Financial Reporting and Analysis (7th Ed.)

Chapter 14 Solutions

Pensions and Postretirement Benefits

Problems

Problems

P14-1. Determining components of pension expense (LO14-3, LO14-4,

LO14-6)

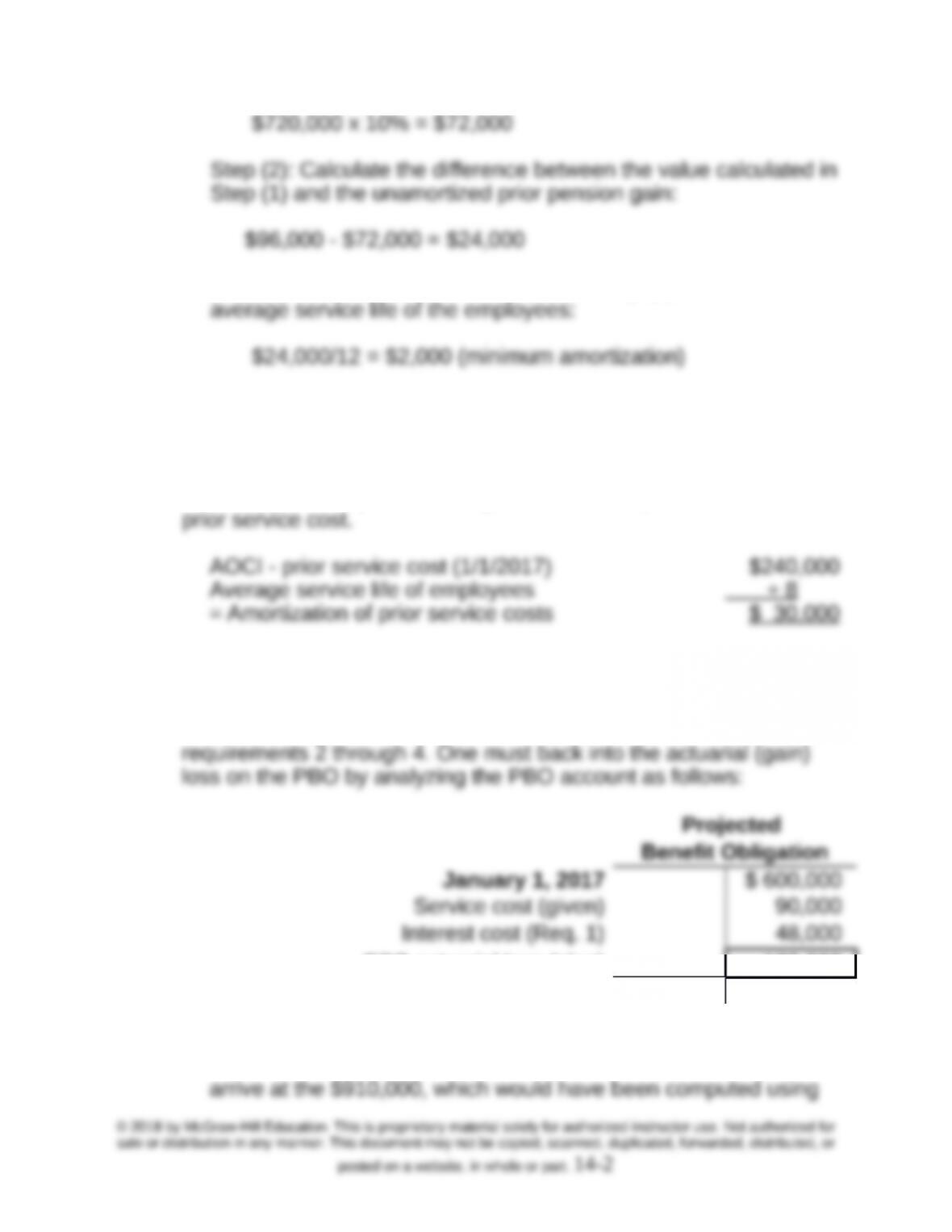

Requirement 1: Interest cost

Beginning balance of PBO $600,000

Requirement 2: Expected dollar return on plan assets

Beginning balance of fair value of plan assets $720,000

Requirement 3: Actual return on plan assets

Fair value of plan assets

1/1/17 balance $720,000

Actual return on plan assets = $825,000 – $720,000 + $0 – $0 =

$105,000

Requirement 4: Minimum amortization of unrecognized

pension gain

Step (1): Determine the “corridor” amount by taking 10% of the

larger of PBO or the fair value of plan assets:

© 2018 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for

sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or

posted on a website, in whole or part. 14-1

Step (3): Amortize the value obtained in Step (2) over the

Requirement 5: Recognized prior service costs

This calculation assumes that the plan amendment was made at

12/31/2016. No separate average service life is provided for the

Requirement 6: Balance in AOCI – Net actuarial (gain) loss

12/31/2017

Information needed to compute the plan assets effects come from

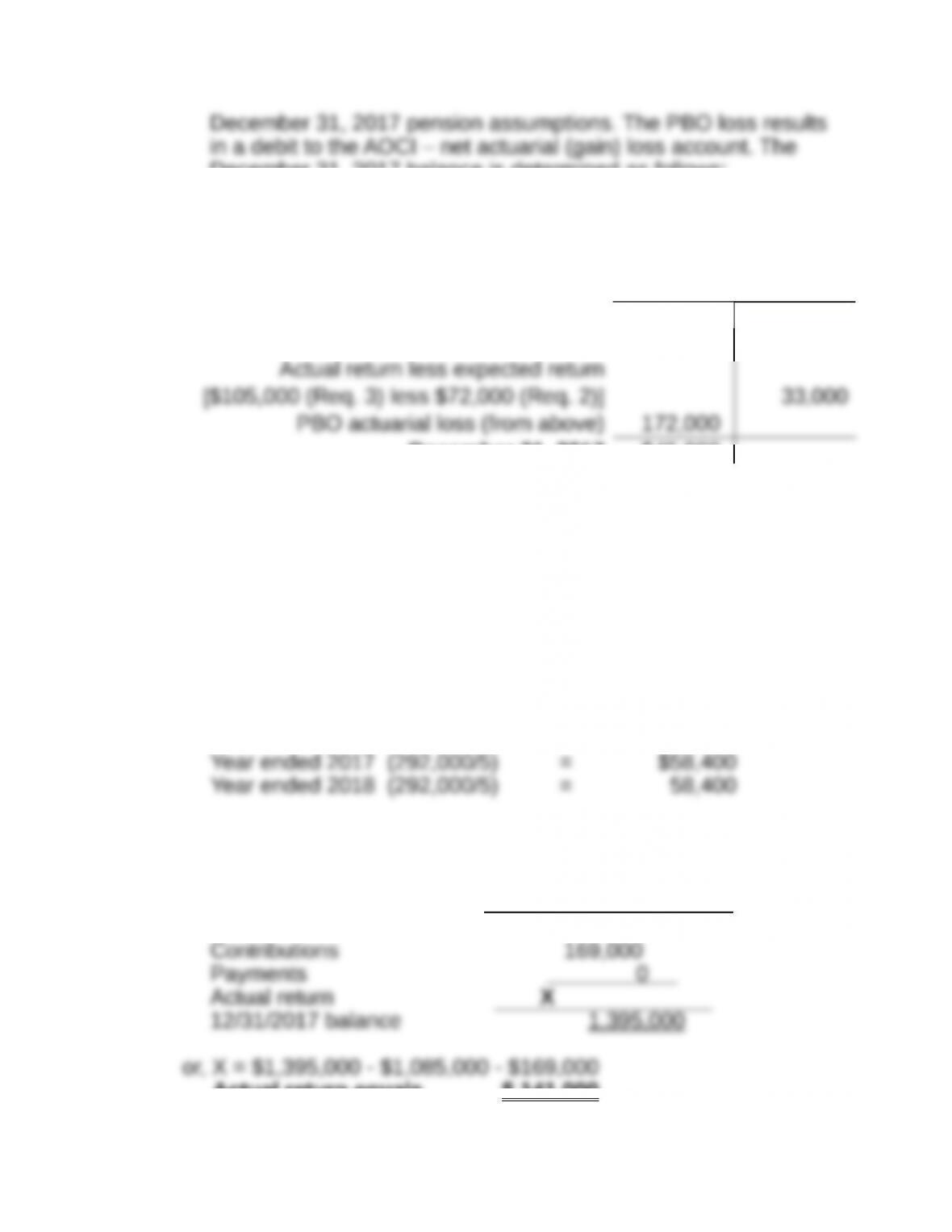

PBO actuarial loss (plug) 172,000

December 31, 2017 910,000

The $172,000 is a loss because we need to increase the PBO to

December 31, 2017 balance is determined as follows:

AOCI – net actuarial

(gain= Cr.) loss = Dr.

January 1, 2017 $ 96,000

Amortization (Req. 4) $ 2,000

December 31, 2017 $45,000

P14-2. Determining expense and balance sheet amounts (journal

entries) (LO14-3, LO14-4, LO14-6)

Note that this problem distinguishes between fair value of plan

assets and market-related value. See the chapter discussion

related to GE pensions.

Requirement 1:

Prior Service Cost Amortization:

Requirement 2:

Actual Return on Plan Assets:

Fair Value Plan Assets

1/01/2017 balance 1,085,000

Actual return equals $ 141,000

© 2018 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for

sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or

posted on a website, in whole or part. 14-3

Requirement 3:

Unexpected Gain for 2017:

Requirement 4:

Pension Expense for 2017:

$ 168 ,700

Requirement 5:

Required Pension Journal Entries for 2017:

DR Pension expense $110,300

To record amortization component of pension expense

To record the unexpected gain on plan assets

DR Pension asset (liability) $113,250

CR OCI – net actuarial (gain) loss $ 113,250

Requirement 6:

AOCI – net actuarial (gains) and losses:

© 2018 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for

sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or

posted on a website, in whole or part. 14-4

AOCI – net actuarial (gain) loss at 12/31/2017 $ (178 ,300)

Amortization of Unrecognized Gains—Corridor Approach:

Market Related Gain Amount

Year PBO Value of Plan

Assets Loss (Gain) Not in

MRV

Subject to

Amort

*Fair value of $1,395,000 less Market related value of $1,369,000

Amount outside corridor $(7,300)

Requirement 7: Check of pension asset (liability) account

PBO $(1,450,000)

Pension asset (liability)

Asset gain entry 65,050

P14-3. Determining expense and balance sheet amounts (journal

entries) (LO14-3, LO14-4, LO14-6)

Note that this problem distinguishes between fair value of plan

© 2018 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for

sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or

posted on a website, in whole or part. 14-5

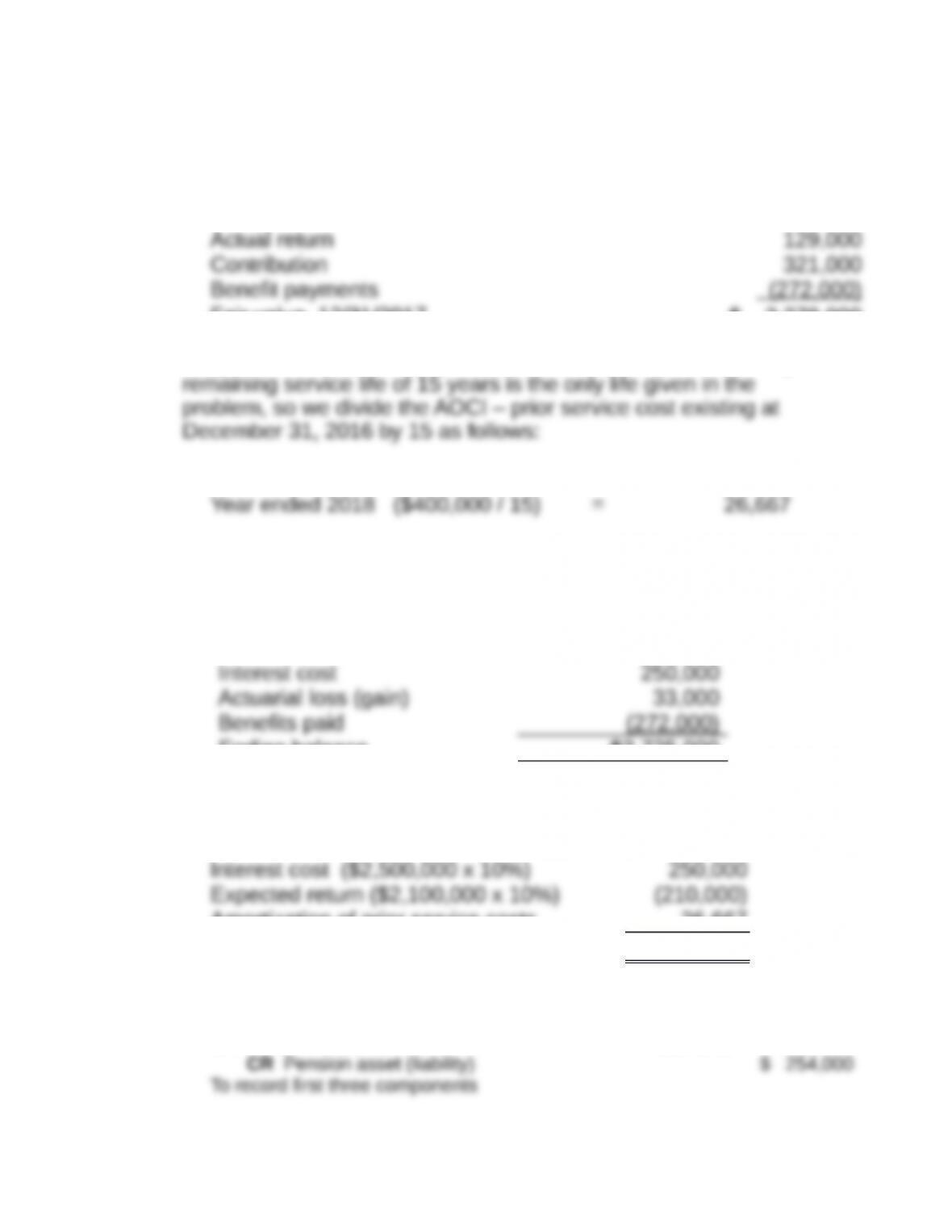

Requirement 1: Fair value of plan assets:

Fair value, 12/31/2016 $ 2,100,000

Fair value, 12/31/2017 $ 2,278,000

Requirement 2: Prior Service Cost Amortization – The average

Year ended 2017 ($400,000 / 15) = $ 26,667

Requirement 3: PBO at December 31, 2017

Beginning balance $2,500,000

Service cost 214,000

Ending balance $2,725,000

Requirement 4: Compute pension expense for 2017:

Service cost $ 214,000

Amortization of prior service costs 26,667

$ 280,667

Requirement 5: Required Pension Journal Entries for 2017:

DR Pension expense $254,000

© 2018 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for

sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or

posted on a website, in whole or part. 14-6

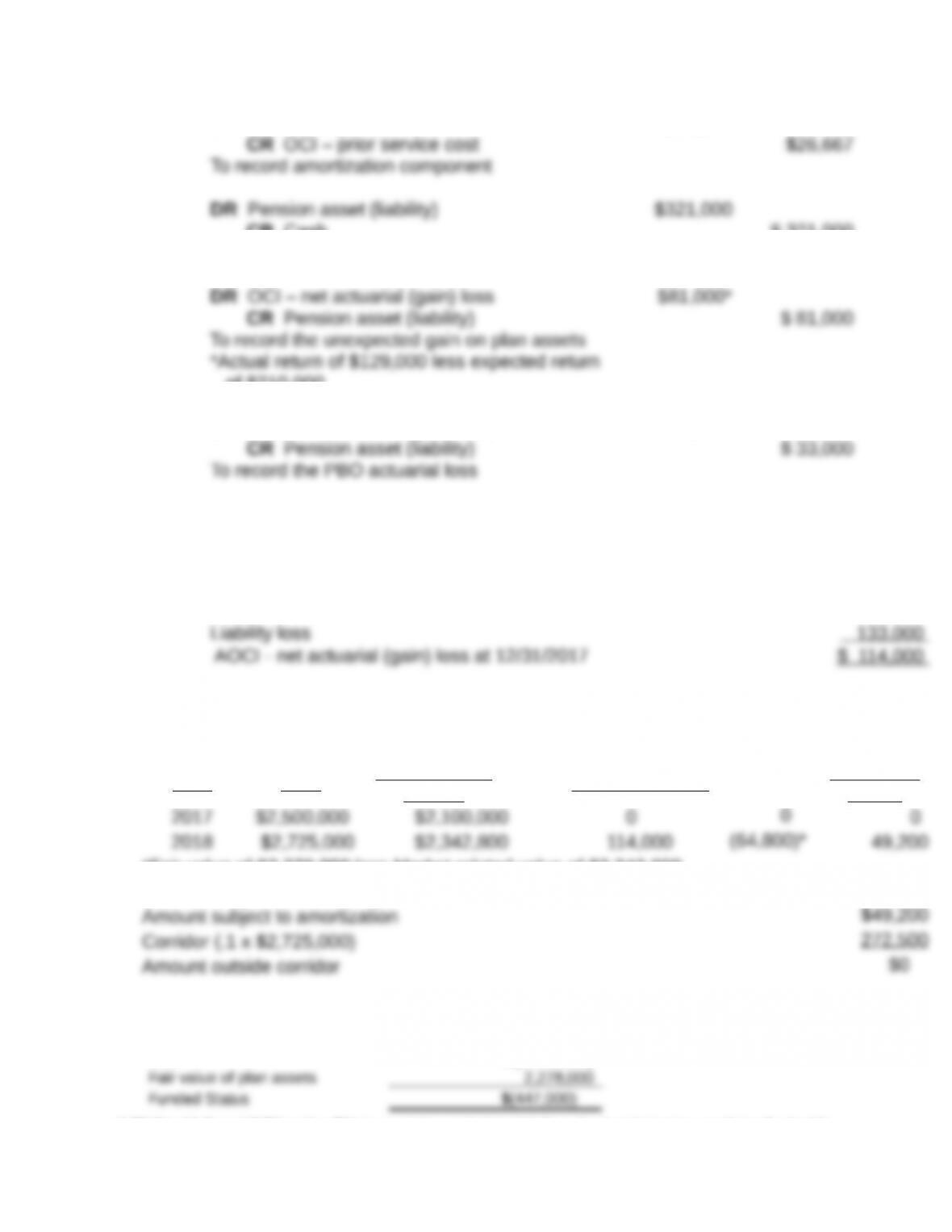

DR Pension expense $26,667

CR Cash $ 321,000

To record contribution

of $210,000

DR OCI – net actuarial (gain) loss $33,000

Requirement 6: AOCI – Net actuarial (gain) loss and amortization:

Asset loss $ 81,000

Amortization of Unrecognized Gains—Corridor Approach:

Market Related Loss Amount

Year PBO Value of Plan

Assets Net Loss (Gain) Not in

MRV

Subject to

Amort

*Fair value of $2,278,000 less Market related value of $2,342,800.

2018 calculation

Requirement 7: Check of pension asset (liability) account

PBO $(2,725,000)

© 2018 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for

sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or

posted on a website, in whole or part. 14-7

Pension asset (liability)

PBO loss entry (33,000)

Ending balance $(447,000)

P14-4. Relating pension concepts to pension accounting (LO14-1,

LO14-2, LO14-3)

Problem information

Pension Plan Data

Defined benefit plan

Inception date: 1/1/2017

Generosity 0.02

Employee Data

Start date 1/1/2014

1 75,000

Timeline

1/1/201

7 12/31/2031 12/31/2051

© 2018 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for

sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or

posted on a website, in whole or part. 14-8

(Rerement

(Start

date)

Requirements 1 and 2: Service cost, interest cost, and PBO

2017 2018

Retirement benefit earned for

year of service $1,500a$1,500

cPV13,7% x PVOA 20,7% x $1,500

dBeginning PBO of $6,163 x .07

Alternative PBO calculation

Requirement 3 and 4: Fair value of plan assets and funded status

2017 2018

Beginning balance $ – $1,200

Funded status (Plan assets less PBO) $(4,963) $(10,680)

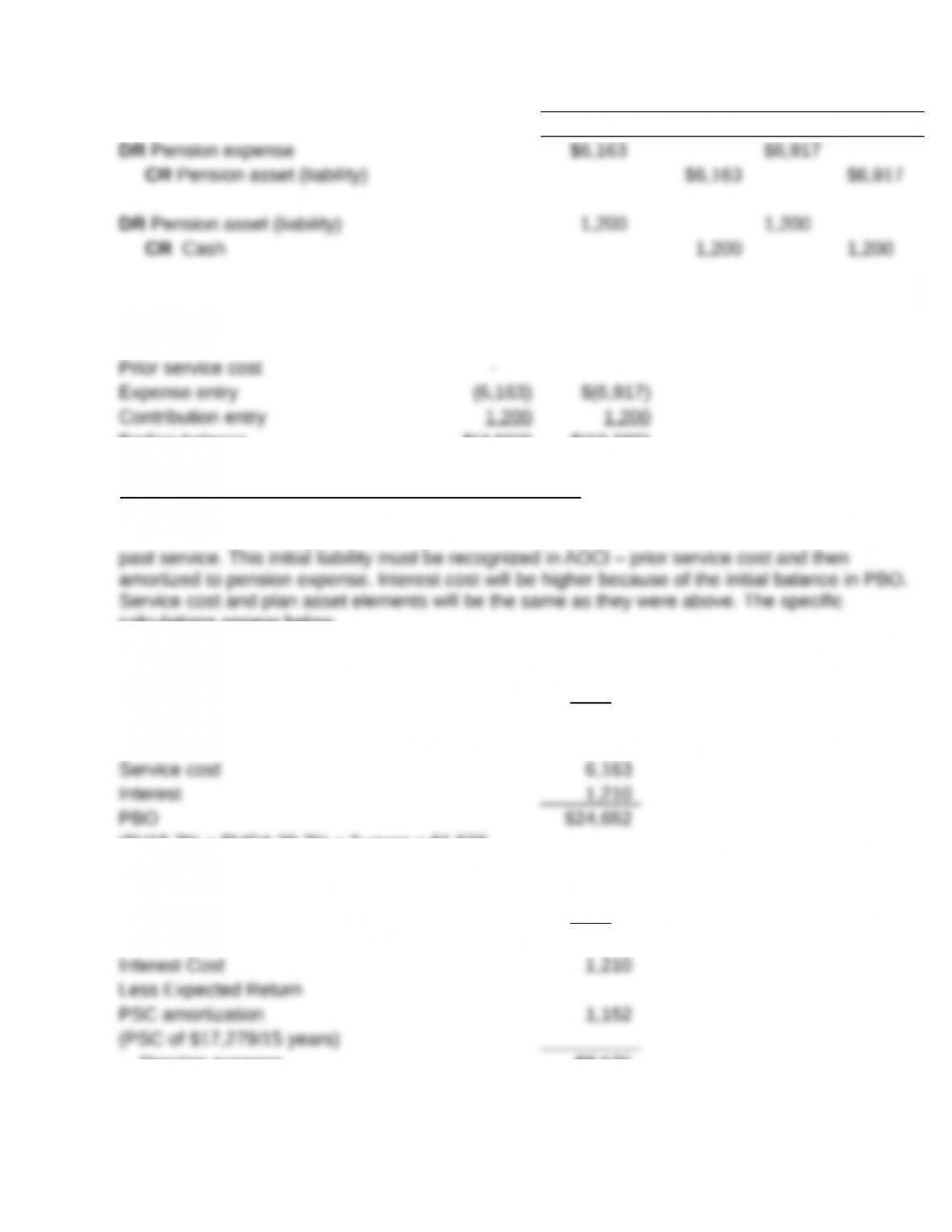

Requirement 5: Pension expense

2017 2018

Service Cost $6,163 $6,594

Pension expense $6,163 $6,917

Requirement 6: Journal Entries

© 2018 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for

sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or

posted on a website, in whole or part. 14-9

2017 2018

Pension asset (liability) account 2017 2018

Beginning balance $ – $(4,963)

Ending balance $(4,963) $(10,680)

Requirement 7 – Effect of granting prior service cost

Instead of PBO starting at zero, it begins at an initial liability of $17,279 for the three years of

calculations appear below.

Effect on PBO

2017

PBO at inception (PSC) $17,279e

ePV15,7% x PVOA 20,7% x 3 years x $1,500

Effect on Expense

2017

Service Cost $6,163

Pension expense $8,525

© 2018 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for

sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or

posted on a website, in whole or part. 14-10

Effect on journal entries

2017

DR OCI – prior service cost $17,279

CR Pension asset (liability) $17,279

CR OCI – prior service cost 1,152

To record pension expense for the year

Funded Status

PBO $24,652

Check on Funded Status

Pension asset (liability) account

Contribution entry 1,200

$(23,452)

© 2018 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for

sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or

posted on a website, in whole or part. 14-11