Financial Reporting and Analysis (7th Edition)

Chapter 3 Solutions

Revenue Recognition

Exercises

Note: Exercises E3-1 through E3-4 deal with when a contract subject to the

revenue recognition rules exists. In order for a contract to exist that is subject to

ASC Topic 606, the following conditions must all have been met:

All parties to the contract have approved the contract and are legally

obligated to perform their obligations under the contract.

Payment terms can be identified, although consideration may include a

variable component.

Collection is probable. Assessment of collectibility “is based on whether the

E3-1. Existence of a contract

Note: See the beginning of this chapter’s solutions for the criteria for existence of a

contract.

In scenario 1, no legally binding contract has been entered into as of the end of the

year. Even though the customer usually places an order by the end of the

In scenario 2, again there is no contract until the order is received by fax. It is

In scenario 3, there is a contract upon receipt of the order by phone. This situation

creates an oral contract, which is legally binding on the two parties. The fact

In situation 4, there is a contract when Amiel and the customer agree. The price

need not be certain in order for there to be a contract subject to the revenue

E3-2. Existence of a contract

Note: See the beginning of this chapter’s solutions for the criteria for existence of a

contract.

There is no contract subject to the revenue recognition rules until Latter receives

payment for two reasons. First, Latter has specifically stated that it will not ship

the goods until a cashier’s check is received, indicating that Latter has not

E3-3. Existence of a contract

Note: See the beginning of this chapter’s solutions for the criteria for existence of a

contract.

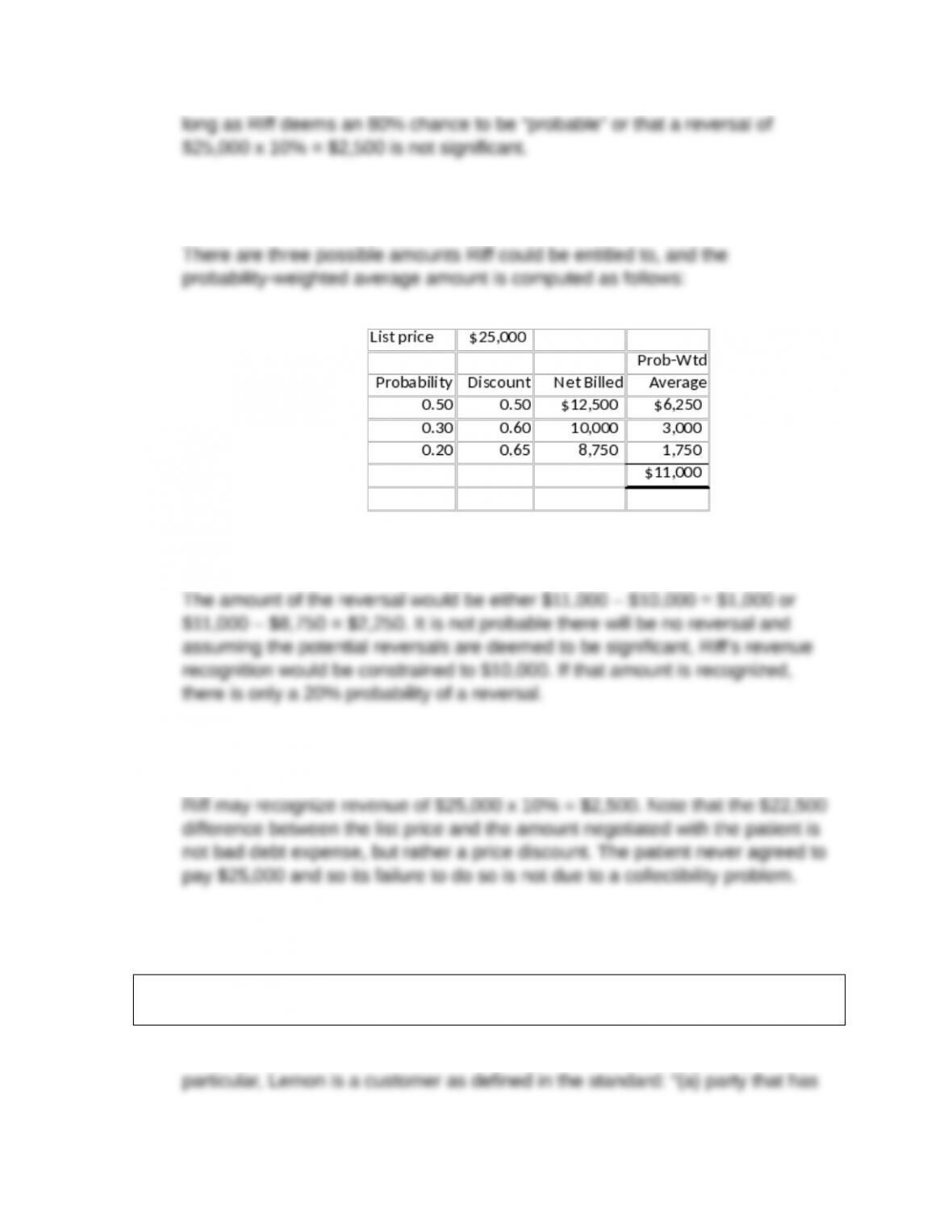

In scenario 1, once it is determined the patient is insured with one of Riff’s preferred

In scenario 2, Riff may recognize revenue when it determines the patient is insured.

In scenario 3, Riff may recognize revenue when it determines the patient is insured.

So, Riff may recognize $11,000 of revenue, subject to the constraint that it must be

probable that a significant reversal will not be necessary. If that amount of

revenue is recognized, there is a 50% chance that a reversal will be required.

In scenario 4, Riff may recognize revenue once it comes to a financial agreement

with the patient. Until that time, Riff cannot assert that the other party to the

transaction intends to perform its obligations. Once the agreement is reached,

E3-4. Existence of a contract

Note: See the beginning of this chapter’s solutions for the criteria for existence of a

contract.

In scenario 1, Lemon has a contract with Morley that is subject to ASC Topic 606. In

Note the contrast in scenario 2. In this scenario, Lemon and Morley have formed a

joint venture because they have agreed that each will supply certain resources

E3-5. Principal vs. agent

The following are indicators that a firm is an agent, not a principal, to the transaction:

Another party has primary responsibility for fulfilling the contract terms.

The firm does not bear any inventory risk.

In scenario 1, Van Allen is an agent. In addition to being compensated through

commission, it is likely (because Van Allen is a broker) that it is not responsible

In scenario 2, Van Allen is again an agent. It is still compensated via commission

In scenario 3, Van Allen is a principal. Van Allen controls pricing and bears inventory

E3-6. Deposits

Requirement 1:

At this point, there is no contract subject to ASC Topic 606 and no revenue may be

recognized, so Pogrund records a Customer deposit:

Requirement 2:

At this point, there is a contract subject to ASC Topic 606, but Pogrund has not yet

transferred any goods or services to the customer, so it may not recognize any

revenue. The additional deposit increases the Customer deposit liability.

Requirement 3:

The contract has been terminated and Pogrund is entitled to retain the deposit with

no further obligations to David. It may now recognize revenue:

E3-7. Warranties

Requirement 1:

The standard warranty is not a separate performance obligation because it clearly is

intended to assure the equipment was defect free at the time of sale. So,

Kruger recognizes revenue in the amount of the sale.

In addition to recording cost of goods sold (DR Cost of goods sold; CR Inventory),

Kruger recognizes Warranty expense in the same period as Sales revenue:

Requirement 2:

The extended warranty is a separate performance obligation because it provides

goods and services beyond assuring the equipment is defect free at the time of

the sale. The total consideration must be allocated to the two performance

obligations. The revenue related to the sale of the equipment is recognized

Given that the equipment and the extended warranty have standalone prices of

$50,000 and $3,000, respectively, and assuming the total consideration

Again Kruger records cost of goods sold (DR Cost of goods sold; CR Inventory) and

also Warranty expense for the standard warranty.

E3-8. Contract modification

From the facts given, it is clear that the second transaction was negotiated

separately from the first and therefore the increment to the contract price

E3-9. Contract modification

From the facts given, the additional goods are distinct, but the increment to the

transaction price is not commensurate with the standalone price of the

additional goods. Therefore, the original contact is considered cancelled and

E3-10. Volume discount and variable consideration

A volume discount creates variable consideration when there is uncertainty about

the likelihood the volume discount will be taken. Revenue should be recognized

Requirement 1:

At the end of the first quarter, Glick assesses the likelihood Newman will reach the

volume discount threshold. The assessment is that Newman is very unlikely to

reach that threshold. So, the most likely outcome is that ultimately Glick will be

Requirement 2:

At the end of the second quarter, Glick reassesses the likelihood Newman will reach

the volume discount threshold. The new assessment is that Newman is very

likely to reach that threshold. So, the most likely outcome is that ultimately Glick

will be entitled to collect (from sales to Newman to date) (1,200 + 4,500) x $30

x 90% = $153,900 from Newman. Glick records $153,900 – $36,000 =

E3-11. Revenue recognition at a point in time or over time

In scenario 1, revenue recognition should be over time. The service is transferred to

In scenario 2, Kleymenova is creating an asset that has no alternative use and has

In scenario 3, the consulting work improves or enhances the collection system,

In scenario 4, none of the three criteria that result in revenue recognition over time

are met. The client does not receive and consume the services over time. The

client does not control an asset that is being improved. The asset Kleymenova

E3-12. Allocation of transaction price and revenue recognition

Gerakos allocates 2/3 ($60,000/$90,000) of the $80,000 transaction price, or

$53,333, to the software and 1/3 ($30,000/$90,000) of the $80,000 transaction

price, or $26,667 to the technical support. All the revenue allocated to the

So, total revenue in 2019 is $53,333 + ($26,667 x 1/3) = $62,222. Revenue in 2020

E3-13. Allocation of transaction price and revenue recognition

Gerakos allocates $60,000 of the $80,000 transaction price to the software and the

residual of $20,000 to the technical support. All the revenue allocated to the

software is recognized when it is sold, which is in 2019. The revenue allocated

So, total revenue in 2019 is $60,000 + ($20,000 x 1/3) = $66,667. Revenue in 2020

E3-14. Allocation of transaction price and revenue recognition

Gerakos allocates $30,000 of the $80,000 transaction price to the technical support

and the residual of $50,000 to the software. All the revenue allocated to the

So, total revenue in 2019 is $50,000 + (30,000 x 1/3) = $60,000. Revenue in 2020 is

E3-15. Allocation of transaction price and revenue recognition

Requirement 1:

First Ginzel must assess whether there the data extraction is a distinct performance

obligation. To be distinct, goods or services must be of benefit to the customer

separately. The data extraction is not separately beneficial. The purpose of

Therefore, there is a single performance obligation consisting of the marketing

reports, and the performance obligation is satisfied over time as each report is

delivered. Therefore, the $110,000 transaction price is all associated with the

Requirement 2:

Costs to fulfill a contract should be capitalized and then recognized in the income

statement in a pattern that is consistent with the pattern in which revenue is

E3-16. Determining liability for unperformed obligation under ASC Topic 606

As of December 31, 2019, Jerry’s has a liability for unperformed obligations for the

E3-17. Determining liability for unperformed obligation under ASC Topic 606

Initially, Regal records a $250,000 liability for the gift certificates. It expects $250,000

x 10% + $25,000 of breakage, which may be recognized as revenue in

proportion to the redemption of the gift certificates. As of December 31, 2019,

The entries for the gift certificate activity for the year are:

The liability reported in the December 31, 2019 balance sheet is $250,000 –

$200,000 – $22,222 = $27,778.

E3-18. Determining when to recognize revenue

Requirement 1:

Bullseye entered into a contract calling for the sale of 250,000 gallons of fuel. There

is one performance obligation, but the obligation is being satisfied over time

Note also that it would be equivalent for Bullseye to treat each gallon as one of

250,000 separate performance obligations (or, for that matter, each half gallon

Requirement 2:

Bullseye recognizes revenue over time, with the proportion of fuel transferred as the

best measure of the extent to which the customer has benefited. The

E3-19. Breakage

For each $105 club purchase, Cassidy has 5 possible oil changes that may be

redeemed. Each is a performance obligation, and the transaction price is

allocated in proportion to the standalone values of the performance obligations.

Cassidy may also recognize breakage revenue and reduce its liability in proportion

to the actual redemptions. For each club purchase, Cassidy expects 4.5 of the

Therefore, with each oil change, Cassidy recognizes revenue of $21 + $2.33 =

$23.33.

Suppose, for example, Cassidy sells 100 club memberships and, as expected, 450

of the 500 possible oil changes are redeemed. Cassidy receives cash of $105 x