

109,891

Amortization in 2007 per

cash flow statement

Capitalized costs during 163,859

17-8

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

2007 per cash flow

statement

Unidentified debit 5,377

Ending balance 2007 175,906

From the above account analysis, the following journal entries were made:

a. DR Software Development Costs and

Licenses

163,859

CR Cash 163,859

b. DR Amortization expense–software 109,891

CR Software Development Costs and

Licenses

109,891

The “unidentified debit” represents a discrepancy between working capital

components of net accrual adjustments on the cash flow statement and

changes in those accounts on the balance sheet. In this case, the discrepancy

is most likely due to the effects of purchases and disposals of businesses

given (1) that Take-Two reports changes in assets and liabilities net of such

effects on its cash flow statement, and (2) that Take-Two’s cash flow statement

investing section reports an outflow in 2007 related to purchases of businesses

of $5,795.

17-9

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.