P15-12. Calculating EPS when the capital structure is complex (LO

15-6)

Requirement 1:

The preferred stock pays a 10% dividend ($500,000), so there

must be $5 million of preferred stock outstanding. Since each

each $100 par value preferred share must convert into 4 shares of

common.

Requirement 2:

The after-tax interest on the Series B debt was $300,000. Since

this equals gross interest divided by one minus the 40% tax rate,

convert into 40 common shares (200,000 shares/5,000

certificates).

Requirement 3:

The after-tax interest on the $5 million of Series A debt was

common stock at 50 shares per certificate.

Requirement 4:

Under the treasury stock method, the proceeds received from

exercising stock options are used to buy back shares on the open

share ($1 million/16,666 shares).

Requirement 5:

One reason Series A debt carries a lower interest rate (8%) than

certificates.

P15-13. Analyzing shareholders’ equity (LO 15-1, LO 15-5)

(AICPA adapted)

Requirement 1: Statement of retained earnings

Trask Corp.

Statement of Retained Earnings

For the Year Ended December 31, 2017

Balance, December 31, 2016, as originally reported

Net Income 2,400,000

Balance, December 31, 2017

$17,400,000

Requirement 2: Shareholder’ equity section

Trask Corp.

Shareholders’ Equity Section of Balance Sheet

December 31, 2017

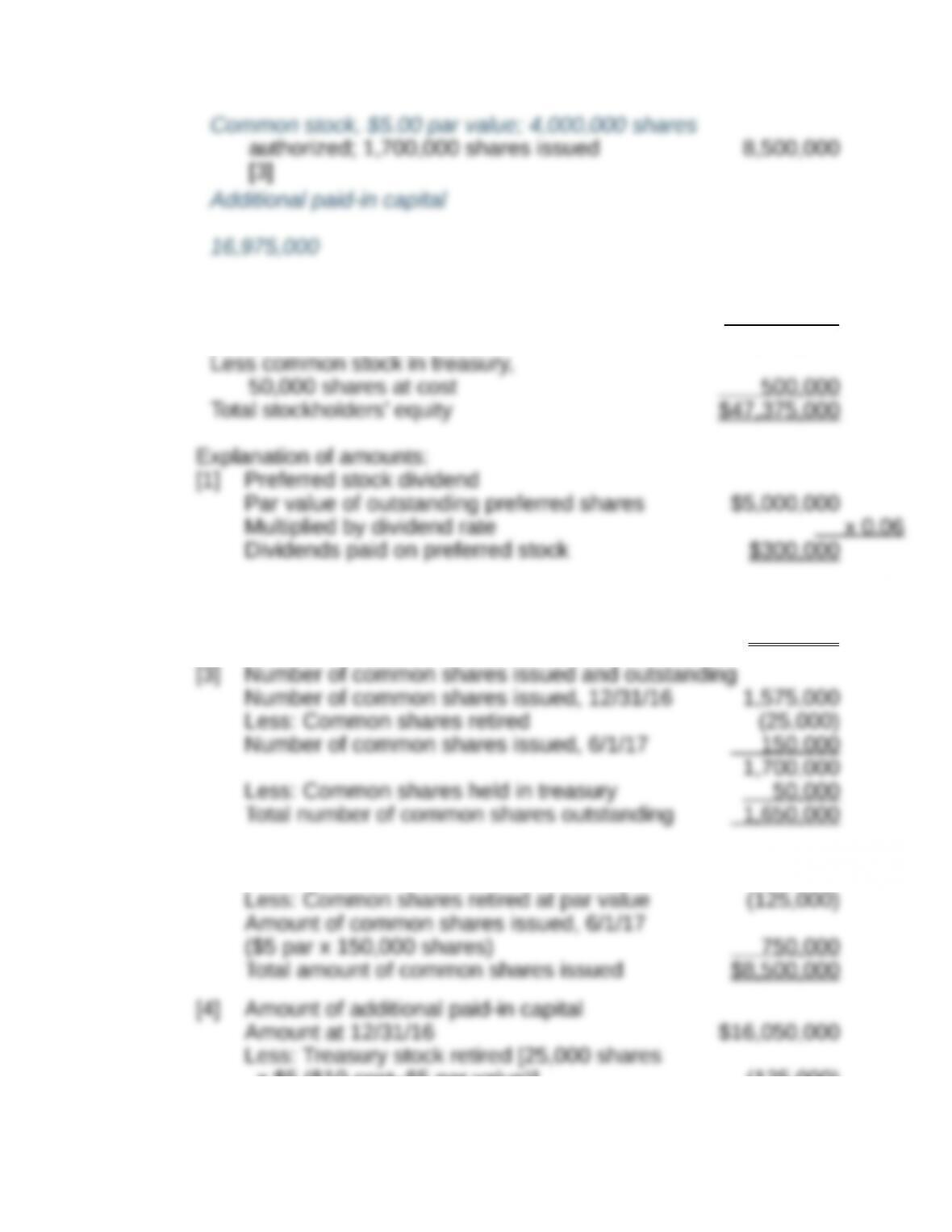

Preferred stock, $100 par value, 6% cumulative;

[4]

Retained earnings 17 ,400,000

47,875,000

[2] Property dividend issued

Fair value of Harbor stock distributed

(15,000 shares @ $60) $900 ,000

Amount of common shares issued

Amount of common shares issued, 12/31/16 $7,875,000

x $5 ($10 cost–$5 par value)] (125,000)

Amount received upon issuance of common

Total amount of additional paid-in capital $16 ,975,000

*Additional paid-in capital includes $300,000 related to stock

paid-in capital, but this transfer does not affect the net amount of

Additional paid-in capital.

Requirement 3: Computation of book value per share

Total stockholders’ equity $47,375,000

$25.68

P15-14. Stockholders’ equity (LO 15-1, LO 15-3, LO 15-5)

Part A:

Requirement 1:

There are 300,000 shares of preferred stock outstanding. The par

Requirement 2:

The journal entry to record the sale of 10,000 shares of preferred

CR Additional paid-in capital

240,000

Requirement 3:

The journal entry to record the $0.10 annual dividend on the

$1,000

Requirement 4:

There were 98.1 million shares of Class A common shares

Requirement 5:

“Authorized” shares is the upper limit on the number of shares that

can be sold (issued) and is set by the company’s board of

company, they are “treasury” shares.

Requirement 6:

Some companies issue two classes of stock to separate voting

Requirement 7:

According to the cash flow statement, new shares were issued

Part B:

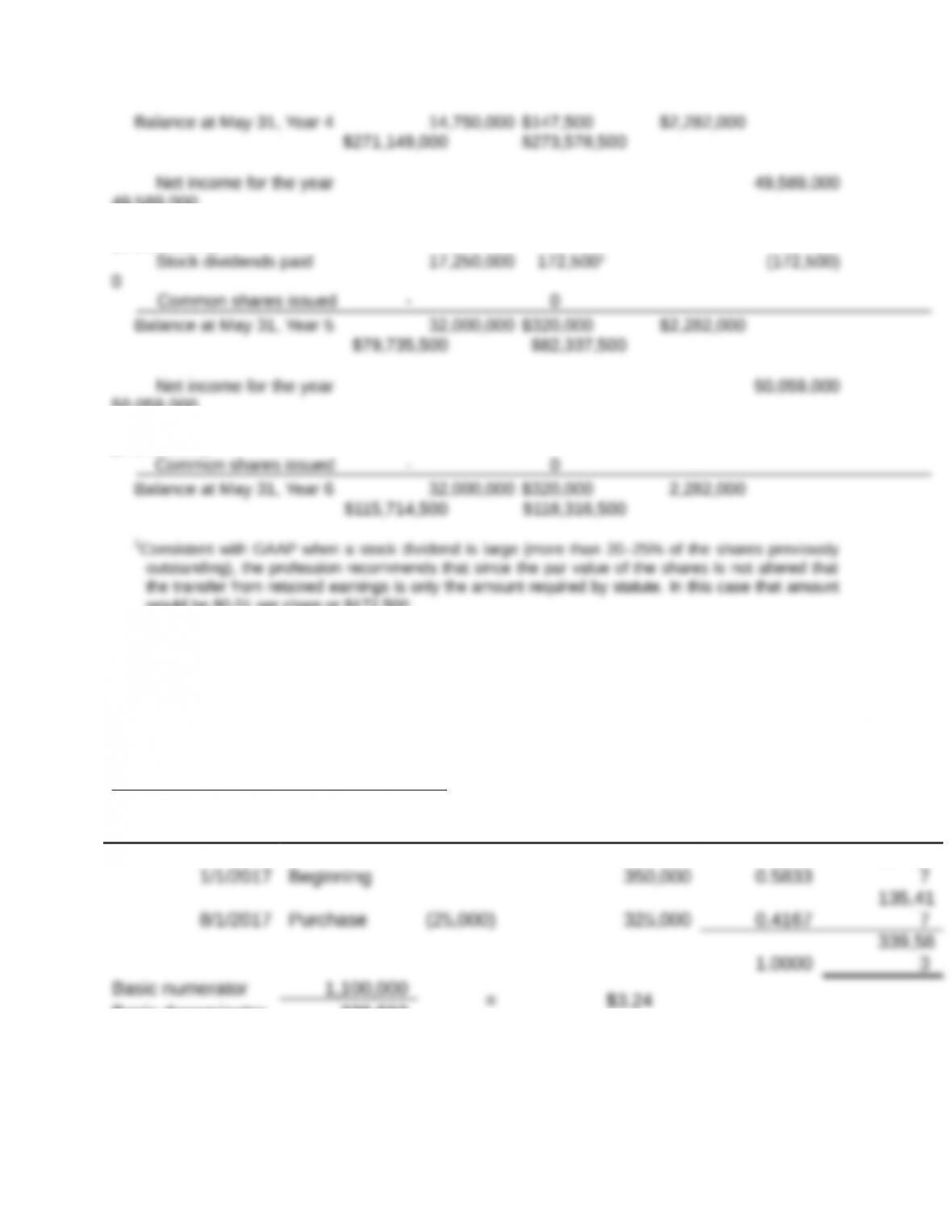

The schedule below shows the calculations.

Common Common Additional Total

Shares Stock $0.01 Paid-In Retained

Stockholders’

Issued Par Value Capital Earnings

Equity

Balance at May 31, Year 3: 14,750,000 $147,500 $2,282,000

49,589,000

Dividends paid (240,830,000)

(240,830,000)

50,059,000

Dividends paid (14,080,000)

(14,080,000)

would be $0.01 per share or $172,500.

P15-15. Computing basic and diluted EPS (LO 15-6)

Requirement 1. Basic EPS

Weighted average of outstanding shares

Portion

Date Transaction Change Outstanding of Year Weighted

204,16

Basic denominator 339,583

Requirement 2. Diluted

339,5

P15-16. Computing basic and diluted EPS (LO 15-6)

Requirement 1: Basic EPS

Weighted average of outstanding shares

Portion

Date Transaction Change O/S of Year Weighted

1/1/2017 Beginning 257,000 0.75 192,750

(32,000

Requirement 2: Diluted EPS

Basic Interest

825,000

65,00

0a =

890,00

0

249,000

30,00

0a

77,500b

356,50

0

Basic Bonds Options

= 2.50

aBonds

Numerator

bOptions

Outstanding

125,00

0

Additional shares

77,50

0

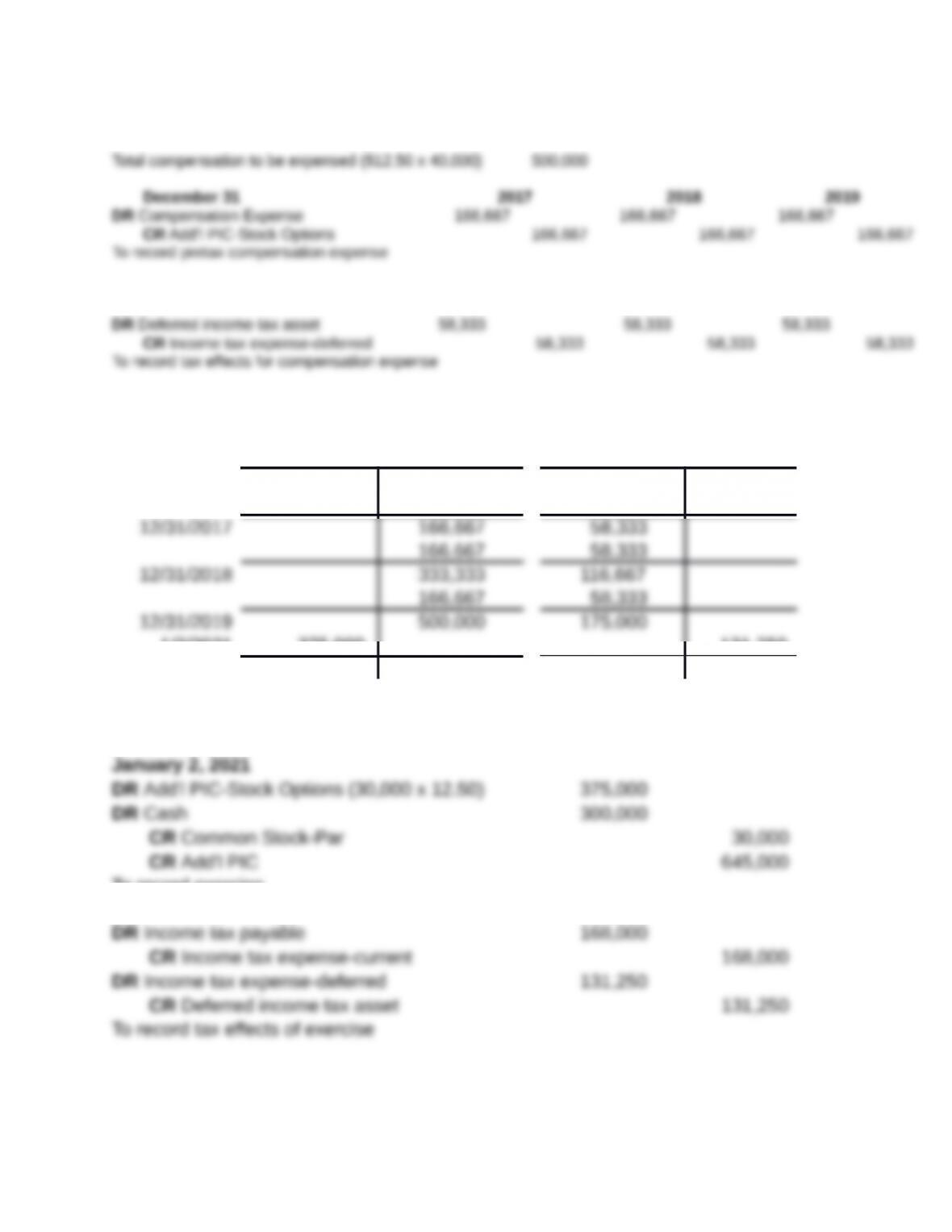

P15-17. Stock option accounting (LO 15-7, LO 15-8)

Requirement 1 – Pretax journal entries

To record annual expense

July 1, 2019

DR Add’l paid-in capital – options 1,600,000

Requirement 2 – Tax journal entries

31-Dec 2017 2018

DR DIT Asset (0.35 x 800,000) 280,000 280,000

DR Income tax expense – deferred

560,000

CR DIT Asset 560,000

Permanent difference ,500,000) 35% (525,000)

Requirement 3: Effect on income tax expense and effective tax rate

Income tax expense-deferred 560,000

(1,085,000

As shown above, the exercise will reduce income tax expense, which will reduce the

Darth’s effective tax rate below the 35% statutory rate.

Requirement 4: Presentation in statement of cash flows

P15-18. Stock option accounting (LO 15-7, LO 15-8)

Requirement 1 – Journal entries from 2017 to 2019

Tax rate 35%

Requirement 2 – Journal entries at exercise

Additional PIC – Options DIT Asset

166,667 58,333

1/2/2021 375,000 131,250

1/2/2021 125,000 43,750

Intrinsic value at 1/2/2021 [30,000 x ($26-$10)] 480,000

To record exercise

Pretax Tax rate Tax savings

GAAP Compensation 375,000 35% 131,250 DIT asset

Requirement 3 – Journal entries at exercise

Income tax expense-deferred 131,250

the reduction in income tax expense will reduce the effective rate below the 35% statutory

rate.