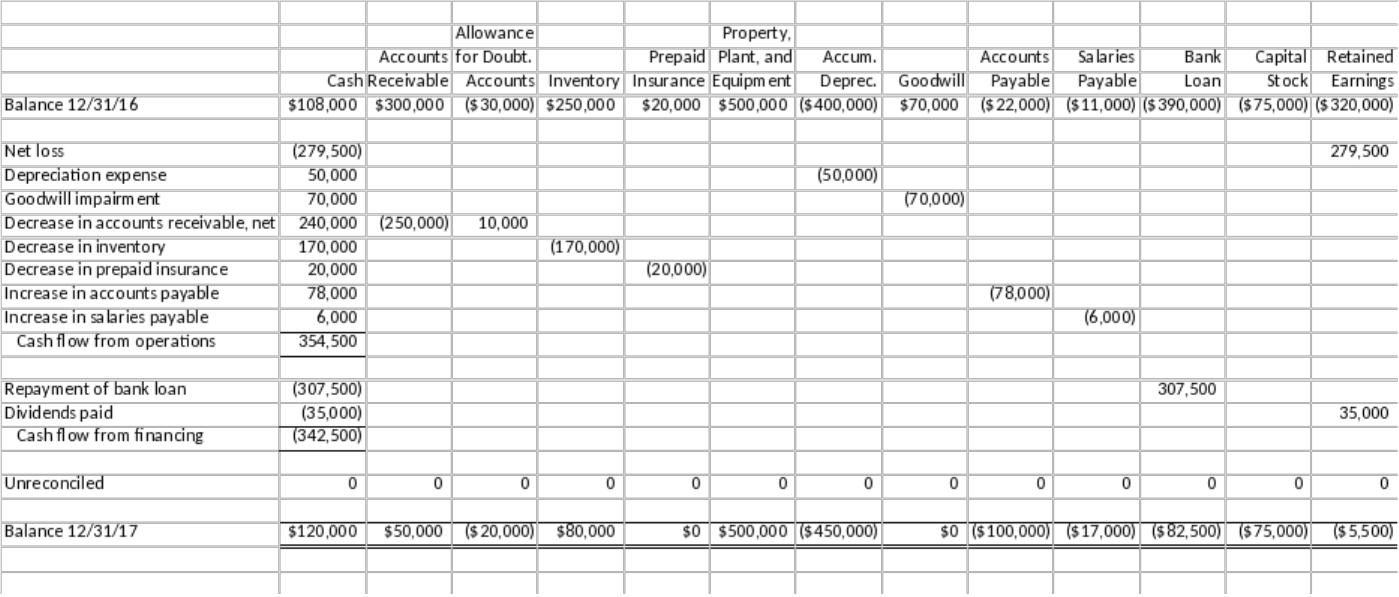

P17-5. Preparing and analyzing cash flow statement

Requirement 1:

Global Trading Company

Statement of Cash Flows

For the Year Ended December 31, 2017

Cash flow from operations

Net loss for the year ($279,500)

Cash flow from operations 354,500

Cash flow from financing activities

Cash flow from financing activities (342 ,500)

Net increase in cash 12,000

The following spreadsheet derives the amounts in the cash flow statement. For

17-1

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

17-2

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education.

Requirement 2:

Global Trading reported a net loss in 2017, which is clearly an indication of

has declined in value.

However, examining the components of the reconciliation between net income

and operating cash flow suggests that the positive operating cash flow is

temporary and will not continue unless Global returns to profitability. Global

bills or anticipates having difficulty and is therefore trying to preserve cash.

Global did pay off its bank loan in 2017, although its situation would suggest

that this may have been because it was required to do so, either because the

and receivable balances as much as it did, unless it had been able to obtain

other financing.

It is likely Global was not able to find a new source of funding, and so it

17-3

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

dividends in 2017, which, given the company’s situation, seems rather

imprudent.

Finally, the balance sheet indicates that fixed assets are almost fully

place, Global has little hope of turning around its performance.

Requirement 3:

Determination of bad debts written off can be obtained from T-account analysis

Determination of credit sales for the year can be obtained from T-account

analysis of accounts receivable:

account.

Requirement 4:

Effect of omission of inventory purchase:

Income Statement

No effect. (Purchases and ending inventory are understated by equal amounts.

17-4

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

Statement of Cash Flows

Although the cash flow from operations are unaffected, two components are

Balance Sheet

P17-6. Reconciling changes in balance sheet accounts with amounts reported in

the cash flow statement

Requirement 1:

The 2015 cash flow statement showed an increase in accounts and notes

balance sheet ($182.1 million – $169.5 million = $12.6 million).

Possible explanations for the difference for accounts receivable include:

Foreign exchange translation adjustments whereby the U.S. dollar value of

the change in receivables.

Requirement 2:

Stanley Black & Decker had nearly $1.2 billion of operating cash flow. It was

partially offset by a $205 million investing cash outflow. Still, those two

million to repurchase common stock, and about $630 million to redeem

preferred stock in 2015.

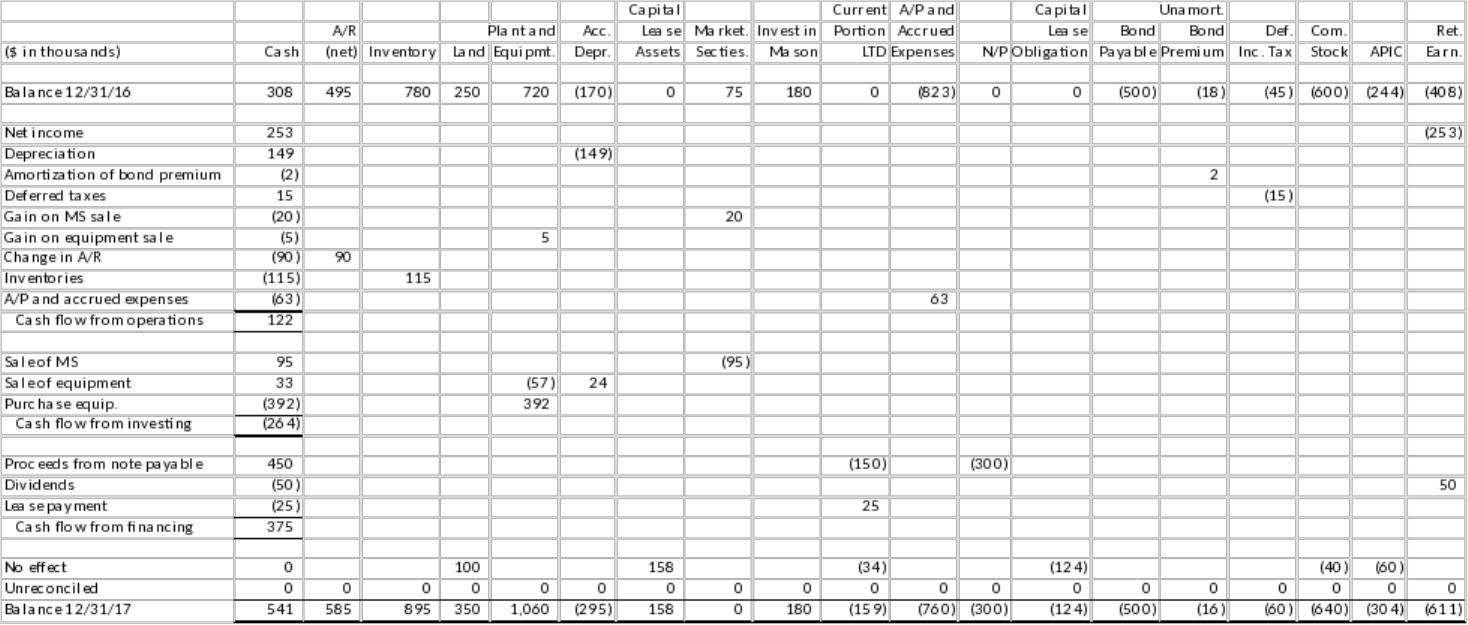

P17-7. Preparing cash flow statement–indirect method

(AICPA adapted)

Cash flow for 2017 using the indirect method:

17-5

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

Bergen Corporation

Statement of Cash Flows

For the Year Ended December 31, 2017

– Gain on sale of equipment (5,000)

– Increase in accounts receivable, net (90,000)

– Increase in inventories (115,000)

Purchase of equipment (392 ,000)

Net cash outflow from investing activities (264,000)

Net cash flow provided by financing activities 375 ,000

Net increase in cash 233,000

17-6

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

17-7

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education.

P17-8. Working backward from the statement of cash flows

(2) DR Cash (Operations—Depreciation expense

add-back) $ 496,106

CR Accumulated depreciation $496,106

P,P&E add-back) $ 32,482

DR Cash (Investing—Proceeds from sale of

P,P&E) 4,150

CR Property, plant and equipment $36,632

accounts receivable) $140,082

(9) DR Cash (Operations—Decrease in

inventories) $ 2,302

CR Inventories $2,302

(10) DR Prepaid expenses $ 5,825

17-8

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

(14) DR Cash (Operations—Increase in other

noncurrent liabilities) $ 24,434

CR Other noncurrent liabilities $24,434

(15) DR Property, plant and equipment $ 693,489

CR Cash (Financing—payment of

dividends) $325,295

(22) DR Cash (Financing—proceeds from other,

net) $ 18,530

17-9

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

CR Other, net $18,530

17-10

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.