P5-4 Decomposing return on common shareholders’ equity

Requirement 1:

ROCE measures a company’s performance in using capital

provided by common shareholders to generate earnings. ROCE

ROA measures the profitability of operations before considering how

Requirement 2:

Financial leverage has the effect of making ROCE more extreme.

That is, in good years (i.e., when ROA is high), ROCE is even

higher when the firm has leverage, and the more leverage, the

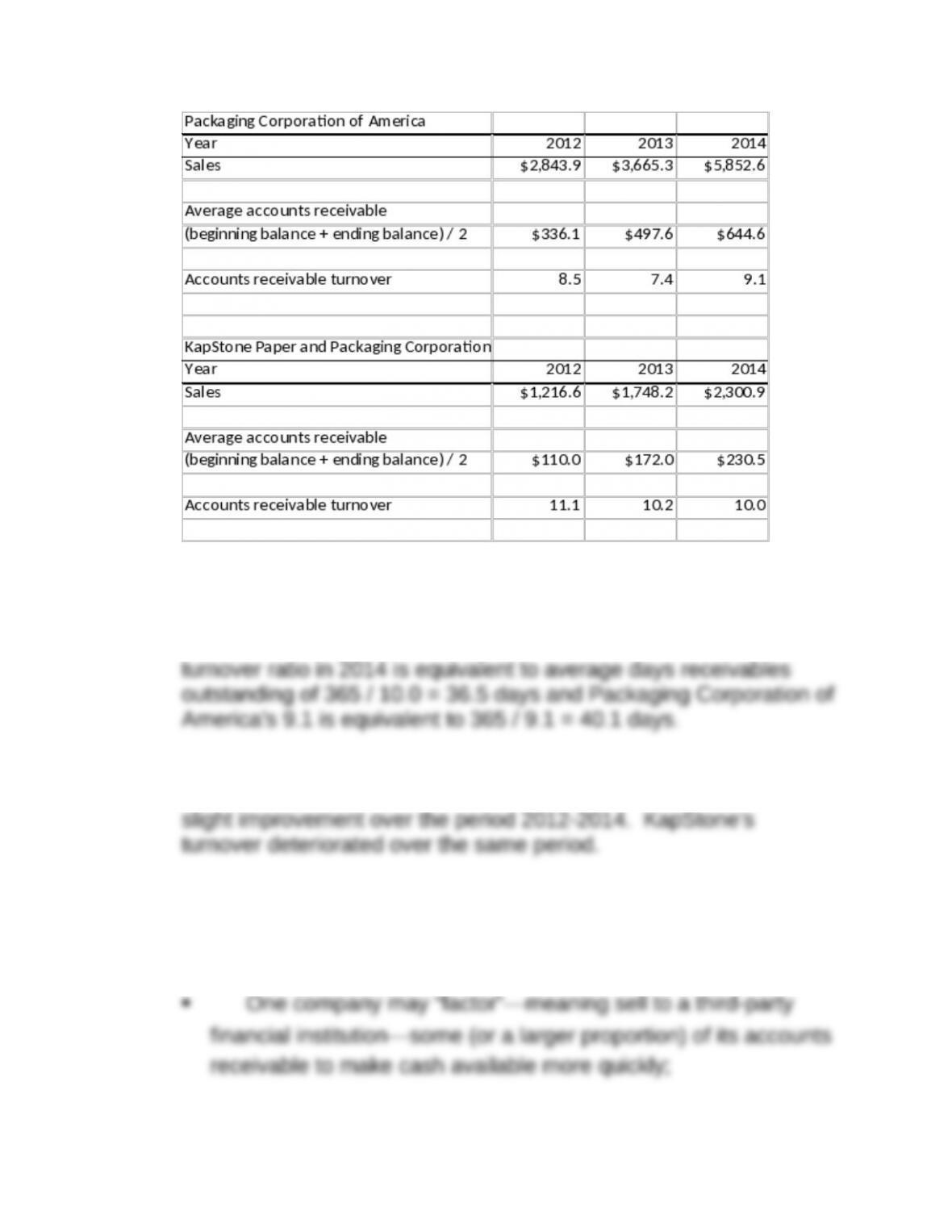

P5-5 Interpreting accounts receivable turnover

Requirement 1:

Accounts receivable turnover is computed as sales divided by

average accounts receivable outstanding, where average

Requirement 2:

KapStone collected its receivables somewhat more quickly in 2014

than did Packaging Corporation of America. KapStone’s 10.0

Requirement 3:

Packaging Corporation of America’s receivable turnover showed

Requirement 4:

Possible reasons for the different accounts receivable turnover

ratios include:

One company may be more aggressive in its collection

efforts;

Requirement 5:

Computing average accounts receivable outstanding by averaging

the beginning and ending balance assumes the change in the

receivables outstanding happened evenly throughout the year. If

Firms whose operations are seasonal are likely to show significantly

different receivable levels throughout the year, whereas the annual

balance sheet takes a snapshot at the same point in the seasonal

“Window dressing” refers to actions managers might take to make

the balance sheet as of the reporting date (i.e., year end) appear

more healthy than it is during the rest of the year. To the extent that

To mitigate this effect, one might take an average of quarterly

averages. The assumption now is that the change over each

12/31/16, 3/31/17, 6/30/17, 9/30/17, and 12/31/17. The weights on

the five dates, respectively, are 1/8, 1/4, 1/4, 1/4, and 1/8.

P5-6 Analyzing inventories

Danaher’s inventory turnover ratio improved from 2012 to 2014.

Inventory turnover will remain constant when cost of goods sold and

average inventory level grow at the same rate. In 2013, average

Danaher’s higher inventory turnover indicates it is servicing its

P5-7 Analyzing fixed asset turnover

Requirement 1:

Lennox International has higher turnovers (both current asset and

fixed asset) than Tecumseh Products, except in 2014 when

Requirement 2:

Because ROA = Operating profit margin x Asset turnover, it is

Operating profit margin 2012 2013 2014

Lennox’s operating margins have been positive and growing, while

Tecumseh’s have been negative the last two years. Tecumseh’s

P5-8 Determining accounting quality

Requirement 1:

Capitalizing leases increases the amount reported for both assets

and liabilities, thereby increasing both the numerator and

denominator in the long-term debt to assets ratio. For reasons

Requirement 2:

A firm’s creditworthiness represents its ability to repay its obligations

on a timely basis. Any information relevant to assessing that ability

should be considered in a determination of creditworthiness. Lease

obligations, whether treated as capital leases or operating leases

Standard and Poor’s describes the reasons it constructively

capitalizes leases as follows:

We view the accounting distinction between operating and

capital leases as substantially artificial. In both cases, the

leases, thereby:

enhancing comparability of operating and financial results

bringing financial ratios closer to the underlying economics

P5-9 Comparing profitability for three companies

Company A is Consolidated Edison. Public utilities are the most

capital intensive of the three industries. Consistent with the

significant investment in fixed assets, Company A has by far the

P5-10 Determining profitability

Note to the instructor: The following preliminary calculations provide

needed data for the remainder of the problem. Dollar amounts are

in millions.

2012 2013 2014

Average assets = (Beginning assets

Requirement 2:

Nucor experienced a slight ROA decline from 2012 to 2013. ROA

rebounded in 2014. Although some of the improved ROA in 2014

Requirement 3:

2012 2013 2014

ROCE (Net income/Average common

Note to the instructor: Nucor had no preferred stock outstanding and

Requirement 4:

Financial leverage “exaggerates” ROCE relative to ROA. That is,

P5-11 Business strategy and profit performance

Requirement 1:

Tiffany pursues a classic differentiation strategy: the particular

luxury items sold by Tiffany are simply not available elsewhere.

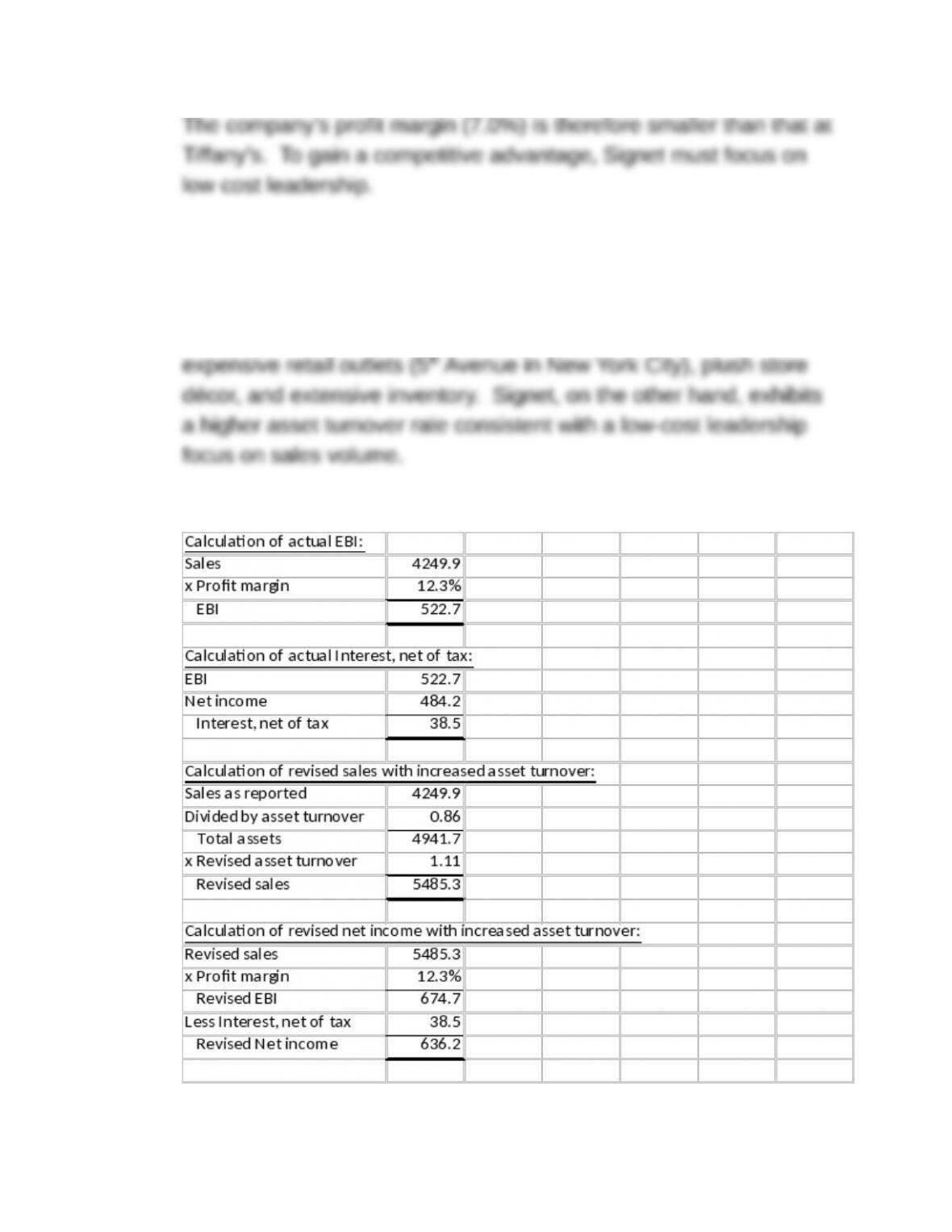

Requirement 2:

Tiffany generates $0.86 in sales for each asset dollar, compared to

$1.11 at Signet. This comparatively low asset turnover rate is

consistent with a Tiffany’s strategy of differentiation built around

Requirement 3:

Requirement 4:

To earn an ROA of 10.5% at the company’s current asset turnover

P5-12 Blockbuster Inc.

Requirement 1:

Cash provided by (used for) investing activities is a positive number

when the firm raises more cash from investment sales than it uses

Requirement 2:

Cash flow from operations in 2007 was -$56, and investing activities

only generated $77 million cash in that year. The cash used to pay

down debt by $329 million may have come from the company’s

Requirement 3:

Cash flow from operations in 2009 was again insufficient to cover

the company’s $846 million debt payment that year. So, the cash

Requirement 4:

The company must make sizable debt payments in each of the next

five years, but it has only generated modest cash from operations

P5-13 Analyzing why financial ratios change

(AICPA adapted)

Requirement 1:

Daley’s current liabilities are increased by the declaration of a cash

dividend. So, this transaction would reduce the current ratio.

unchanged.

Requirement 2:

Inventory increases and accounts receivable decrease. Assuming

the original transaction was profitable, the reduction in accounts

receivable exceeds the increase in inventory, thereby reducing

Requirement 3:

Current assets and current liabilities fall by equal amounts.

Because the current ratio exceeds 1, it will increase with the

Requirement 4:

Current assets increase, so the current ratio increases. There is no

change in inventory turnover. Because a loss is recorded, the