Financial Reporting and Analysis (7th Ed.)

Chapter 12 Solutions

Financial Reporting for Leases

Exercises

Exercises

E12-1. Accounting for lessee with purchase option under ASC 840 (LO

12-3)

Requirement 1: Amount capitalized by Leland at 07/01/2017

The $100,000 represents a bargain purchase as the amount is

significantly below the expected residual value of $600,000. Given

that the lease contains a bargain purchase option, it meets criterion

Requirement 2: Lease obligation amortization table

Part 2 – Amortization table

Interest Principal

Date Expense Payment Reduction Balance

7/1/17 $ 1,849,591

*Rounded

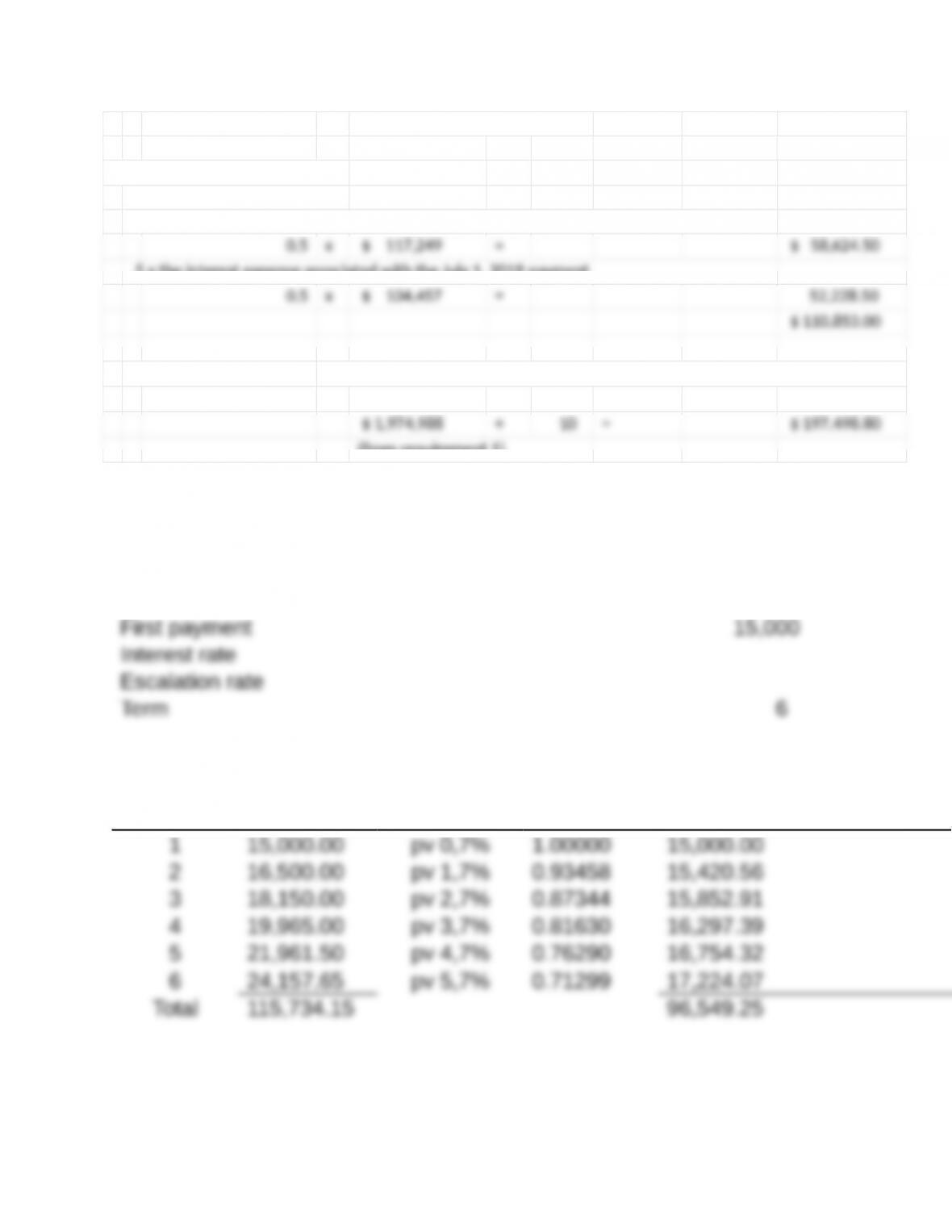

Requirement 3: Depreciation and interest expense

December 31, 2017

Interest expense: .5 x the interest expense associated with the June 30, 2018 payment

December 31, 2018

Interest expense:

.5 x the interest expense associated with the June 30, 2018 payment

Requirement 4: Do requirements 1 to 3 for payments in

advance

Requirement 4.1: Amount capitalized by Leland at 07/01/2017

The $100,000 represents a bargain purchase as the amount is

significantly below the expected residual value of $600,000. Given

that the lease contains a bargain purchase option, it meets criterion

2 and is classified as a capital lease. The amount to be capitalized

Requirement 4.2: Lease obligation amortization table

Part 2 – Amortization table

Interest Principal

Date Expense Payment Reduction Balance

*Rounded

Note that all of the first payment on July 1, 2017 goes for principal

reduction because no interest has accrued at July 1. Also, note that the

obligation balance increases instead of decreases from July 1, 2021 to

Requirement 4.3: Depreciation and interest expense

December 31, 2017

Interest expense: .5 x the interest expense associated with the July 1, 2018 payment

depreciation expense: .5 x the capitalized amount divided by the economic life (because criterion 2 is

met)

(from requirement 1)

December 31, 2018

Interest expense:

.5 x the interest expense associated with the July 1, 2018 payment

.5 x the interest expense associated with the July 1, 2019 payment

depreciation expense: Capitalized amount divided by the economic life of 10 years

(from requirement 1)

E12-2. Accounting for lessee with uneven, beginning of period lease

payments under ASU 2016-02 (LO 12-1, LO 12-6)

Requirement 1 – Journal entry at 1/1

Present value of each payment at 1/1

Payment Payment

PV

assumption

7% PV

factor Present Value

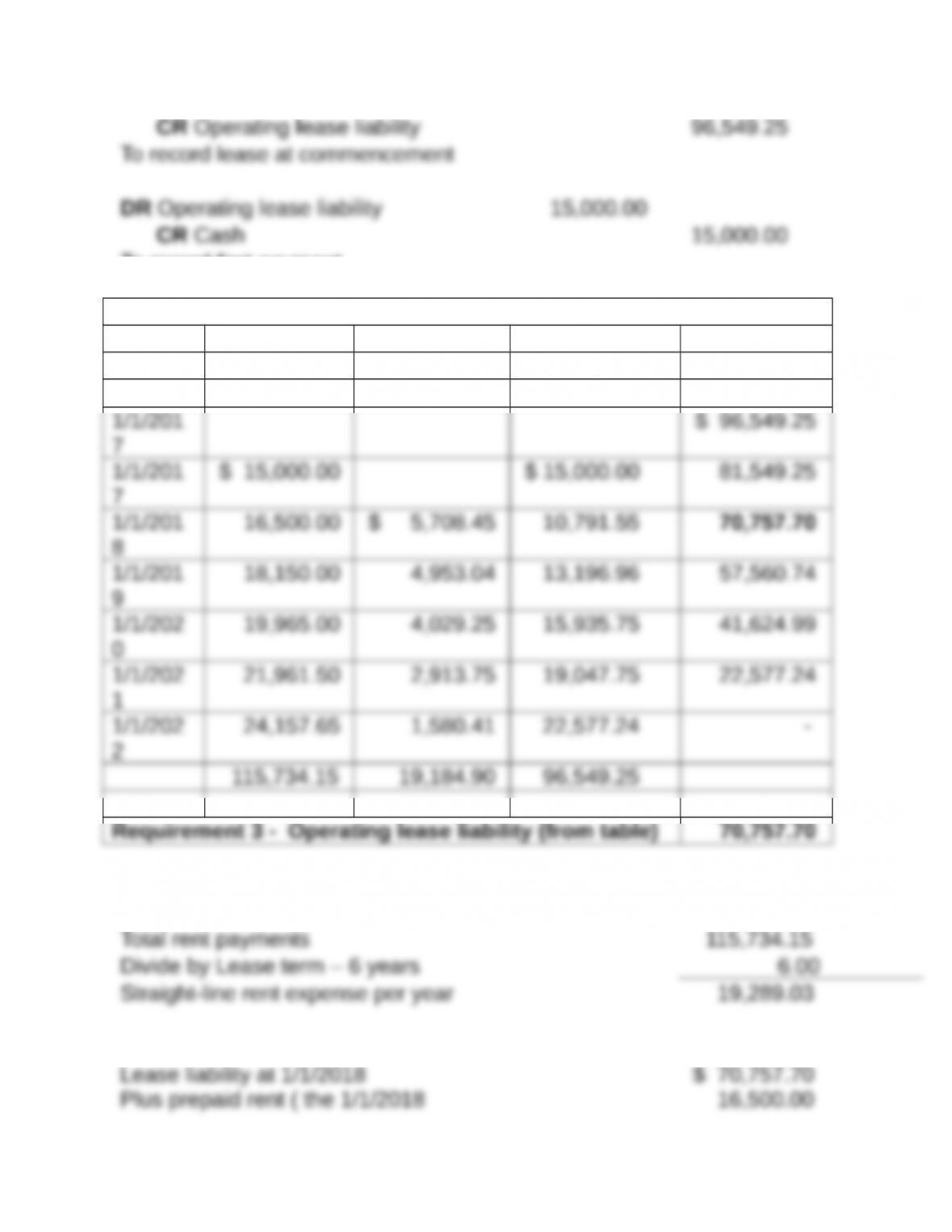

DR Right-of-use asset—Operating lease

96,549.25

To record first payment

Requirement 2 – Amortization table

Total Interest Principal

Date Payment Expense Reduction Balance

Requirement 4 – Right-of-use asset—Operating lease

Relation between lease liability and right-of-use asset

payment)

Less difference between prior cash

payments and rent expense

Journal entry approach:

12/31/17

(Straight-line expense of $19,289.03 less interest on liability $5,708.45)

To record lease expense and effects on right-of-use asset and liability

1/1/2018

Right of use asset

Operating lease liability

E12-3. Accounting for lessee with purchase option under ASC 840 (LO

12-3)

(AICPA adapted)

Because the purchase option approximates the fair value of the

To find the amount of the capitalized lease, we need to find the

present value of the minimum lease payments plus the present

So, the amount of the capitalized lease asset is $230,863.

E12-4. Accounting and reporting for lessee under ASC 840 (LO 12-3,

LO 12-5)

(AICPA adapted)

Requirement 1:

To compute the 12/31/2018 lease liability amount, we can construct

an amortization schedule.

Date

Annual

Lease

Payments

Interest

on Unpaid

Obligation

Reduction of

Lease

Obligation

Lease

Obligation

Inception $676,000

We can see from the amortization table that the reduction of the

Requirement 2:

Based on the above table, $42,400 would be classified as a current

To extend it one more year and obtain the current liability at

12/31/2018, we need to look at the next year on the amortization

schedule.

Date

Annual

Lease

Payments

Interest on

Unpaid

Obligation

Reduction of

Lease

Obligation

Lease

Obligation

Inception $676,000

We can see that in 2019, the reduction of the lease obligation will be

E12-5. Accounting for lessee under ASU 2016-02 (LO 12-6)

(AICPA adapted)

Part 1 – Lease classification

Criterion 4

Present Value:

Payment pvoa 3, 9% Present value

0

Ratio of present value to fair value

5

No criterion is met, so it is an operating lease.

Part 2 – Amortization table

Interest Principal

Date Payment Expense Reduction Balance

The lease liability equals $225,165 from the above table. Because

Part 3 – Rent expense

Given that Child used the asset for an entire year, Child would have

one year of expense equal to the amount of the $128,000 lease

E12-6. Accounting for a sales-type lease under ASC 840 (LO 12-7, LO

12-8)

(AICPA adapted)

To find the amount of interest income for 2018, we need to look at

the lease amortization schedule below. Benedict accrues the

Date

Annual

Payment

Interest

Revenue

Reduction

in Net

Investment

Net

Investment

We can see from the table that for the second year, ending

E12-7. Accounting for a direct financing lease under ASC 840 (LO

12-1, 12-7, 12-8)

(AICPA adapted)

To find the amount of interest revenue earned over the life of the

lease, we need to first determine the amount of the each lease

payment. Let Y = amount of each payment.

Next, we must find the gross investment or lease payments

receivable:

The interest revenue earned over the life of the lease is equal to the

gross investment less the net investment.

Total interest revenue that Glade will earn over the life of the lease