Financial Reporting and Analysis (7th Ed.)

Chapter 4 Solutions

Structure of the Balance Sheet and Statement of Cash Flows

Exercises

Exercises

E4-1. Analyzing balance sheet classification

b Long-term receivables

(d) Accumulated amortization

f Current maturities of long-term debt

c Machinery

h Donated capital

a Short-term investments

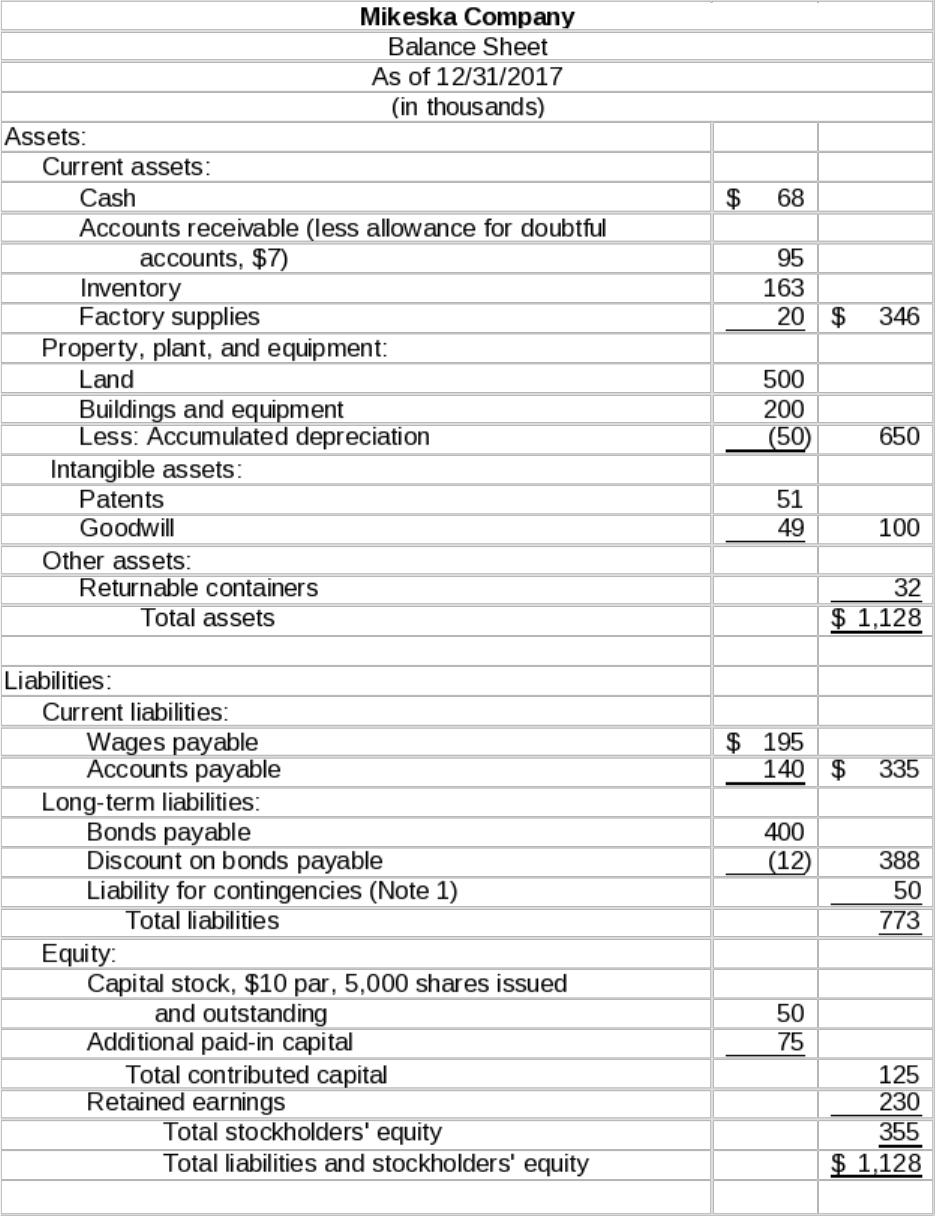

E4-2. Preparing a balance sheet

(1) This classification assumes this amount has been properly accrued. If,

instead, the item is interpreted as an appropriation of retained earnings, it

E4-3. Making financial disclosures

Investments in available-for-sale securities. Eagle must disclose

Accounts receivable (net). Estimated uncollectibles, discounts, returns,

Inventories. The basis of pricing inventories should be disclosed, that is,

lower of cost or net realizable value, or lower of cost or market

when the LIFO or retail inventory method is used. The inventory

Property, plant, and equipment. Major classes of depreciable assets

should be disclosed. Depreciation expense and the methods

Current liabilities and long-term debt. Maturities, interest rates, and other

terms and conditions provided in the loan agreement should be

Stockholders’ equity. For each class of stock, disclosure should be made

regarding the par or stated value and the total number of shares

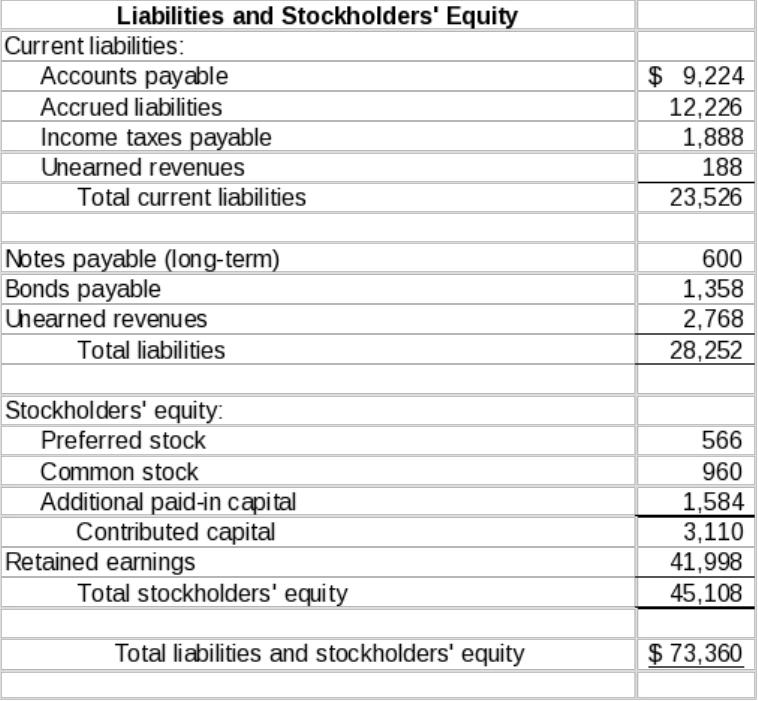

E4-4. Balance sheet classification

Reagan Company

Balance Sheet

As of December 31, 2017

Assets Liabilities and Stockholders’ Equity

Current assets: Current liabilities:

Cash Accounts payable

Finished goods

Prepaid expenses Long-term liabilities

Total current assets Bonds payable

Land

Buildings Stockholders’ equity:

Less: Accumulated depreciation Preferred stock

Machinery and equipment Common stock

Trademarks

Total assets

E4-5. Determining collections on account

(AICPA adapted)

Cash receipts from sales include collections on account plus cash sales,

computed as follows:

Alternative Solution: T-account analysis of accounts receivable

Accounts Receivable

X = $2,915,000

Total cash receipts from sales:

E4-6. Determining cash from operations

(AICPA adapted)

Cash flows from operations:

Note that cash dividends paid is a financing activity.

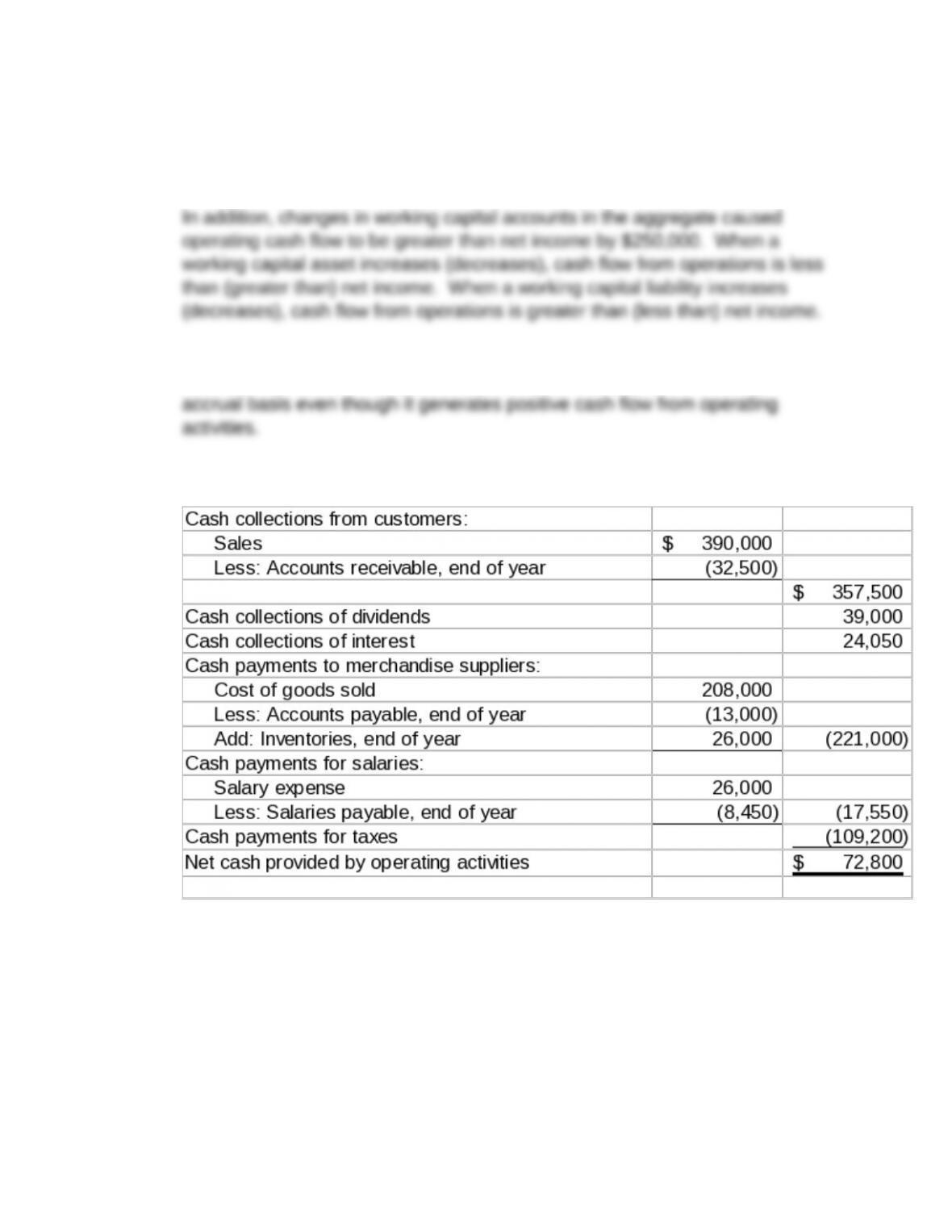

E4-7. Determining cash payments to suppliers

E4-8. Determining cash disbursements

(AICPA adapted)

To answer this question, one needs to first determine the accrual basis

expenses and then (1) subtract from this figure expenses not paid in cash; and

(2) add amounts paid out in cash not recorded as accrual expenses.

Total accrual basis expenses:

Subtract: Noncash expenses

E4-9. Determining cash collections on account

(AICPA adapted)

Cash collected from customers can be determined by finding the change in

accounts receivable.

E4-10. Determining cash from operations and reconciling with accrual net

income

Requirement 1:

Cash provided by operating activities:

Requirement 2:

Net income was $100,000, while cash flow from operating activities was

($150,000). $30,000 of difference is explained by depreciation, a noncash

expense. It reduced net income without having any effect on cash flow.

Depreciation caused net income to be $30,000 less than cash flow from

Note: This problem demonstrates that a firm can be profitable under the accrual

E4-11. Determining cash from operations and reconciling with accrual net

income

Requirement 1:

Cash provided by operating activities:

Noncash expenses:

Changes in working capital accounts:

Requirement 2:

Net loss was $200,000, while cash flow from operating activities was $100,000.

$50,000 of difference is explained by depreciation, a noncash expense. It

reduced net income without having any effect on cash flow. Depreciation

caused net income to be $50,000 less than cash flow from operating activities.

Note: This problem demonstrates that a firm can be unprofitable under the

E4-12. Cash provided (used) by operations

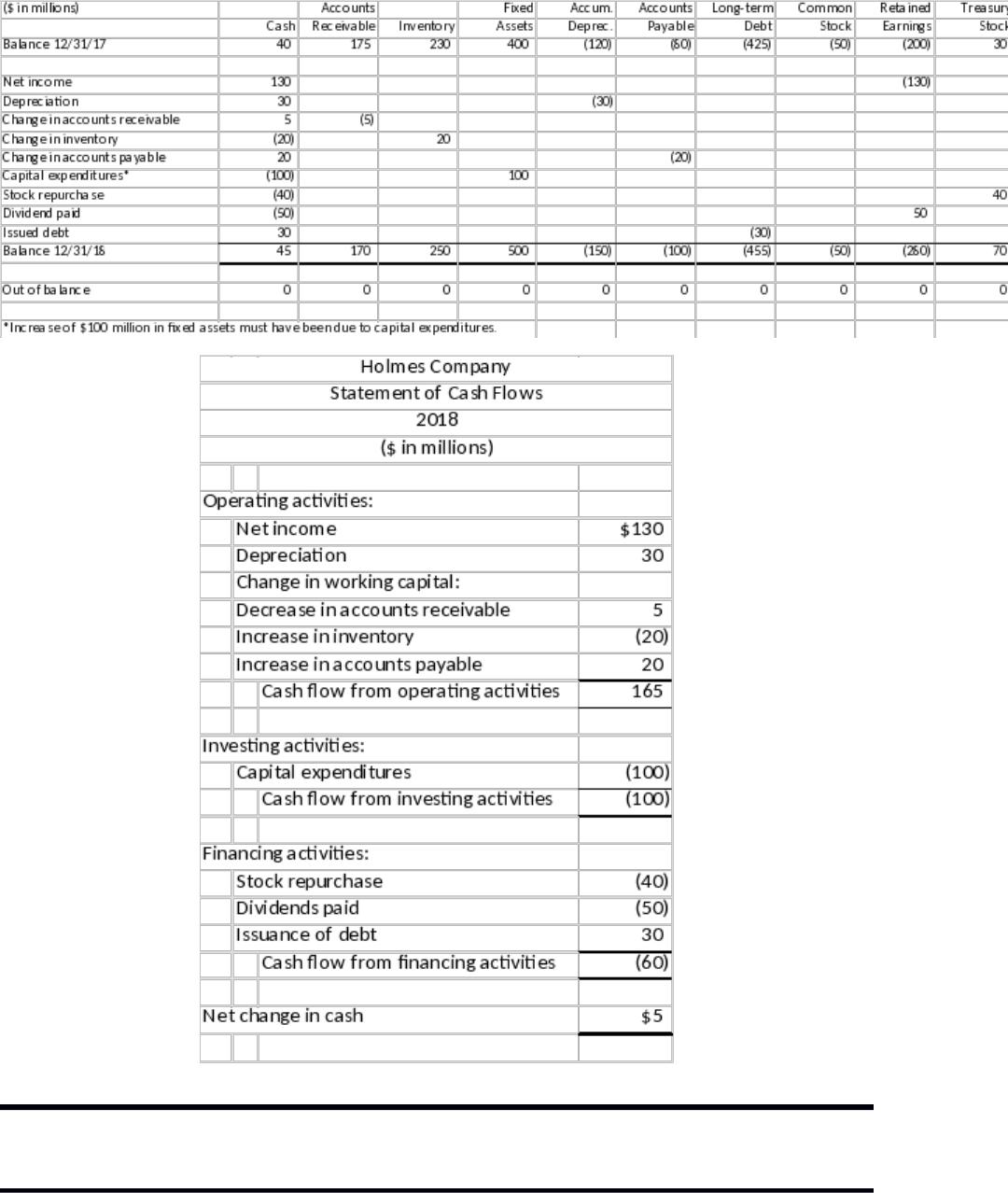

E4-13. Construction of cash flow statement

Financial Reporting and Analysis (7th Ed.)

Chapter 4 Solutions

Structure of the Balance Sheet and Statement of Cash Flows

Problems

Problems

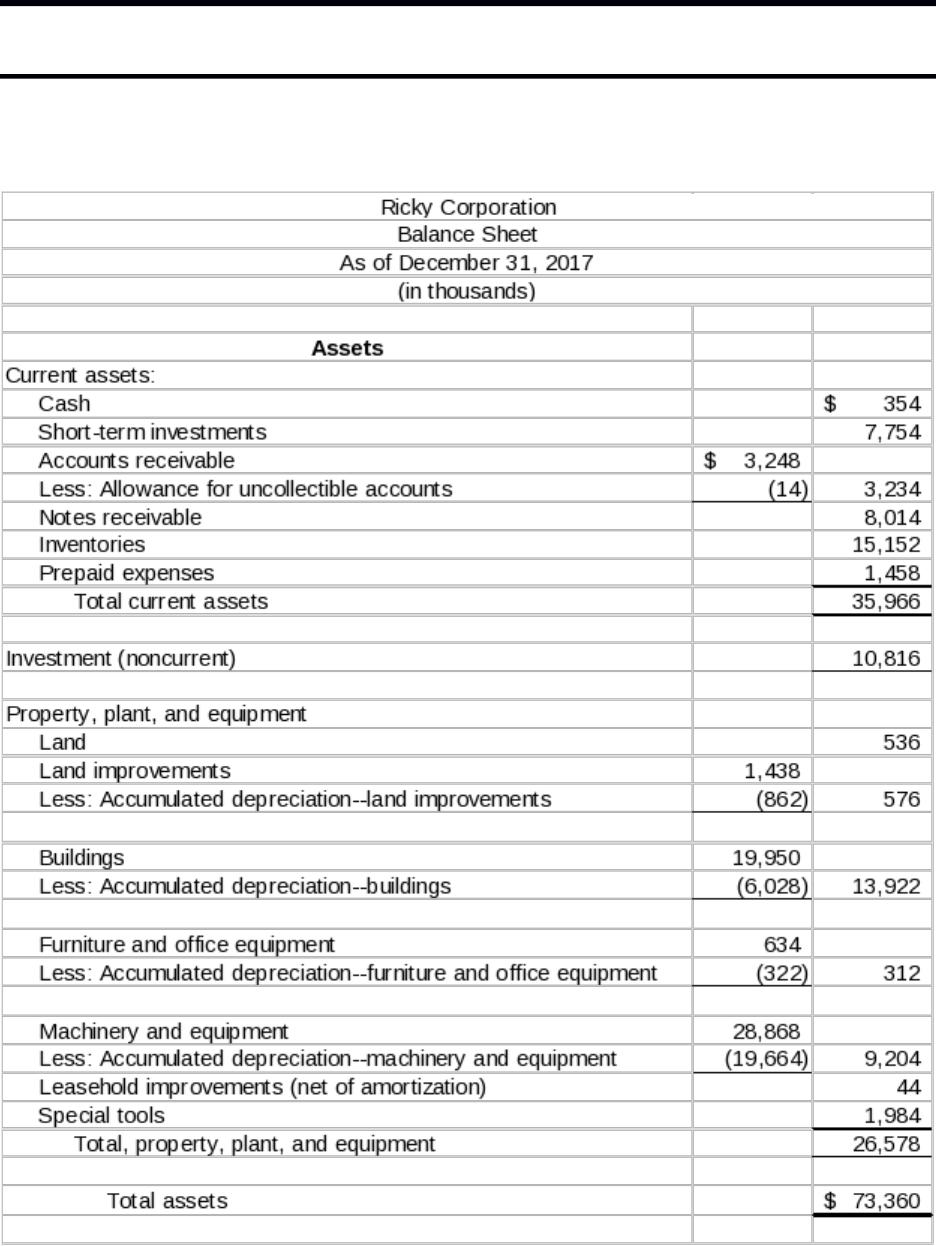

P4-1. Preparing a balance sheet