CHAPTER 11 Financial Instruments and Liabilities

Chapter 11

Financial Instruments and Liabilities

True-False

1. A liability that is satisfied through the payment of cash is referred to as a denominational lia-

bility.

2. A current monetary liability is shown on the financial statements at the undiscounted amount

due.

3. A product warranty provided with the sale of an item of merchandise gives rise to a nonmone-

tary liability.

4. Bonds are required by GAAP to be reported on the balance sheet at market value.

5. A rise in the market rate of interest will cause the value of a financial instrument such as a

bond to rise.

6. When market rates of interest increase, the use of floating-rate debt benefits the issuing com-

pany.

7. The retirement of a bond that has a $250,000 maturity value and a $10,000 balance in premi-

um on bonds payable (bond premium) creates a $15,000 gain if the bond is retired at a cost of

$245,000.

8. The gain or loss on the early retirement of a bond is the difference between the amount paid to

retire the bond and the bond’s carrying value at the date of retirement.

9. GAAP guidelines eliminate reporting income statement gains associated with many debt-for-

debt and debt-for-equity swaps and instead require disclosure of the effects of the swaps.

10. A debt-for-debt swap of debts with equal maturity values that occurs when the market rate of

interest is higher than the stated rate of the old debt will give rise to a gain on debt extinguishments.

11. When hedging commodity price risk with a futures contract, the value of the contract in-

creases as the selling price of the commodity increases.

12. A lender can effectively convert a fixed-rate debt into a floating-rate debt by using an interest

rate swap.

13. A call option contract requires the holder to buy a specific underlying asset at a set price dur-

ing a specific time period.

14. Changes in the fair value of all derivatives other than hedges must be recognized in income

when they occur.

15. IFRS allows the fair value accounting option for liabilities only to eliminate or significantly

reduce the “mismatch” that arises when different measurement bases are used for related finan-

cial instruments.

CHAPTER 11 Financial Instruments and Liabilities

Topic: IFRS―Debt

Multiple-Choice Questions

16. A probable future sacrifice of an economic benefit arising from a present obligation to transfer

assets or provide services to other entities in the future as a result of a past transaction is a/an

a. asset.

b. liability.

c. equity.

d. expense.

17. Which of the following is a correct statement about preparing a balance sheet?

a. All current liabilities must be due within the current calendar year.

b. Bonds payable are reported in long-term liabilities with the current year portion shown sepa-

rately in that section of the balance sheet.

c. Some financial instruments possess the characteristics of both debt and equity.

d. A financial instrument’s legal form will define how it is classified on the balance sheet.

18. Noncurrent monetary liabilities are initially recorded at their

a. future value.

b. historical value.

c. present value when incurred.

d. undiscounted amount due.

19. Which of the following would only be found in current liabilities on the balance sheet?

a. Derivative contracts.

b. Accrued compensation for services already rendered by employees.

c. Income tax liabilities.

d. Deferred revenue.

20. When the market rate of interest is below the stated rate of interest, a bond sells at

a. par.

b. a premium.

c. a discount.

d. stated value.

21. Strauss Company sold $100,000 of long-term bonds in the open market for $100,000. The

entry to record the transaction would be

a. DR Cash 100,000

CR Bonds payable 100,000

b. DR Bonds payable 100,000

CR Cash 100,000

c. DR Accounts payable 100,000

CR Bonds payable 100,000

CHAPTER 11 Financial Instruments and Liabilities

d. DR Cash 100,000

CR Interest payable 100,000

22. When the effective yield of a bond is the same as the stated rate on the bond, the bond is sold

at

a. a discount.

b. a premium.

c. par.

d. a price above par.

23. Theta Company has prepared to sell bonds with a stated rate of 6% when the market rate is

8%. These bonds will sell in the market at

a. par.

b. a discount.

c. a premium.

d. stated value.

24. Theta Company has prepared to sell bonds with a stated rate of 6% when the market rate is

5%. These bonds will sell in the market at

a. par.

b. a discount.

CHAPTER 11 Financial Instruments and Liabilities

c. a premium.

d. stated value.

25. When computing the issue price of a bond that has a stated rate of 8% payable semiannually

and a market rate of 10%, the discount rate used would be

a. 8%.

b. 10%.

c. 4%.

d. 5%.

26. Amortization of discount on bonds payable (bond discount) results in which of the follow-

ing?

a. A decrease in bond interest expense.

b. An increase in net income.

c. An increase in the carrying value of the bond.

d. An increase in stockholders’ equity due to the decrease in bond interest expense.

27. Generally accepted accounting principles require that when bonds are sold at a discount, the

discount must be allocated to interest expense using the

a. cash interest method.

b. effective interest method.

CHAPTER 11 Financial Instruments and Liabilities

c. bond yield method.

d. cumulative interest method.

28. Baker Company issued $200,000 of ten-year bonds to yield 11% when the stated rate of the

bonds was 9%. Present value interest factors (PVIF) are:

9% 11%

PVIF of $1, 10 years 0.42241 0.35218

PVIF of Annuity of $1, 10 years 6.41766 5.88923

The entry to record the bond issuance would be

a. DR Cash 176,442

DR Bond premium 23,558

CR Bonds payable 200,000

b. DR Cash 176,442

DR Bond discount 23,558

CR Bonds payable 200,000

c. DR Cash 223,558

CR Bond premium 23,558

CR Bonds payable 200,000

d. DR Cash 223,558

CR Bond discount 23,558

CR Bonds payable 200,000

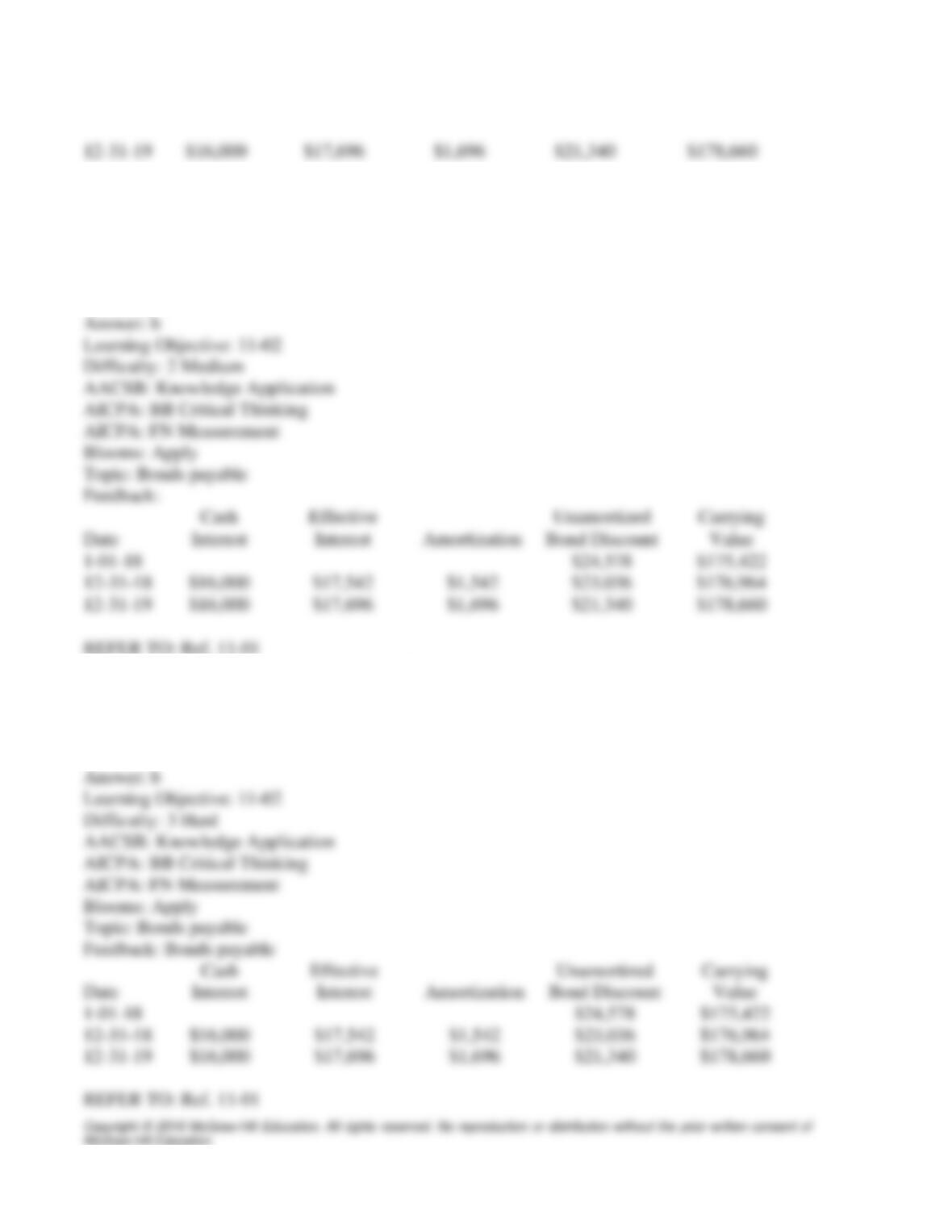

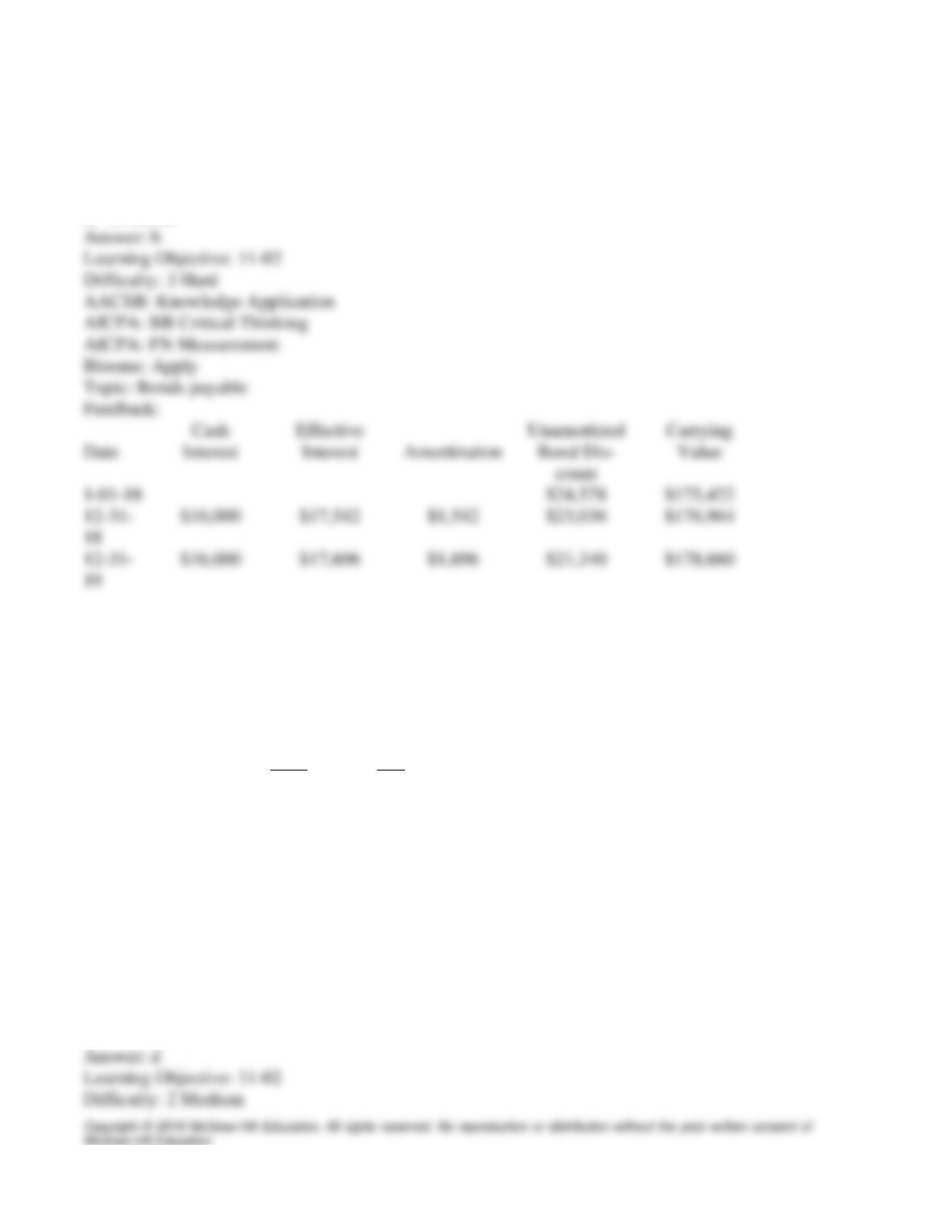

29. The bond carrying amount at the end of 2018 is

a. $175,422.

b. $176,964.

c. $200,000.

d. $201,542.

30. The bond interest expense for 2018 is

a. $16,000.

b. $17,542.

c. $20,000.

d. $21,542.

CHAPTER 11 Financial Instruments and Liabilities

REFER TO: Ref. 11-01

31. The amount of cash interest paid in 2018 on the bonds is

a. $14,458.

b. $16,000.

c. $17,542.

d. $20,000.

32. The bond carrying value at the end of 2019 is

a. $175,422.

b. $178,660.

c. $200,000.

d. $203,238.

33. The amount of bond discount amortization for 2019 is

a. $1,696.

b. $2,458.

c. $3,080.

d. $4,000.

34. The amount of cash interest paid in 2019 is

a. $16,000.

b. $18,000.

c. $19,080.

d. $20,000.

35. The amount of bond interest expense for 2019 is

CHAPTER 11 Financial Instruments and Liabilities

a. $16,000.

b. $17,696.

c. $18,458.

d. $19,280.

Use the following to answer questions 36 – 42:

REFERENCE: Ref. 11_02

The Ness Company sells $5,000,000 of five-year, 10% bonds at the start of the year. The bonds

have an effective yield of 9%. Present value factors are below:

10% 9%

PV $1 factor 1 year 0.90909 0.91743

PV $1 factor 2 years 0.82645 0.84168

PV $1 factor 3 years 0.75131 0.77218

PV $1 factor 4 years 0.68301 0.70843

PV $1 factor 5 years 0.62092 0.64993

REFER TO: Ref. 11_02

36. The bonds will sell for

a. $4,805,525.

b. $5,000,000.

c. $5,050,000.

d. $5,194,475.

37. The bond interest expense for Year 1 is

a. $467,503.

b. $500,000.

c. $532,497.

d. $538,895.

38. The amount of cash interest paid in Year 1 on the bonds is

a. $450,000.

b. $467,503.

c. $500,000.

d. $538,895.

39. The bond carrying value at the end of Year 1 is

a. $4,500,000.

b. $5,000,000.

c. $5,126,556.

d. $5,161,978.

40. The amount of bond premium amortization for Year 2 is

a. $32,497.

b. $35,422.

c. $38,895.

d. $50,000.

41. The bond carrying value at the end of Year 2 is

a. $4,805,525.

b. $5,000,000.

c. $5,126,556.

d. $5,194,475.

42. The amount of bond interest expense for Year 2 is

a. $450,000.

b. $464,578.

c. $500,000.

d. $535,422.

43. A bond with a maturity value of $700,000 was initially issued for $715,000. The bond has a

ten-year life and a stated interest rate of 10%. The total interest expense over the life of the bond

is

a. $700,000

b. $715,000

c. $685,000

d. not determinable without knowing the bond’s effective yield.

44. On January 1, 2018 when the effective interest rate was 14%, a company issued bonds with a

maturity value of $1,000,000. The stated rate of interest is 12%, the bonds pay interest semi-

annually and sold for $893,640. The amount of bond discount amortized on July 1, 2018 is ap-

proximately

a. $1,000

b. $2,555

c. $2,000

d. $5,110

45. Which of the following statements is correct?

a. Amortization of discount on bonds payable (bond discount) results in an increase in a

bond’s carrying value.

b. Amortization of discount on bonds payable (bond discount) results in a decrease in bond

interest expense.

c. Amortization of premium on bonds payable (bond premium) results in an increase in a

bond’s carrying value.

d. Amortization of premium on bonds payable (bond premium) results in an increase in bond

interest expense.

46. When a bond is sold at a discount the effective interest rate is

a. equal to the stated rate.

b. above the stated rate.

c. below the stated rate.

d. equal to the stated rate for a period of time and then above the stated rate for a period of

time.

47. Which of the following statements is not correct regarding amortization when using the ef-

fective interest method (basis)?

a. Amortization of discount on bonds payable (bond discount) increases in later years relative

to earlier years of a bond’s life.

b. Amortization of premium on bonds payable (bond premium) increases in later years rela-

tive to earlier years of a bond’s life.

c. Amortization of both premium on bonds payable (bond premium) and discount on bonds

payable (bond discount) decreases in later years relative to earlier years of a bonds life.

CHAPTER 11 Financial Instruments and Liabilities

d. Amortization of discount on bonds payable (bond discount) results in an increase in interest

expense and in an increase in the bond’s carrying value.

48. When a bond is sold at a premium the

a. effective interest rate is less than the stated rate.

b. effective interest rate is greater than the stated rate.

c. effective interest rate relative to the stated rate is not known.

d. interest expense during the life of the bond exceeds the amount of cash interest payments

during the life of the bond.

49. Floating-rate debt is the most common method for lenders to protect themselves from losses

that may arise as a result of

a. increases in the market interest rate.

b. decreases in the market interest rate.

c. increases in the stated interest rate on bonds.

d. decreases in the stated rate on bonds.

50. The market value of floating-rate debt of $200,000 will

a. rise by $2,000 with a 1% rise in interest rates.

b. fall by $2,000 with a 1% fall in interest rates.

c. remain unchanged with a change in interest rates.

CHAPTER 11 Financial Instruments and Liabilities

d. will rise in the short run and fall in the long run with a change in interest rates.

51. Which of the following statements with respect to floating-rate debt is incorrect?

a. If the market rate of interest increases, the market value of the floating-rate debt will re-

main the same.

b. If the market rate of interest decreases, the cash interest payment required by the issuing

company would decrease.

c. If the market rate of interest increases, the investors benefit while the issuing corporation

does not benefit.

d. If the market rate of interest decreases, both the issuing company and the investors benefit.

52. When market rates of interest decrease, the use of floating-rate debt benefits

a. investors.

b. issuing companies.

c. all parties.

d. no one.