E12-8. Determining lease payment and depreciation amounts for a capital lease

(LO 12-1, LO 12-3, LO 12-5)

Note that the calculations will be the same for a finance lease under ASC 842.

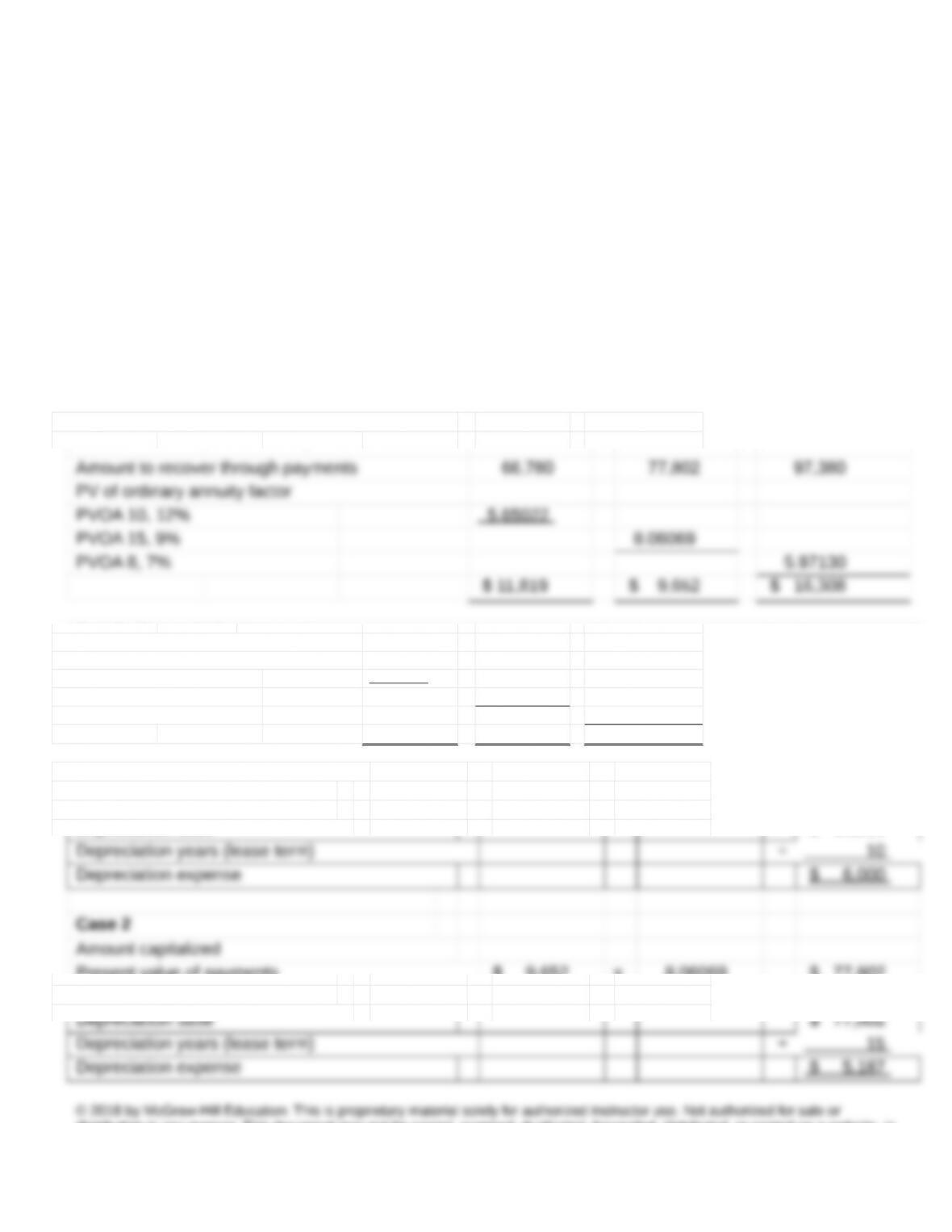

Part 1 – Lease payment computations

Case 1 Case 2 Case 3

Amount to recover through payments 66,780 77,802 97,380

PV of ordinary annuity factor

PVOA 10, 12% 5.65022

PVOA 15, 9% 8.06069

PVOA 8, 7% 5.97130

$ 11,819 $ 9,652 $ 16,308

Part 2 – Depreciation expense

Case 1

Amount capitalized

Case 2

Amount capitalized

© 2018 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or

distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in

whole or part. 12-1

Case 3

Amount capitalized

Present value of payments $ 16,308 x 5.97130 $ 97,380

PV of bargain purchase option 4,500 x 0.58201 2,619

© 2018 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or

distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in

whole or part. 12-2

E12-9. Determining lease payment, lease classification, and lease liability under ASU 2016-02 (ASC 842) (LO

12-1, LO 12-6)

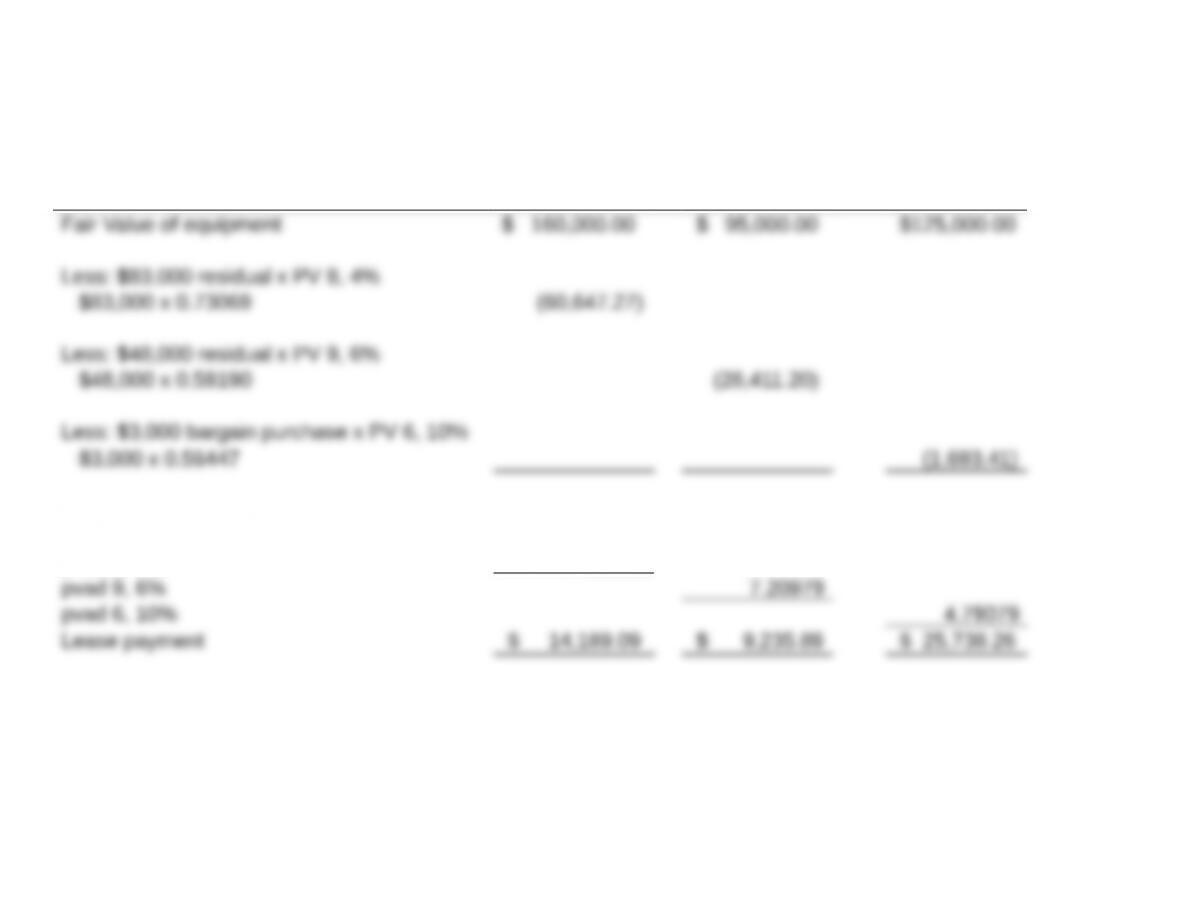

Part 1: Lease payments

Case 1 Case 2 Case 3

Amount to recover through payments $ 99,372.53 $ 66,588.80 $123,306.59

Divide by pvad factor

pvad 8, 4% 7.00205

© 2018 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any manner. This document may not be

copied, scanned, duplicated, forwarded, distributed, or posted on a website, in whole or part. 12-3

Part 2: Lease classification

Bargain purchase option (criterion 2) no no yes

Ratio of lease term to economic life (critierion 3)

Part 3. Lease liability on the Balance Sheet

Case 1 Case 2 Case 3

© 2018 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any manner. This document may not be

copied, scanned, duplicated, forwarded, distributed, or posted on a website, in whole or part. 12-4

E12-10. Determining lease classification and lease liability under

ASU 2016-02 (LO 12-6)

(AICPA adapted)

Part 1 – Lease classification

Present Value:

Implicit rate is known so

use 11%

Payment pvad 5, 11% Present value

No criterion is met, so it is an operating lease.

Part 2 – Operating lease liability

Since Day knows the lessor’s implicit rate, Day must use Parr’s

implicit discount rate. We can determine the amount of Day’s lease

liability at the beginning of the lease term as follows:

© 2018 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for

sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or

posted on a website, in whole or part. 12-5

E12-11. Accounting for lessee operating lease under ASU 2016-02

(ASC 842) (LO 12-1, LO 12-6)

(AICPA adapted)

Part 1 – Value of leased equipment

Present Value:

Payment pvoa 5, 11% Present value

Part 2 – Rent expense

Rent payment

Portion of

year

Rent

expense

© 2018 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for

sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or

posted on a website, in whole or part. 12-6

Refer to the above effective interest table

12/31/2017 12/31/2018

The principal reduction of $5,934.51 is not multiplied by 25% because it

represents the portion of the $36,959 that will be paid in 2018. In contrast,

E12-12. Accounting for lessee guaranteed residual under ASC 840

(LO 12-3, LO 12-5)

(AICPA adapted)

We know that there is no interest accrued when the first payment

© 2018 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for

sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or

posted on a website, in whole or part. 12-7

Date

Annual

Payment

Interest

on Unpaid

Obligation

Reduction

of Lease

Obligation

Lease

Obligation

Inception $61,615

E12-13. Accounting for executory costs under a capital lease under

ASC 840 and ASU 2016-02 (ASC 842) (LO 12-1, LO 12-3, LO

12-6)

(AICPA adapted)

Requirement 1: ASC 840

A partial lease amortization table for Roe Company follows. Keep

in mind that executory costs are part of the annual payment but

Date

Annual

Payment

Executory

Costs

Interest

on Unpaid

Obligation

Reduction

of Lease

Obligation

Lease

Obligation

As shown in the table, Roe would report $248,686 as its lease

liability on the December 31, 2018 balance sheet.

Requirement 2: ASU 2016-02 (ASC 842)

E12-14. Accounting for sale and leaseback under ASC 840 and ASU

2016-02 (ASC 842) (LO 12-4, LO 12-6)

(AICPA adapted)

© 2018 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for

sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or

posted on a website, in whole or part. 12-8

Requirement 1 – Deferred gain under ASC 840:

deferred and amortized over the life of the lease. Therefore, no

gain is recognized on the sale and leaseback in 2017.

Requirement 2 – Treatment of gain in subsequent years under

ASC 840:

Lane should defer the $120,000 gain on the sale of equipment and

amortize it over the 12-year lease term.

Requirement 3 – Treatment of gain under ASU 2016-02:

Because the ratio of the lease term to the economic life is 80%

(12-year lease term ÷ 15-year economic term), the lease would

E12-15. Determining cash flow statement effects of capital versus

operating leases under ASC 840 and ASU 2016-02 (ASC 842)

(LO 12-5, LO 12-6)

Requirement 1 – Operating lease under ASC 840:

Requirement 2 – Capital lease under ASC 840:

Operating Investing Financing

Cash Flows Cash Flows Cash Flows

© 2018 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for

sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or

posted on a website, in whole or part. 12-9

Operating cash flows are reduced by the amount of each period’s

interest expense since GAAP treats interest expense as an

operating cash outflow. Depreciation expense would not affect the

operating section under the direct method. In the initial year of the

lease, a firm treats the capital lease as a significant noncash

Requirement 3 – Operating lease under ASU 2016-02 (ASC

842):

If the lease is an operating lease under ASU 2016-02 (ASC 842),

in the initial year of the lease, the firm would treat the operating

lease as a significant noncash investing and financing activity for

$77,313. Rent expense would be the same as it would have been

under ASC 840. The amortization of the right-of-use asset in each

E12-16. Determining ratio effects of capital versus operating leases

under ASC 840 and ASU 2016-02 (ASC 842) (LO 12-2, LO12-5,

LO 12-6)

Requirement 1 – ASC 840 capital lease effect on current ratio

and debt-to-equity ratio:

© 2018 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for

sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or

posted on a website, in whole or part. 12-10

Nova’s current ratio prior to the leasing transaction was

$2,000/$2,000 = 1.0. After the leasing transaction is recorded,

Prior to the lease transaction, Nova’s debt-to-equity ratio was

$2,500/

Requirement 2 – ASC 840 capital lease effect on turnover

ratio:

Prior to the lease transaction, Nova’s asset turnover ratio was

$10,500/$5,000 = 2.1. After the leasing, the ratio will decrease

Requirement 3 – ASC 840 operating lease effect on ratios:

Sandra’s current ratio, debt-to-equity ratio, and total asset turnover

Requirement 4 – ASU 2016-02 operating and finance lease

effects on ratios

Under ASU 2016-02, the effects of the lease at commencement

would be identical for Sandra and Nova. Under ASU 2016-02, a

© 2018 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for

sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or

posted on a website, in whole or part. 12-11