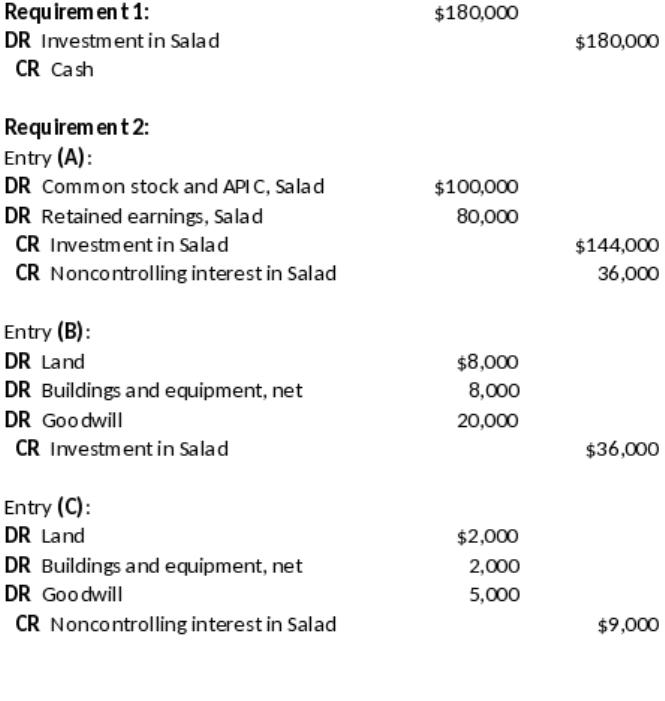

P16-8. Elimination entries and consolidated balance sheet under acquisition

method

16-1

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

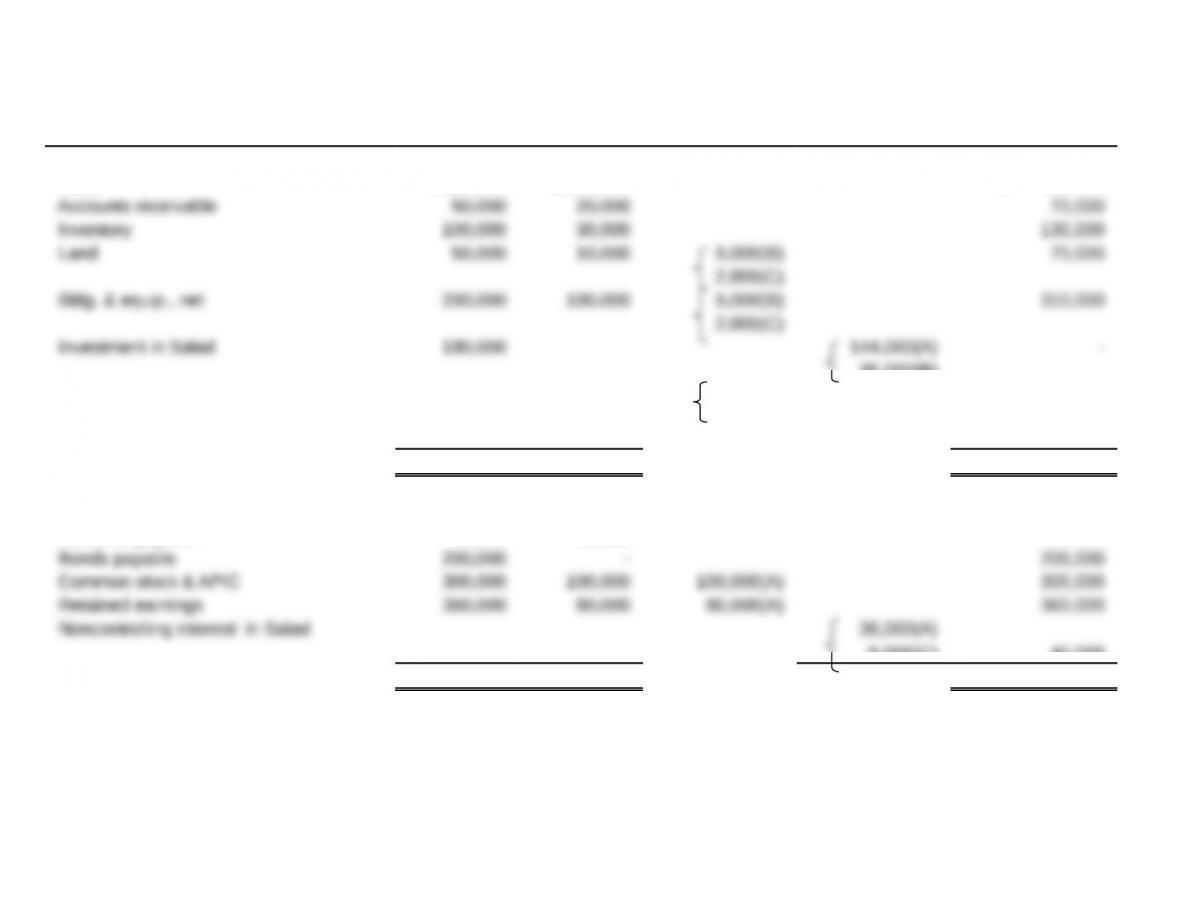

Requirement 3:

Plate Salad

Eliminations Consolidated

Dr Cr Balance Sheet

Assets

Cash $ 320,000 $ 100,000 $ 420,000

36,000(B)

Goodwill 20,000(B) 25,000

5,000(C)

Total $ 900,000 $ 260,000 $ 1,025,000

Liabilities & Equity

Accounts payable 40,000 80,000 120,000

9,000(C) 45,000

Total $ 900,000 $ 260,000 $ 1,025,000

16-2

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education.

P16-9. Eliminating entries and accounting for goodwill

Requirement 1:

DR Investment in Saturn $1,000,000

CR Cash $1,000,000

Requirement 2:

Requirement 3:

2017 2018

Pluto’s income $500,000 $350,000

Saturn’s income 200,000 100,000

life.

P16-10. Comparing translation effect on ratios

(CFA Adapted)

Remeasurement is the process under which a subsidiary’s local currency

results are translated into the parent’s currency. ASC 830 requires

inventory accounting results in a lag in recognizing exchange rate changes.

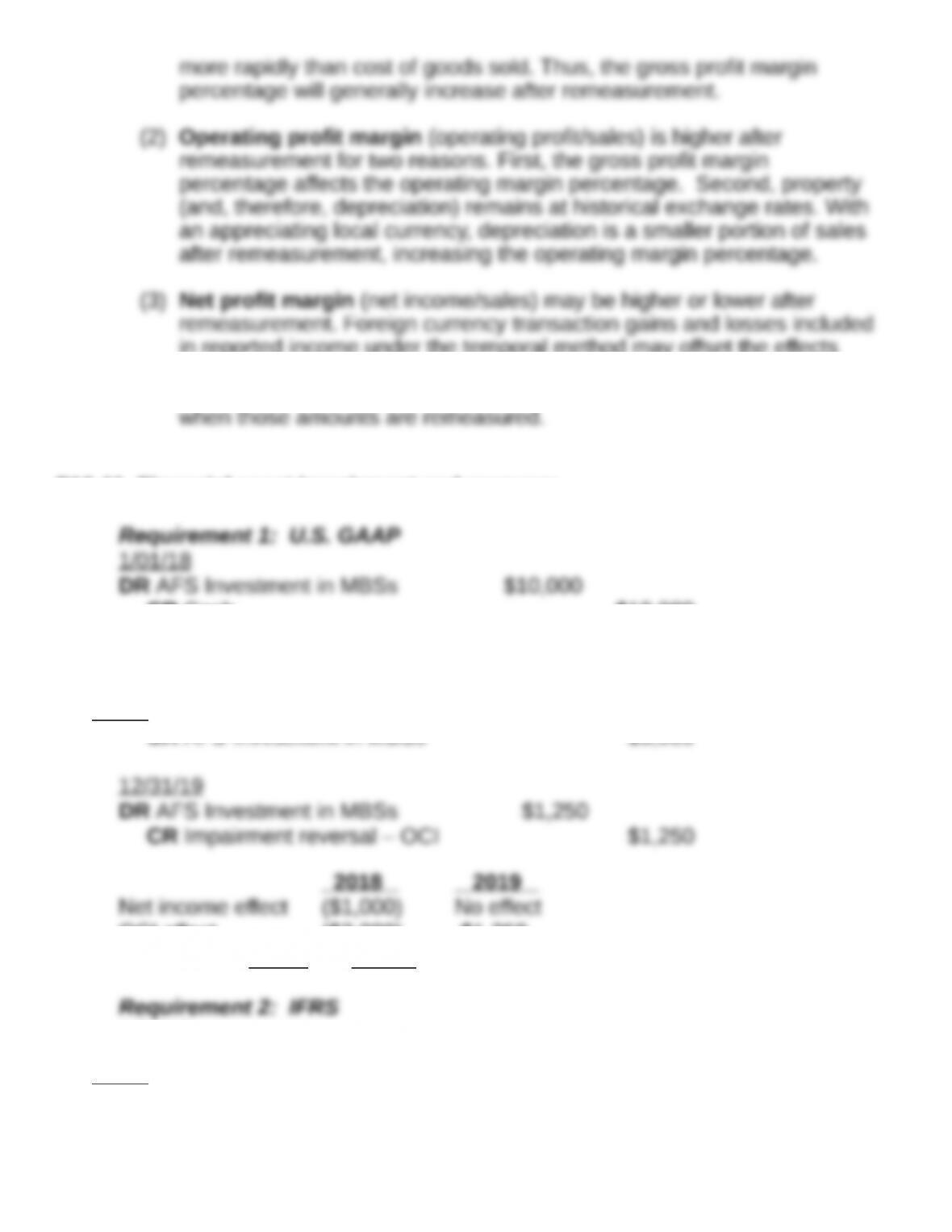

(1) Gross profit margin percentage (gross profit/sales) is higher after

percentage will generally increase after remeasurement.

(2) Operating profit margin (operating profit/sales) is higher after

remeasurement for two reasons. First, the gross profit margin

after remeasurement, increasing the operating margin percentage.

(3) Net profit margin (net income/sales) may be higher or lower after

when those amounts are remeasured.

P16-11. Financial asset impairment and recovery

Requirement 1: U.S. GAAP

1/01/18

DR AFS Investment in MBSs $10,000

CR Impairment reversal – OCI $1,250

2018 2019

Requirement 2: IFRS

1/01/18

DR AFS Investment in MBSs $10,000

CR Cash $10,000

16-4

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

OCI effect No effect No effect

Requirement 3(a): U.S. GAAP

The recovery due to other factors will be recorded as a reversal of the

previously recorded impairment in OCI. The journal entry is:

Requirement 3(b): IFRS

The $3,000 impairment due to credit losses and other factors recorded in 2018

P16-12. Variable interest entities

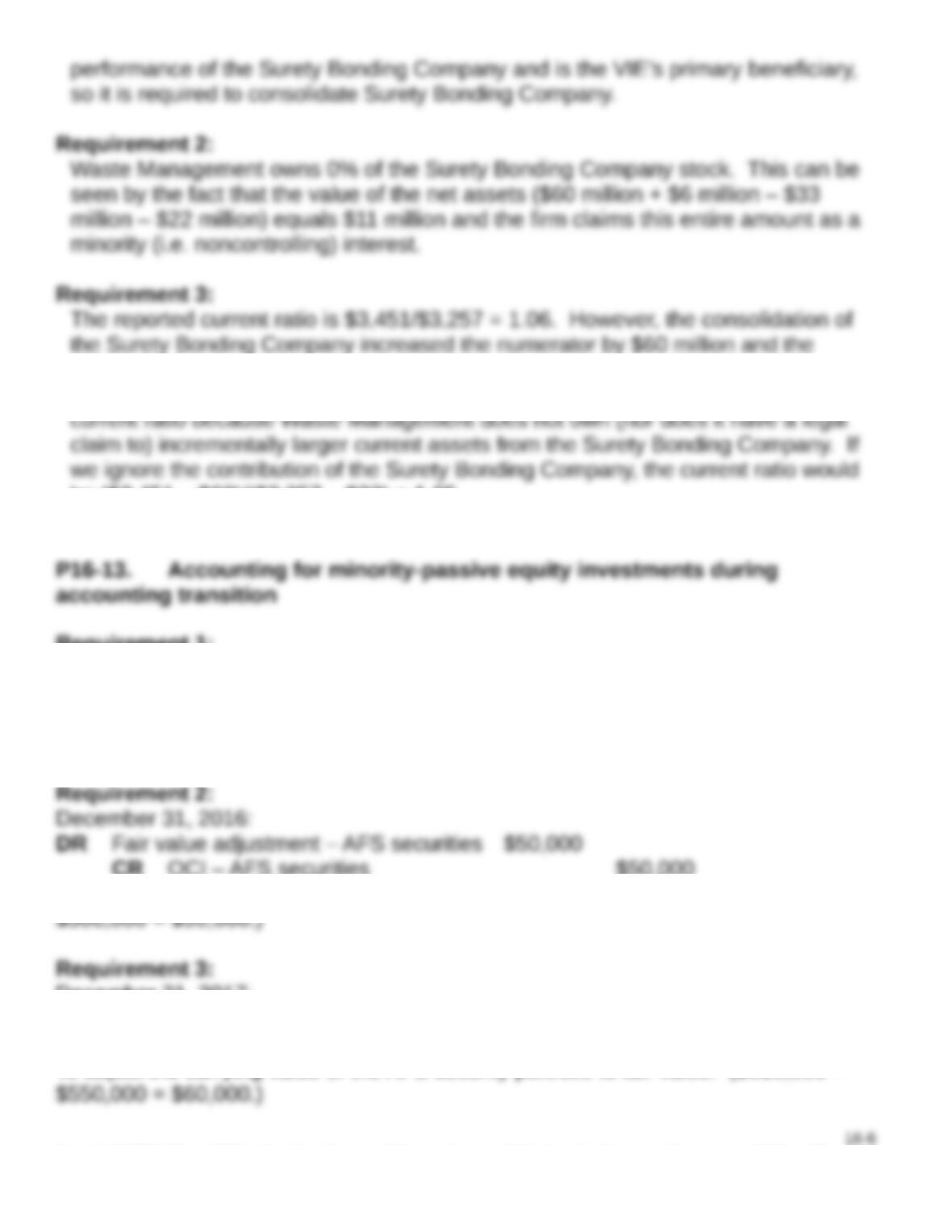

Requirement 1:

A variable interest entity must be consolidated by the entity deemed to be its

so it is required to consolidate Surety Bonding Company.

Requirement 2:

Waste Management owns 0% of the Surety Bonding Company stock. This can be

Requirement 3:

The reported current ratio is $3,451/$3,257 = 1.06. However, the consolidation of

the Surety Bonding Company increased the numerator by $60 million and the

we ignore the contribution of the Surety Bonding Company, the current ratio would

be ($3,451 – $60)/($3,257 – $33) = 1.05.

P16-13. Accounting for minority-passive equity investments during

accounting transition

Requirement 1:

Requirement 2:

December 31, 2016:

$500,000 = $50,000.)

Requirement 3:

December 31, 2017:

DR Fair value adjustment – AFS securities $60,000

16-6

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

Requirement 4:

January 1, 2018:

DR Accumulated OCI* – AFS securities $110,000

*Assumes the amount credited to OCI each year was subsequently closed to AOCI

during the closing process.

Requirement 5:

December 31, 2018:

DR Unrealized loss on equity securities $20,000

Requirement 6:

July 1, 2019:

DR Cash $640,000

To record the sale of Spiegel stock.

Financial Reporting and Analysis (7th Ed.)

Chapter 16 Solutions

Intercorporate Investments

Cases

Cases

C16-1. Shopko: Business acquisitions and analysis of sales growth

Requirement 1:

16-7

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

The financial statement user should recognize that a significant part of the

31.8% increase in consolidated revenue for Year 1 is attributable to the

lead to an incorrect assessment of revenue growth from Year 0 to Year 1.

The pro forma note disclosures report results for Year 0 and Year 1 as if the

15.2%, computed as ($4,181,567 – $3,630,951)/$3,630,951

Requirement 2:

The 15.2% growth rate provides a better estimate of sustainable revenue

The instructor might point out that the minimum GAAP pro forma disclosures

are so limited (i.e., sales, net income and EPS) that reconstruction of

C16-2. Measurement and reporting of noncontrolling interest under

acquisition method

NOTE: $ amounts in thousands

Requirement 1:

ASC 805-20-30, paragraph 7 requires the acquirer (ICG) to measure

market prices of the noncontrolling shares, other valuation techniques must

be applied.

Requirement 2:

ASC 805-20-30, paragraph 8 indicates that the purchase price for the

appropriate to discount the value of the noncontrolling shares for the

16-8

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

absence of control. ICG stated that it discounted the noncontrolling shares

Requirement 3:

(The amounts that follow are in thousands of dollars.) The $19,670

purchase price for 89% of GovDelivery’s equity implies a full fair value of

$1,011 ($2,431-$1,420), or 41.6% ($1,011/$2,431).

Requirement 4:

The acquisition would have no effect on the consolidated income statement

acquisition.

The 12/31/09 consolidated balance sheet would include GovDelivery’s

Consolidation would be achieved with the standard elimination entries

Investment account on ICG’s books (credit), and allocate $1,420 to

noncontrolling interest (credit).

Requirement 5:

Customer lists, trademarks/trade names, and technology will be amortized

each year as follows:

potentially affect consolidated income. Other net assets do not have a

16-9

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

stated useful life so their subsequent consolidated income effect is

unknown.

proportionate, as discussed in requirement 3.

C16-3. Air Products: Joint ventures and off-balance-sheet effects

Requirement 1:

The primary reason that companies enter into joint ventures is because

primary explanation for joint ventures.

It is also true that if ownership of the joint venture is exactly 50:50, then—

debt-to-equity.

Requirement 2:

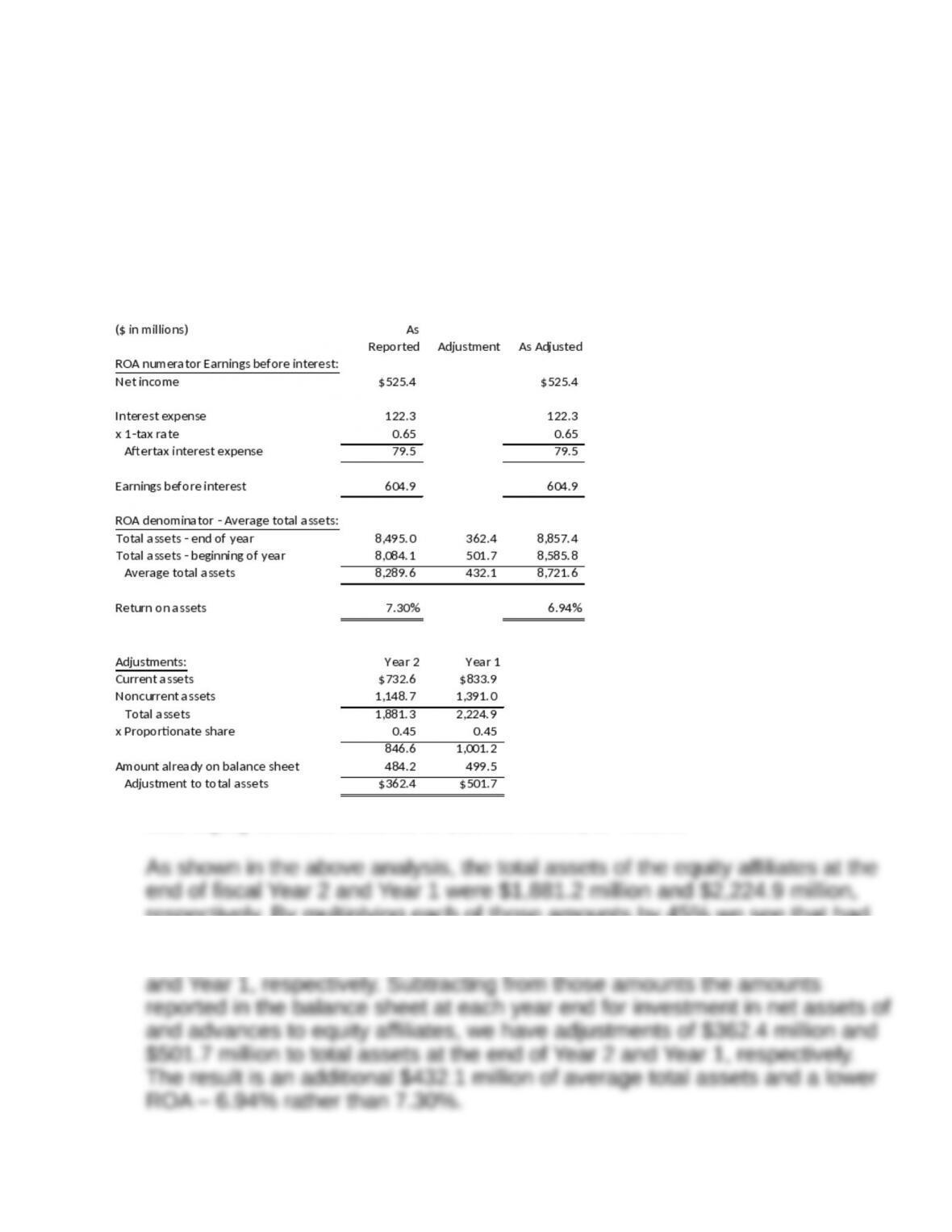

All of the following computations depend upon estimates and assumptions.

statements is 7.30%. After adjusting for the joint ventures, it is 6.94%.

16-10

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

The adjustments are made because the denominator in the ROA computation

total equity affiliates’ income of $196.3 million, or 45.2%.

As shown in the above analysis, the total assets of the equity affiliates at the

end of fiscal Year 2 and Year 1 were $1,881.2 million and $2,224.9 million,

The result is an additional $432.1 million of average total assets and a lower

ROA – 6.94% rather than 7.30%.

16-11

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.