Financial Reporting and Analysis (7th Ed.)

Appendix B Solutions

Essentials of Financial Statement Analysis

Exercises

EB-1 Determining reportable segments (LO B-1)

(AICPA adapted)

ASC 280 provides quantitative guidelines for reporting segments. A

company must report separate segment information if either

1. Segment revenue equals or exceeds 10% of total revenue from

internal and external customers, or

2. Segment assets equal or exceed 10% of total segment assets.

The Hardware sales segment exceeds both the 10% of revenue and

assets thresholds.

The Consulting segment exceeds the 10% of revenue threshold.

The Financing segment exceeds the 10% of assets threshold.

Lannister would not have to disclose separate information for the Hardware

service and Rising technology segments.

EB-2 Determining reportable segments (LO B-1)

(AICPA adapted)

ASC 280 provides quantitative guidelines for reporting segments. A

company must report separate segment information if the absolute value of

operating profit or loss equals or exceeds 10% of the maximum of either:

1. the total segment operating profit for those segments with profits, or

2. the absolute value of the total segment operating loss for those

segments with losses.

The first step is to compute the total income or total loss to be used for the

10% threshold. Mannix would compute the threshold as follows:

Segment

s with

income

Segment

s with

losses

B-1

Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

Appliances $357

Healthcare 233

Transportation $ (57)

Financial

Services 46

Other stuff (124)

Total $636 $(181)

The maximum value here is $636. Any segment with operating profit or loss

(in absolute terms) greater than or equal to $63.6 (10% of $636) would be a

reportable segment. In this case, Mannix would report separate information

for Appliances, Healthcare, and Other stuff.

EB-3 Aggregating operating segments (LO B-1)

To aggregate segments, the segments must be similar with regard to all of

the following:

1. Product and service,

2. Production process,

3. Type or class of customer,

4. Product and service distribution methods, and

5. Regulatory environment.

The Television stations and the Merchandise sales segments cannot be

aggregated because items 1-4 are not the same. The Television

entertainment production and the Movie entertainment production

segments might be aggregated. The product and service and production

process are similar. However, the initial customer and distribution methods

are different for the two segments. In one case, the initial customer is

television stations, but in the second case, the initial customer is movie

theaters. The accountant may have to evaluate what percentage of

revenue comes from the initial customer as a percentage of total revenue.

In any event, the accountant must use professional judgment to determine

whether the two segments can be combined.

Financial Reporting and Analysis (7th Ed.)

Appendix B Solutions

Essentials of Financial Statement Analysis

B-2

Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

Problems

PB-1 Determining reportable segments

Requirement 1:

U.S. GAAP requires companies to provide segment information to

Requirement 2:

U.S GAAP requires a management approach where the information

is disclosed in the same manner that it is organized internally for

“making operating decisions and assessing performance.” The

standards define an operating segment as a component of a public

Requirement 3:

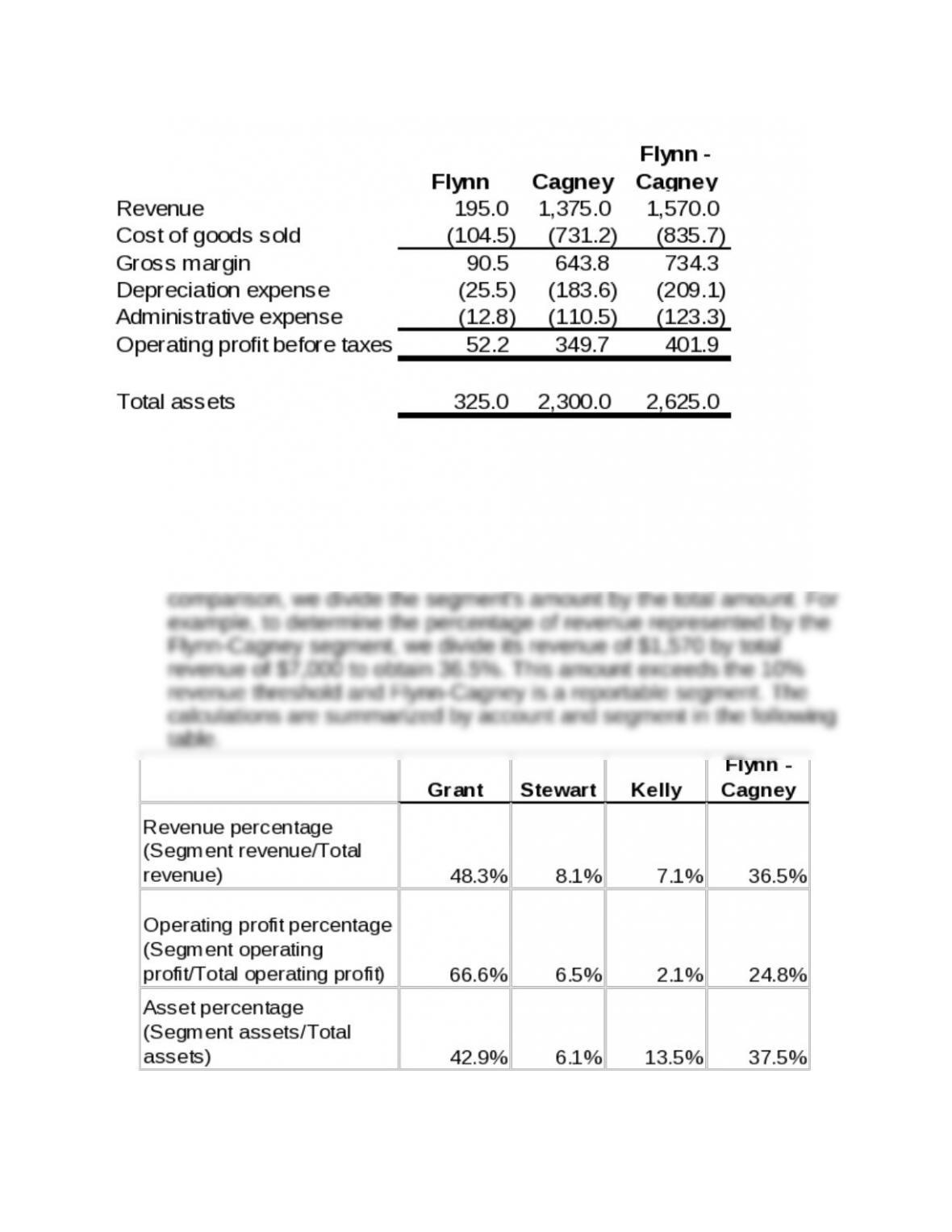

First, Bogart would aggregate operating segments where possible.

The problem states that the Flynn and Cagney segments have

similar economic characteristics, products, processes, customers,

B-3

Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

All amounts are in millions of dollars.

Second, we determine whether any of the segments meet the

quantitative thresholds. Segments are reportable when they

represent 10% or more of revenue, 10% or more of operating profit or

loss (absolute value), or 10% or more of assets. For each

B-4

Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

The calculations show that the 10% revenue, operating profit, and

asset percentages are exceeded for the Grant and Flynn-Cagney

segments. Only one of the comparisons needs to exceed the

Based on the above calculations, Grant, Kelly, and Flynn-Cagney are

reportable segments. The three segments comprise 91.9% (48.3% +

Financial Reporting and Analysis (7th Ed.)

Appendix B Solutions

Essentials of Financial Statement Analysis

Cases

CB-1. IBM: Analyzing reportable segment disclosures (LO B-2)

All amounts are in millions of U.S. dollars. All amounts are 2012

unless indicated otherwise.

Requirement 1:

FASB ASC 280 – Segment Reporting requires companies to disclose

financial information for each operating segment of their business.

Operating segments for purposes of this disclosure must be the same

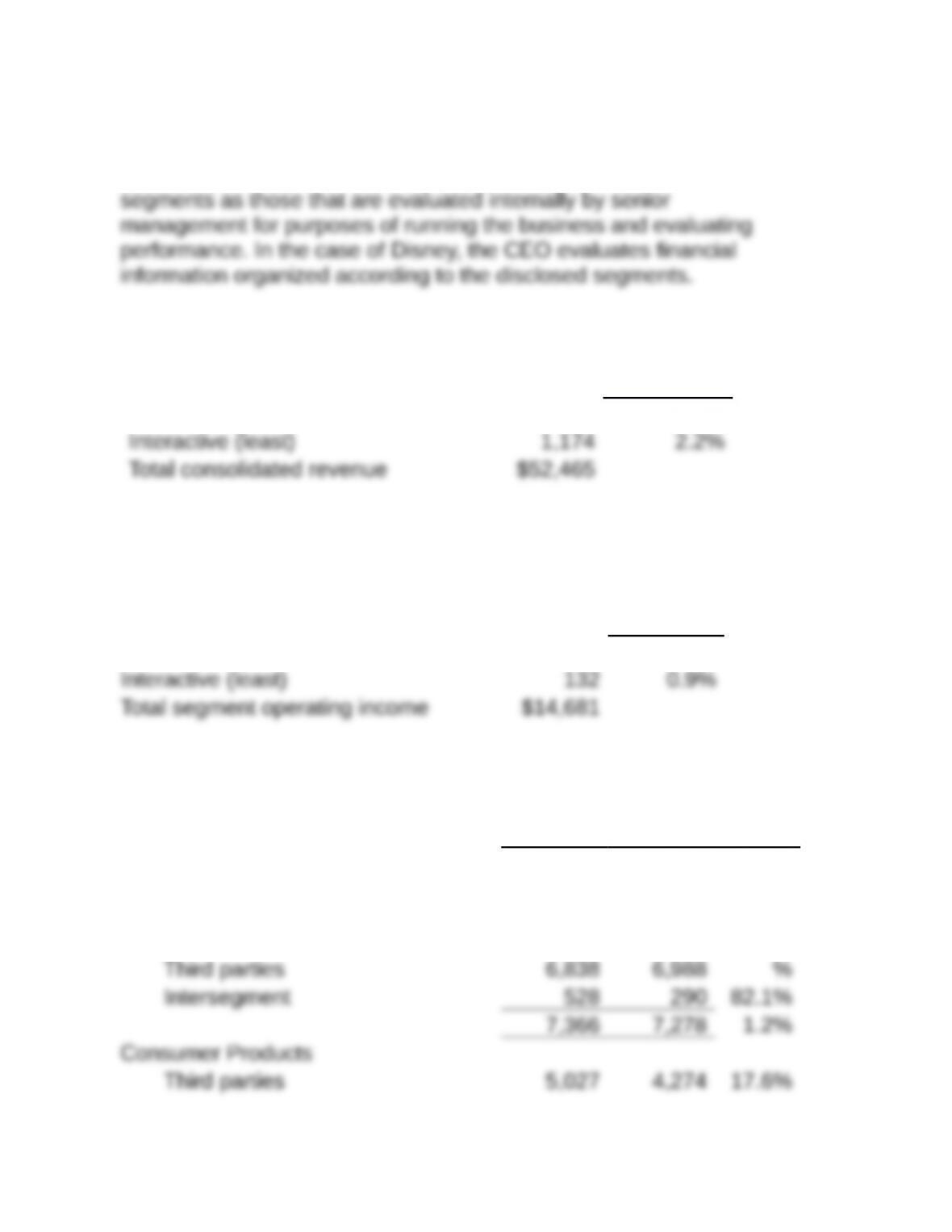

segments as those that are evaluated internally by senior management for

Requirement 2:

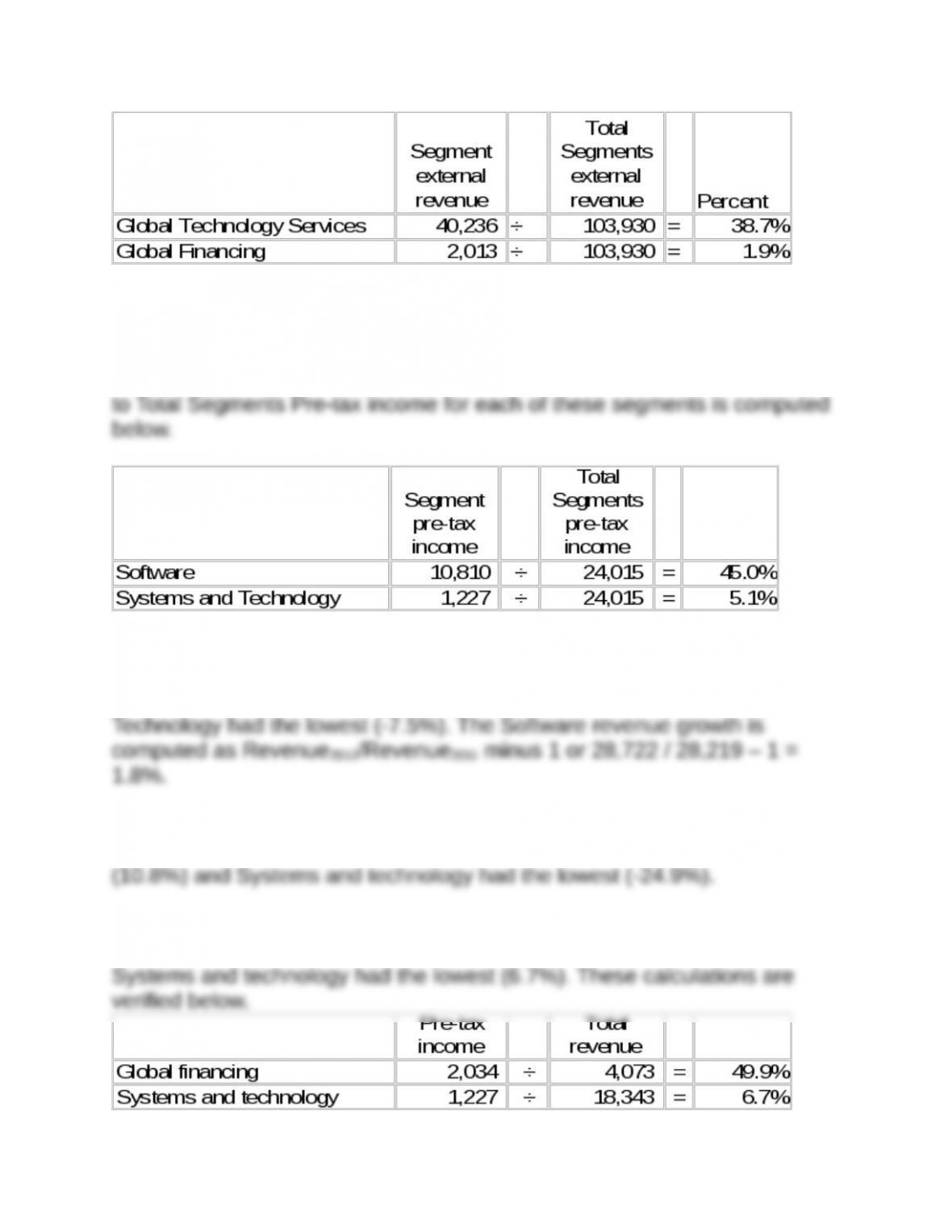

Global Technology Services has the most external revenue ($40,236) and

Global Financing has the least ($2,013). The percent of Segment external

B-5

Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

Requirement 3:

Software has the most Pre-tax income ($10,810) and Systems and

Technology has the least ($1,227). The percent of Segment Pre-tax income

Requirement 4:

Software had the highest growth in revenue (1.8%) and Systems and

Requirement 5:

Global technology services had the highest growth in Pre-tax income

Requirement 6:

Global financing had the highest Pre-tax income margin (49.9%) and

B-6

Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

Requirement 7:

Analysts may use the information to predict growth in earnings for next

year, evaluate how well IBM is managing different segments, or determine

if the mix within segments of income and revenue is changing. The analysis

in Requirements 3 through 6 suggest that the Systems and Technology

Requirement 8:

The Global Financing segment’s balance sheet and income statement are

similar to those of a bank. Most of its assets are financial assets and its

Requirement 9:

Note that most of IBM’s revenue comes from outside the U.S. Therefore,

analysts must consider the effects of currency rate changes and economic

Requirement 10 – How would a stronger U.S. dollar affect IBM’s future

reported revenue?

Given that only 34.7% of IBM’s revenue is in the U.S., we would expect

consolidated revenue and profit to decrease substantially because of the

increasing strength of the dollar. Because the ratio of US$ per unit of

CB-2. Walt Disney Company: Analyzing reportable segment

disclosures (LO B-2)

Requirement 1 – Significance of CEO review

B-7

Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

FASB ASC 280 – Segment Reporting requires companies to disclose

financial information for each operating segment of their business.

Operating segments for purposes of this disclosure must be the same

Requirement 2 – Most and least external revenue

Percent of

Total

Media Networks (most) $23,264 44.3%

Requirement 3 – Most and least segment operating

income

Percent of

Total

Media Networks (most) $7,793 53.1%

Requirement 4 – Highest and lowest growth in revenue

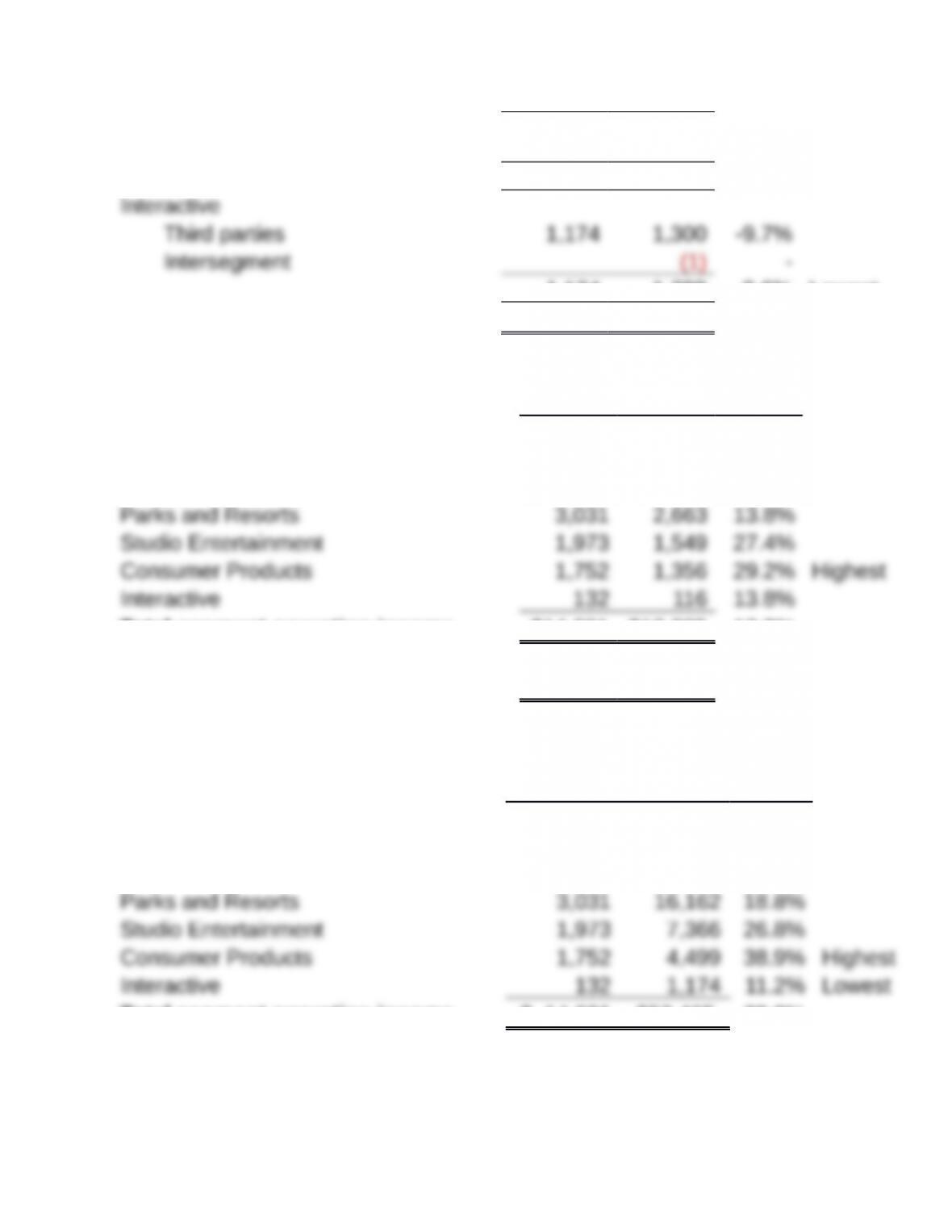

Segment 2015 2014

Growt

h

Media Networks $23,264 $21,152 10.0%

Parks and Resorts 16,162 15,099 7.0%

Studio Entertainment

-21.5

B-8

Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

Intersegment (528) (289)

-82.6

%

4,499 3,985 12.9% Highest

1,174 1,299 -9.6% Lowest

Total consolidated revenues $52,465 $48,813 7.5%

Requirement 5 – Highest and lowest growth in operating income

2015 2014 Growth

Growth=2015 amount/2014 amount less 1

Segment

Media Networks $7,793 $7,321 6.4% Lowest

Total segment operating income $14,681 $13,005 12.9%

Income before income taxes $13,868 $12,246 13.2%

Requirement 6 – Highest and lowest operating income margin

Income Revenue

Margi

n

Margin=operating income/revenue

Segment

Media Networks $ 7,793 $23,264 33.5%

Total segment operating income $ 14,681 $52,465 28.0%

Requirement 7 – Analyst use

B-9

Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

Analysts may use the information to predict growth in earnings, evaluate how

well Disney is managing different segments, or determine if the mix within

segments of income and revenue is changing. An analyst would want to make

growth forecasts based on the expected mix of revenue. The analysis in

Requirement 8 – Percentage of revenue earned in the U.S.

Percent=locality/total Percent

United States and Canada $40,320 76.9%

Europe 6,507 12.4%

Requirement 9 – Percentage of revenue earned in the U.S.

Consumers in the rest of the world probably still like Frozen, Star

Wars, and Winnie the Pooh. However, the dollar increased in value

B-10

Copyright © 2018 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.