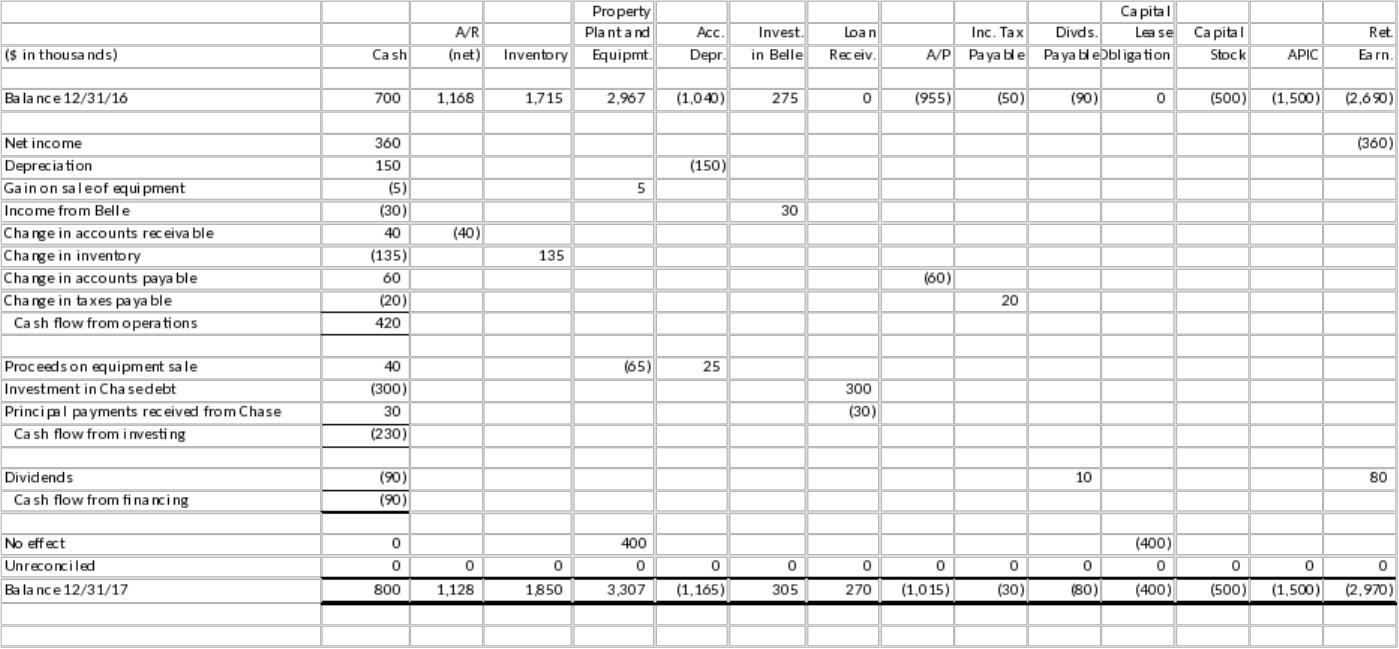

P17-9. Preparing a statement of cash flows—indirect method

(AICPA adapted)

Omega Corporation

Statement of Cash Flows

For the Year Ended December 31, 2017

Cash Flow from Operating Activities:

Net income $360,000

Adjustments to reconcile net income to cash provided

by operating activities:

Depreciation1150,000

Changes in assets and liabilities:

Decrease in accounts receivable 40,000

Cash Flows from Investing Activities:

Proceeds from sale of equipment 40,000

1Depreciation

Net increase in accumulated depreciation

Proceeds $40,000

Carrying value 35 ,000

Gain $ 5 ,000

17-2

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

17-3

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education.

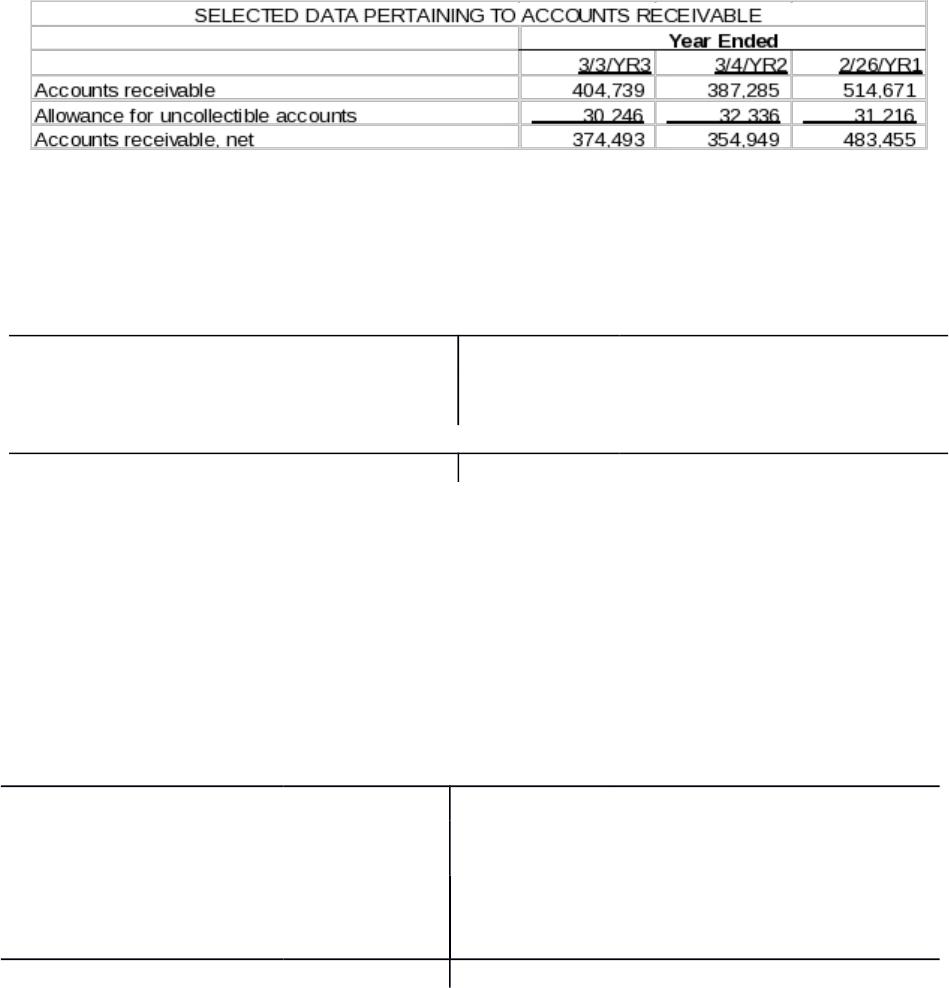

P17-10. Operating cash flow impact of securitization

Requirement 1:

Use the data presented in the problem to first determine gross accounts

receivable:

Next, determine the amount of accounts receivable written off during Year

3:

Allowance for Doubtful Accounts

The preceding information, in conjunction with information given in the

problem, can then be used to reconstruct summary entries in the accounts

receivable account, thus solving for cash collected from customers.

Accounts Receivable

Beginning balance $ 387,285 $ 20,000 Securitizations in YR3

Credit sales for YR3 17,507,719 28,693 Accounts written off

during YR3

17,441,572 Collections from

customers during YR3

Ending balance 404,739

Requirement 2:

17-4

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

$ 32,336 Beginning balance

Accounts written off

during YR3 (plug)

28,693 26,603 Bad debts expense for YR3

(given)

30,246 Ending balance

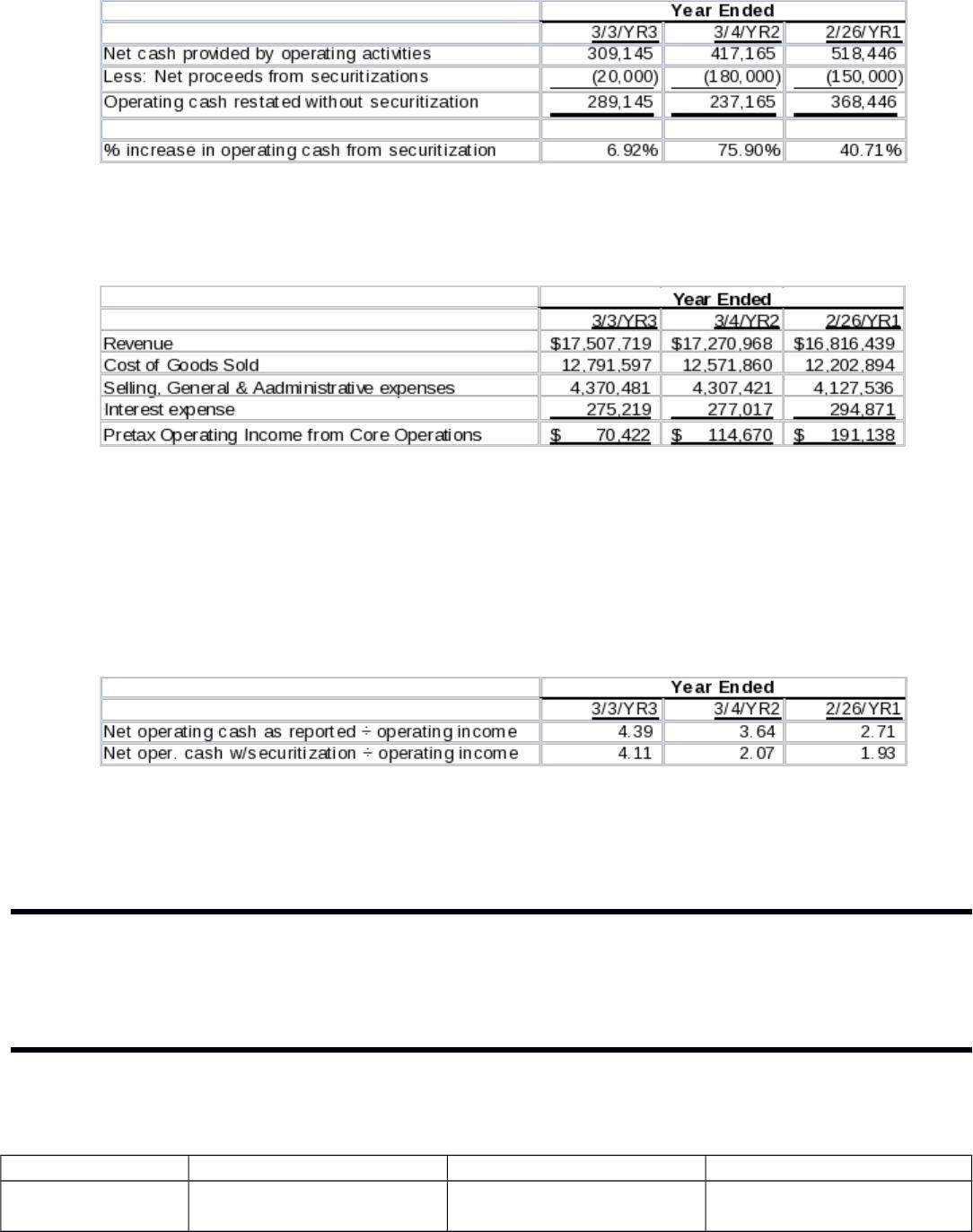

While the impact of securitization on operating cash flows for fiscal Year 3 might not be

considered material, the increases in the two prior years certainly were.

Requirement 3:

Note: Pretax operating income as defined in this analysis excludes the effects of

(nonrecurring) events not related to core business operations and the impact of the large,

and inconsistent, income tax benefit.

Dividing operating cash flows (both with and without securitization as

determined in requirement 2) by pretax operating income results in the

following:

A healthy business should produce positive operating cash flows and these cash flows

should usually exceed operating income because of the presence of non-cash charges

(e.g., depreciation). In Rite Aid’s case, this expected relationship is in evidence without the

effects of securitization, but is significantly enhanced by securitization.

Financial Reporting & Analysis (7th Ed.)

Chapter 17 Solutions

Statement of Cash Flows

Cases

Cases

C17-1. Statement of cash flow differences under IFRS and U.S. GAAP

Telstra Seven Group Holdings First Solar

Operating

section

1. Interest and other

items of a similar nature

1. Interest received

3. Interest paid

17-5

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

received

2a. Dividends received

from equity accounted

investees

2b. Other dividends

received

3. Interest and other

costs of finance paid

Investing section 1. Interest received

2a. Distributions

received from Foxtel.

2b. Dividends received

Financing section 3. Finance costs paid

(i.e., interest)

As illustrated, key areas of difference between IFRS and U.S. GAAP under current

standards are where interest and dividends received and interest paid are reported.

All of these items are reported in the operating section under U.S. GAAP. IFRS

permits firms to report these items in other sections of the statement of cash flows. A

number of top 100 Australian firms follow the approach taken by Seven Group

Holdings; a few others report interest or dividends received as investing activities.

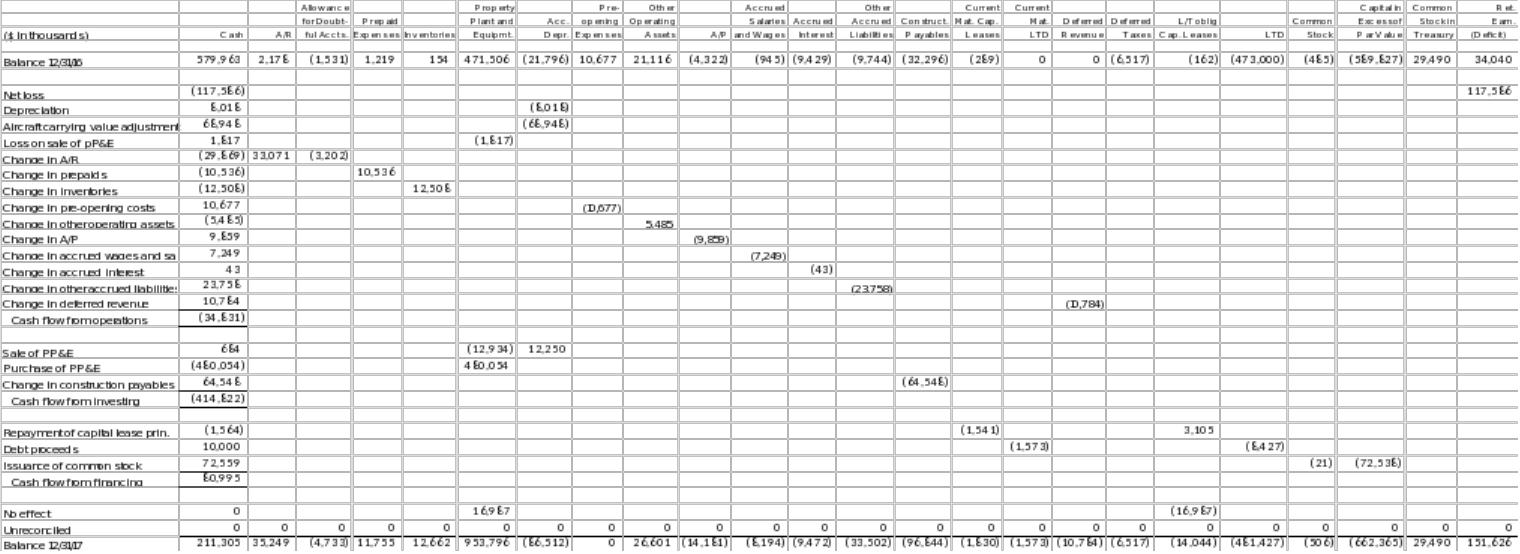

C17-2. Lucky Lady, Inc.: Preparing comprehensive statement of cash flows

Note: All amounts shown in this solution are “$ in thousands”

Lucky Lady, Inc.

Statement of Cash Flows

For the Year Ended 12/31/17

Cash Flows from Operating Activities:

Net loss ($117,586)

+ Depreciation expense 8,018

+ Aircraft carrying value adjustment 68,948

+ Loss on sale of property, plant & equip.

(book value $2,501–cash received $684) 1,817

– Increase in net accounts receivable (29,869)

– Increase in prepaid expenses (10,536)

– Increase in inventories (12,508)

+ Decrease in pre-opening costs 10,677

– Increase in other operating assets (5,485)

+ Increase in accounts payable 9,859

+ Increase in accrued salaries & wages 7,249

+ Increase in accrued interest on LT debt 43

+ Increase in other accrued liabilities 23,758

17-6

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

+ Increase in deferred revenue 10 ,784

Cash flow from operations ( 34 ,831)

Cash Flows from Investing Activities:

Sale of property, plant & equipment 684

Purchase of PP&E and cost of building (480,054)

+ Increase in construction payables1 64 ,548

(415,506)

Cash flow from investment activities (414 ,822)

Cash Flow from Financing Activities:

Repayment of principal in capital lease (1,564)

Additional borrowing (laundry loan) 10,000

Issuance of additional common stock 72 ,559

Cash flow from financing activities 80 ,995

Total change in cash (368,658)

Cash at 12/31/16 579 ,963

Cash at 12/31/17 $211 ,305

1Alternatively, this could be shown as a financing activity cash inflow.

17-7

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

17-8

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education.

Note on significant non-cash transaction: The Company entered

into a capital lease agreement and recorded an asset and a

corresponding liability for $16,987.

Property, Plant and Equipment

Beginning balance $471,506

New capital lease 16,987 $14,751 Cost of asset sold (net book value

$2,501 + Acc. dep. $12,250)

Other new additions X

Ending balance $953,796

Solve for X:

$953,796 = $471,506 + $16,987 + X – $14,751

X = $480,054

Accumulated Depreciation

$21,796 Beginning balance

Acc. depr. on asset sold X 8,018 Depreciation expense

68,948 Carrying value adjustment

$86,512 Ending balance

Solve for X:

$86,512 = $21,796 + $8,018 + $68,948 – X

X = $12,250

Capital Lease Obligation (including current maturities)

$451 Beginning balance

Repayment of principal X 16,987 New capital lease

$15,874 Ending balance

Solve for X:

$15,874 = $451 + $16,987 – X

X = $1,564

Note: Alternatively, the cash flow statement could show in cash flow

from operations a $3,855 addback for bad debt expense and a

($33,724) reduction for the increase in receivables instead of the

($29,869) increase in net receivables. The following analysis shows

how these amounts are determined.

Allowance for Doubtful Accounts

17-9

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.

$1,531 Beginning balance

Bad debts written off X 3,855 Bad debt expense

$4,733 Ending balance

$4,733 = $1,531 + $3,855 – X; X = $653

Gross Accounts Receivable

Beginning balance $2,178 $653 Bad debts written off

Revenue 57,800 X Cash collected

Ending balance $35,249

$35,249 = $2,178 + $57,800 – $653 – X; X = $24,076

17-10

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of

McGraw-Hill Education.