Financial Reporting and Analysis (7th Ed.)

Chapter 4 Solutions

Structure of the Balance Sheet and Cash Flow Statement

Cases

Cases

C4-1. Subsequent events

Event 1:

The loan, and the nature of the collateral, should be disclosed in the

notes to the financial statements. The loan would not be reflected in

Event 2:

The existence of the lawsuit should be disclosed in the notes to the

Event 3:

Disclosure of the bond issuance would be provided in the notes to the

Event 4:

Disclosure of the loss of inventory would be required in the notes to

the financial statements because this loss has a significant effect on

Event 5:

C4-2. Related party matters

Requirement 1: Review FASB ASC Topic 850: Related Party Disclosures

Requirement 2: Note to the instructor: Students were directed to the

4-1

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

13. Related Party Transactions

Adelphia currently manages cable television systems which are principally

owned by limited partnerships in which certain of Adelphia’s principal

shareholders who are executive officers have equity interests.

Adelphia has agreements with Olympus and the Managed Entities which

provide for the payment of fees to Adelphia. The aggregate fee revenues

from Olympus and the Managed Entities amounted to $2,022, $5,033 and

$34,905 for the nine months ended December 31, 1998 and the years ended

December 31, 1999 and 2000, respectively. In addition, Adelphia was

Interest expense – net includes interest income from affiliates for borrowings

At March 31, 1998, Adelphia had interest rate swaps with affiliates for a

notional amount of $175,000, which expired during the nine months ended

During the nine months ended December 31, 1998 and the years ended

December 31, 1999 and 2000, Adelphia paid $3,422, $11,227 and $15,864,

respectively, to entities owned by certain shareholders of Adelphia primarily

for property, plant and equipment.

Adelphia’s related party note does not adequately explain the extent of the

company’s related party payables and receivables. As the SEC notes,

Adelphia should have ensured – in accordance with FASB ASC Topic 850

(pre-Codification SFAS 57) – that the specifics of individual material related

Requirement 3:

4-2

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

Adelphia’s practice of offsetting related party payables and receivables—

besides being a GAAP violation—was significant in that it obscured the

extent and magnitude of self-dealing and assisted Adelphia in creating the

Note to the Instructor: Adelphia and the Rigases used the CMS as a

central “treasury function” for Adelphia, its subsidiaries, and the affiliated

Rigas Entities. Thousands of related party transactions went through the

CMS—a fact that was known to Adelphia’s auditor. The general ledger

system shared with Adelphia and its subsidiaries was structured into cost

Requirement 4:

There is a general presumption that transactions reflected in financial

statements were negotiated on an arm’s-length basis between

independent parties, both of whom are looking out for their own interests.

However, that presumption is not justified when related party transactions

C4-3. Analyzing international reporting

Requirement 1:

Some of the differences between Pittards’ balance sheet and those prepared

in accordance with U.S. GAAP are:

1. Pittards reports all amounts in pounds sterling.

4-3

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

2. Pittards uses a modified report form with liabilities deducted from assets

3. Fixed assets are presented before current assets. Accounts in both

4. Tangible fixed assets (which include land, buildings, plant machinery,

5. “Stocks” and “debtors” would be labeled as “inventory” and “accounts

8. “Profit and loss account” and what Pittard’s refers to as “own shares”

9. “Pension scheme” would be referred to as a “pension benefit obligation”

in the U.S. Note: Pittards operated two pension schemes until closing

10. Pittards presents a subtotal for “net current assets (liabilities)” and lists

11. The phrase noting approval by the board of directors that appears at the

12. Pittards presents both company and group balance sheets in

4-4

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

Requirement 2:

Note to the instructor: This balance sheet comparison exercise

As illustrated in the following table, both companies frequently use different

item.

Burberry Pittards

Typical U.S.

Balance Sheet

terminology

amounts falling

due within one

year

Bank overdrafts &

borrowings

Banks loans &

overdrafts

Notes payable

Trade & other

payables

Trade creditors Accounts payable

Non-current

liabilities

Creditors—

amounts falling

Long-term debt

Several other differences in presentation/format also exist between these

two balance sheets:

1. Unlike, Burberry, Pittards presents no “total assets” subtotal.

4-5

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

Requirement 3:

British balance sheets group assets and liabilities with similar characteristics

(e.g., Fixed assets, Capital and reserves) together. Netting liabilities against

C4-4. Bertha’s Bridal Boutique: Determining cash flow amounts from

comparative balance sheets and income statements

Requirement 1:

Cash collected during 2017 from accounts receivable is calculated

below.

Requirement 2:

To find cash payments during 2017 on accounts payable to suppliers,

we first must compute purchases.

We then use the purchases amount to compute cash payments made

to suppliers.

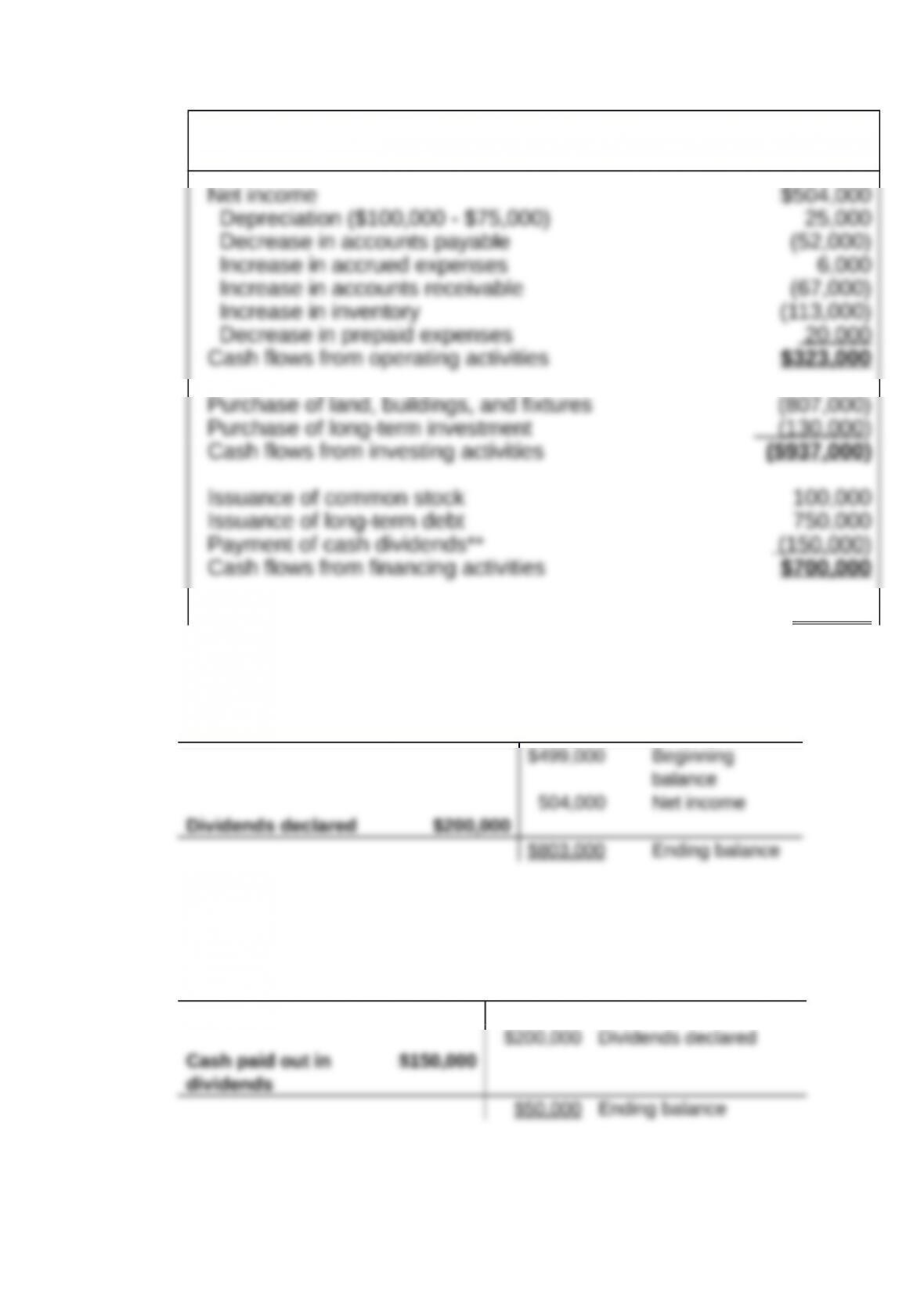

Requirements 3, 4, and 5:

4-6

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

Bertha’s Bridal Boutique

Statement of Cash Flows

Net cash flows for 2017 $86 ,000

**The amount listed for payment of cash dividends can be computed using

T-account analysis as follows:

Retained Earnings

Using the dividends declared amount we found above, we can find the

actual cash paid out for dividends by looking at the dividends payable

account.

Dividends payable

– Beginning balance

4-7

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

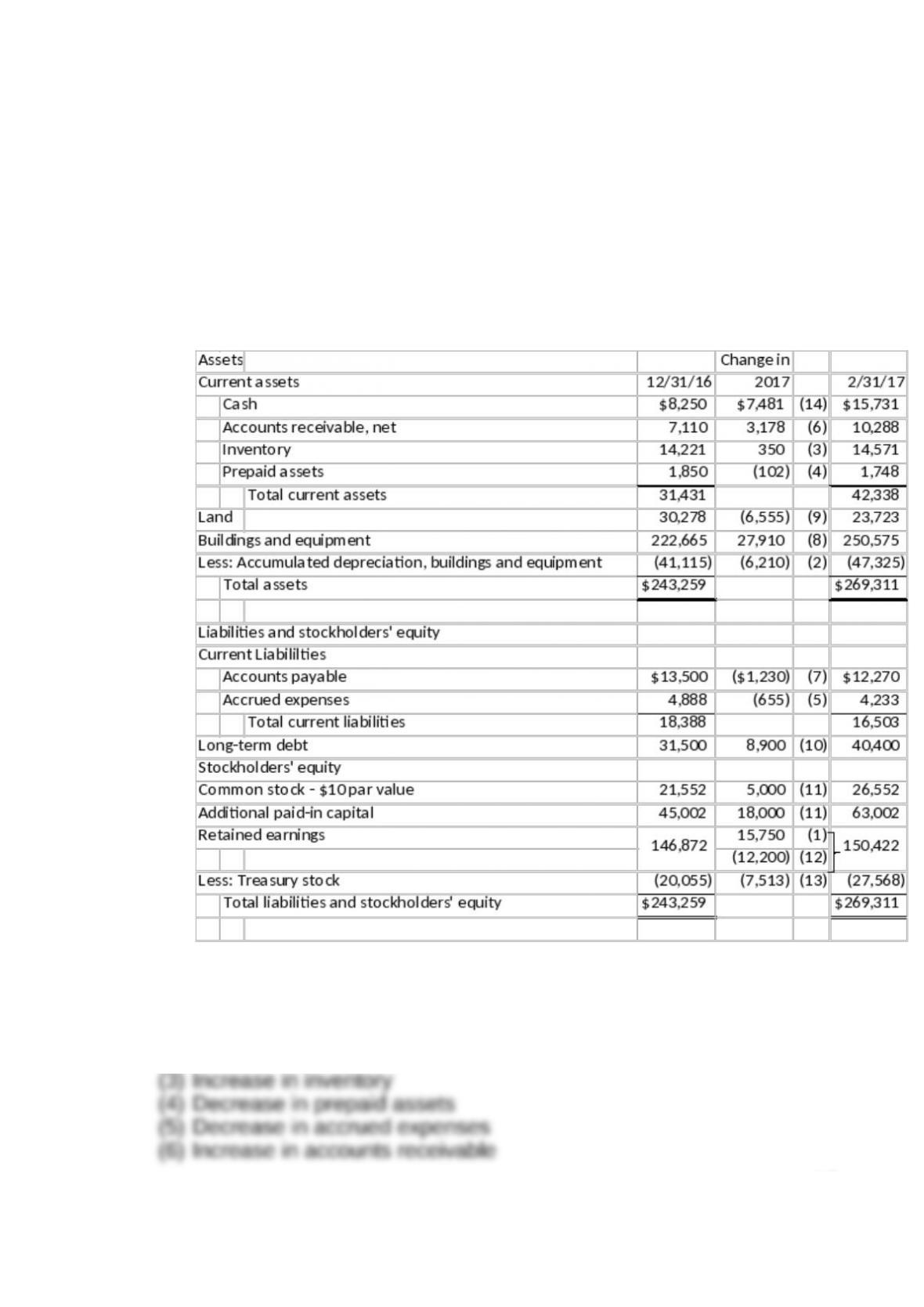

C4-5. Crash Zone Corp.: Understanding the relation between

successive balance sheets and cash flow statement

Amounts in the change column were obtained from the following cash

flow statement items:

(1) Net income

(2) Depreciation expense

4-8

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

(7) Decrease in accounts payable

(8) Purchase of equipment

(9) Proceeds from sale of land

(10) Issuance of long-term debt

4-9

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.