P13-7. Tax rate reconciliation schedules for IFRS vs. U.S. GAAP

Note: If the weighted average tax rate or effective rate is rounded before doing

Calculations relevant to both reconciliations:

Country X Country Y Total

(Tax Expense pre-tax book income)

(1) Given in problem.

(2) Sum of pre-tax book income and adjustments.

(3) Tax based on pre-tax book income:

Requirement 1:

US GAAP:

Reconciliation Note

s

Amount

s

Rate

Tax on pre-tax income

Amounts:

(1) 0.28 * pre-tax income = .28 * $2,350,000 = $658,000

(2) Tax effect depends on relevant tax rate in country where income is tax-exempt:

(3) Tax effect depends on relevant tax rate in country where expenses are not

deductible:

(4) Difference between sum of amounts (1), (2) and (3) and total income tax

expense. It can also be calculated directly as follows:

Pre-tax book income in Country Y *

(Difference in tax rates between Country Y and Country X) =

Rates: Adjustments to the statutory rate of 28% are calculated by dividing the amount

of each adjustment by pre-tax book income.

Requirement 2:

IFRS:

Reconciliation Notes Amounts Rates

Tax based on

weighted average

Amounts:

(1) See table above for calculation of total tax on pre-tax book income and

weighted-average statutory tax rate.

(2) and (3) See computations (2) and (3) under Requirement 1.

(3) See calculation of income tax expense in table above.

Rates: Adjustments to the weighted average statutory rate are calculated by

dividing the amount of each adjustment by pre-tax book income.

Note that the only difference between the two reconciliations (Requirement 1

vs. Requirement 2) is that under IFRS the reconciliation begins with the tax at

the weighted-average statutory rate ($735,000, Requirement 2), whereas under

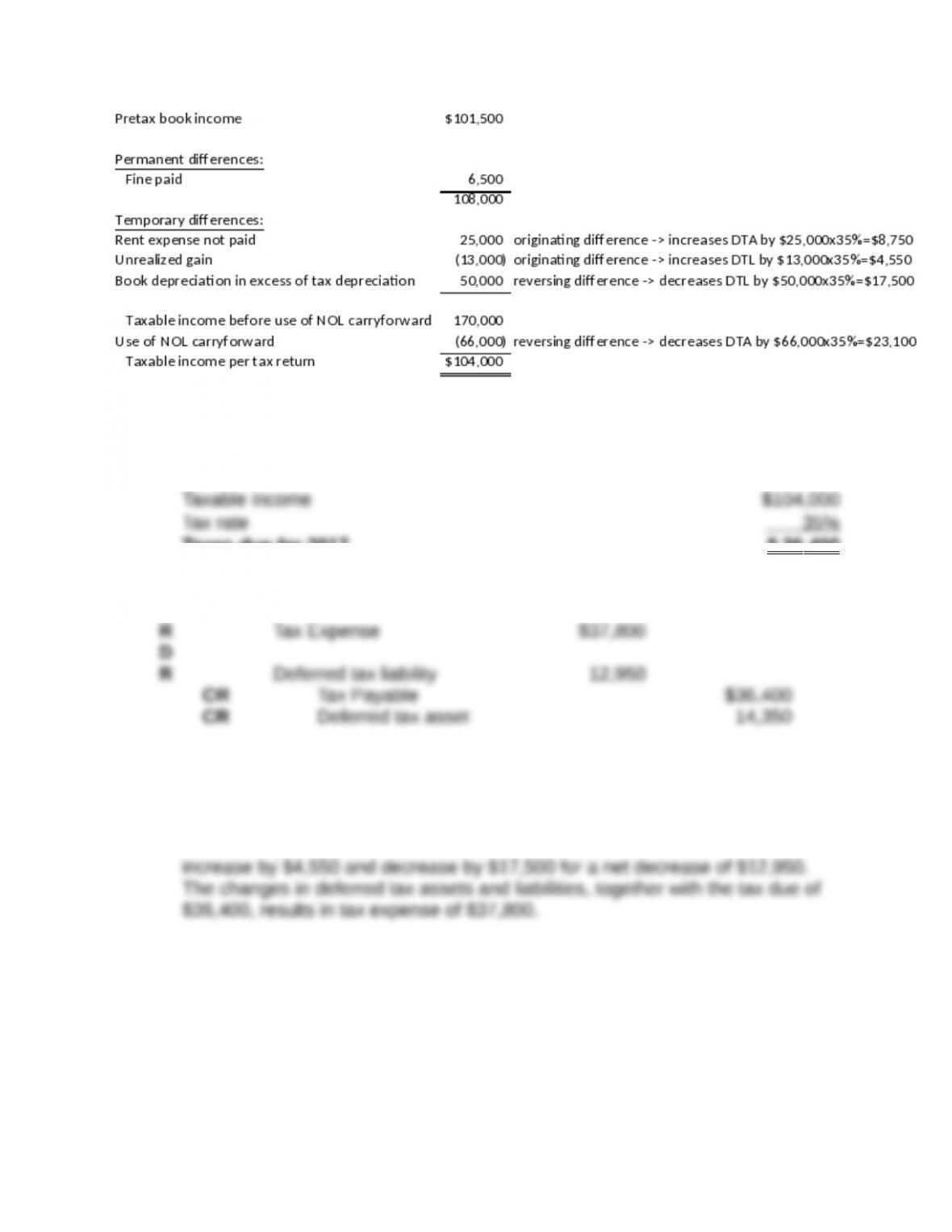

P13-8. Converting book income to taxable income and computation of taxes

due

Requirement 1:

The calculation of Madison Corporation’s taxable income for 2017 is as follows:

Requirement 2:

Taxes due for 2017 $ 36 ,400

Journal entry (not required):

D

The changes in deferred tax asset amounts are shown with each of the related

temporary differences shown in the reconciliation of pretax book income and

taxable income in Requirement 1. Deferred tax assets increase by $8,750 and

decrease by $23,100, for a net decrease of $14,350. Deferred tax liabilities

P13-9 Calculating taxes due, deferred taxes, and tax expense

Requirement 1:

Requirement 2:

Requirement 3:

Income tax expense = Taxes due + Increase in deferred tax liability –

Increase in deferred tax asset

Because the tax rate did not change and there are no permanent differences,

P13-10. Converting from taxable income to book income

Requirement 1:

Pretax book income can be determined by constructing the reconciliation

between pretax book income and taxable income. Taxable income is given

($98,000), so once the permanent and temporary differences are entered into

Requirement 2:

Temporary difference

Requirement 3:

Because there is no change in the tax rate, income tax expense can also be

P13-11. Making entries for uncertain tax positions

Requirement 1:

At the end of 2017, the recognition threshold was met (i.e., the likelihood of

sustaining the position based on its technical merits was greater than 50%).

So, Phillips recorded its tax provision assuming the position would be

sustained, but also recorded a liability to reduce the recognized benefit to the

largest amount that is cumulatively greater than 50% likely of being realized.

—————-

Requirement 2:

At the end of 2018, the recognition threshold is no longer met, so Phillips must have a

contingency reserve for the entire $350 uncertain tax benefit. There is already a $200

P13-12. Making entries for uncertain tax positions

Requirement 1:

The 2017 income tax provision and taxes payable are reduced by $1,500 x

35% = $525 to reflect the deduction of the expenditure. However, because the

probability of sustaining the uncertain tax position on its technical merits is less

than 50%, the benefit may not be recognized. The following journal entry

reverses the tax benefit of the portion of the expenditure not currently

However, the expenditure is deductible over time, so the following journal entry records the

deferred tax benefit associated with it::

Requirement 2:

Note: $35 = $100 x 35%, where $100 is the amount of annual amortization

permitted under tax law.

P13-13 Comprehensive tax allocation problem

Requirement 1:

Flower Company

Calculation of Taxable Income and Taxes Due

Computation of Taxable Income:

Adjustments for Temporary Differences:

3For tax purposes, one-half of the cash has been collected, therefore one-half

of the profit is recognized. The remaining profit will be recognized in 2018 when

the cash is collected.

Requirement 2:

Computation of change in deferred tax asset and deferred tax liability accounts:

Deferred Deferred

Temporary Difference Tax Asset Tax

Liability

Depreciation

Rent income recognized in income

statement in 2017, taxed in 2018,

Tax benefit of loss carryforward used,

Requirement 3:

Determination of tax expense for 2017:

Tax expense = Taxes due + Increase in deferred tax liability +

Decrease in deferred tax asset

Because the tax rate does not change, tax expense can also be computed as

P13-14. Determining taxes due, deferred taxes, and tax expense

Requirement 1:

Reality Corp.

Calculation of Taxable Income and Taxes Due

Computation of Taxable Income:

Adjustments for temporary differences:

Excess of tax depreciation over book depreciation

($225,000 – $100,000)

Excess of equity in investee earnings over dividends

Received, less portion considered permanent due to

80% dividend exclusion rule [20% x ($80,000 – $30,000)]

Taxable income before use of operating loss carryforward

29,000

Operating loss carryforward used

(10,000)

Taxable income

Taxes due

$6,650

Requirement 2:

Computation of change in deferred tax asset and deferred tax liability

accounts

Deferred Tax

Deferred Tax

Temporary Difference Asset Liability

$54,250 CR

Requirement 3: Determination of Tax Expense for 2017

Tax Expense = Taxes Due + Increase in Deferred Tax Liability – Increase in

Deferred Tax Asset (including effect of increase in valuation

= $56,700

*Increase in valuation allowance:

Because the tax rate did not change, income tax expense is also equal to