Financial Reporting and Analysis (7th Ed.)

Chapter 11 Solutions

Financial Instruments and Liabilities

Exercises

Exercises

E11-1. Finding the issue price (LO 11-2)

(AICPA adapted)

We know that the bonds were priced to yield 8% when the contract

interest rate was only 6%. Since the yield is higher than the contract

interest rate, we know the bonds were sold at a discount, and we

must use the yield to maturity to find interest expense and the price

of the bond.

Present value of interest payments

E11-2. Determining market price following a change in interest rate

(LO 11-2)

Now we’ve moved one year closer to the maturity date. So, two

aspects of the calculation in E11-1 will have changed: The yield to

maturity is now 10% (or 5% per period), and there are 18 periods to

maturity.

Present value of principal

E11-3. Finding the discount at Issuance (LO 11-2)

To find the amount of amortization on July 1, 2017 we first need to

know the book value of the bond on that date. Since this is the first

interest payment date, the beginning-of-period book value is the

same as the original issue (selling) price, which is the face value

Semiannual:

E11-4. Determining a bond’s balance sheet value (LO 11-2)

(AICPA adapted)

Even though the bonds pay interest only annually on December 31,

the

June 30 balance sheet would still need to reflect interest accrued

since the issue date:

975

Interest expense is $23,475 = $469,500 x 10% x 1/2 year, interest

payable is $22,500 = $500,000 x 9% x 1/2 year, and the

amortization is the difference between these two amounts.

E11-5. Calculating gain or loss at early retirement (LO 11-4)

(AICPA adapted)

The gain (or loss) on bond extinguishment can be computed as

follows:

The reacquisition price is the cash paid out by Davis to reacquire its

bonds. Since it is less than the book value of the bonds, the

company realizes a gain on the retirement of its debt.

E11-6. Amortizing a premium (LO 11-2)

(AICPA adapted)

To find the amount of unamortized premium on June 30, 2018, we

first need to find the interest expense for 2018 (6% of the June 30,

2017, book value, 6% of $105,000).

Date

Interest

Payment

Interest

Expense

Premium

Amortization Book Value

The carrying (or book) value of the bond on June 30, 2018, is

$104,300. We know that the face value of the bond is $100,000 and

E11-7. Recording loss contingencies (LO 11-9)

(AICPA adapted)

Brower expects to receive $3.2 million as compensation for the

expropriation of its manufacturing plant. The plant has a book value

of $5.0 million, so the estimated loss is $1.8 million ($5.0 book value

– $3.2 million expropriation proceeds). The journal entry to record

the intended expropriation is:

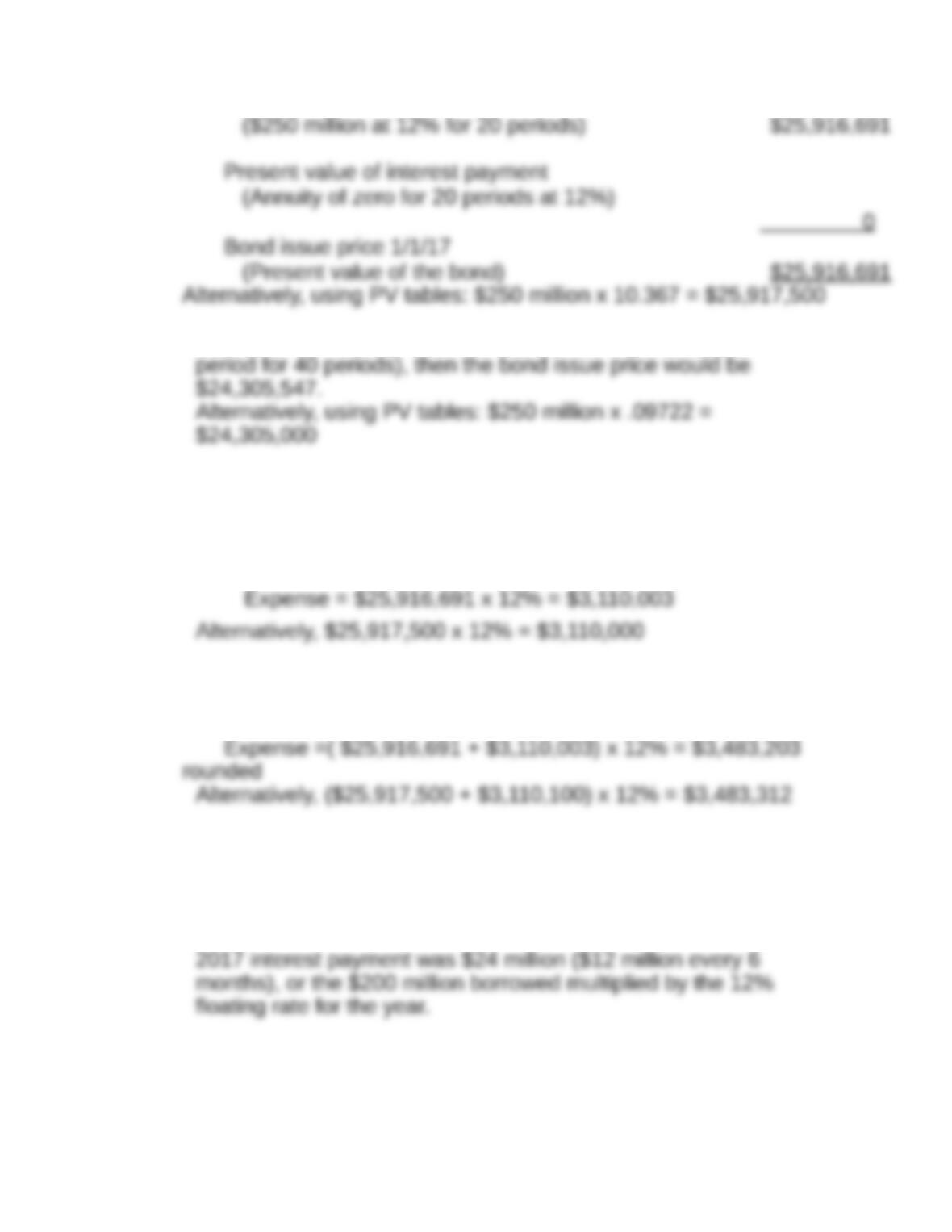

E11-8. Zero coupon bond (LO 11-2)

Requirement 1:

These bonds have a face value of $250 million, a zero coupon

rate, a market yield rate of 12%, and mature in 20 years. The issue

price is:

Present value of principal

If the market interest rate is instead 12% semi-annually (6% each

Requirement 2:

How much interest expense would the company record on the

bonds in 2017? Although the bonds don’t pay interest, an expense

would still be recorded:

Requirement 3:

Interest expense in 2018 would be:

E11-9. Floating-rate debt (LO 11-3)

Requirement 1:

The floating interest rate for 2017, set on January 1 of that year,

was 12% or the LIBOR rate of 6% plus 6% additional interest. The

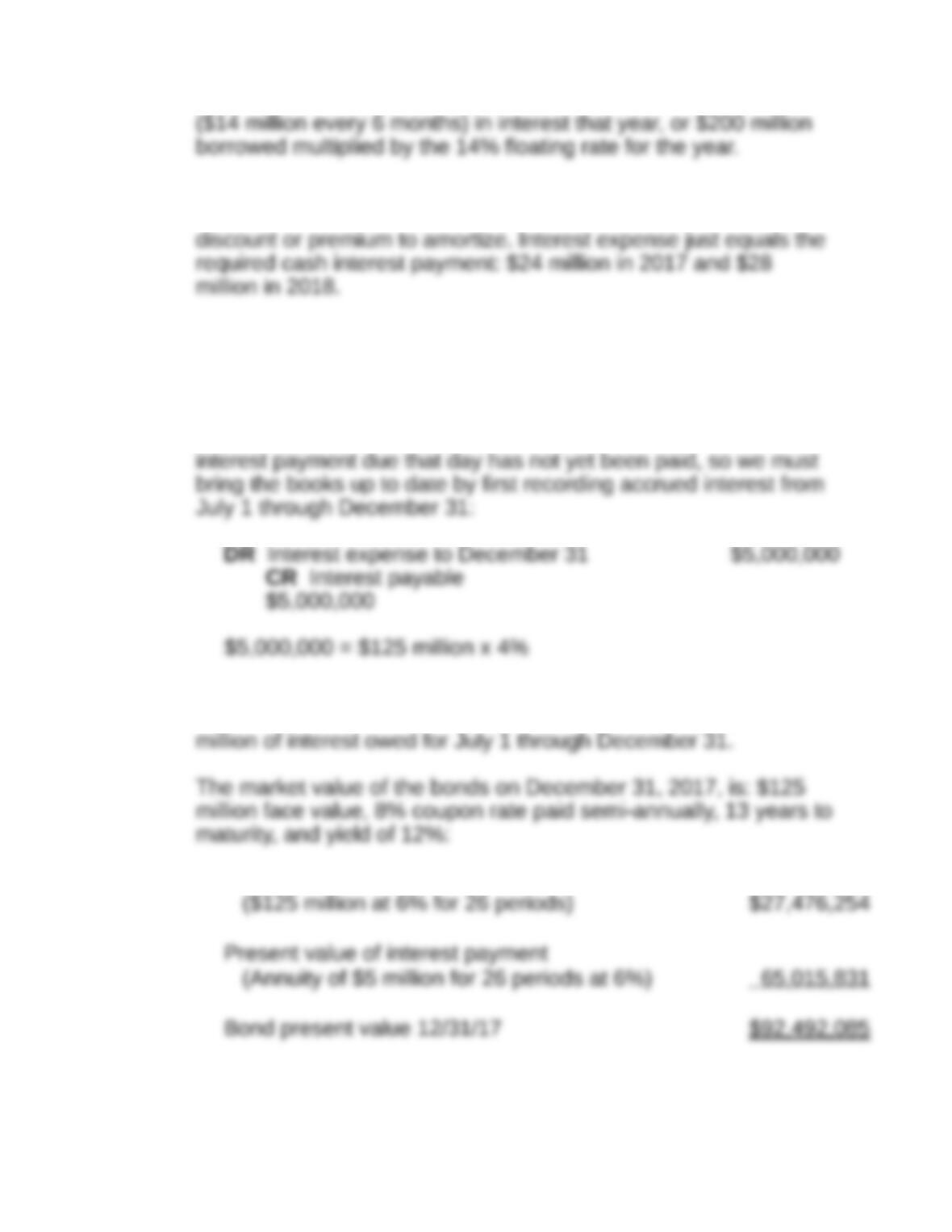

For 2018, the floating rate will be 14%, or a LIBOR rate of 8% plus

6% additional interest. So the company will pay out $28 million

Requirement 2:

The debentures were issued at par for $200 million, so there is no

E11-10. Identifying incentives for early debt retirement (LO 11-4)

Requirement 1:

We must first determine the book value of the bonds on December

31, 2017—almost two years after issuance. That would seem easy

because the bonds were issued at par, but there is a catch: The

The total book value (including Interest) of the debt on December

31, 2017, is $130 million, the $125 million borrowed plus the $5

Present value of principal

Plus the accrued interest of $5 million gives a total market value of

the bond equal to $97,492,085.

The entry to record the debt extinguishment is:

CR Taxes payable

$11,377,770

Requirement 2:

There are several reasons a company might want to retire debt

early: take advantage of lower interest rates; postpone scheduled

principal repayments; eliminate a conversion feature attached to

the debt; improve the company’s mix of debt and equity capital; or

E11-11. Early extinguishment of debt (LO 11-2, LO 11-4)

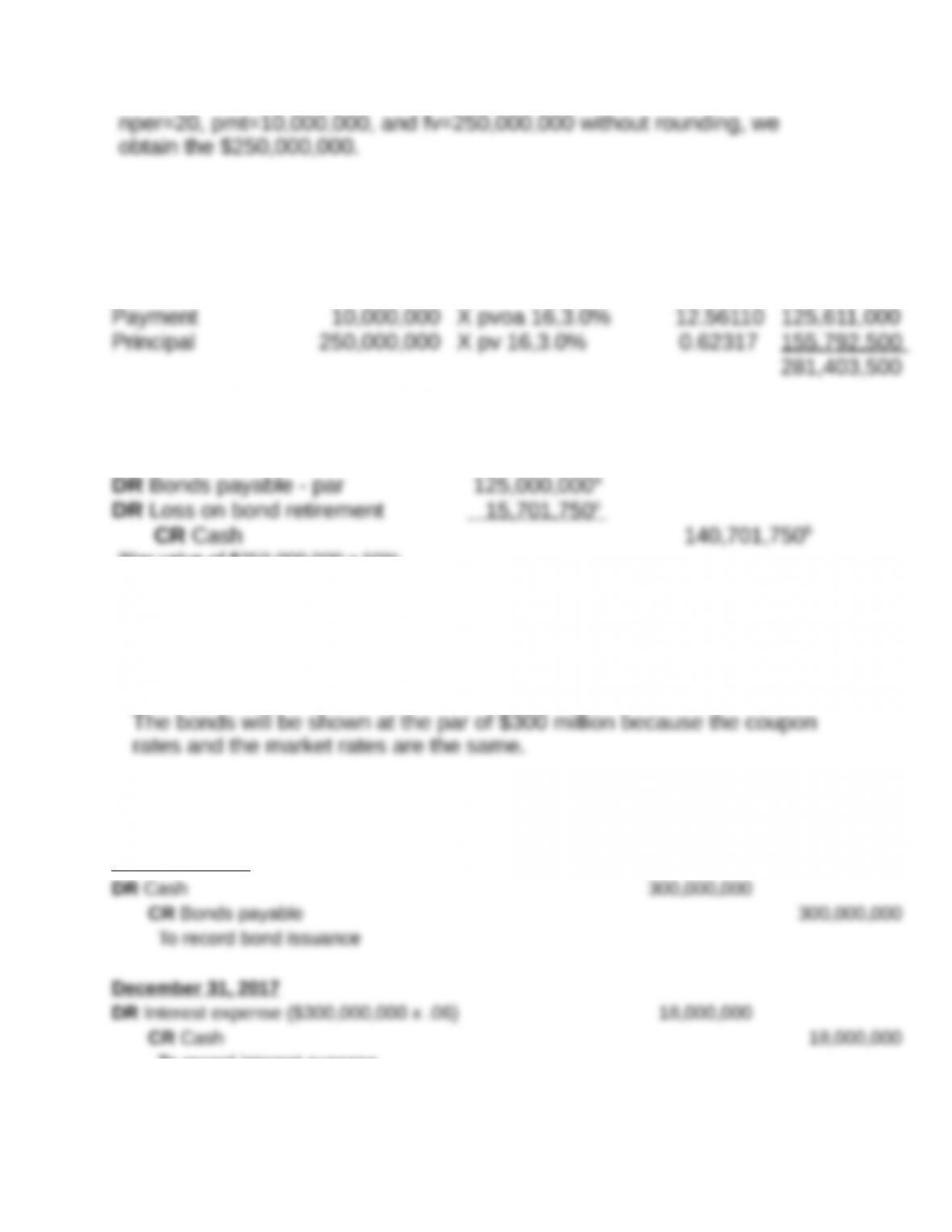

Requirement 1 – Issuance price

Because the coupon and market rates are equal, the bonds will sell for par

value, or $250,000,000. We can check this result by using present value

tables as follows.

*$10,000,000 = $250,000,000 par x 8%÷2.

The computed amount does not equal $250,000,000 because the present

Requirement 2 – Bond price at July 1, 2019

Remaining periods 16

Market rate 6%

Payments per year 2

Requirement 3 – Journal entry if 50% of the bonds are retired on July

1, 2019

aPar value of $250,000,000 x 50%.

bBond price of $281,403,500 x 50%.

cBonds payable of $125,000,000 less cash outflow of $140,701,750.

E11-12. Fair value option (LO 11-5)

Requirement 1: Book value on January 1, 2017

Requirement 2: Journal entries during 2017

January 1, 2017

To record interest expense

To record change in bond price

After the second journal entry, the bonds payable net of the adjustment will

reflect fair value. The interest expense and unrealized gain would probably

netted in one financing expense line item on the income statement.

*Price adjustment calculation

Remaining periods

9

Market rate 9%

Payments per year 1

Market value (tables)

246,043,500

Requirement 3 – Increase in interest rate and deteriorating financial condition

If the increase in interest rate were due to worsening financial health, the credit

E11-13. Noninterest-bearing loan (LO 11-3)

Requirement 1:

The present value of this payment stream, discounted at 9%, is:

Total present value of payment stream

$451,822

Requirement 2:

The purchase would be recorded at its implied cash price of

$451,822 as:

Interest expense at 9% per year on the unpaid balance would also be recorded over time.

Requirement 3:

McClelland should purchase from Agri-Products because it has

offered the best price.

E11-14. Understanding GAAP hedges (LO 11-8)

Requirement 1:

A “hedged item” can be (1) an existing asset or liability on the

company’s books, (2) a firm commitment, or (3) an anticipated

1. Manufacturer’s work-in-process inventory is an existing asset.

2. Credit card receivables are an existing asset at JC Penney.

Requirement 2:

The qualifying hedge instrument is most often a derivative security,

although not all derivatives meet the GAAP rules and some

qualifying hedges do not involve derivatives. Insurance contracts,

options to purchase real estate, equity and debt securities, and

Requirement 3:

Eligible risks for hedge accounting are those that arise from overall

changes in the fair value or cash flow of the hedged item, or from

(a) Alliant Energy’s risk that summer demand will exceed its

(b) Ford’s risk of steel price increases is an eligible risk of

(c) American Express’s risk that members won’t pay their bills is

(d) The risk of grain mold is not an eligible risk.