E9-9. Computing ending inventory and cost of sales under direct and

absorption costing (LO 12)

(AICPA adapted)

Requirement 1:

Finished goods inventory under variable (direct) costing.

Finished Goods Inventory

To begin, we know cost of goods manufactured and the beginning

balance. We need to find cost of goods sold in order to find ending

inventory. To do this, we must identify the cost to make one unit. We

can obtain this number by dividing the variable cost of goods

manufactured ($800,000) by the number of units manufactured,

Beginning inventory $0

Jacob Perez Company’s ending inventory under the variable costing method would be

$250,000.

Requirement 2:

Operating income under absorption costing is:

Absorption costing includes fixed manufacturing costs in inventory.

To find the fixed manufacturing cost portion of cost of goods sold,

we take:

Under absorption costing, operating (SG&A) expenses are treated

Requirement 3:

Finished goods inventory and cost of goods sold under absorption

costing.

Finished Goods Inventory

To begin, we know cost of goods manufactured and the beginning balance.

We need to find cost of goods sold in order to find ending inventory. To do

this, we must identify the cost to make one unit. We can obtain this number

by dividing the cost of goods manufactured ($1,152,000) by the number of

units manufactured, which is given as 80,000. From this calculation, we get

E9-10. Computing ending inventory and cost of goods sold under

absorption and variable costing (LO 12)

(AICPA adapted)

Requirement 1:

To find the cost of finished goods inventory at December 31, 2017, we first need to find cost

of goods sold for the year; then we will use a T-account analysis to obtain a figure for ending

Now that we know cost of goods sold, we can analyze the finished

goods inventory T-account.

Finished Goods Inventory

X = $7,200

Requirement 2:

Cost of goods manufactured under absorption costing is computed

as follows:

Therefore, comparative total expense would be:

Variable

Costing_

Absorption

_Costing_

Operating income under absorption costing would be $2,500 higher

E9-11. Changing to FIFO method (LO 4)

(AICPA adapted)

Use the given data (cost of goods sold, ending inventory) to derive

purchases, as indicated below:

Average Cost: 2017 2018

Cost of goods sold:

Purchases will be the same regardless of the inventory method in

use, so purchases (derived above), and the given FIFO ending inventory

FIFO: 2017 2018

Cost of goods sold:

Having determined FIFO cost of goods sold, net income for 2018 under

FIFO can be calculated:

2017 2018

Sales $1,000,00

Net income for 2018 is $5,000 higher than it would have been under

average cost. Although ending 2018 FIFO inventory is $15,000 higher,

which decreases cost of goods sold, beginning 2018 FIFO inventory is

$10,000 higher, which increases cost of goods sold. Netting the beginning

E9-12. Converting LIFO to FIFO (LO 5)

Requirement 1:

KW Steel Corp. Waretown Steel

($ in millions) 2017 2016 2017 2016

Balance sheet

(Gross margin/sales)

(COGS/average

inventory)

A comparison of the ratios suggests that KW has a lower gross

margin rate than Waretown, but a better inventory turnover.

Requirement 2:

KW Steel Corp. Waretown Steel

($ in millions) 2017 2016 2017 2016

Cost of Goods sold—LIFO 3,427.8

(COGS/average inventory)

KW’s gross profit rate, as restated, is still below Waretown’s, but the

difference is not quite as great. KW’s inventory turnover has

E9-13. Identifying effects of a LIFO liquidation (LO 6)

Requirement 1:

Requirement 2:

Requirement 3:

When prices are rising, selling more units than are purchased

results in a gross margin increase. This increase occurs when older

units, having lower costs, are presumed to be sold, thus

percentage is .50. But with the LIFO liquidation, the reported

margin percentage is .529. This mismatch can be avoided by

purchasing enough inventory in any given year to avoid liquidating

old LIFO layers.

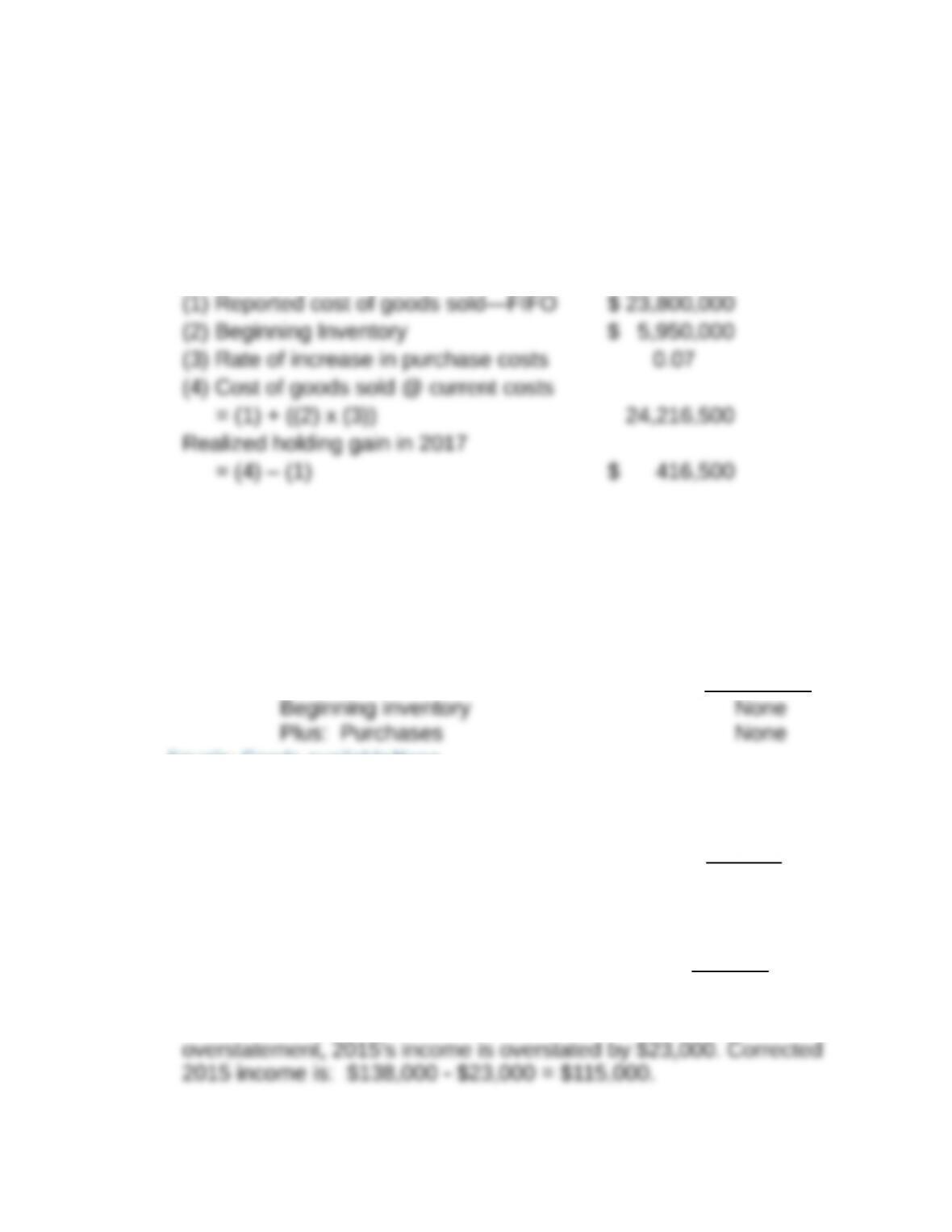

E9-14. Eliminating FIFO holding gains (LO 1, 8)

Realized holding gain in 2017

E9-15. Correcting inventory errors (LO 14)

(CMA adapted)

The easiest way for students to visualize inventory error adjustment

is to use the cost of goods sold formula and analyze the errors one

at a time. Starting with the 2015 error and assuming beginning 2015

inventory was correctly stated:

2015 Error

Equals: Goods availableNone

Minus: Ending inventory

overstated by

$23,000

Equals: Cost of goods sold

understated by

$23,000

Since cost of goods sold is understated due to the ending inventory

Moving on to 2016, the December 31, 2015 ending inventory

becomes the beginning 2016 inventory. Therefore, two adjustments

must be made to 2016 income—one for the feed-forward effect of

the 2015 error and another for the $61,000 2016 understatement.

2015 Error 2016 Error

Beginning inventory

overstated by

$23,000

None

Plus: Purchases None None

overstated by

$23,000

Minus: Ending inventory None

understated by

$61,000

Equals: Cost of goods sold

overstated by

$23,000

overstated by

$61,000

Therefore, 2016 cost of goods sold is overstated by $84,000, and

income is understated by this amount. The corrected 2016 income

is $254,000 + $84,000 = $338,000.

The 2017 computation is:

2016 Error 2017 Error

Beginning inventory

understated by

$61,000

None

Equals: Goods available

understated by

$61,000

None

Minus: Ending inventory None

understated by

$17,000

Equals: Cost of goods sold

understated by

$61,000

overstated by

$17,000

Therefore, 2017 cost of goods sold is understated by $44,000.

E9-16. Computing inventory impairment (LO 10)

(AICPA adapted)

1. Because Moore is using FIFO, market is defined as net

realizable value (NRV) under Accounting Standards Update (ASU)

2015-11. Replacement cost is not used in LCNRV calculations.

a. NRV for product #1 is $25 ($30 selling price less $5 cost to

b. NRV for product #2 is $74 ($100 selling price less $26 cost

2. Because Moore is using LIFO, market is defined as replacement

cost, but it cannot exceed net realizable value or be below net

realizable value less normal profit margin.

a. Market for product #1 is $16 ($25 NRV less $9 profit),

b. Market for product #2 is the replacement cost of $46, which