P10-16. Making asset age and intercompany comparisons (LO 10-3)

Requirement 1:

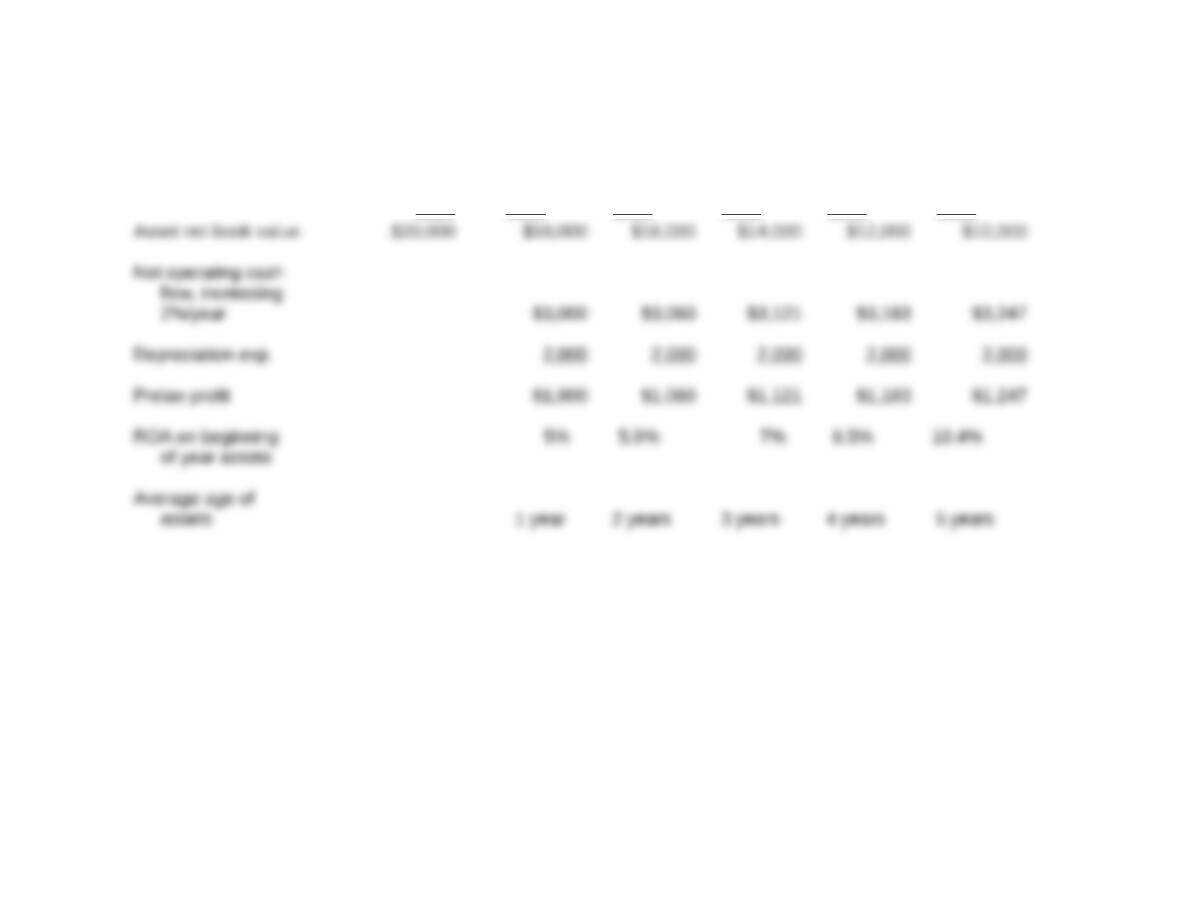

ROA for Gardenia Co. (000s omitted):

Jan. 1 Dec. 31 Dec. 31 Dec. 31 Dec. 31 Dec. 31

2017 2017 2018 2019 2020 2021

© 2018 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any manner. This document may not be

copied, scanned, duplicated, forwarded, distributed, or posted on a website, in whole or part. 10-1

Requirement 2:

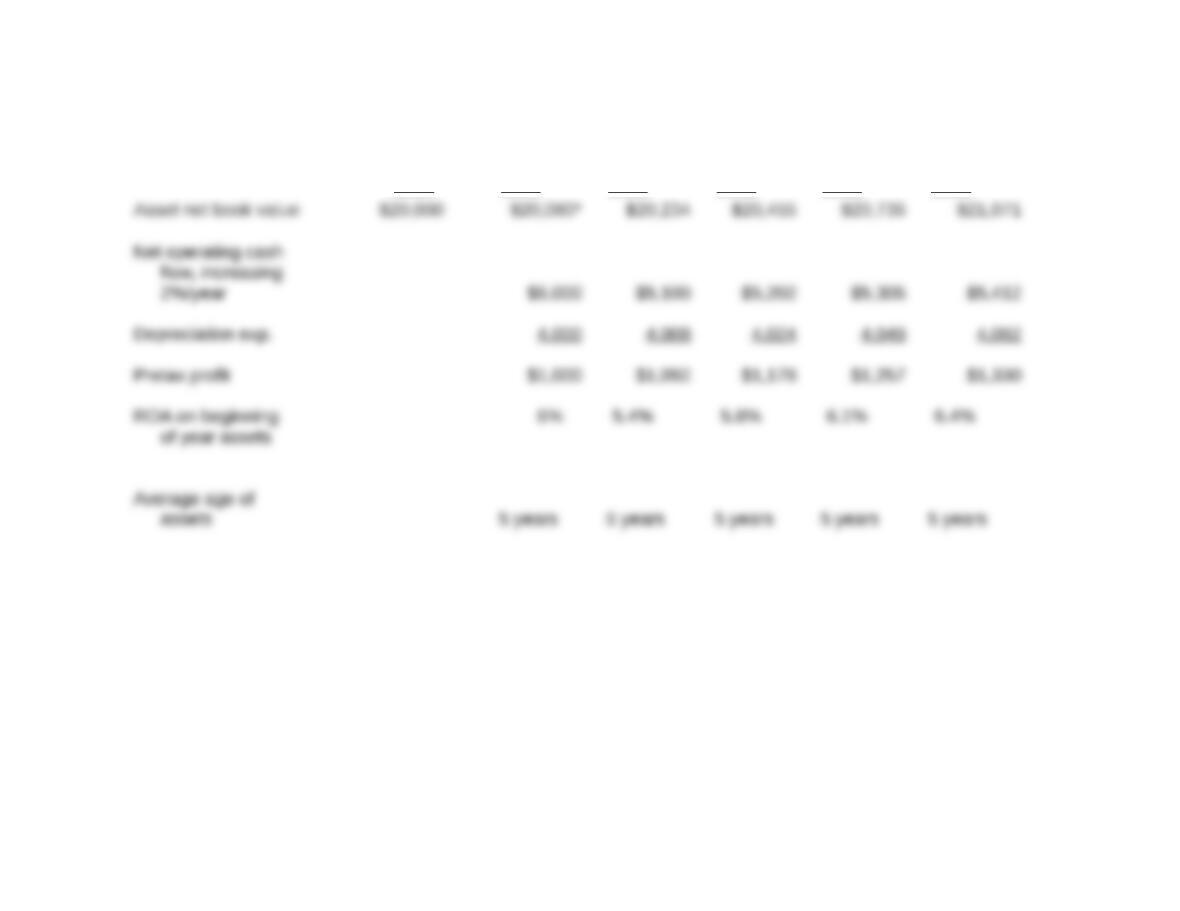

ROA for Lantana Co. (000s omitted):

Jan. 1 Dec. 31 Dec. 31 Dec. 31 Dec. 31 Dec. 31

2017 2017 2018 2019 2020 2021

© 2018 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any manner. This document may not be

copied, scanned, duplicated, forwarded, distributed, or posted on a website, in whole or part. 10-2

2017

2018 2019

2020 2021

Beginning of the

(Beginning of year

x 10%)

1 Assets are, on average, 5 years old, with a 10-year life = ½ depreciated.

Therefore, $20,000,000 net asset base x 2 = $40,000,000 gross asset base.

Requirement 3:

Gardenia’s rapidly increasing ROA gives the appearance of significant

year-to-year improvement. But this is illusory because the ROA increase is

caused primarily by the increasing average age of its asset base. This factor

Lantana’s much smaller upward drift in ROA is attributable to the stable

average asset age that results from its continual replacement of 10% of its

P10-17. Accounting for asset retirement obligations (LO 10-6)

Requirement 1:

GAAP requires companies to recognize an asset retirement obligation (ARO)

when a reasonable estimate of its fair value can be made. These legal

obligations arise when a company builds or buys an asset that requires

mandatory expenditures at the end of the asset’s useful life to protect public

© 2018 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for

sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or

posted on a website, in whole or part. 10-3

welfare or improve safety. For example, dismantling an offshore oil platform

requires expenditures to protect and restore the marine environment.

Coyote Co. can estimate the fair value of this obligation as the present value

of the estimated future cash outflows.

Amortization table:

(a) (b) (c)

Year

Present Value

ARO

At 1/1

Accretion

Expense

Present Value

ARO

At 12/31

*rounding error of $31

Requirement 2:

The costs associated with the decommissioning of the power plant will be

shown on the income statement as both:

Increased depreciation expense each period as a result of recording and

DR Accretion expense $931,380

CR Asset retirement obligation $931,380

The $15,000,000 total decontamination cost is shown as part of the expense

of operating the power plant and is matched with the revenue generated by

the plant over its productive life. Prior to the issuance of pre-Codification

© 2018 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for

sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or

posted on a website, in whole or part. 10-4

SFAS No. 143, companies would often ignore these costs until they were

incurred at the end of the asset’s life, thereby overstating operating income.

P10-18. Accounting for assets held for sale (LO 10-6)

Requirement 1:

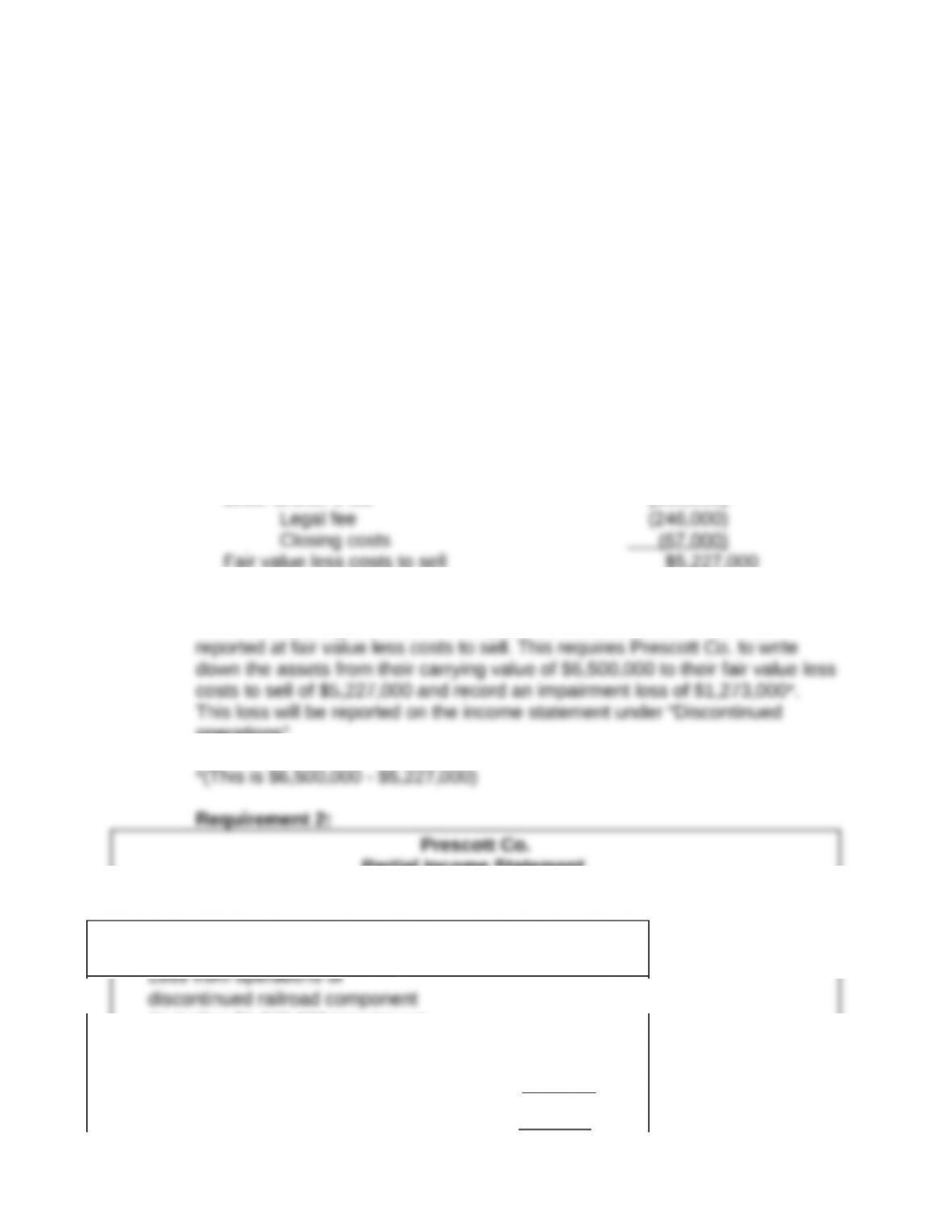

Carrying value at 12/31/17:

When assets are held for sale, they are reported at the lower of carrying value

or fair value less costs to sell. The fair value less costs to sell of the railroad

assets is:

Since management has committed to a plan, has identified a potential buyer,

and is anticipating a sale within the year, the railroad assets should be

*(This is $6,500,000 – $5,227,000)

Requirement 2:

Prescott Co.

Partial Income Statement

For the Year Ending December 31, 2017

Discontinued operations (see Note xx)

Loss from operations of

discontinued railroad component

(Including $1,273,000 impairment

loss) (1 ,748,000)+

Net income $6 ,127,000

© 2018 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for

sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or

posted on a website, in whole or part. 10-5

*(This is net income of $7,400,000 plus the loss of $475,000 added back on the

railroad component)

+(This is the loss on the railroad component of $475,000 plus the impairment loss of

$1,273,000)

Prescott’s income statement for the year ended December 31, 2017 should

report discontinued operations for the railroad component after income from

continuing operations and before extraordinary items.

Requirement 3:

Operating margin ROA

With DCO treatment

*(This is $20,000,000 – $1,800,000)

+(This is $94,500,000 – $6,500,000)

If the disposal does not qualify as a discontinued operation, Prescott Co.

would continue to report the results for the railroad component as part of

ongoing operations year-to-year.

Requirement 4:

During 2018 the assets held for sale will not be depreciated. The assets will

continue to be valued at the lower of carrying value or fair value less costs to

sell. Any losses previously recorded may be recovered—but not in excess of

the cumulative loss previously recognized (FASB ASC 360-10-35-40).

© 2018 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for

sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or

posted on a website, in whole or part. 10-6

P10-19.Evaluating approaches to long-lived asset valuation (LO 10-1)

Requirement 1:

Expected benefit approaches focus on the estimated value of long-term

assets in an output market, that is, a market where the assets could be sold.

This approach assigns a value to an asset based on the expected future cash

flows the asset is capable of generating. One valuation measure under this

Another valuation measure under this approach is what the asset would bring

if it were sold in the marketplace. In this case, the Boeing 777 would be

valued at its net realizable value. Problems that arise in implementing the

Economic sacrifice approaches focus on an asset’s cost in an input market—

a market where the asset could be acquired. The most obvious example of

Historical cost is the dominant approach underlying current GAAP. A second

example of an economic sacrifice approach is current replacement cost. This

Requirement 2:

From the perspective of a financial analyst, the answer to the question is yes.

Since the primary input into financial analysis is information about a firm,

analysts would like to have these other valuations in addition to historical

cost. After all, if they feel that any of the additional valuations are not as

reliable as historical cost in a given setting, they can always choose to ignore

© 2018 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for

sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or

posted on a website, in whole or part. 10-7

them. But having these data would make trend analyses, cross-sectional

Requirement 3:

The primary benefit is a more relevant valuation of the company’s assets,

and, thus, a more relevant valuation of the entire company (i.e., its common

stock). The primary cost, which most managers would probably argue

P10-20. Weakness of the Straight-line Depreciation Method (LO 10-1, LO 10-7)

Requirement 1:

a. Annual depreciation expense = (Cost – salvage) ÷ life

$3,962 = ($15,849 − $0) ÷ 4

End

of Depreciation Accumulated Book

Year Expense Depreciation Value

b. If the company were to record straight-line depreciation, its four years’

income statements would appear as follows:

1 2 3 4

Revenue

$

5,000

$

5,000

$

5,000

$

5,000

Depreciation expense

3,96

2

3,96

2

3,96

2

3,96

3

Net income (A) $ $ $ $

© 2018 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for

sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or

posted on a website, in whole or part. 10-8

1,038 1,038 1,038 1,037

$

$

$

$

26.2%

Requirement 2:

a.

Under the present value method of depreciation, annual depreciation expense

is the difference between the present value of future cash flows at the

beginning of year and end of year.

Beginning

of year PV

Annual of Future

Depreciatio

n

Accumulate

d

Year cash flow cash flows expense Depreciation

Book

Value

b.

1 2 3 4

Revenue

$

5,000

$

5,000

$

5,000

$

5,000

Depreciation expense

3,41

5

3,75

6

4,13

3

4,54

5

Net income (A)

$

1,585

$

1,244

$

867

$

455

Initial investment (B) $ $ $ $

© 2018 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for

sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or

posted on a website, in whole or part. 10-9

Requirement 3:

Clearly, the rising annual return on investment under straight-line is an illusion,

created by the use of an arbitrary method of depreciation. In this example, with

straight-line depreciation, a constant numerator (Net income) is divided by a

declining denominator (Initial investment) to produce a rising annual return on

On the other hand, the present value method yields an annual return on

investment of 10% in the income statement so long as the actual cash flows

coincide with the anticipated cash flows. If the actual cash flows were to

exceed, or fall short of, the anticipated cash flows, the annual return on

investment would be correspondingly higher or lower. The use of this method

enables a reader of the income statement to determine whether, and to what

Requirement 4:

The “present value method” is not an acceptable method in U.S. financial

speculative. So while this approach certainly seems to fit the general

depreciation criteria of a method that is both “systematic and rational,” it falls

short when it comes to verifiability and objectivity. It may, however, be used by

companies for internal reporting purposes, especially when one seeks to

evaluate the performance of divisions and subsidiaries.

© 2018 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for

sale or distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or

posted on a website, in whole or part. 10-10