P11-23. Hedging a Planned Sale (LO 11-7, LO 11-8)

Requirement 1:

Newton plans to sell some of its corn inventory next March, six

months from now (October). This sale will take place at the March

market price. However, Newton does not want to be exposed to

Requirement 2:

The forward contract has zero value at inception, as indicated in

Requirement 4:

The following entries are made on March 15:

DR Other comprehensive income $70,000

DR Cash $25,000

Notice that the total revenue and cash flow from selling corn is

Requirement 5:

The answer to this question depends on how Newton designates

the forward contract hedge. If Newton designates the forward

contract as a cash flow hedge of 50% of planned sale of corn

inventory, the hedge is “fully effective”. In this case, the entries

If Newton designates the forward contract as a cash flow hedge of

the entire planned sale of corn inventory, the hedge would be

considered “ineffective” under GAAP and thus not qualify for

P11-24. Using an interest-rate swap as a cash flow hedge (LO 11-7, LO

11-8)

Requirements 1 and 2:

The analysis is summarized in the following table.

Notional Interest Cash

amount rate interest

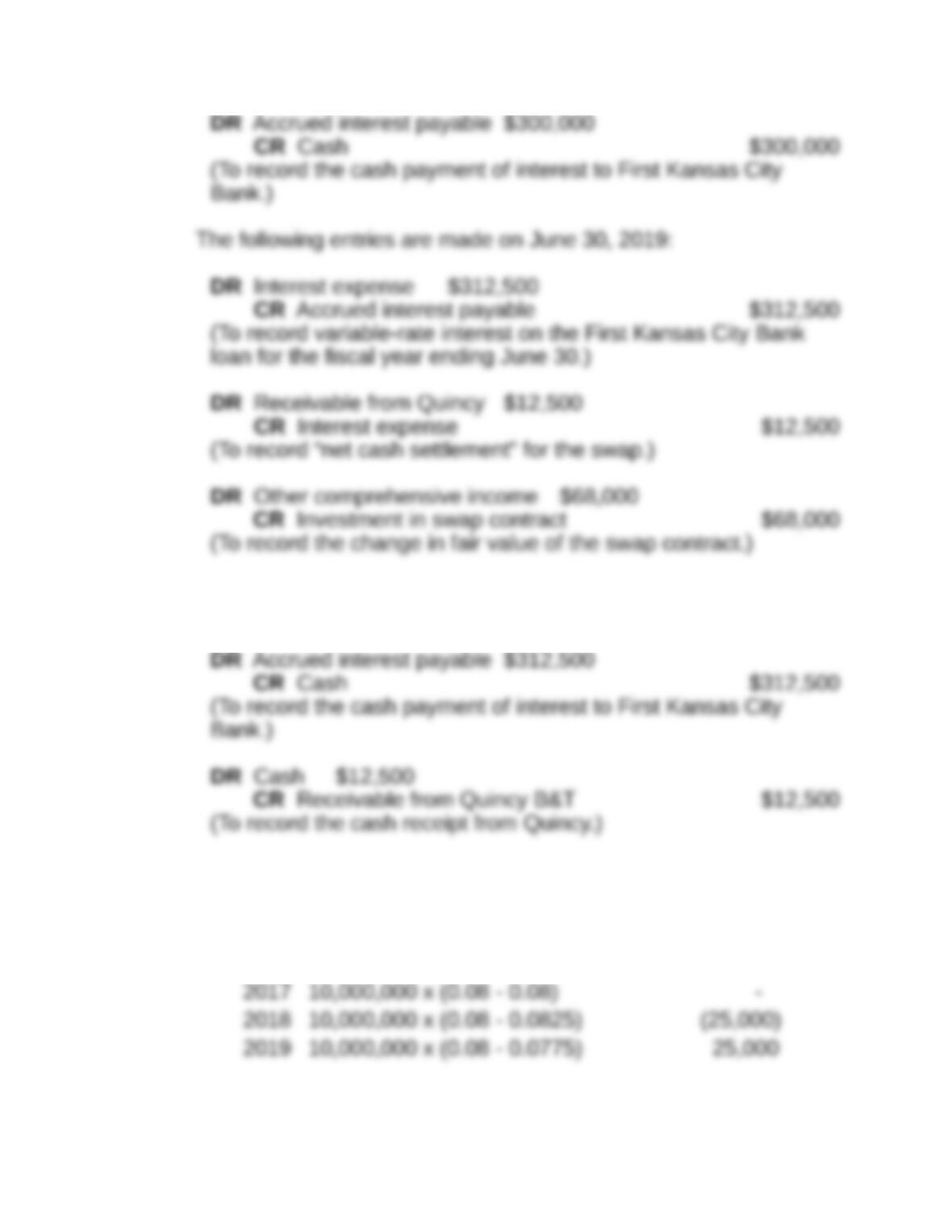

July 1, 2018:

The July 1, 2018 “net cash settlement” for Basie is zero because

the fixed-rate payment and the variable-rate payment are the

Basie pays First Kansas City $300,000 on July 1, 2018 and

$312,500 on July 1, 2019. Notice that the July 1, 2019 payment is

Requirements 3 and 4:

The swap contract has zero value at inception, as indicated in the

problem statement, so there is no entry made when the contract is

signed.

No entry is made to record “net cash settlement” for the swap

because it is zero.

The following entry is made on July 1, 2018:

Although not required by the problem statement, the following

entries are made on July 1, 2018:

P11-25. Using an interest-rate swap as a fair value hedge (LO 11-7, LO

11-8)

Requirement 1: Cash settlements on swap:

The December 31, 2017 “net cash settlement” for Four Brothers is

zero because the fixed-rate and the variable-rate are the same,

Requirement 2: Cash paid to Guiffrie on bond

Requirement 3: 2017 journal entries

The swap contract has zero value at inception, as indicated in the

problem statement, so there is no entry made when the contract is

signed.

DR Guiffrie Bank Loan (debt) $45,000

(To record the change in fair value of the swap contract)

No entry is made to record “net cash settlement” for the swap

contract because it is zero.

Requirement 4: 2018 journal entries

CR Cash $25,000

(To record the “net cash settlement” payment to Herman Bank)

DR Swap contract $68,000

Swap Contract

P11-26. Determining hedge Effectiveness (LO 11-7, LO

11-8)

Requirement 1: Journal entries – no hedge treatment

Because the futures contracts are deemed “ineffective” for GAAP

purposes, the special hedge accounting rules cannot be used.

October 1, 2017:

December 31, 2017:

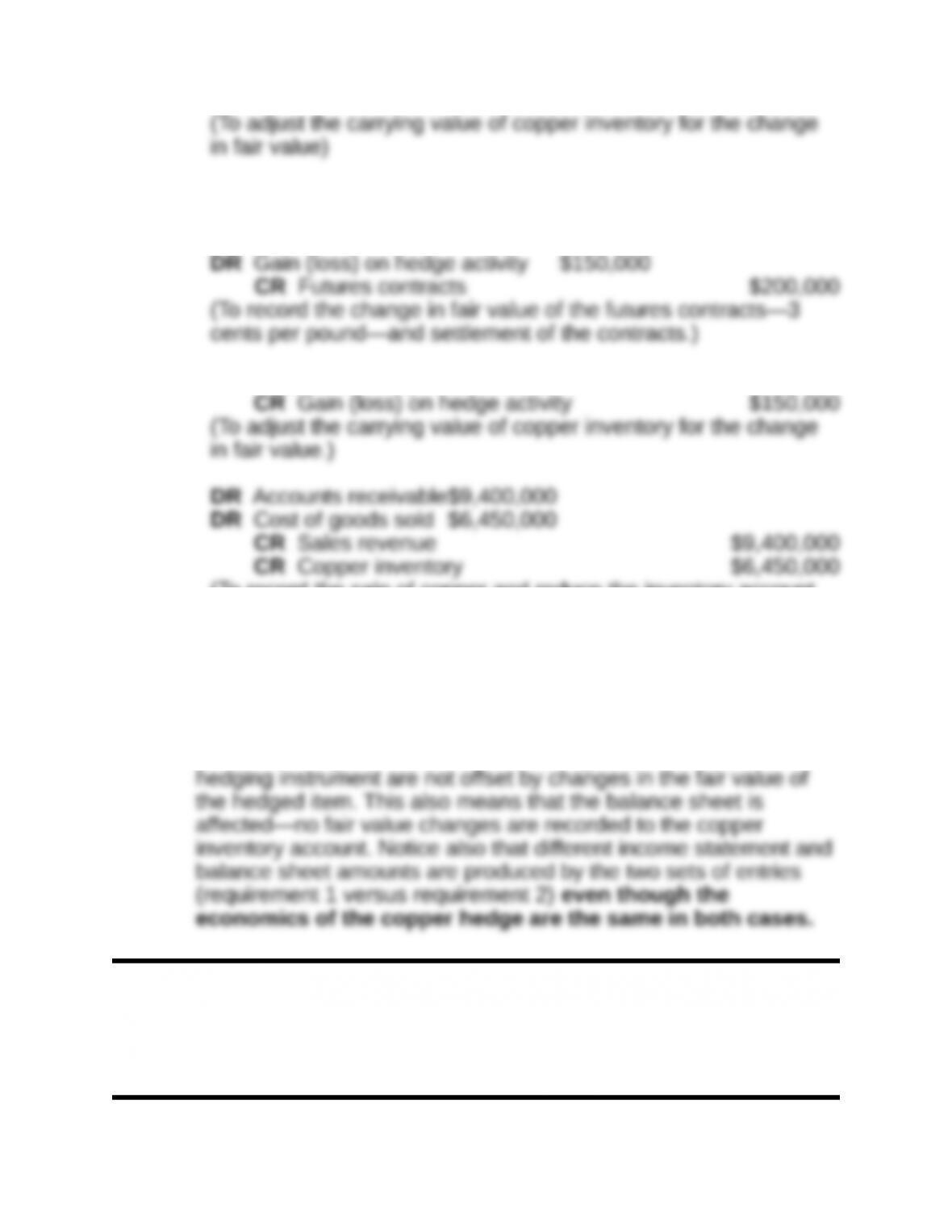

DR Futures contracts $200,000

CR Gain (loss) on futures contracts $200,000

(To record the change in fair value of the futures contracts: 5

million pounds at 4 cents per pound.)

February 26, 2018:

DR Cash $ 50,000

DR Accounts receivable$9,400,000

DR Cost of goods sold 6,500,000

(To record the sale of copper and reduce the inventory account

by the original cost of the copper.)

Requirement 2: Journal entries with half the futures effective

Now the futures contracts are deemed “effective” for GAAP

October 1, 2017:

No journal entry

December 31, 2017:

February 26, 2018:

DR Cash $ 50,000

DR Copper inventory $150,000

(To record the sale of copper and reduce the inventory account

by the adjusted cost of the copper.)

Requirement 3: Impact on financial statements

These journal entries illustrate how the income statement and the

balance sheet are affected by the definition of the hedged item.

Notice how the first set of entries (requirement 1) gives rise to

greater earnings volatility because changes in the fair value of the

Financial Reporting and Analysis (7th Ed.)

Chapter 11 Solutions

Financial Instruments and Liabilities

Cases

Cases

C11-1. Century and beyond bonds (LO 11-1, LO 11-2)

Requirement 1: Present value of principal to price

The issue price of Draper’s $200 million century bonds is also $200

million. The follows from the fact that the market yield (7.5%)

exactly equals the stated interest rate. A financial calculator on

To find the principal contribution to issue price, we need to

determine the present value of $200 million to be received 100

years from January 1, 2017 using the market yield of 7.5% as our

discount rate. The present value factor for a single payment in 100

periods at 7.5% is 0.000723. Multiplying this factor by the amount

of the payment ($200 million) yields a present value of $145,000

What about the interest payment stream? Well, interest payments

must contribute the remaining amount of the issue price

Requirement 2: Tax savings

The present value of the company’s interest tax deduction is equal

to the present value of the interest payment stream, multiplied by

the effective tax rate of 35%. This tax savings present value is

To find the amount of tax savings lost if only the first 40 years of

interest payments are deductible, we first need to find the present

interest payment—at 7.5% is $188.916 million. The tax benefit of

this 40-year deduction is $66.121 million ($188.916 million x 35%) in

Requirement 3: Issue price at different rates

The market yield (8.5%) is above the stated (coupon) interest rate,

and this means the $200 million century bonds will sell at a discount

to their face value. To find the issue price using a financial calculator

Requirement 4: Ohio State bond

A major source of cash for educational institutions such as The Ohio

State University is tuition paid by students. The primary economic

benefit from issuing century bonds is that Ohio State has access to

$500 million cash immediately rather having to wait until sometime

Requirement 5: Reason for Treasury or Congress intervention

Both the treasury and Congress are concerned that these bonds do

not meet the definition of debt, and therefore, should not receive the

Requirement 6: GAAP treatment

GAAP currently treats century and millennium bonds, as they are

described here, as debt. This may change in the future.