Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

P15-5. Analyzing convertible debt (LO 15-9)

(AICPA adapted)

Requirement 1:

Journal entry to record the original issuance of the $10 million convertible bond

at par:

Notice that this entry does not assign any value to the conversion option.

Requirement 2:

Interest expense on the bond would be computed and recorded in the usual

4%, so interest expense would be $400,000 (or $10 million x 4%).

Requirement 3:

When issued, each $1,000 bond certificate could be converted into 5 shares of

shares x 40%). The journal entry to

DR Convertible bond payable $4,000,000

Some students may instead use the market value-method described in

Requirement 4.

Requirement 4:

The preceding entry used the “book value” method to record the conversion—

the issued stock was recorded at the book value of the debt retired. Had the

CR Additional paid-in capital 4,800,000

Notice that this entry records the stock at its market value ($90 per share) at

accounting loss when the book-value method is used.

P15-6. Cash-settled convertible debt (LO 15-9)

Part [A]: Using the bifurcation approach as required by U.S.

GAAP:

Requirement 1:

The fair value of the debt and equity components of the convertible

debt instrument would be determined by first measuring the fair

rounded to the nearest dollar.

Requirement 2:

The journal entry to record the issuance of the convertible notes

using the bifurcation approach is:

Requirement 3:

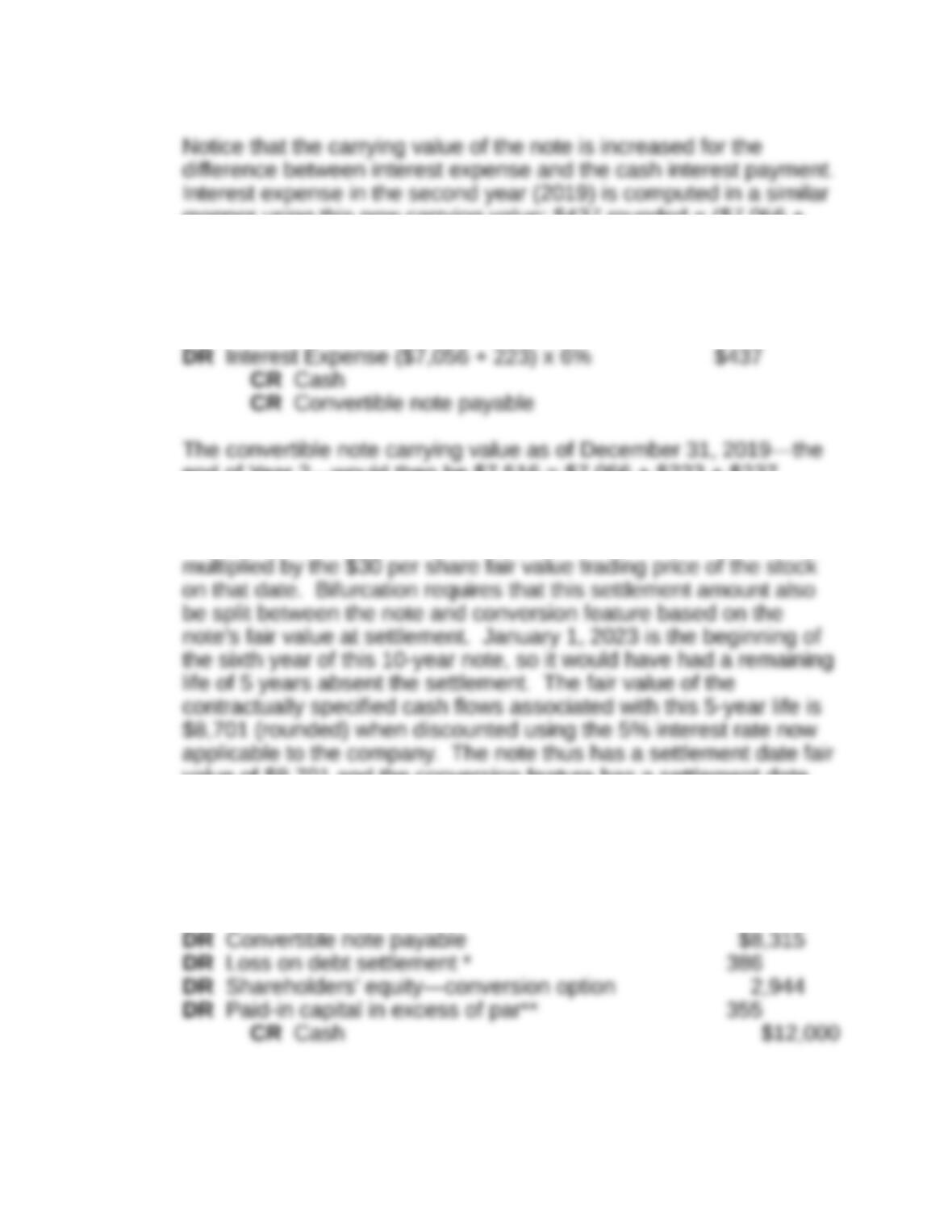

Interest expense in the first year (2018) would be computed as the

DR Interest Expense $423

manner using this new carrying value: $437 rounded = ($7,056 +

$223) X .06.

Requirement 4:

In 2019, Avnext would record interest expense with the following

journal entry:

end of Year 2—would then be $7,516 = $7,056 + $223 + $237.

Requirement 5: The cash settlement amount as of January 1,

2023 is $12,000 and represents the cash value of 400 shares

value of $8,701 and the conversion feature has a settlement date

fair value of $3,299 or $12,000 minus $8,701.

Requirement 6:

The journal entry to record the cash settlement of the notes on

January 1, 2023 is:

*The loss on debt settlement is computed as the difference between

the debt fair value on the settlement date ($8,701) and its carrying

issuance carrying value ($2,944).

Part [B]: Using the traditional approach for convertible debt

that does not have a cash settlement option:

Requirement 1:

Bifurcation would be ignored and the entire proceeds at issuance

would be assigned to the convertible note liability as:

DR Cash $10,000

Requirement 2:

Interest expense in 2018 would be computed as the debt carrying

value ($10,000) multiplied by the implied effective interest rate (2%).

Interest expense for 2019 would also be $200, or the $10,000

carrying value multiplied by the 2% interest rate.

Requirement 3:

The carrying value of the convertible note as of December 31, 2019

Requirement 4:

Absent bifurcation, the following entry would be made to record the

conversion and cash settlement of the note on January 1, 2023:

CR Cash $12,000

P15-7. Computing EPS (LO 15-6)

Requirement 1: Calculation of basic earnings per share

Basic earnings per share =

Net income- Preferred dividends

Weighted-average number of

common shares

=

$1,700,000 - $200,000

230,000*

= $6.52

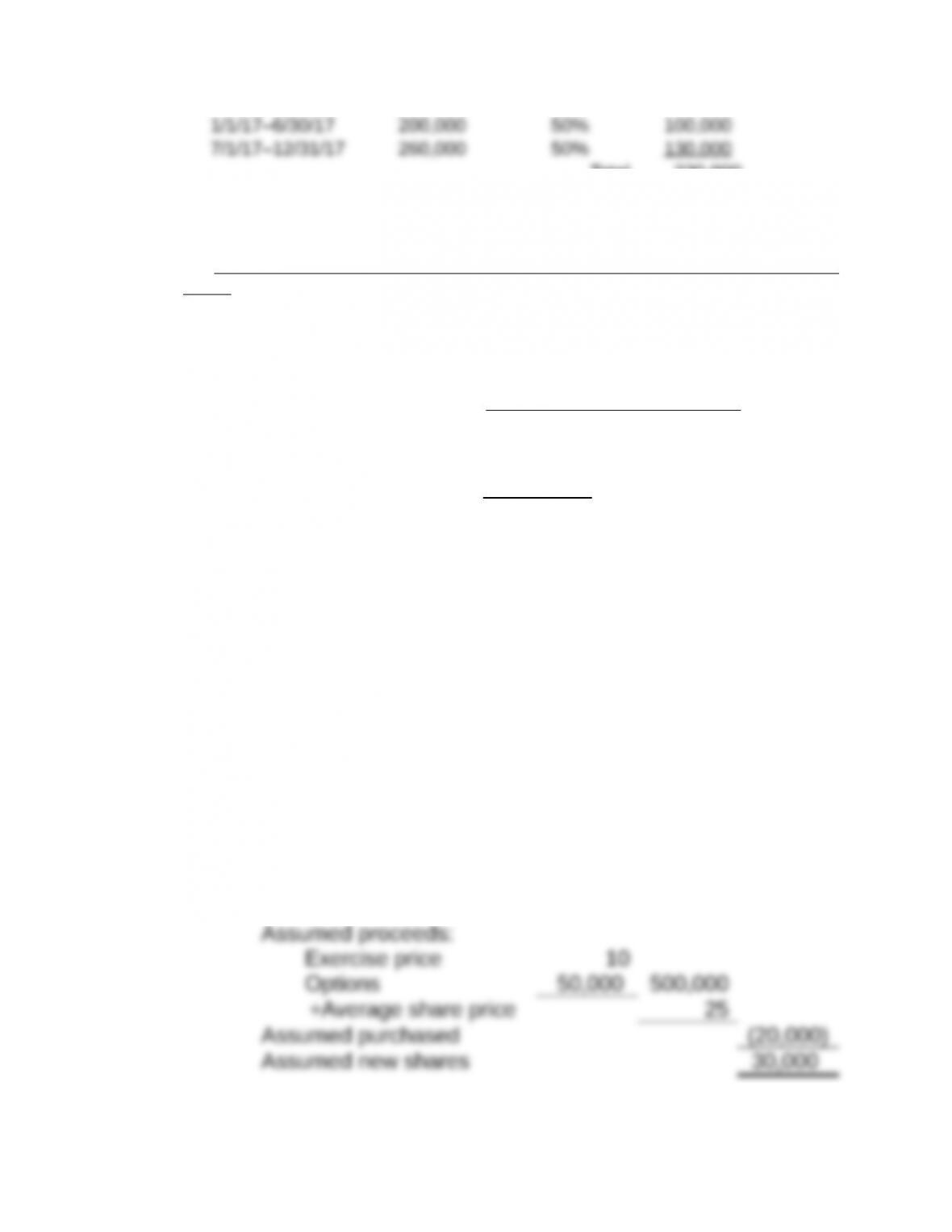

*Calculation of weighted-average number of common shares:

Shares % of the Year Weighted

Time Period Outstanding Outstanding Average

Total 230,000

Requirement 2: Calculation of diluted earnings per share

Net income - Preferred dividends + Income effect of dilutive securities

Weighted average number of common shares + Shares for dilutive

securities

=

***50,000 +**230,000

*$32,500+$200,000-$1,700,000

= $1,532,500

280,000

= $5.47

*(500,000 x 0.10) x (1.0 - 0.34) = 32,500

**From Requirement 1 above.

***(500,000/1,000) x 100 = 50,000

Requirement 3: Types of dilutive securities

Common examples are options, warrants, convertible debt, and

convertible preferred stock.

Requirement 4: Effects of options

The options would increase the denominator in requirement 2 as

follows:

Shares under option 50,000

The prior diluted EPS is adjusted as follows:

P15-8. Setting limits on dividends (LO 15-4)

Requirement 1:

Lenders restrict a subsidiary’s ability to pay dividends to the parent

corporation so that the subsidiary’s cash flows are available to

earnings (as is the case for General Chemical).

Requirement 2:

The parent company’s dividend payout ratio was just over 7.05%

Requirement 3:

At the end of the year, Tredegar Industries still had about $51,000

Requirement 4:

The year-end balance in retained earnings is $99,027 so the

Business Corporation Act does not apply.

Requirement 5:

Neither restriction seems important because the company declared

dividend.

P15-9. Repurchasing stock and calculating EPS (LO 15-1, LO 15-2)

Requirement 1:

If the stock buyback had not occurred, an additional 1,237,000

would have been:

Year Ended October 31

$ in thousands 2014 2015 2016 2017

Earnings per share as reported $0.50 $0.80 $2.50 $1.13

Earnings per share without share repurchase $0.50 $0.80 $1.92 $0.82

Requirement 2:

After adjusting for the stock repurchase, it becomes clear that

Requirement 3:

Other reasons for the decline in average common shares include

these same securities.

P15-10. Preferred stock and credit analysis (LO 15-3)

Requirement 1:

Entry to record the issuance of preferred stock on January 1, Year

2:

Year 1:

DR Dividends $240.00

CR Cash

CR Cash

$611.52

($611.52 = $7,644 x 8%)

Requirement 3:

The company would make entries identical to those in

deduction for interest.

Requirement 4:

The following schedule shows the computation of AT&T Wireless

Services’ interest coverage and long-term debt to equity ratios for

both years:

As reported 8% Debt

Year 2

Year 1

Year 2

Year 1

Interest expense on debt

$386

$85

$386

$85

Lenders might restrict a company’s ability to issue additional

debt repayment, and this might increase the company’s credit risk.

Requirement 6:

In this case, the (mandatorily redeemable) preferred stock would

P15-11. Calculating earnings per share (LO 15-6)

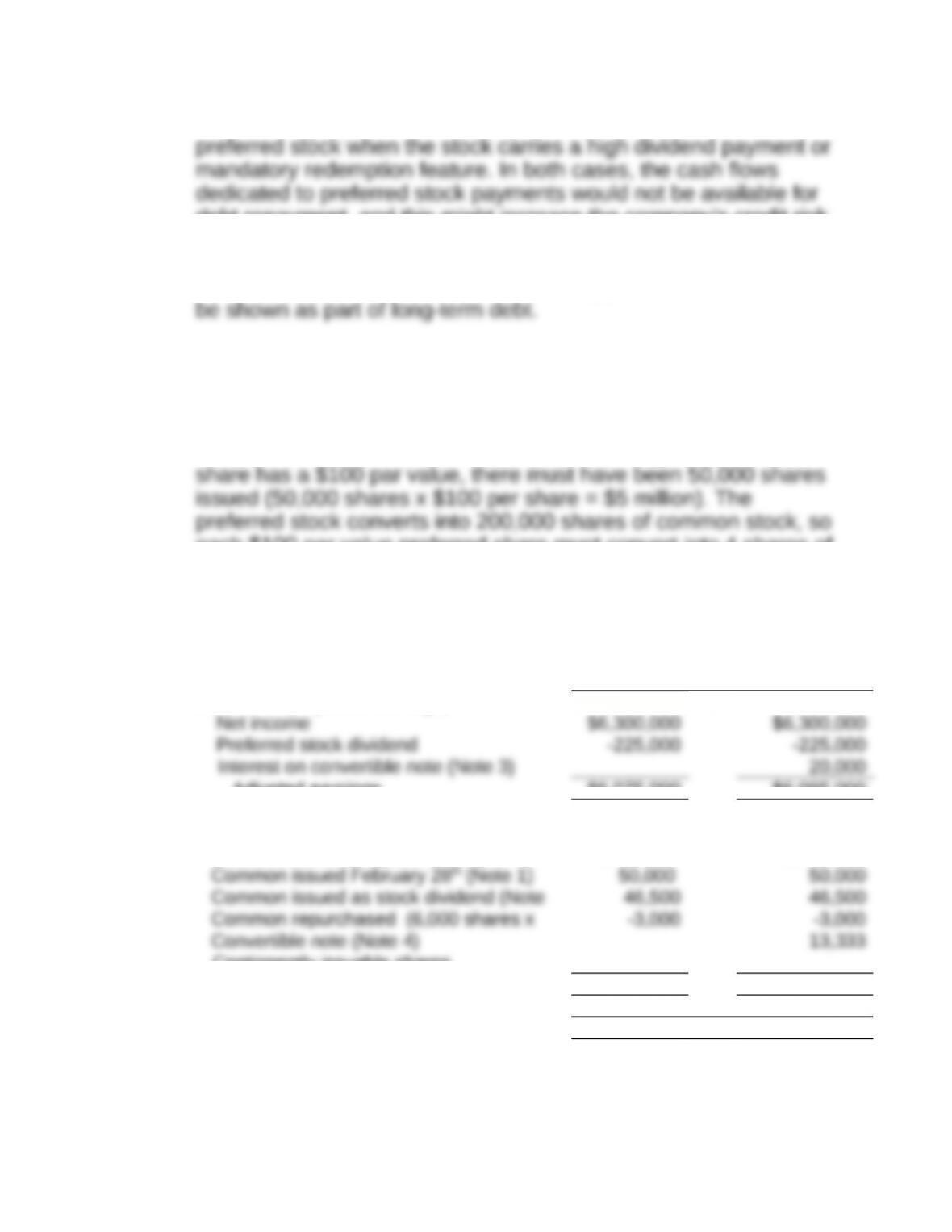

Requirement 1:

The preferred stock pays a 10% dividend ($500,000), so there

must be $5 million of preferred stock outstanding. Since each

each $100 par value preferred share must convert into 4 shares of

common.

Basic Diluted

Numerator (adjusted earnings)

Net income $6,300,000 $6,300,000

Preferred stock dividend -225,000 -225,000

Interest on convertible note (Note 3) 20,000

Adjusted earnings

$6,075,000

$6,095,000

Denominator (weighted-average shares):

Common outstanding on January 1 1,800,000 1,800,000

Contingently issuable shares

Weighted-average shares

1,893,500

1,906,833

Earnings per share

$3.21

$3.20

1. Common shares issued February 28: 60,000 shares X 10/12

(1- .40 tax rate) X 4/12 of year = $20,000 interest after-tax.

4. Common shares issued upon conversion: 40 shares X 1,000

certificates x 4/12 of year.

Contingently issuable shares (not mentioned in the chapter) are

issuable shares is 60,000 X 0/12 = 0 shares.

Contingently issuable shares are not included in the computation of

basic EPS until issued.