P11-17. Unconditional purchase obligations (LO 11-6, LO

11-9)

Requirement 1:

The following schedule shows the present value computation

using an 8% discount rate:

Year

Purchase

commitment Present

value factor

Present value

amount

Requirement 2:

Using the amounts now shown on the balance sheet, the

3.33

If the unconditional purchase obligation contracts were included on

the balance sheet with the company’s other long-term debt, total

4.69

Requirement 3:

Under current GAAP, contracts of this sort are not booked because

neither party is viewed as having taken any action—no cash or

property has yet been exchanged, there is just a promise to do so

in the future. Some companies prefer this approach because it

P11-18. Loss contingencies (LO 11-9)

Requirement 1:

A loss contingency is an event that results in the possibility of

future loss. A primary example of a loss contingency is litigation.

Loss contingencies can be disclosed either by recognizing a

Loss contingencies are included in the financial statements

because the event will possibly cause future loss. That is, the

The Exxon and Borden illustrations are examples of loss

contingencies. A loss contingency meets GAAP guidelines for

Requirement 2:

GAAP states that a loss contingency shall be accrued if it is (1)

probable and (2) the amount of the loss can be reasonably

Requirement 3:

There are several reasons why Exxon does not report a dollar

amount for the loss contingency. First, while a liability clearly

exists, a reasonable estimate of the amount of the liability may not

be possible. Second, even if Exxon could reasonably estimate the

liability, it may be hesitant to disclose the estimate because doing

Stock analysts are unlikely to ignore the loss contingency when

valuing Exxon. Analysts realize that a significant loss has occurred

even if the company does not place a specific dollar amount on the

Requirement 4:

Exxon first reported a balance sheet liability for the Exxon Valdez

spill in 1996, once the court entered the $5.058 billion judgment

Requirement 5:

The Court’s willingness to hear the Exxon appeal will have no

impact on the company’s recorded contingent liability. If and when

Requirement 6:

As the company states in its financial statement note, Visa

recognizes a litigation loss contingency provision when it deems

the loss to be probable and the amount can be reasonably

estimated. When the litigation process is itself quite lengthy, Visa

Requirement 7:

As explained in the company’s financial statement footnote, a $4.1

billion increase to the accrued litigation liability was recorded in

P11-19. Debt-for-debt swaps (LO 11-4, LO 11-10)

Requirement 1:

Since the bonds were originally sold at par, the carrying amount on

December 31, 2017 is equal to $5,000,000. If this bond issued

were retired in exchange for a bond issue valued at $3,200,000

there would be a pre-tax gain of $1,800,000. The journal entry to

record the exchange would be:

Requirement 3:

Requirement 4:

Other ways to avoid the covenant’s violation include: issue

additional common stock, reissue any treasury stock that is being

Requirement 5:

IFRS guidance stipulates that an exchange of financial instruments

qualifies as an extinguishment of debt only if the terms—stated

interest rate, duration, payment schedule, etc.—of the instruments

are “substantially” different. Absent substantial differences in

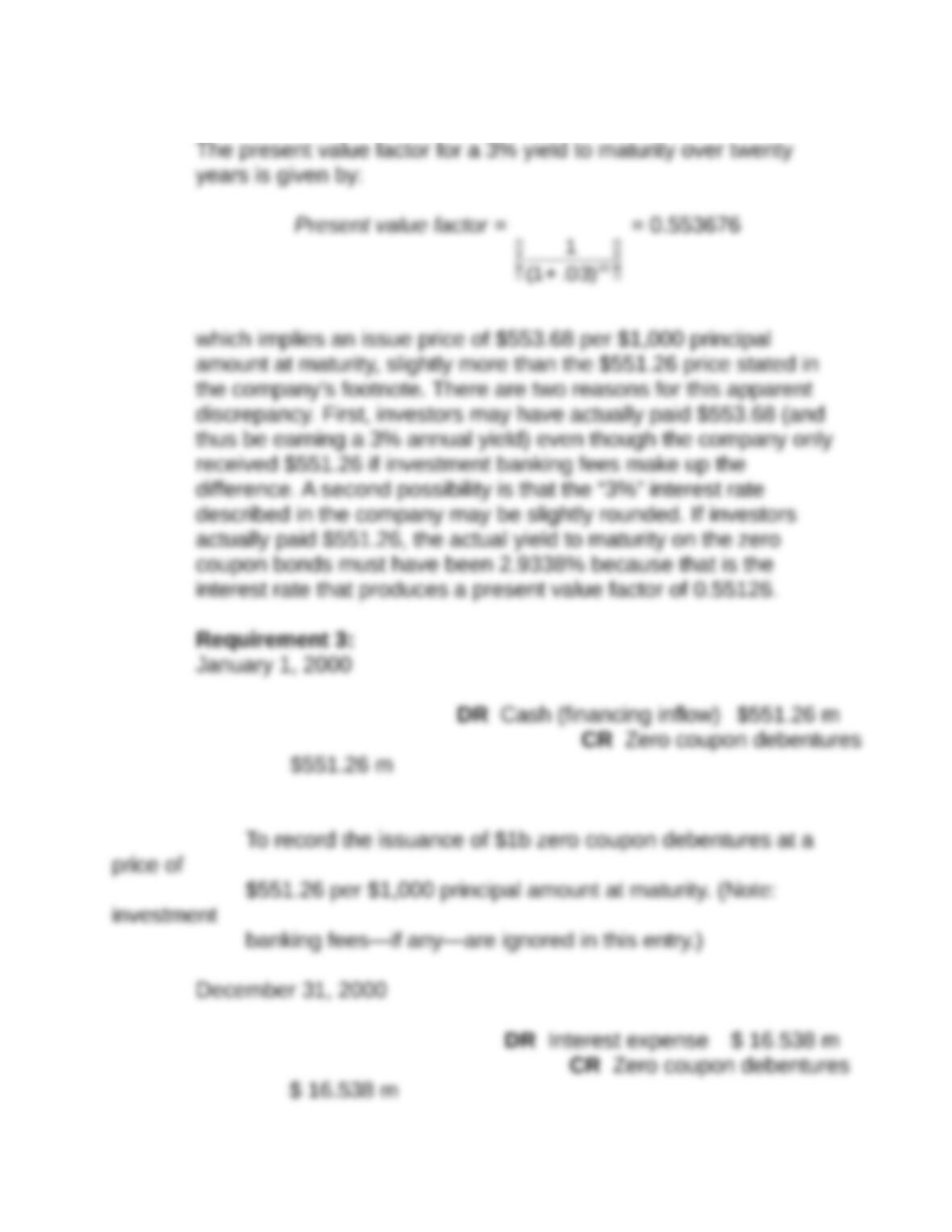

P11-20. Zero coupon bonds (LO 11-2)

Requirement 1:

ALZA issued $1.0 billion maturity value zero coupon debentures at

Requirement 2:

To record interest expense for the year at a 3% effective

interest rate.

Requirement 4:

Interest rates throughout the economy have declined, making

ALZA’s 3% zero coupon debentures even more attractive to

investors who then bid up the price of the company’s debt.

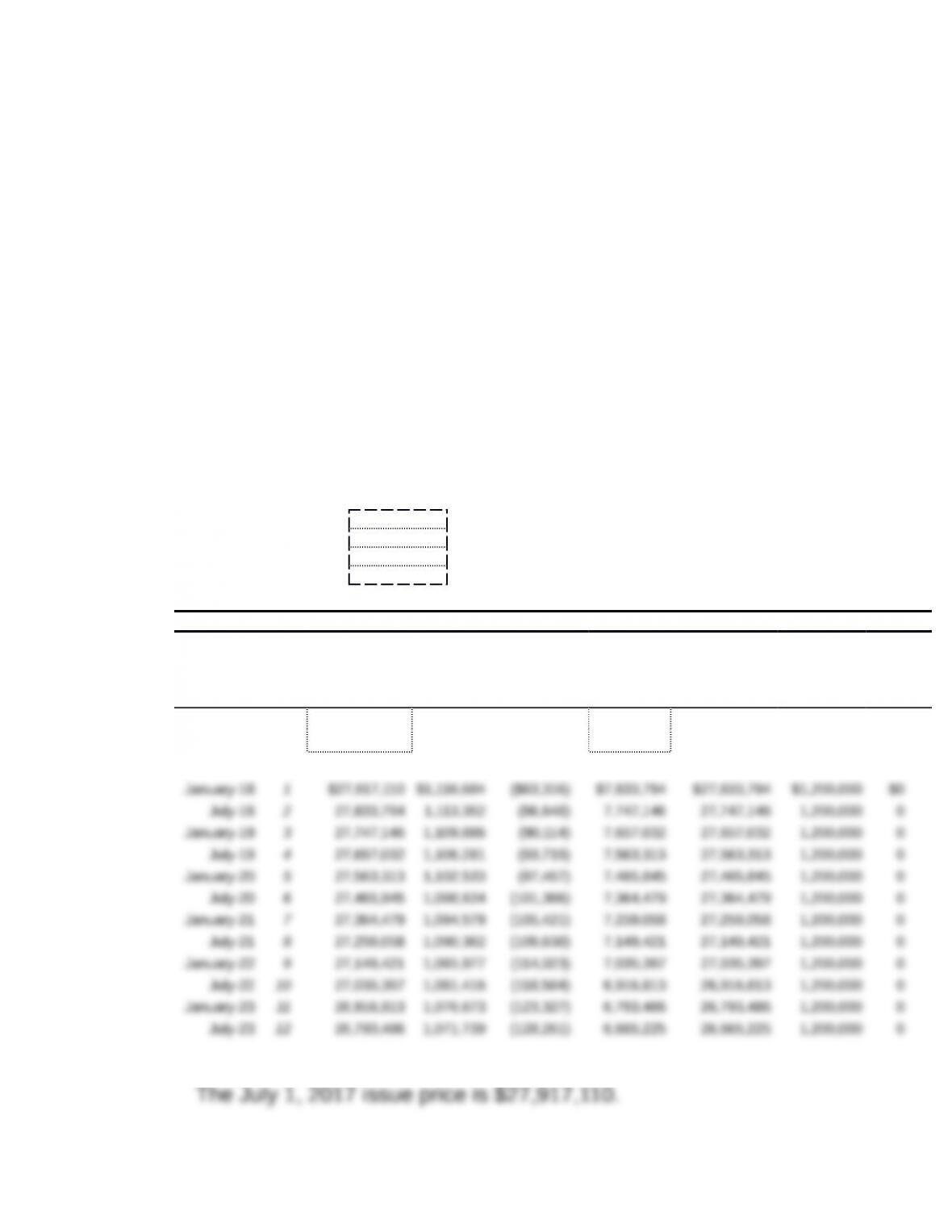

P11-21. Comprehensive problem on premium bond (LO 11-2)

The following schedule shows the details for most parts of this

question.

Amortization table for 20-year bond with semi-annual interest

payments

Bond Principal $20,000,000

Coupon Interest Rate 6.0%

Market Interest Rate 4.0%

Month and Year Issued July-17

Amortization Table

Month/Year Period

Bond Carrying

Amount at

Start of Period

Interest

Expense

Bond

(Premium)

Discount

Amortization

Premium

(Discount)

Balance

Bond Carrying

Amount at

End of Period

Cost

Interest

Payment

Principal

Payment

Issue date: $27,917,110 $7,917,110

Requirement 1:

Requirement 2:

Requirement 3:

The entry for December 31, 2018 is:

Requirement 4:

Points to be made include: the company received $27.9 million

cash in exchange for a promise to repay on $20 million in principal

and $2.4 million in interest each year; because more than $20

million was received, the true interest rate is less than 6% each

Requirement 5:

Deere will not record the guarantee as a liability on its financial

Requirement 6:

From the amortization schedule in Requirement 1, we can see that

the book value of the entire debt issue is $26,793,486 on July 1,

Requirement 7:

If the market yield on the debt is 10%, its market price would be

$23,074,490 and 40% of the debt would have a market value of

P11-22. Hedging a Purchase

Commitment (LO 11-7, LO 11-8)

Requirement 1:

Silverado must give the supplier a six-month advance commitment

for titanium purchases at a fixed price, but the company does not

want to forego the possibility that titanium prices will decline over

the period. So, the company enters into a forward contract to sell

Was it a good idea? Yes, in this case, because titanium prices fell

to $285 per pound by June 30.

Requirement 2:

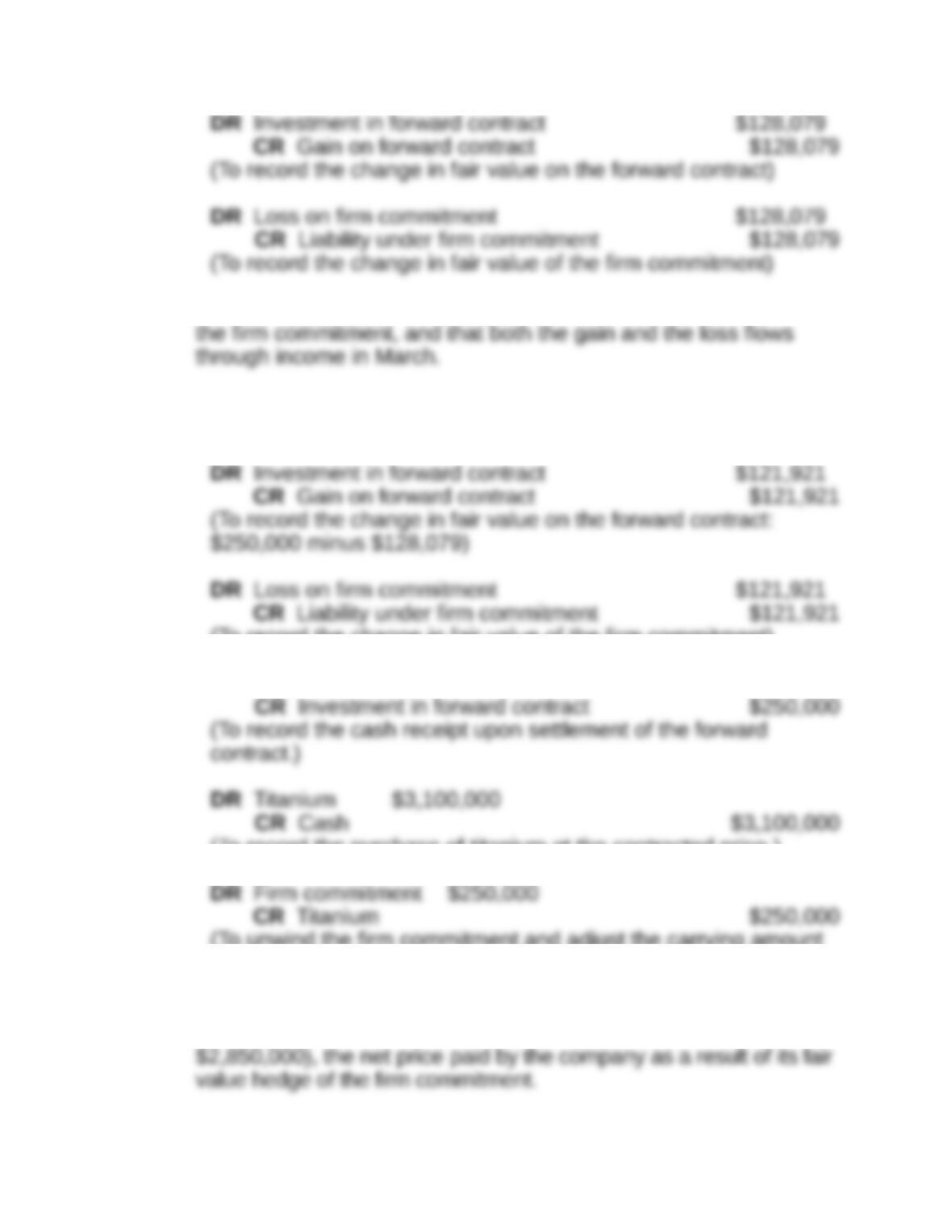

Requirement 3:

The following entries are made on March 31:

Notice that the gain on the forward contract is offset by the loss on

Requirement 4:

The following entries are made on June 30:

(To record the change in fair value of the firm commitment)

DR Cash $250,000

(To record the purchase of titanium at the contracted price.)

(To unwind the firm commitment and adjust the carrying amount

of the titanium purchase.)

Notice that titanium inventory is now on the books at June 30

market price of $285 per pound ($3,100,000 minus $250,000 =