Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

P9-11. Evaluating inventory cost-flow changes (LO 4)

Requirement 1:

“Better matching of revenues and expenses . . .”

Matching does not refer to the physical flow of goods, but rather

to cost-flow assumptions.

“Better correlation of accounting and financial information . . .”

“Better presentation of inventories . . .”

LIFO provides more information because of the requirement to

disclose LIFO reserve.

Under specific identification, financial statement users will not

Requirement 2:

“Conform all inventories . . . to the same method of valuation.”

This would simplify the analyst’s task.

“Reflects more recent costs in the balance sheet . . .”

If input costs are changing, the average cost method will reflect

© 2018 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for

sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or

posted on a website, in whole or part. 9-1

“Better matching of current costs with current revenues . . .”

If the company expects to reduce its inventory levels, LIFO

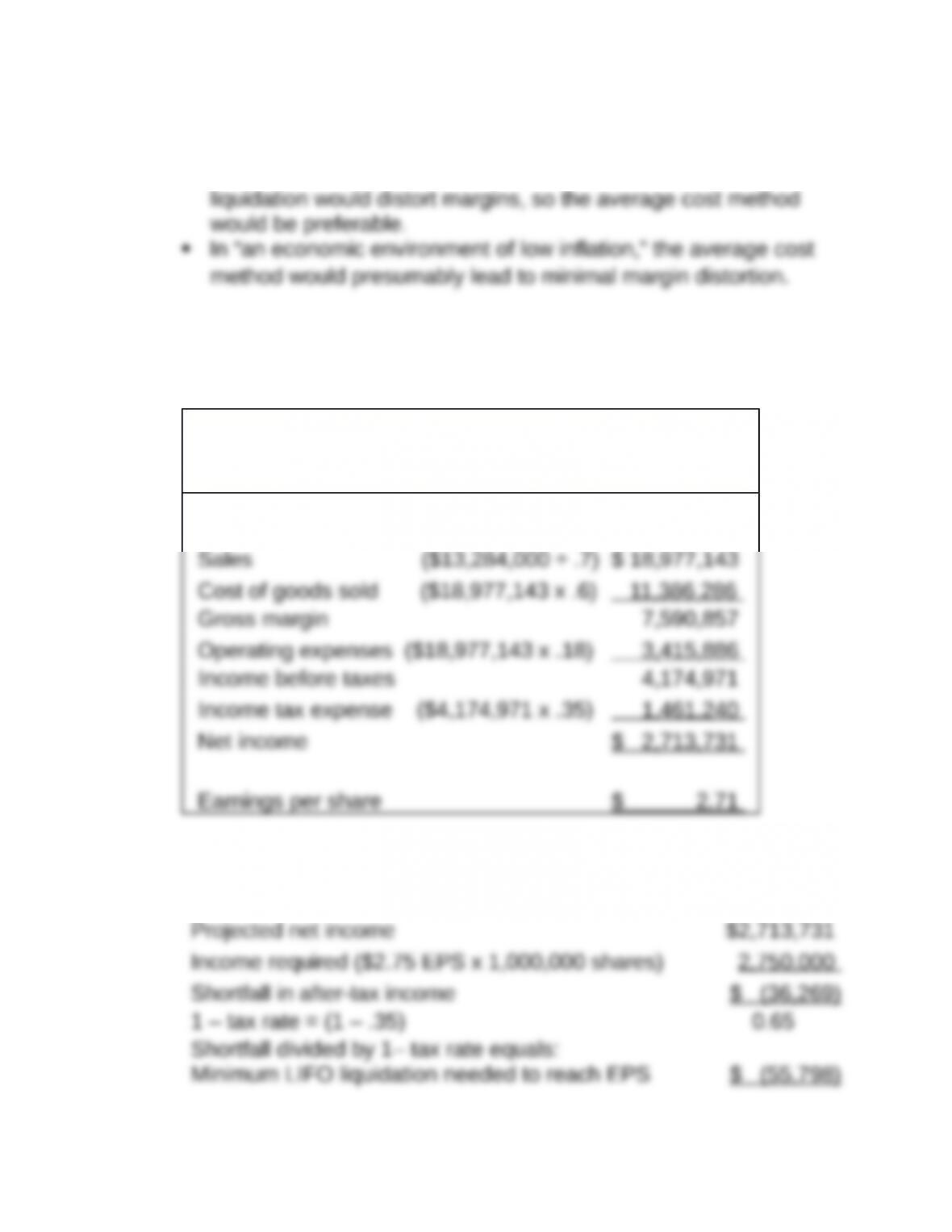

P9-12. Assessing managerial opportunism (LO 6, 9)

Requirement 1:

JKW Corporation

Projected Income Statement

For the Year Ended December 31, 2017

Projected

Income

Requirement 2:

© 2018 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for

sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or

posted on a website, in whole or part. 9-2

target

P9-13. Computing LIFO and ratio effects (LO 1, 3, 5, and 6)

Requirement 1:

Cost of goods manufactured:

Finished goods

= $65,638

Finished goods inventory turnover:

Cost of goods sold

Average finished goods inventory

=

$65,374

0.5($2,684 $2,420)

= 25.62

365

25.62

= 14.25 days

Work-in-process inventory turnover:

Cost of goods manufactured

Average work-in - process inventory

=

$65,638

0.5($40,285 $39,921)

= 1.64

365

1.64

= 223 days

Comments:

© 2018 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for

sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or

posted on a website, in whole or part. 9-3

Yes. We know that Bacardi ages its rum for 1–3 years, so we would

expect work-in-process turnover to be slow. (In fact, 223 days is

Requirement 2:

FIFO income (estimate):

FIFO net income = LIFO net income + Change in LIFO reserve

(1 - tax rate*)

* Tax rate = 17% per information given in the question.

Comments:

The substantial drop in the LIFO reserve indicates that the price of

molasses (the major component of raw materials inventory) has

Requirement 3:

Inventory turnover ratio (in days):

LIFO cost of goods sold Pre-tax liquidation

Avg. LIFO inventory Avg. LIFO reserve

=

$65,374 - $1,400* /(1 - 0.17)

0.5($53,812 $20,800 $51,892 $700)

$63,687

$63,602

= 1.001

© 2018 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for

sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or

posted on a website, in whole or part. 9-4

365

1.001

= 364.5 days

* Recall that liquidation caused a decrease in net income.

Comments:

This total turnover measure should reflect the entire conversion

process from purchase of raw materials through manufacture and

above is less than the 1- to 3-year aging schedule disclosed in

One possible reason for this apparent discrepancy is the equal

weight given to beginning and ending LIFO reserves in the

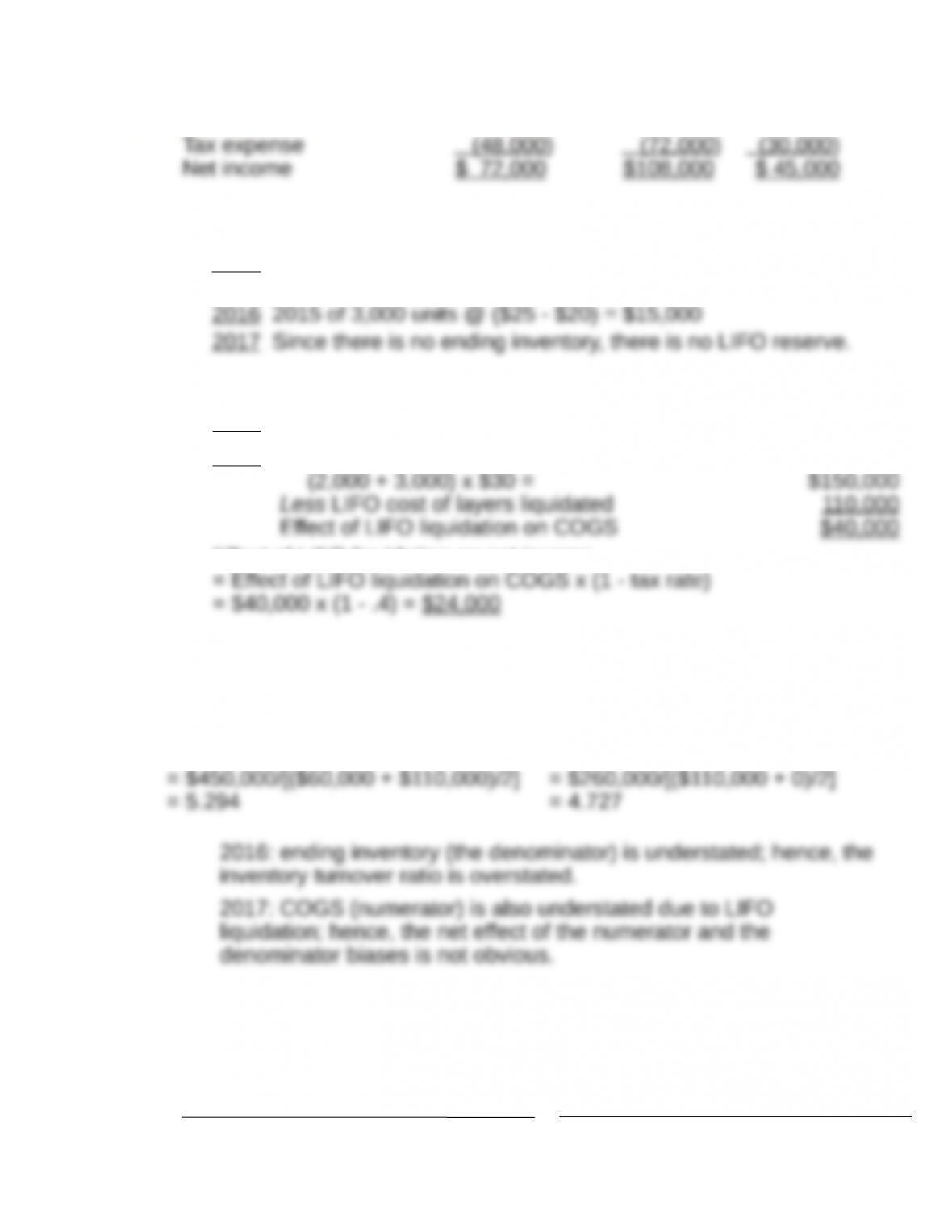

P9-14. Determining LIFO amounts—comprehensive (LO 5, 6, 7)

Requirement 1:

Year Cost of goods sold Ending inventory

2016

18,000 units x $25 =

$450,000

2,000 units x $25 =

$50 ,000

3,000 units x $20 =

$60 ,000

$110 ,000

2017

5,000 units x $30 =

$150,000

0

2,000 units x $25 =

$50,000

3,000 units x $20 =

$60,000

$260,000

Requirement 2:

Income statements 2015 2016 2017

© 2018 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for

sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or

posted on a website, in whole or part. 9-5

Pre-tax income 120,000 180,000 75,000

Requirement 3:

2015 Since the price changes only at the beginning of the year, there

is no LIFO reserve at the end of 2015.

Requirement 4:

2016 Purchases exceed sales; hence, there is no LIFO liquidation.

2017 Replacement cost of layers liquidated:

Effect of LIFO liquidation on net income

Requirement 5:

Inventory turnover for 2016

COGS/Average inventory

Inventory turnover for 2017

COGS/Average inventory

Requirement 6:

Adjusted inventory turnover

for 2016

Adjusted inventory turnover

for 2017

© 2018 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for

sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or

posted on a website, in whole or part. 9-6

COGS + effect of LIFO

liquidation on COGS

COGS + effect of LIFO

liquidation on COGS

Requirement 7:

Gross margin rate for 2016

($270,000/$720,000) = 37.5%

Gross margin rate for 2017

($140,000/$400,000) = 35%

Gross margin on a per-unit basis:

Requirement 8:

Estimated FIFO COGS = LIFO COGS + Beginning LIFO reserve -

Ending LIFO reserve

Requirement 9:

2015: 0

Requirement 10:

P9-15. Identifying FIFO holding gains (LO 5, 8)

© 2018 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for

sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or

posted on a website, in whole or part. 9-7

When inventory levels are constant (or nearly so), a good estimate

of realized holding gains included in FIFO Income is:

Net realizable value = Selling price – 8% sales commission.

P9-17. Computing inventory impairment (LO 10, 11)

1. Because Jake is using FIFO, U.S. GAAP defines market as net

realizable value (NRV). This is the same approach used in IAS 2:

“Inventories shall be measured at the lower of cost and net realisable

Item

Original

Cost

Net Realizable

Value (NRV)

Inventory

Value

Used

2. Cost of goods sold would be increased and inventory would be

decreased.

3. Inventory valuation is based on total inventory, which allows losses

on some items to be offset by gains on other items. In this case, we

use the total historical cost value of $1,126 because it is lower than

Item

Original

Cost

Net Realizable

Value (NRV)

© 2018 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for

sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or

posted on a website, in whole or part. 9-9

© 2018 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for

sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or

posted on a website, in whole or part. 9-10