Financial Reporting and Analysis (7th Ed.)

Chapter 16 Solutions

Intercorporate Investments

Exercises

Exercises

E16-1. Accounting for trading and available-for-sale securities

(AICPA adapted)

Requirement 1:

Only the unrealized holding gains/losses from trading securities are recognized as income.

from 12/31/16 to 12/31/17 = $155,000 – $100,000 = $55,000.

Requirement 2:

Any unrealized gain or loss for the year on Tyne’s available-for-sale securities should be recorded

$150,000 original cost).

Note the distinction between OCI and AOCI. The “A” stands for “accumulated.” So, while OCI

represents comprehensive income (changes in equity not due to transactions with owners) that are

accumulation of retained net income.

E16-2. Accounting for minority-passive equity investments under new rules

(AICPA Adapted)

Requirement 1:

Note that these facts are identical to those in E16-1. However, the date in this problem puts it

gain in 2020.

The gain during the year on Alpha was $155,000-$100,000 = $55,000 and the gain on Beta was

Requirement 2:

16-1

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

The issue here is how the transition from the old rules to the new ones is handled. Although there

earnings. As a result, there is no AOCI related to Tyne’s equity investments reported at December

31, 2020.

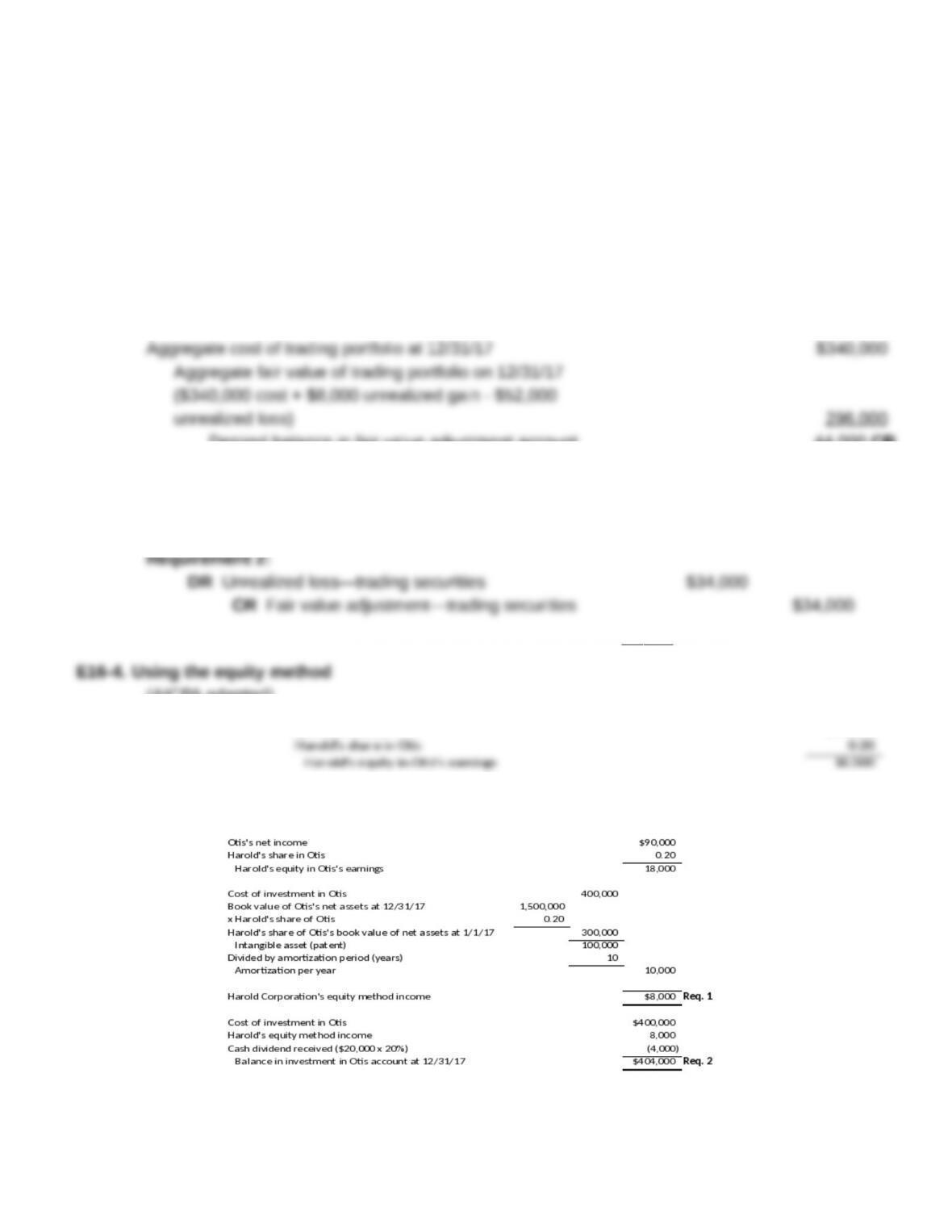

E16-3. Accounting for trading securities

Requirement 1:

Aggregate cost of trading portfolio at 12/31/17 $340,000

Balance prior to adjustment 10 ,000 CR

Requirement 2:

DR Unrealized loss—trading securities $34,000

E16-4. Using the equity method

(AICPA adapted)

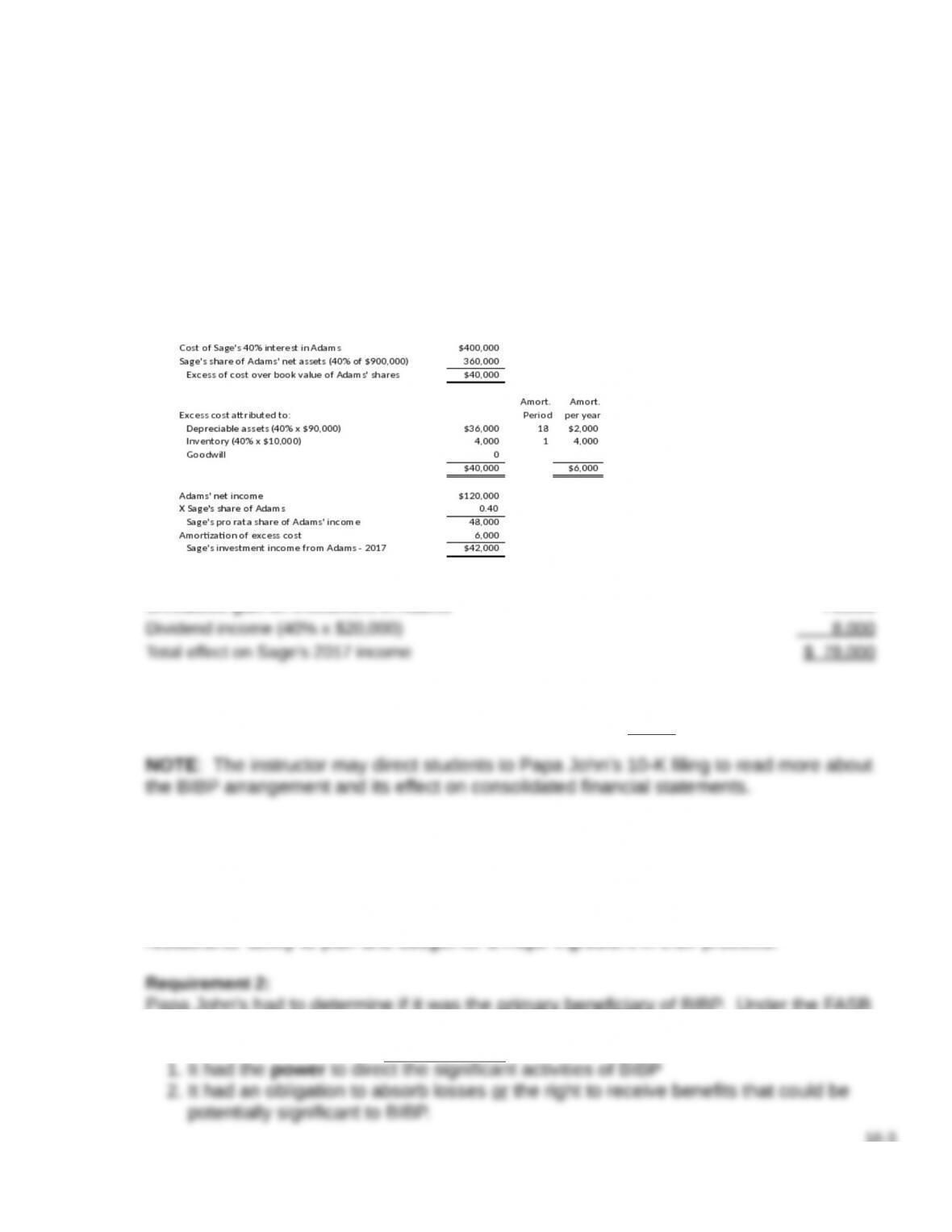

E16-5. Using the equity method and fair value option

(AICPA adapted)

16-2

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

Requirement 1:

Requirement 2:

Sage’s initial investment in Adams $400,000

Requirement 3:

Fair value of Sage’s investment in Adams on 12/31/17 $470,000

Fair value of Sage’s investment in Adams on 1/2/2017 400,000

E16-6. Determining business rationale and whether to consolidate a VIE; Intra-entity

sales

NOTE: The instructor may direct students to Papa John’s 10-K filing to read more about

the BIBP arrangement and its effect on consolidated financial statements.

Requirement 1:

According to the note disclosure, the purchasing arrangement through BIBP was designed

restaurants’ ability to plan and budget for a major ingredient in their products.

Requirement 2:

Papa John’s had to determine if it was the primary beneficiary of BIBP. Under the FASB

potentially significant to BIBP.

16-3

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

In its 2012 10-K filing, Papa John’s indicated that it was the primary beneficiary of BIBP,

and therefore BIBP is included in Papa John’s consolidated financial statements.

Requirement 3:

included in Inventory must be eliminated.

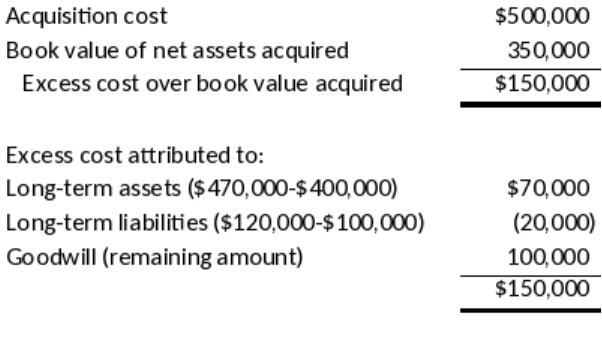

E16-7. Determining the value of goodwill

Acquisition cost of Shake’s stock $4,000,000 ($20 x 200,000)

E16-8. Goodwill–acquisition method

(AICPA adapted)

*Identifiable net assets excludes goodwill.

E16-9. Preparing consolidated financial statements

(AICPA adapted)

Beginning retained earnings (Pitt Company) $500,000

Ending retained earnings $650 ,000

Note that Saxe’s amounts need not be considered explicitly because Pitt’s consolidated results

include Saxe’s.

E16-10. Determining consolidated retained earnings

Pack will report Retained Earnings of $780,000 in its December 31, 2017 consolidated balance

16-4

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

E16-11. Consolidated balances using the acquisition method

Following is Sea Company’s consolidation worksheet immediately after the acquisition of Island

Company:

Sea Island

Eliminations Consolidated

Dr Cr Balance Sheet

Assets

Other assets $ 750,000

$

320,000 $15,000 B $1,095,000

10,000 C

Stockholders’

Equity

Common stock

450,00

0

200,00

0 200,000 A 450,000

230,00

Requirement 1:

Imputed full fair value of the acquisition $300,000 ($180,000/.6)

Island’s acquisition date book value (250,000)

50,000

16-5

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

The consolidated total assets will be $1,120,000, as shown in the consolidation worksheet. This

amount consists of:

$750,000 of Sea Company assets other than the investment in Island Company

Requirement 2:

Under the acquisition method, noncontrolling interest is based on the $180,000/.6 = $300,000

E16-12. Recording transaction foreign exchange gain/loss

(AICPA adapted)

Requirement 1:

2017:

12/31/17 balance of receivable in dollars

Requirement 2:

2018:

Dollar amount received on 2/1/18

Foreign currency gain in 2018 $12 ,500

E16-13. Accounting for available-for-sale securities

(AICPA adapted)

Journal entry:

DR OCI–unrealized loss in fair value on

available-for-sale securities $20,500

CR Fair value adjustment–available-for-sale securities $20,500

16-6

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

E16-14. Fair value accounting for trading securities

Equity 12/31/18 Unrealized

Security Cost Fair Value gain/(loss)

($14 ,000)

Therefore, the Fair value adjustment account must have a $14,000 credit balance at December

31, 2018. The following analysis shows that given this ending balance and the activity in the

account in 2018, the December 31, 2017 balance must have been $18,000.

Fair Value Adjustment – trading securities

E16-15. Consolidating sales and cost of goods sold with intra-entity transactions

Requirement 1:

Pate recorded $600,000 in sales revenue when it sold goods to Strange. Consolidated sales

be reported at $2,700,000 + $1,600,000 – $600,000 = $3,700,000.

Requirement 2:

Pate recorded $400,000 in cost of sales when it sold to goods Strange. Strange recorded

at $1,800,000 + $900,000 – $600,000 = $2,100,000.

E16-16. Comparison of acquisition versus pooling method

Requirement 1 (Acquisition Method):

The investment is recorded at fair value under the acquisition method.

16-7

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

Requirement 2 (Acquisition Method):

16-8

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

Requirement 2 (continued):

Pushway Stroker

Eliminations Consolidated

Dr Cr Balance Sheet

Assets

Current assets $ 300,000 $ 100,000 $ 400,000

Long term liabilities 250,000 100,000 20,000 B 370,000

Total liabilities 450,000 150,000 620,000 (b)

Note: Answers (a), (b), and (c) are keyed above.

16-9

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education.

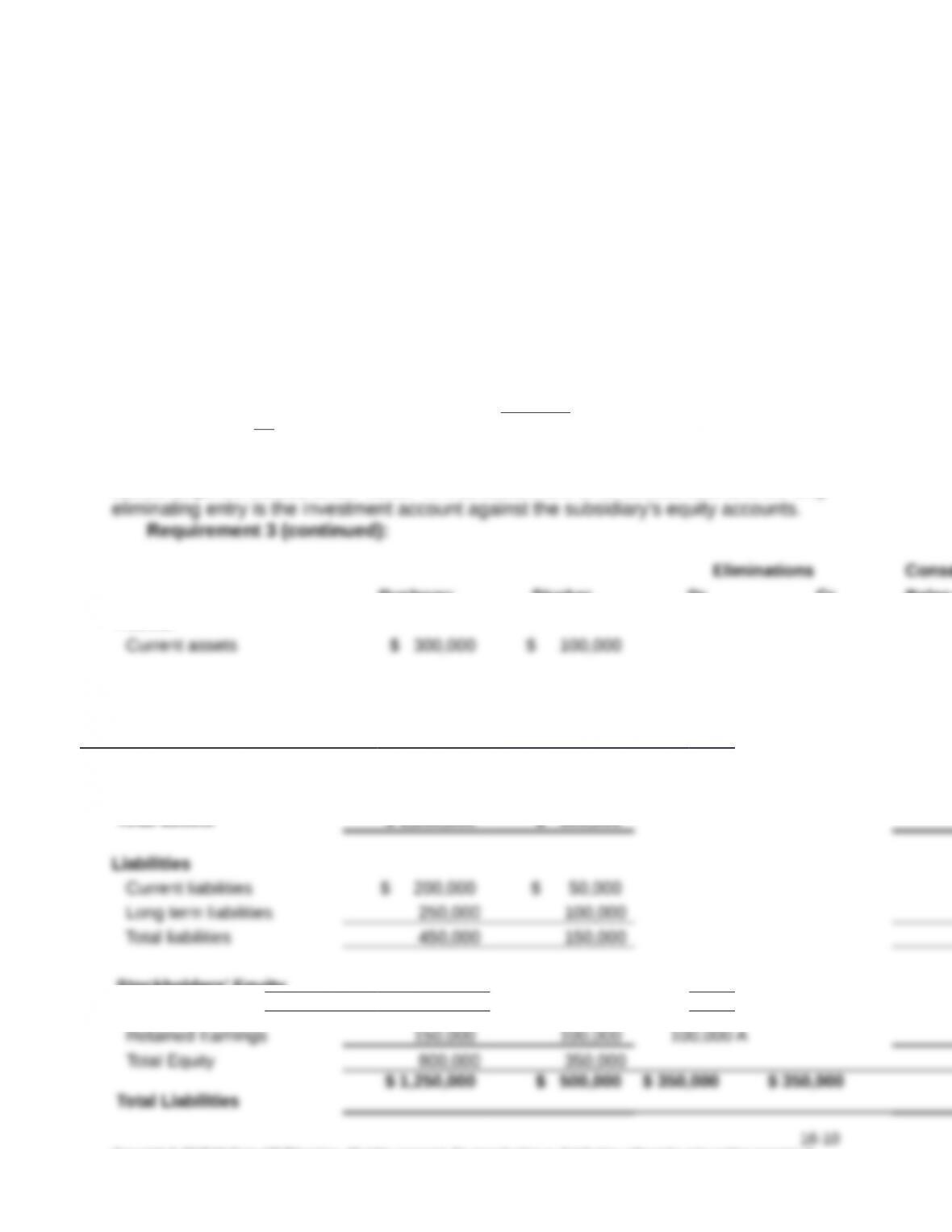

Requirement 3 (Pooling Method):

The acquisition journal entry under pooling would be at Stroker’s book value:

DR Investment in Stroker $350,000

CR Common Stock $350,000

Under the pooling method, the acquisition “cost” is the book value acquired and

equal to the parent company’s total equity ($800,000).

A consolidating worksheet was not required for this problem, but one is provided so you

eliminating entry is the investment account against the subsidiary’s equity accounts.

Requirement 3 (continued):

Pushway Stroker

Eliminations Consolidated

Dr Cr Balance Sheet

Assets

Current assets $ 300,000 $ 100,000

Long term assets 600,000 400,000

Long term liabilities 250,000 100,000

Total liabilities 450,000 150,000

16-10

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

and Equity

Note: Answers (a), (b), and (c) are keyed above.

16-11

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.